The property market in 2026 presents a unique paradox: homeowners with substantial equity refuse to lower prices, yet buyers struggle to afford even modest homes. With mortgage rates hovering above 6%[1] and only 21% of available homes affordable to middle-income buyers[4], property surveyors face unprecedented pressure to justify valuations in markets where traditional pricing models clash with economic reality. Understanding Affordability-Driven Valuation Challenges: How Surveyors Justify Property Values in Price-Sensitive Markets has become essential for professionals navigating this complex landscape.

As approximately one-third of properties reduce asking prices and affordability constraints persist across most metropolitan areas, surveyors must articulate clear, defensible rationale for their valuations. This comprehensive guide explores the methodologies, data sources, and communication strategies that enable surveyors to support their assessments while managing client expectations during challenging negotiations.

Key Takeaways

- Market fundamentals have shifted dramatically: Only 50% of U.S. metropolitan areas remain affordable when property taxes and insurance costs are factored in, requiring surveyors to incorporate comprehensive ownership cost analysis into valuations[3]

- Data-driven justification is non-negotiable: With home price growth slowing to just 1.3% annually, surveyors must leverage robust comparable sales data, adjustment factors, and regional performance metrics to defend valuations[1]

- Regional divergence demands localized expertise: Northeast and Midwest markets show resilience while Sunbelt regions face compounded pressures from insurance costs and oversupply, necessitating market-specific valuation approaches[1]

- Ownership costs now materially impact values: Rising reconstruction costs (up 6.6% year-over-year), insurance premiums, and property taxes must be integrated into valuation frameworks, not treated as afterthoughts[3]

- Clear communication prevents disputes: Transparent explanation of valuation methodology, market constraints, and price adjustment rationale helps manage client expectations and supports successful negotiations

Understanding the 2026 Affordability Crisis and Its Impact on Property Valuations

The Scope of the Affordability Challenge

The property market has undergone a dramatic transformation over the past decade. Markets where people can afford to buy homes plummeted 40% over ten years, declining from 354 metropolitan areas in 2014 to just 212 in 2025[3]. Even more striking, regions with high affordability (index 200+) shrunk from 41 markets to merely 4[3].

This affordability collapse fundamentally changes how surveyors approach valuation reports. Traditional valuation methods that focused primarily on comparable sales and property characteristics must now incorporate broader economic factors that directly impact a buyer's ability to purchase.

Key affordability metrics surveyors must track include:

