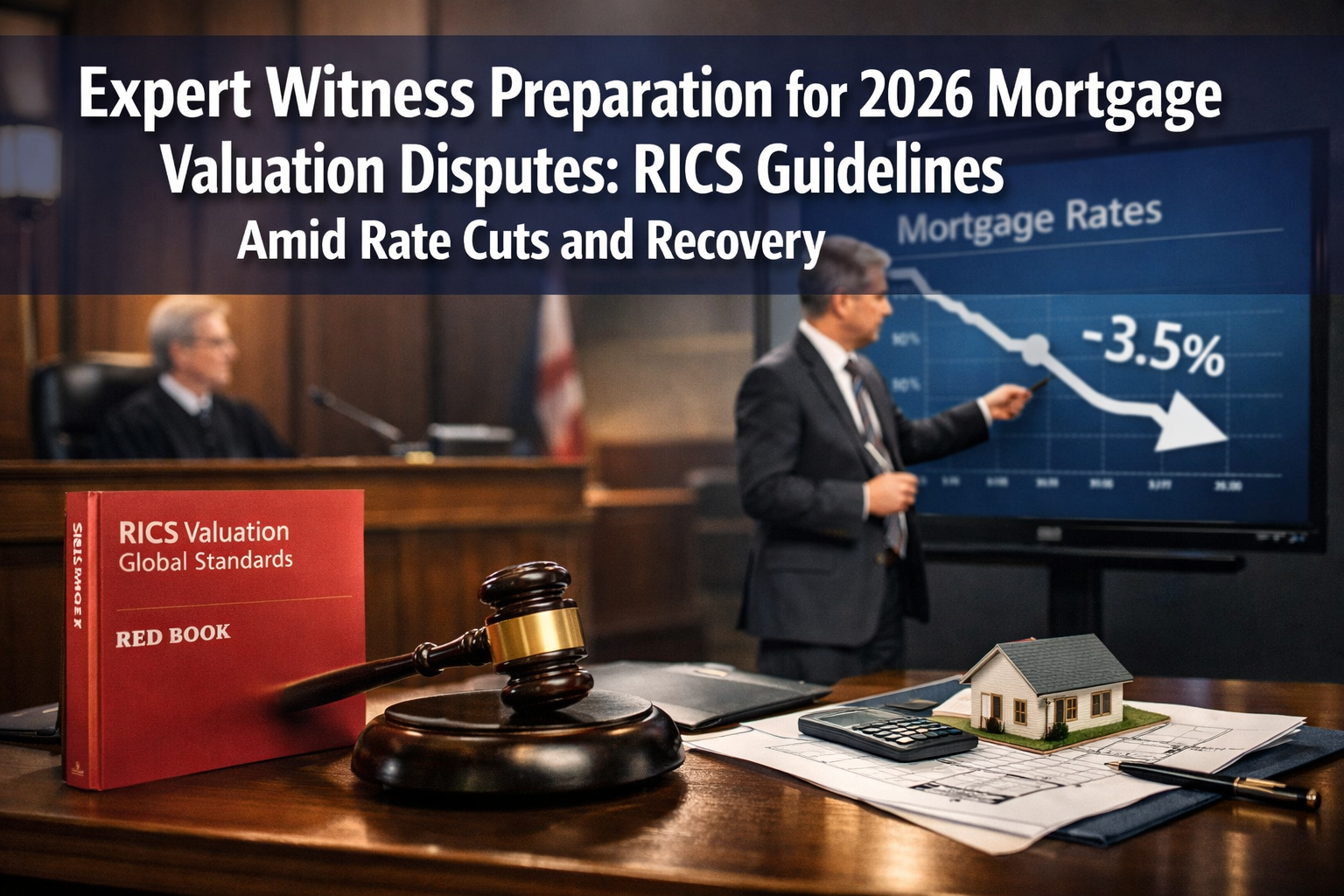

As mortgage rates tumble to 3.5% in 2026, the UK property market is experiencing a resurgence of buyer activity and, inevitably, a corresponding rise in valuation disputes. Lenders, borrowers, and investors are challenging property assessments with renewed vigor as market conditions stabilize following years of volatility. For chartered surveyors serving as expert witnesses in these contentious cases, the stakes have never been higher—or the professional standards more demanding.

Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery represents a critical intersection of evolving regulatory frameworks, enhanced professional obligations, and dynamic market conditions. With the Royal Institution of Chartered Surveyors (RICS) implementing major updates to both its Bank Lending Valuations Standard and its Expert Witness Standard, professionals must navigate a transformed landscape of evidence gathering, testimony preparation, and valuation defense strategies.

This comprehensive guide explores the essential elements of expert witness preparation in the current environment, examining how the latest RICS guidelines, Basel 3.1 requirements, and market recovery dynamics shape professional practice in 2026.