- 📊 Median income-to-price ratios in the target market

- 💰 Mortgage payment affordability at current interest rates

- 🏠 Total ownership costs including insurance, taxes, and HOA fees

- 📈 Local wage growth versus property appreciation rates

- 🔍 Buyer demographic shifts and purchasing power trends

How Mortgage Rates Shape Valuation Parameters

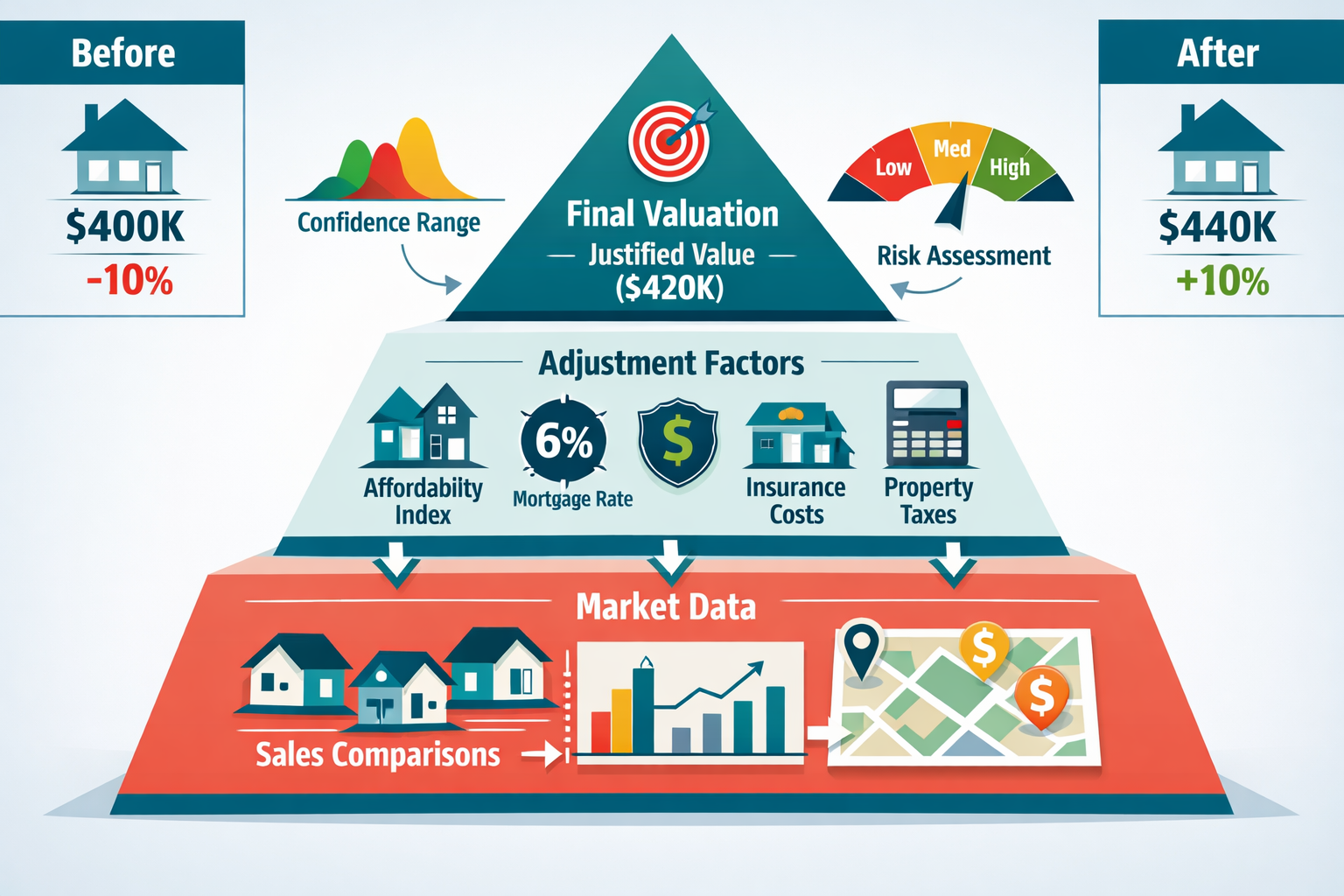

Mortgage rates are expected to remain above 6% for much of 2026, with a return to the 3-4% ranges considered "highly unlikely"[1]. This sustained high-rate environment constrains buyer purchasing power significantly, creating a ceiling effect on property values regardless of seller expectations.

For surveyors, this means recalibrating valuation approaches to reflect payment affordability rather than simply price comparisons. A property that would have been valued at £500,000 when rates were 3% may need adjustment when the same monthly payment at 6% rates supports only a £400,000 purchase price.

Understanding valuation factors in this context requires sophisticated financial modeling that accounts for:

| Factor | Impact on Valuation | Adjustment Consideration |

|---|---|---|

| Mortgage Rate Environment | Direct impact on buyer purchasing power | -10% to -15% value adjustment from peak rates |

| Insurance Premium Increases | Reduces affordability in high-risk areas | -3% to -8% in Florida, Texas, Louisiana markets |

| Property Tax Escalation | Ongoing ownership cost burden | -2% to -5% depending on jurisdiction |

| HOA Fee Trends | Monthly payment impact | -1% to -3% in communities with rising fees |

Regional Disparities in Affordability Pressures

Not all markets face identical affordability challenges. Northeast and Midwest markets demonstrate greater resilience with more moderate pandemic-era price appreciation, contrasting sharply with Sunbelt weakness in Florida, Texas, and other pandemic-boom regions[1].

Soft markets in Florida, Texas, and Louisiana face compounded ownership pressures from insurance premiums, property taxes, and HOA fees, alongside new construction inventory, placing significant downward pressure on values[1]. Surveyors working in these regions must account for these localized factors when justifying valuations.

"The divergence between regional markets means surveyors can no longer apply national trends uniformly. A property in the Midwest may maintain value while a comparable property in Florida faces 15-20% downward pressure from insurance costs alone." – Market Analysis Expert

Affordability-Driven Valuation Challenges: Methodologies for Supporting Property Values with Market Data

Building a Robust Comparable Sales Database

The foundation of any defensible valuation in price-sensitive markets is a comprehensive comparable sales database. However, in 2026's challenging environment, surveyors must go beyond traditional comparable selection criteria.

Essential elements of a robust comparables database include:

- Recent transactions (ideally within 3-6 months in volatile markets)

- Adjustment documentation showing how each comparable differs from the subject property

- Days on market trends indicating pricing accuracy and market acceptance

- Price reduction history revealing seller capitulation patterns

- Financing terms identifying cash sales versus financed purchases

- Buyer demographics understanding who can actually purchase in the market

When working with commercial property valuations, the comparable selection becomes even more critical as transaction volumes are lower and each sale carries more weight in the analysis.

Quantifying and Explaining Market Adjustments

In price-sensitive markets, transparency in adjustment methodology separates credible valuations from speculative assessments. Surveyors must clearly articulate why adjustments are made and how they're calculated.

Common adjustments in affordability-constrained markets:

- ✅ Location premium/discount (5-15% based on school districts, amenities, employment access)

- ✅ Condition adjustments (10-25% for properties requiring significant updates)

- ✅ Size and layout modifications (£150-300 per square foot in premium markets)

- ✅ Market conditions trending (0.5-1.5% monthly adjustment in declining markets)

- ✅ Financing concessions (2-5% for seller-paid closing costs or rate buydowns)

The key is documenting the data source and rationale for each adjustment. For example, rather than stating "10% adjustment for superior location," a defensible approach would be: "10% adjustment based on analysis of 15 comparable sales showing consistent 8-12% premium for properties within the Riverside school catchment area over the past 12 months."

Incorporating Ownership Cost Analysis

With residential reconstruction costs increasing 6.6% year-over-year[3]—more than twice the rate of general inflation—surveyors must integrate total ownership cost analysis into their valuation frameworks. This is particularly crucial for insurance reinstatement valuations where coverage gaps can materially impact property values.

Ownership cost components affecting valuations:

💷 Insurance premiums: In high-risk areas, annual premiums can exceed £5,000-10,000, effectively reducing the property value by £50,000-100,000 when capitalized at typical rates

💷 Property taxes: Jurisdictions with rising tax assessments create ongoing affordability burdens that buyers factor into their maximum purchase price

💷 HOA/service charges: Communities with escalating fees (particularly those with deferred maintenance) face value discounts of 5-15%

💷 Utility and maintenance costs: Older properties with inefficient systems carry hidden ownership costs that sophisticated buyers recognize

Leveraging Regional Performance Data

National trends provide context, but regional and hyper-local data drive accurate valuations. With national price growth forecast at just 1.3% over the next 12 months[1], understanding which markets outperform or underperform this average becomes critical.

Surveyors should maintain databases tracking:

- Absorption rates by price point and property type

- Inventory levels and months of supply trends

- New construction activity and its impact on existing home values

- Employment and wage growth in the local market

- Migration patterns (in-migration supporting values vs. out-migration pressuring prices)

For surveyors working across multiple regions—from North West London to South West London—maintaining separate performance metrics for each micro-market ensures valuations reflect true local conditions rather than broad regional averages.

Communicating Valuation Rationale in Affordability-Driven Valuation Challenges: Managing Client Expectations

Structuring the Valuation Report for Maximum Clarity

A well-structured valuation report serves dual purposes: providing defensible analysis and educating clients about market realities. In price-sensitive markets where seller expectations often exceed buyer capacity, clear communication prevents disputes and facilitates realistic negotiations.

Essential components of an effective valuation report:

- Executive Summary: Concise statement of value with key supporting factors

- Market Context Section: Current affordability metrics, mortgage rate environment, and regional trends

- Methodology Explanation: Transparent description of valuation approach and data sources

- Comparable Sales Analysis: Detailed grid with adjustments and explanations

- Risk Factors: Honest assessment of market uncertainties and value volatility

- Supporting Documentation: Charts, graphs, and market data visualizations

The best London property valuation guides emphasize that visual elements—charts showing price trends, maps highlighting comparable locations, and tables organizing adjustment factors—significantly improve client comprehension and acceptance.