Key Takeaways

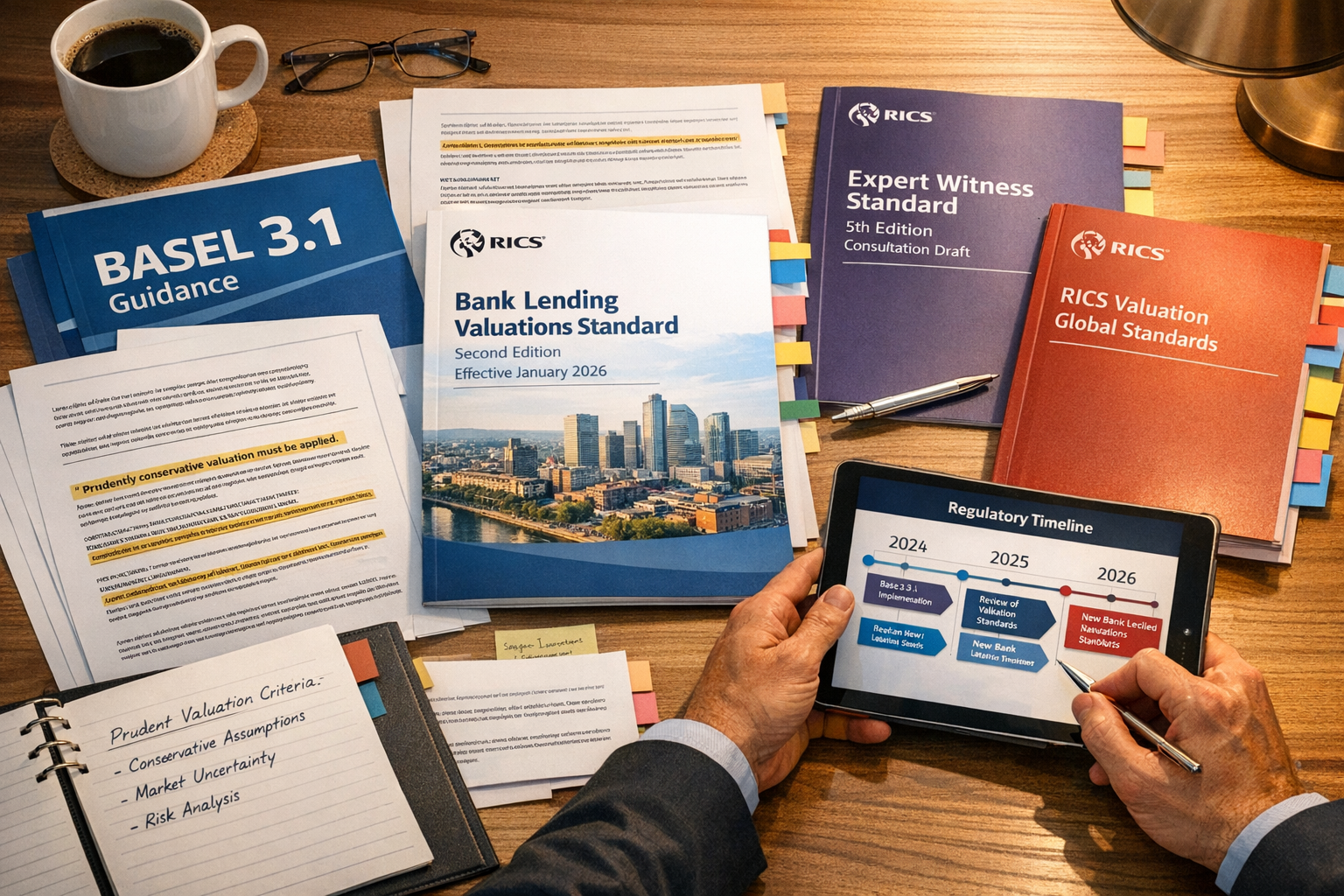

✅ New RICS Standards in Force: The second edition of the Bank Lending Valuations Standard became mandatory on January 1, 2026, introducing Basel 3.1 "prudently conservative valuation criteria" that fundamentally alter how mortgage valuations are conducted and defended in disputes.[2]