Addressing the Price Reduction Phenomenon

With approximately one-third of properties reducing asking prices in 2026, surveyors must help clients understand why initial valuations may differ from eventual sale prices. This requires diplomatic but honest communication about market realities.

Effective strategies for discussing price reductions:

🔹 Present historical data: Show how properties initially listed above market value experienced extended days on market and eventual price cuts

🔹 Quantify carrying costs: Calculate the financial impact of overpricing (mortgage payments, insurance, maintenance) during extended listing periods

🔹 Demonstrate buyer behavior: Share data on how buyers in the current market respond to properties at different price points relative to comparables

🔹 Explain the "chasing the market down" risk: Illustrate how sequential price reductions often result in lower final sales prices than realistic initial pricing

Managing Seller Expectations in Equity-Rich Markets

A unique challenge in 2026 is the seller pullback phenomenon: homeowners with substantial equity and low mortgage rates are pulling listings rather than accepting price cuts[1][5]. This behavior limits inventory and prevents natural price corrections, creating tension between what sellers want and what buyers can afford.

Surveyors must navigate this delicate situation by:

- Acknowledging the seller's position: Recognize their equity and low carrying costs

- Presenting opportunity cost analysis: Calculate the value of selling now versus waiting 12-24 months in a flat or declining market

- Offering scenario planning: Provide valuations under different market conditions (optimistic, realistic, pessimistic)

- Highlighting buyer constraints: Explain that even qualified buyers face affordability limits regardless of property quality

For RICS valuation services, maintaining professional standards while delivering unwelcome news requires balancing empathy with analytical rigor.

Negotiation Support and Value Justification

Surveyors increasingly find themselves supporting clients through negotiations where buyers challenge valuations based on affordability constraints. Effective negotiation support requires:

Pre-negotiation preparation:

- Anticipate likely buyer objections (high ownership costs, comparable sales, market trends)

- Prepare response documentation with supporting data

- Identify areas of potential compromise versus non-negotiable value components

During negotiations:

- Provide real-time market data to counter unrealistic buyer positions

- Suggest creative solutions (seller financing, rate buydowns, repair credits) that bridge value gaps

- Maintain objectivity while advocating for defensible valuations

Post-negotiation analysis:

- Document lessons learned for future valuations

- Track whether negotiated prices align with or deviate from initial valuations

- Adjust methodologies based on market feedback

The Role of Technology and Data Analytics in Modern Valuations

Automated Valuation Models (AVMs) and Their Limitations

While technology has advanced significantly, Affordability-Driven Valuation Challenges: How Surveyors Justify Property Values in Price-Sensitive Markets require human expertise that AVMs cannot replicate. Automated models struggle with:

- Rapid market shifts: AVMs rely on historical data and lag current market conditions

- Unique property characteristics: Algorithm-based models poorly account for distinctive features

- Localized affordability factors: Insurance costs, property taxes, and HOA fees vary dramatically even within zip codes

- Market psychology: Seller reluctance and buyer constraints create pricing dynamics beyond statistical modeling

Surveyors should use AVMs as starting points rather than final determinations, applying professional judgment to adjust for factors automated systems miss.

Leveraging Market Intelligence Platforms

Professional surveyors in 2026 increasingly rely on sophisticated market intelligence platforms that aggregate:

- Real-time listing data with price reduction tracking

- Mortgage rate impacts on purchasing power

- Insurance premium trends by location

- Property tax assessment changes

- Demographic and employment data

These platforms enable surveyors to provide clients with data-driven insights that justify valuations with empirical evidence rather than subjective opinion.

Geographic Information Systems (GIS) for Micro-Market Analysis

GIS technology allows surveyors to visualize and analyze spatial patterns affecting property values:

- Heat maps showing price per square foot variations across neighborhoods

- Proximity analysis quantifying value impacts of amenities, schools, and employment centers

- Risk zone mapping for flood, fire, and other hazards affecting insurance costs

- Development pipeline tracking identifying new construction that may pressure existing home values

For surveyors covering diverse areas—from Central London to Berkshire—GIS tools provide consistent analytical frameworks across varied markets.

Specialized Valuation Scenarios in Affordability-Constrained Markets

Matrimonial and Probate Valuations

Matrimonial valuations and probate valuations present unique challenges in price-sensitive markets. These valuations often occur under compressed timelines with parties holding conflicting interests.

Key considerations:

- Date of valuation significance: Market conditions may have shifted significantly between the relevant date and current conditions

- Forced sale scenarios: Probate sales may require discounts reflecting urgency and "as-is" condition

- Partition disputes: Fair market value may differ from achievable sale price in distressed circumstances

- Tax implications: Valuation methodology may need adjustment based on tax treatment requirements

Shared Ownership and Leasehold Valuations

Shared ownership valuations and freehold valuations require specialized knowledge of how affordability constraints affect these unique property types.

Shared ownership properties face compounded affordability challenges:

- Rent payments on the unowned portion reduce borrowing capacity

- Staircasing opportunities depend on revaluation, creating uncertainty

- Resale markets are narrower, limiting buyer pools

- Service charges and ground rent add to ownership costs

Leasehold properties with short remaining terms face severe value impacts in affordability-constrained markets, as buyers struggle to secure financing and factor in lease extension costs.

Commercial Property Considerations

While this article focuses primarily on residential markets, commercial property surveyors face parallel affordability-driven challenges:

- Tenant affordability: Rising operating costs affect lease renewal rates and tenant quality

- Financing constraints: Higher interest rates impact capitalization rates and investor returns

- Alternative use potential: Residential conversion opportunities may exceed commercial valuations in some markets

- Economic uncertainty: Recession risks and employment trends affect demand fundamentals

Regulatory Compliance and Professional Standards

RICS Red Book Requirements

Surveyors must ensure their valuation approaches comply with RICS Red Book standards, which require:

- Competence: Surveyors must possess adequate knowledge of the market and property type

- Independence: Valuations must be objective and free from conflicts of interest

- Transparency: Methodology, assumptions, and limitations must be clearly stated

- Market value definition: Valuations must reflect "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction"

The Red Book valuation framework provides essential guidance for navigating affordability-driven challenges while maintaining professional standards.

Documentation and Liability Protection

In price-sensitive markets where valuations may be challenged, comprehensive documentation protects surveyors from liability claims:

✔️ Inspection notes: Detailed property condition observations

✔️ Comparable selection rationale: Why specific comparables were chosen and others excluded

✔️ Adjustment calculations: Mathematical basis for all value adjustments

✔️ Market data sources: Citations for market trends, statistics, and forecasts

✔️ Assumptions and limiting conditions: Clear statement of valuation parameters

✔️ Date of valuation: Explicit acknowledgment that values change over time

Continuing Professional Development

The rapidly evolving market conditions in 2026 require surveyors to maintain current knowledge through:

- Regular review of market research and forecasts

- Participation in professional development courses on valuation methodology

- Engagement with industry publications and thought leadership

- Networking with peers to understand market trends across regions

- Technology training on new analytical tools and platforms

Future Outlook: Preparing for Evolving Market Conditions

Projected Market Recovery Patterns

Housing supply and sales activity are projected to improve slightly from 2025 levels, keeping price appreciation gains modest through 2026[1]. However, the path to recovery remains uncertain with several potential scenarios:

Optimistic scenario: Mortgage rates decline to 5-5.5%, improving affordability and stimulating demand, leading to 3-4% annual appreciation

Base case scenario: Rates remain at 6%+, affordability constraints persist, resulting in 1-2% appreciation with significant regional variation

Pessimistic scenario: Economic recession reduces employment and income, pushing prices down 5-10% in overheated markets

Surveyors must prepare clients for all scenarios rather than presenting single-point forecasts as certainties.