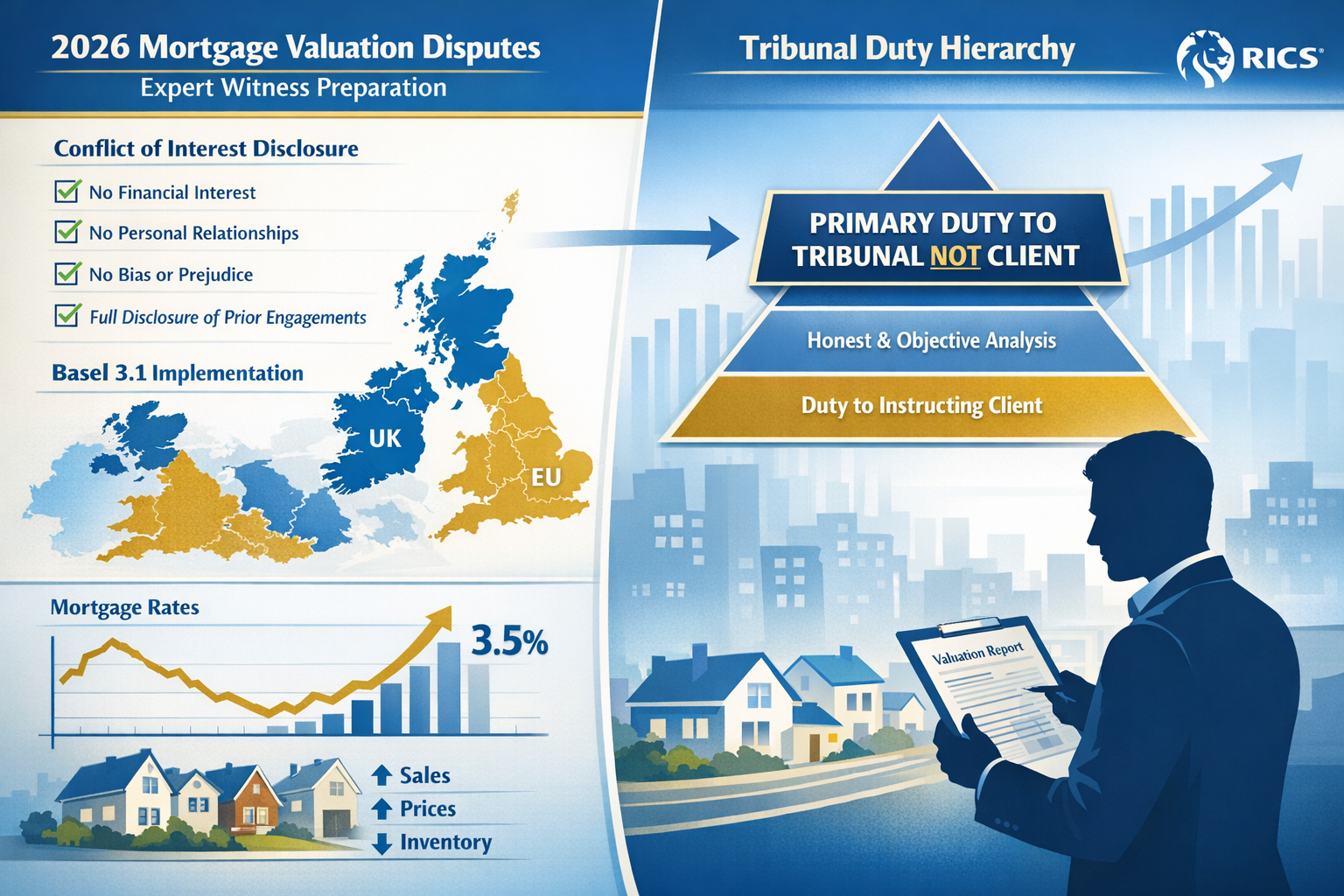

✅ Enhanced Expert Witness Obligations: The 5th edition of RICS' "Surveyors acting as expert witnesses" standard (consultation launched August 2025) reinforces that the primary duty is to the tribunal, not the client, with stricter conflict of interest disclosure requirements.[1]

✅ Jurisdiction-Specific Implementation Required: Expert witnesses must identify how their specific jurisdiction has implemented Basel 3.1 guidance before accepting valuation instructions, adding complexity to pre-case preparation.[2]

✅ Market Recovery Context Matters: With mortgage rates at 3.5% driving increased buyer enquiries, valuation disputes are rising as lenders and borrowers contest assessments in stabilizing but still uncertain market conditions.

✅ Professional Independence is Paramount: Updated fee guidance, template usage protocols, and risk mitigation strategies protect professional independence while managing high-volume mortgage valuation cases.[1]

Understanding the 2026 Regulatory Landscape for Expert Witness Preparation

The Bank Lending Valuations Standard: Second Edition

The Bank Lending Valuations Standard (second edition) became mandatory for RICS members on January 1, 2026, marking a watershed moment for expert witness preparation in mortgage valuation disputes.[2] This professional standard applies to all valuation services provided for bank lending purposes in or subject to EU jurisdictions, creating a unified framework that expert witnesses must reference when defending their assessments.

The standard incorporates Basel 3.1 guidance and the EU's Capital Requirements Regulation (CRR III), introducing "prudently conservative valuation criteria" that fundamentally change the evidentiary foundation of mortgage valuations.[2] These criteria require valuers to apply conservative adjustments that account for:

- Market volatility and uncertainty 📊

- Liquidity constraints in specific property segments

- Long-term sustainable value rather than peak market conditions

- Regulatory capital requirements for lending institutions

For expert witnesses, understanding these criteria is essential when preparing testimony. Disputes often center on whether a valuation properly applied prudently conservative principles or whether excessive caution undervalued a property, potentially costing a borrower favorable lending terms.

Basel 3.1 Implementation Across Jurisdictions

A critical challenge for expert witness preparation in 2026 is the variable implementation of Basel 3.1 across jurisdictions.[2] While the RICS standard provides global guidance, individual countries and regulatory bodies have adopted Basel 3.1 requirements with jurisdiction-specific modifications.

RICS has published a new global practice information document titled "Bank lending valuations: Basel 3.1 prudently conservative valuation criteria adjustments, 1st edition" to assist members and regulators in understanding these variations.[2] Expert witnesses must:

- Identify the specific jurisdiction where the disputed valuation was conducted

- Research local implementation of Basel 3.1 requirements

- Document regulatory context in expert reports

- Explain jurisdiction-specific adjustments clearly to tribunals

This jurisdictional complexity means that expert witness preparation cannot follow a one-size-fits-all approach. A valuation conducted in London may apply different prudently conservative criteria than one in Frankfurt or Dublin, even when both reference the same RICS standard.

The Expert Witness Standard: Fifth Edition Updates

On August 26, 2025, RICS launched a public consultation for the 5th edition of its "Surveyors acting as expert witnesses" standard—the first major update since 2014.[1] This comprehensive revision reflects years of collaborative development with technical experts and addresses emerging challenges in expert witness practice.

The updated standard reinforces several fundamental principles that apply to Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery:

Primary Duty to the Tribunal 🏛️

The standard explicitly states that the primary duty of expert witnesses is to the tribunal, not the client.[1] All reports and evidence must be independent, unbiased, and within the surveyor's true area of expertise. This principle applies globally despite local legal differences.

In practical terms, this means expert witnesses must:

- Resist client pressure to modify opinions

- Present balanced evidence that acknowledges weaknesses

- Clearly delineate facts from professional opinion

- Maintain objectivity even when retained by one party

Enhanced Conflict of Interest Disclosure

The 5th edition includes clearer requirements for identifying and disclosing conflicts of interest, with explicit explanation of legal consequences for non-compliance.[1] For mortgage valuation disputes, potential conflicts include:

- Previous valuation work for the same property

- Ongoing relationships with the lender or borrower

- Financial interests in comparable properties

- Professional relationships that could bias judgment

Expert witnesses must conduct thorough conflict checks before accepting instructions and maintain detailed records of the disclosure process. For more information on professional standards, see our guide to RICS valuation costs.

Fee Guidance and Professional Independence

The updated standard provides clear guidance on conditional and deferred fees while protecting professional independence.[1] In high-volume mortgage valuation cases, fee arrangements can create subtle pressures that compromise objectivity.

The standard clarifies that:

- Fees should not be contingent on case outcomes

- Payment terms must not influence professional opinions

- Template usage must be disclosed and appropriate

- Risk mitigation strategies should protect professional judgment

Preparing Expert Evidence in the 2026 Market Recovery Context

Understanding Current Market Dynamics

The 3.5% mortgage rate environment of 2026 represents a significant shift from the higher-rate period of 2022-2024. This recovery has triggered increased buyer enquiries and transaction volumes, but also heightened disputes as market participants contest valuations in a stabilizing but still uncertain environment.

Expert witnesses must contextualize their valuations within this recovery framework by addressing:

Market Velocity and Comparables 🏘️

With transaction volumes increasing, the availability of comparable sales has improved, but quality varies. Expert reports must explain:

- Time adjustments for comparables from different market phases

- The reliability of recent transactions versus historical data

- How market momentum affects valuation confidence

- The distinction between asking prices and achieved prices

Regional Divergence

The 2026 market recovery is not uniform across the UK. London and the Southeast are experiencing different dynamics than Northern regions, requiring expert witnesses to demonstrate deep local market knowledge. Our analysis of expert witness roles in Northern property disputes provides additional context on regional variations.

Lender Risk Appetite

As rates fall, lender risk appetite is evolving. Some institutions are relaxing loan-to-value ratios while others remain cautious. Expert witnesses must understand how lender-specific policies interact with Basel 3.1 prudently conservative requirements when defending valuations.

Evidence Gathering for Mortgage Valuation Disputes

Effective Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery requires systematic evidence gathering that anticipates challenge points and builds a defensible foundation.

Documentary Evidence Foundation 📄

A robust expert report begins with comprehensive documentation:

| Evidence Type | Purpose | Key Considerations |

|---|---|---|

| Original valuation report | Establish baseline assessment | Review methodology, assumptions, limitations |

| Comparable sales data | Support market value opinion | Verify transactions, adjust for differences |

| Market analysis reports | Contextualize valuation date conditions | Source credibility, data recency |

| Regulatory guidance | Demonstrate compliance | RICS standards, Basel 3.1, local requirements |

| Correspondence records | Show professional process | Instructions, clarifications, disclosures |

| Site inspection records | Evidence physical inspection | Photos, measurements, condition notes |

Methodology Documentation

Expert witnesses must clearly document their valuation methodology, particularly when applying Basel 3.1 prudently conservative criteria. This includes:

- Valuation approach selection (comparative, income, cost)

- Adjustment calculations with supporting rationale

- Assumption testing and sensitivity analysis

- Limitation acknowledgment and impact assessment

The RICS Red Book – Global Standards define specific valuation types (Market Value, Fair Value, Investment Value, Synergistic Value) that form the technical foundation for expert evidence.[3] Understanding these definitions and their application is essential for credible testimony. For comprehensive guidance, review our best London property valuation guide.

Site Inspection and Physical Evidence

Physical inspection evidence strengthens expert credibility. In mortgage valuation disputes, key inspection elements include:

- Property condition assessment with photographic evidence

- Measurement verification and floor plan accuracy

- Defect identification affecting value

- Comparable property inspections when feasible

- Neighborhood analysis and location factors

Many disputes arise from differing assessments of property condition or location quality. Detailed inspection records provide objective evidence that supports professional judgment.

Defending Valuations Against Lender Challenges

Lender challenges to mortgage valuations typically fall into several categories, each requiring specific defense strategies:

Challenge Type 1: Excessive Conservatism

Borrowers may argue that Basel 3.1 prudently conservative criteria were applied too aggressively, resulting in artificially low valuations that limited borrowing capacity.

Defense Strategy:

- Document specific Basel 3.1 adjustments with regulatory references

- Demonstrate jurisdiction-specific implementation requirements

- Show comparable valuations with similar adjustments

- Explain lender-specific risk policies if applicable

- Present market data supporting conservative approach

Challenge Type 2: Insufficient Market Analysis

Lenders may contest valuations that rely on limited comparable data or fail to account for market trends.