Structural Changes Affecting Long-Term Valuations

Several structural market changes will influence valuations beyond 2026:

🏗️ Housing deficit persistence: A structural housing shortage remains despite affordability challenges, providing long-term price support[4]

🌡️ Climate risk integration: Insurance costs and climate hazards will increasingly factor into valuations, particularly in coastal and fire-prone areas

👥 Demographic shifts: Aging populations, remote work trends, and migration patterns will reshape demand across regions

🏛️ Policy interventions: Government programs addressing affordability may alter market dynamics through subsidies, zoning changes, or tax incentives

Adapting Valuation Practices for Resilience

Forward-thinking surveyors are adapting their practices to remain relevant in evolving markets:

- Expanding service offerings: Adding market feasibility studies, highest-and-best-use analysis, and investment advisory services

- Developing niche expertise: Specializing in complex property types, distressed markets, or specific geographic areas

- Enhancing client communication: Providing educational content and market updates that position surveyors as trusted advisors

- Investing in technology: Adopting advanced analytics, visualization tools, and data platforms

- Building strategic partnerships: Collaborating with mortgage brokers, financial planners, and real estate professionals

Conclusion

Affordability-Driven Valuation Challenges: How Surveyors Justify Property Values in Price-Sensitive Markets represents one of the most significant professional challenges facing property surveyors in 2026. With mortgage rates above 6%, middle-income buyers affording only 21% of available homes, and ownership costs rising faster than general inflation, traditional valuation approaches require substantial adaptation.

Success in this environment demands:

- Robust data analysis leveraging comprehensive comparable sales databases, regional performance metrics, and ownership cost integration

- Transparent communication that educates clients about market realities while maintaining professional credibility

- Methodological rigor that withstands scrutiny from skeptical buyers, lenders, and other stakeholders

- Technological adoption that enhances analytical capabilities while recognizing the irreplaceable value of human expertise

- Continuous learning that keeps pace with rapidly evolving market conditions and regulatory requirements

The surveyors who thrive in 2026 and beyond will be those who embrace these challenges as opportunities to demonstrate their value. By providing clear, defensible valuations supported by empirical data and communicated with empathy and professionalism, surveyors can guide clients through difficult markets while maintaining the integrity of the profession.

Actionable Next Steps

For surveyors seeking to enhance their practice in affordability-constrained markets:

- Audit your current methodology: Review recent valuations to identify areas where affordability factors could be better integrated

- Expand your data sources: Invest in market intelligence platforms that provide real-time affordability metrics and ownership cost data

- Enhance report templates: Revise valuation reports to include dedicated sections on market affordability and ownership cost analysis

- Develop client education materials: Create guides explaining current market conditions and valuation challenges

- Seek specialized training: Pursue professional development focused on complex valuation scenarios and emerging market trends

- Build referral networks: Establish relationships with mortgage advisors, financial planners, and legal professionals who can provide complementary expertise

The property market of 2026 may be challenging, but it also presents opportunities for surveyors who adapt their practices to meet evolving client needs. By combining analytical rigor with clear communication and genuine client advocacy, surveyors can successfully navigate Affordability-Driven Valuation Challenges: How Surveyors Justify Property Values in Price-Sensitive Markets while building stronger, more resilient practices.

For expert assistance with complex valuations in today's challenging market, consider consulting with experienced professionals who understand the nuances of valuation in London and surrounding regions. Whether you need residential, commercial, or specialized valuation services, working with qualified surveyors ensures you receive defensible, market-appropriate assessments that withstand scrutiny and support successful transactions.

References

[1] Veroforecast Signals Slower Home Price Growth In 2026 As Affordability Constraints Persist – https://www.veros.com/veroforecast-signals-slower-home-price-growth-in-2026-as-affordability-constraints-persist

[2] 2026 Valuation Advisory North American Market Survey – https://www.nmrk.com/insights/market-report/2026-valuation-advisory-north-american-market-survey

[3] 10 Things To Know About The Property Market January 2026 – https://www.cotality.com/press-releases/10-things-to-know-about-the-property-market-january-2026

[4] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[5] Housing Market Predictions 2026 – https://www.redfin.com/news/housing-market-predictions-2026/

[6] 2026 Commercial Real Estate Outlook Stabilization Selectivity And A Market That Rewards Precision – https://bbgres.com/2026-commercial-real-estate-outlook-stabilization-selectivity-and-a-market-that-rewards-precision/

[7] Emerging Trends In Real Estate Pwc Uli – https://www.pwc.com/us/en/industries/financial-services/asset-wealth-management/real-estate/emerging-trends-in-real-estate-pwc-uli.html

[8] Expert Forecasts Point To Affordability Improving In 2026 – https://thekeystoneteam.com/blog/expert-forecasts-point-to-affordability-improving-in-2026