Defense Strategy:

- Present comprehensive comparable search methodology

- Explain time adjustments and market trend analysis

- Demonstrate local market expertise with transaction data

- Address regional divergence and micro-market factors

- Show sensitivity analysis for key assumptions

Challenge Type 3: Methodology Disputes

Parties may challenge the valuation approach or specific techniques used.

Defense Strategy:

- Reference RICS Red Book methodology requirements[3]

- Cite professional standards and guidance notes

- Explain approach selection rationale

- Present alternative methodology results for comparison

- Demonstrate consistency with market practice

For complex valuation disputes involving multiple properties or specialized assets, our valuation reports in London provide additional context on professional standards.

RICS Guidelines for Expert Witness Testimony and Report Preparation

Structuring Expert Reports for Maximum Impact

The structure of an expert report significantly influences its persuasive power and credibility. RICS guidelines emphasize clarity, logical organization, and transparent reasoning.[1]

Essential Report Components 📋

A comprehensive expert witness report for mortgage valuation disputes should include:

-

Executive Summary

- Concise overview of key opinions

- Clear statement of conclusions

- Summary of critical evidence

-

Expert Qualifications and Independence

- Professional credentials and experience

- Conflict of interest disclosure

- Statement of primary duty to tribunal

- Confirmation of independence

-

Instructions and Scope

- Detailed description of instructions received

- Scope of work undertaken

- Limitations and exclusions

- Documents reviewed

-

Factual Background

- Property description

- Transaction context

- Relevant market conditions

- Chronology of events

-

Methodology and Analysis

- Valuation approach explanation

- Basel 3.1 criteria application

- Comparable analysis

- Adjustment calculations

- Assumption testing

-

Professional Opinion

- Clear statement of conclusions

- Reasoning and supporting evidence

- Degree of confidence

- Alternative scenarios if appropriate

-

Supporting Documentation

- Appendices with data tables

- Comparable sales schedules

- Photographs and site plans

- Regulatory references

- Professional credentials

Writing for Tribunal Understanding

Expert witnesses must remember that tribunals, judges, and arbitrators may not have technical valuation expertise. The 5th edition RICS standard emphasizes the importance of accessible, clear communication.[1]

Plain Language Principles 💬

- Avoid jargon or define technical terms when first used

- Use active voice for clarity and directness

- Provide context for technical concepts

- Include visual aids (charts, graphs, tables) to illustrate complex data

- Structure logically with clear headings and numbered paragraphs

For example, rather than writing:

"The subject property's valuation reflects a prudently conservative adjustment factor of 15% applied to the comparative evidence base to account for market volatility parameters consistent with Basel 3.1 regulatory framework requirements."

Write:

"The property valuation includes a 15% downward adjustment to account for market uncertainty. This adjustment follows Basel 3.1 banking regulations, which require valuers to use conservative estimates that protect lenders from potential market declines."

Handling Cross-Examination and Oral Testimony

Preparation for cross-examination is a critical component of Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery. The updated RICS standard provides guidance on maintaining professional composure and credibility under questioning.[1]

Pre-Testimony Preparation Checklist ✅

- Review all written reports and supporting documents thoroughly

- Anticipate challenge points and prepare responses

- Practice explaining technical concepts in plain language

- Prepare visual aids for courtroom presentation

- Coordinate with instructing solicitors on procedural matters

- Review opposing expert reports and identify disagreements

- Refresh knowledge of current market conditions

- Confirm all factual statements and data sources

Cross-Examination Best Practices

During testimony, expert witnesses should:

- Listen carefully to questions and answer only what is asked

- Maintain composure even under aggressive questioning

- Acknowledge limitations and areas of uncertainty honestly

- Correct errors immediately if identified

- Avoid advocacy for the instructing party

- Defer to tribunal on legal or procedural matters

- Request clarification when questions are unclear

- Maintain professional demeanor throughout

Handling Disagreements with Opposing Experts

Professional disagreements between expert witnesses are common and expected. The RICS standard emphasizes that experts should:

- Clearly identify areas of agreement and disagreement

- Explain the basis for differing opinions professionally

- Avoid personal criticism of opposing experts

- Focus on methodology and evidence, not personalities

- Acknowledge valid points made by opposing experts

- Maintain respect for professional colleagues

For guidance on handling contentious disputes professionally, see our resources on construction disputes resolution.

Applying Prudently Conservative Valuation Criteria in Expert Reports

Understanding Basel 3.1 Requirements

The Basel 3.1 prudently conservative valuation criteria represent the most significant technical change affecting expert witness preparation in 2026.[2] These requirements fundamentally alter how mortgage valuations are conducted and defended.

Core Principles of Prudently Conservative Valuation 🏦

Basel 3.1 guidance requires valuations to:

- Reflect sustainable long-term value rather than peak market conditions

- Account for market volatility and potential downturns

- Consider liquidity constraints in specific property segments

- Apply conservative assumptions when data is limited or uncertain

- Protect lender capital adequacy through cautious assessments

Expert witnesses must demonstrate how these principles were applied in the original valuation and defend their application against challenges.

Documenting Conservative Adjustments

Transparency in adjustment methodology is essential for credible expert testimony. Each conservative adjustment should be documented with:

Adjustment Documentation Framework

| Adjustment Type | Documentation Required | Typical Range |

|---|---|---|

| Market volatility | Historical volatility data, market cycle analysis | 5-15% |

| Liquidity discount | Transaction volume data, days on market analysis | 3-10% |

| Property-specific risk | Condition reports, defect analysis, location factors | 2-20% |

| Market uncertainty | Economic forecasts, lending trend data | 5-12% |

| Regulatory buffer | Basel 3.1 guidance, lender-specific requirements | Variable |

Each adjustment must be supported by objective evidence and professional reasoning. Blanket adjustments without specific justification are vulnerable to challenge.

Case Study: Defending Conservative Adjustments in a 2026 Dispute

Scenario: A borrower challenges a £750,000 valuation of a London property, arguing that comparable sales support a £850,000 value. The valuer applied a 12% prudently conservative adjustment under Basel 3.1 guidance.

Expert Witness Defense Strategy:

- Present comparable analysis showing unadjusted market value of £850,000

- Document market volatility in the specific London micro-market over the previous 24 months

- Reference Basel 3.1 requirements for lending valuations with regulatory citations

- Show lender-specific policies requiring conservative adjustments

- Demonstrate jurisdiction-specific implementation of Basel 3.1 in the UK

- Present sensitivity analysis showing value range under different scenarios

- Explain professional judgment in selecting 12% adjustment within acceptable range

This approach demonstrates both technical competence and regulatory compliance, strengthening the expert's credibility.

For additional context on valuation factors that influence professional assessments, review our guide to valuation factors.

Managing Conflicts of Interest and Professional Independence

Enhanced Disclosure Requirements Under the 5th Edition Standard

The updated RICS expert witness standard includes significantly enhanced conflict of interest disclosure requirements.[1] These changes reflect growing recognition that even subtle conflicts can compromise professional independence and expert credibility.

Categories of Potential Conflicts ⚠️

Expert witnesses must identify and disclose:

-

Direct financial interests

- Ownership or investment in the subject property

- Financial relationships with parties to the dispute

- Fee arrangements that create outcome dependency

-

Professional relationships

- Ongoing work for the lender or borrower

- Previous valuation work on the same property

- Employment history with disputing parties

-

Personal relationships

- Family or social connections to parties

- Membership in organizations with relevant interests

- Reputational interests that could bias judgment

-

Indirect interests

- Ownership of comparable properties

- Business interests in the local market

- Professional advancement opportunities tied to case outcome

The Disclosure Process

The 5th edition standard requires a systematic disclosure process that documents:

- Initial conflict check upon receiving instructions

- Written disclosure to all parties and the tribunal

- Ongoing monitoring for emerging conflicts

- Updated disclosures if circumstances change

- Withdrawal procedures if conflicts cannot be managed

Disclosure Template Elements

A comprehensive conflict disclosure should include:

CONFLICT OF INTEREST DISCLOSURE

Expert Name: [Name]

Case Reference: [Reference]

Date: [Date]

I confirm that I have conducted a thorough review of potential conflicts of interest and disclose the following:

1. Direct Interests: [None / Details]

2. Professional Relationships: [None / Details]

3. Personal Relationships: [None / Details]

4. Indirect Interests: [None / Details]

5. Previous Work: [None / Details]

I confirm that [the disclosed interests do not compromise my independence / I have withdrawn from this instruction due to conflicts].

Signed: [Signature]

Date: [Date]

Legal Consequences of Non-Disclosure

The updated standard explicitly explains legal consequences for non-compliance with disclosure requirements.[1] These can include:

- Report exclusion from evidence

- Cost sanctions against the expert or instructing party

- Professional discipline by RICS

- Reputational damage affecting future instructions

- Civil liability in extreme cases

Expert witnesses must take disclosure obligations seriously, erring on the side of over-disclosure when uncertain about potential conflicts.

Fee Arrangements and Risk Mitigation in High-Volume Cases

Acceptable Fee Structures

The 5th edition RICS standard provides clear guidance on fee arrangements that protect professional independence while allowing flexible commercial arrangements.[1]

Acceptable Fee Models 💰

- Fixed fees for defined scope of work

- Hourly rates with estimated ranges

- Staged payments tied to work completion milestones

- Retainer arrangements for ongoing availability

Prohibited Fee Arrangements

- Contingency fees based on case outcomes

- Success bonuses tied to favorable results

- Percentage fees based on valuation amounts

- Deferred fees contingent on winning the case

Managing High-Volume Mortgage Valuation Work

The 2026 market recovery has generated increased volumes of mortgage valuation disputes, creating efficiency pressures that can compromise quality. The RICS standard addresses risk mitigation for high-volume work.[1]

Quality Control Measures

Expert witnesses handling multiple cases should implement:

- Case management systems to track deadlines and deliverables

- Template libraries with appropriate customization protocols

- Peer review processes for complex or high-value cases

- Time allocation standards ensuring adequate preparation

- Workload limits preventing over-commitment

Template Usage Protocols

While templates improve efficiency, the standard requires disclosure of template usage and confirmation that:

- Templates are appropriately customized for each case

- Standard language reflects current professional standards

- Case-specific analysis is genuinely independent

- Templates do not create "cookie-cutter" opinions

For professionals seeking expert surveyor advice on managing complex caseloads, see our expert surveyor advice resources.

Integration with Other Valuation Contexts and Dispute Types

Cross-Application to Related Dispute Types

Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery shares common elements with other valuation dispute contexts:

Matrimonial Valuations 💑

Divorce proceedings often require property valuations that become contentious. The same RICS standards apply, with additional considerations for:

- Date of valuation (separation vs. divorce decree)

- Forced sale scenarios vs. market value

- Emotional attachments affecting objectivity

- Tax implications of valuation conclusions

Our guide to matrimonial valuation provides specialized guidance for these cases.

Leasehold and Freehold Disputes

Valuation disputes in leasehold enfranchisement and freehold acquisition cases apply similar methodologies with specific statutory frameworks. Expert witnesses must understand:

- Statutory valuation assumptions under relevant legislation

- Hope value and marriage value calculations

- Relativity analysis and settlement patterns

- Tribunal precedents and case law

For detailed guidance, see our resources on freehold valuation in London.

Commercial Property Disputes

Commercial mortgage valuations involve additional complexity including:

- Income capitalization methodologies

- Lease covenant strength analysis

- Investment market yield assessment

- Specialized property type considerations

Our commercial property surveyors guide addresses these specialized contexts.

Housing Disrepair and Regulatory Overlap

RICS members acting as expert witnesses in housing disrepair claims—which often overlap with mortgage valuation disputes—must note evolving legislation including Awaab's Law (effective October 2025) and the Housing Health and Safety Rating System (HHSRS).[1]

When property condition affects mortgage valuations, expert witnesses should:

- Reference relevant health and safety legislation

- Document disrepair impact on value with evidence

- Distinguish between valuation opinion and building survey findings

- Coordinate with other experts (structural engineers, building surveyors)

- Explain regulatory compliance implications for lenders

Practical Preparation Checklists for 2026 Mortgage Valuation Disputes

Pre-Instruction Checklist

Before accepting expert witness instructions, complete these steps:

✅ Competence Assessment

- Confirm expertise in the specific property type and location

- Verify current knowledge of local market conditions

- Assess capacity to meet deadlines with quality work

- Review technical complexity against experience level

✅ Conflict Check

- Search internal records for previous work on the property

- Identify relationships with parties to the dispute

- Review financial interests in comparable properties

- Document disclosure decisions

✅ Regulatory Review

- Identify applicable jurisdiction for Basel 3.1 implementation

- Review current RICS standards and guidance notes

- Confirm professional indemnity insurance coverage

- Verify RICS membership status and CPD compliance

✅ Fee Agreement

- Negotiate acceptable fee structure

- Confirm payment terms and schedule

- Document scope of work and deliverables

- Establish variation procedures

Evidence Gathering Checklist

Once instructions are accepted, systematically gather:

✅ Primary Documents

- Original valuation report and supporting documents

- Property title information and legal descriptions

- Planning permissions and building regulation approvals

- Previous valuations and survey reports

- Correspondence related to the dispute

✅ Market Data

- Comparable sales transactions with full details

- Market analysis reports for the relevant period

- Economic data and lending statistics

- Regional market trend analysis

- Rental evidence if income approach is relevant

✅ Physical Evidence

- Site inspection photographs and videos

- Floor plans and measured surveys

- Defect reports and condition assessments

- Location and neighborhood analysis

- Comparable property inspections where feasible

✅ Regulatory Materials

- RICS Red Book standards applicable at valuation date[3]

- Basel 3.1 guidance and jurisdiction-specific implementation

- Lender-specific valuation policies if available

- Professional guidance notes and technical standards

- Relevant case law and tribunal decisions

Report Preparation Checklist

When drafting the expert report:

✅ Structure and Format

- Include all required report components

- Use clear headings and numbered paragraphs

- Provide table of contents for lengthy reports

- Ensure logical flow and organization

- Include executive summary

✅ Content Quality

- Write in plain language accessible to non-experts

- Define technical terms on first use

- Support all opinions with evidence

- Acknowledge limitations and uncertainties

- Address anticipated challenges

✅ Technical Accuracy

- Verify all factual statements and data

- Check calculations and adjustment factors

- Confirm regulatory citations and references

- Review comparable analysis for errors

- Test assumptions with sensitivity analysis

✅ Professional Standards

- Include independence statement and conflict disclosure

- Confirm primary duty to tribunal

- Acknowledge expert witness obligations

- Provide professional credentials

- Sign and date the report

✅ Supporting Materials

- Attach all referenced appendices

- Include photographic evidence

- Provide data tables and calculations

- Add comparable sales schedules

- Include regulatory reference documents

Pre-Testimony Preparation Checklist

Before giving oral evidence:

✅ Document Review

- Re-read all expert reports thoroughly

- Review opposing expert reports and identify disagreements

- Refresh knowledge of supporting documents

- Update market knowledge if significant time has passed

- Prepare responses to anticipated challenges

✅ Practical Preparation

- Coordinate with instructing solicitors on procedures

- Prepare visual aids for courtroom presentation

- Practice explaining technical concepts simply

- Conduct mock cross-examination if possible

- Confirm logistics and timing

✅ Professional Readiness

- Review RICS expert witness standard requirements[1]

- Refresh understanding of tribunal duties

- Prepare professional demeanor and composure

- Organize documents for easy reference

- Confirm understanding of oath or affirmation requirements

Emerging Trends and Future Developments

Anticipated Changes to RICS Standards

The public consultation for the 5th edition expert witness standard closed in late 2025, with final publication expected in 2026.[1] Anticipated changes include:

Technology and Remote Testimony 💻

The standard is expected to address:

- Virtual tribunal participation protocols

- Digital evidence presentation standards

- Remote site inspection methodologies

- Electronic document authentication

- Cybersecurity and data protection

Climate Risk and ESG Considerations

Future valuations will increasingly incorporate:

- Climate risk assessments and flood risk

- Energy performance and retrofit requirements

- Sustainability credentials affecting value

- ESG disclosure requirements for lenders

- Long-term environmental liability

Expert witnesses must prepare for these emerging valuation factors as they become standard practice.

Market Evolution and Dispute Patterns

As the 2026 market recovery continues, dispute patterns are evolving:

Increased Volume of Disputes

Lower mortgage rates are driving transaction volumes, which historically correlates with increased valuation disputes. Expert witnesses should anticipate:

- Higher instruction volumes requiring capacity management

- Greater scrutiny of valuation methodologies

- More sophisticated challenges from opposing experts

- Increased regulatory oversight and professional discipline cases

Technology-Driven Valuation Challenges

Automated Valuation Models (AVMs) and AI-driven valuations are creating new dispute categories:

- Challenges to algorithm-based valuations

- Disputes over data quality and comparables selection

- Questions about professional judgment vs. automated analysis

- Regulatory uncertainty about AVM acceptance for lending

Expert witnesses must understand both traditional and technology-driven valuation methodologies to address these challenges effectively.

Professional Development Requirements

Maintaining competence in this evolving landscape requires ongoing professional development:

Essential CPD Topics for 2026 📚

- Basel 3.1 implementation and prudently conservative criteria

- Updated RICS expert witness standards and obligations

- Market analysis in recovery conditions

- Technology integration in valuation practice

- Climate risk and ESG valuation factors

- Cross-examination skills and testimony techniques

- Professional ethics and independence

RICS members should prioritize these topics in their continuing professional development to maintain expert witness competence.

Conclusion: Mastering Expert Witness Preparation in 2026

Expert Witness Preparation for 2026 Mortgage Valuation Disputes: RICS Guidelines Amid Rate Cuts and Recovery demands a sophisticated understanding of evolving regulatory frameworks, enhanced professional obligations, and dynamic market conditions. As mortgage rates settle at 3.5% and market activity increases, valuation disputes will continue to rise, creating both opportunities and challenges for chartered surveyors serving as expert witnesses.

The key to success lies in rigorous preparation, unwavering professional independence, and comprehensive knowledge of the latest RICS standards. The mandatory Bank Lending Valuations Standard (second edition) and the forthcoming Expert Witness Standard (5th edition) establish clear expectations for professional practice that expert witnesses must master.[1][2]

Actionable Next Steps

To excel in expert witness practice in 2026, chartered surveyors should:

-

Review and internalize the Bank Lending Valuations Standard (second edition) and Basel 3.1 guidance, with particular attention to jurisdiction-specific implementation in your practice area.[2]

-

Implement systematic conflict checking and disclosure procedures that exceed minimum requirements, protecting both professional independence and client interests.

-

Develop robust evidence gathering protocols that anticipate challenges and build defensible foundations for expert opinions, incorporating the latest market data and regulatory guidance.

-

Invest in cross-examination training and testimony skills development, recognizing that oral evidence is often as important as written reports in determining case outcomes.

-

Establish quality control systems for high-volume work that prevent over-commitment and maintain the quality standards expected of expert witnesses.

-

Engage with ongoing professional development focused on emerging valuation factors, technology integration, and evolving professional standards.

-

Build relationships with legal professionals who understand the value of properly prepared expert evidence and support professional independence.

The 2026 market recovery presents significant opportunities for expert witnesses who combine technical excellence with professional integrity. By mastering the latest RICS guidelines, understanding Basel 3.1 requirements, and maintaining unwavering commitment to tribunal duties over client interests, chartered surveyors can build successful expert witness practices while upholding the highest professional standards.

For professional assistance with complex valuation matters or expert witness preparation, consult with experienced chartered surveyors in London who maintain current knowledge of RICS standards and market conditions.

The intersection of regulatory evolution, market recovery, and professional standards creates a challenging but rewarding environment for expert witnesses in 2026. Those who invest in comprehensive preparation, maintain rigorous professional standards, and commit to ongoing development will find themselves well-positioned to serve tribunals, support justice, and advance the valuation profession.

References

[1] Rics Launches Global Consultation On Updated Expert Witness Standard – https://www.rics.org/news-insights/rics-launches-global-consultation-on-updated-expert-witness-standard

[2] Bank Lending Valuations – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/bank-lending-valuations

[3] Breaking Down The Rics Valuation What Every Valuer Should Know – https://globalvaluation.com/breaking-down-the-rics-valuation-what-every-valuer-should-know/

[4] Regulation Practice Alerts – https://www.rics.org/regulation/how-we-regulate/regulation-practice-alerts

[5] Expert Witnesses Single Joint Experts And Independent Experts – https://www.rics.org/dispute-resolution-service/drs-information-hub/expert-witnesses-single-joint-experts-and-independent-experts

[7] New Expert Witness Guidance For Rics Members – https://www.nmrk.com/en-gb/perspectives/new-expert-witness-guidance-for-rics-members