The property market in 2026 stands at a critical crossroads. With mortgage rates stabilizing in the mid-6% range after years of volatility, building surveyors face unprecedented challenges in delivering accurate valuations that account for rate sensitivity and buyer risk perception. As the RICS chief economist emphasizes, mortgage rates remain the single most critical factor influencing sustained market recovery—making it essential for surveyors to adapt their methodologies and documentation practices to reflect this new reality.

Understanding Mortgage Rate Sensitivity in Building Surveys: How Surveyors Navigate Valuation Risk in Uncertain 2026 Environment has become fundamental to professional practice. This comprehensive guide examines how chartered surveyors can incorporate rate volatility into their assessments, adjust for changing buyer psychology, and document assumptions with the rigor that lenders and clients demand in today's uncertain market.

Key Takeaways

- Mortgage rates are forecasted to remain stable around 6-6.4% throughout 2026, creating a new baseline for property valuations that differs significantly from the ultra-low rate environment of previous years [1][2]

- Rate sensitivity analysis must now be embedded in building surveys, with surveyors documenting how property values could fluctuate with 0.5-1% rate movements

- Buyer risk perception has fundamentally shifted, requiring surveyors to account for affordability concerns and financing constraints in their market value assessments

- Regional variations in rate impact demand localized approaches, as some markets show greater sensitivity to financing costs than others [3]

- Professional documentation standards have evolved, with RICS guidance emphasizing transparent assumption disclosure and scenario modeling in valuation reports

Understanding the 2026 Mortgage Rate Landscape

Current Rate Forecasts and Market Conditions

The mortgage rate environment in 2026 presents a picture of relative stability after the turbulence of recent years. Leading industry forecasters project rates to hover in a narrow band throughout the year:

- Fannie Mae: 6.0% average for 30-year fixed mortgages [1]

- Redfin: 6.3% projection [1]

- Mortgage Bankers Association: 6.4% forecast [2]

- National Association of Home Builders: 6.17% estimate [1]

This consensus around the mid-6% range represents a significant shift from both the ultra-low rates of 2020-2021 and the rapid increases experienced in 2022-2023. For building surveyors conducting homebuyer reports and building surveys, this stabilization provides a more predictable foundation for valuation work—but it also demands recognition that rates remain elevated by historical standards.

Impact on Housing Affordability and Demand

The combination of mid-6% mortgage rates and minimal home price growth is expected to create modest improvements in affordability conditions throughout 2026. The Mortgage Bankers Association forecasts that single-family mortgage originations will increase by 8% to $2.2 trillion in 2026, driven primarily by refinancing activity as homeowners locked into higher rates seek relief [2].

However, this improved affordability is relative. Monthly mortgage payments remain substantially higher than during the low-rate era, fundamentally altering buyer behavior and risk tolerance. Chartered surveyors must recognize that:

- Purchase power has declined approximately 30-35% compared to 2020 levels at similar income levels

- Buyer demographics have shifted toward higher-income households better able to absorb elevated financing costs

- Property type preferences have evolved, with buyers seeking smaller homes or different locations to offset rate impacts

Mortgage Rate Sensitivity in Building Surveys: Incorporating Volatility into Valuations

Developing Rate Sensitivity Models

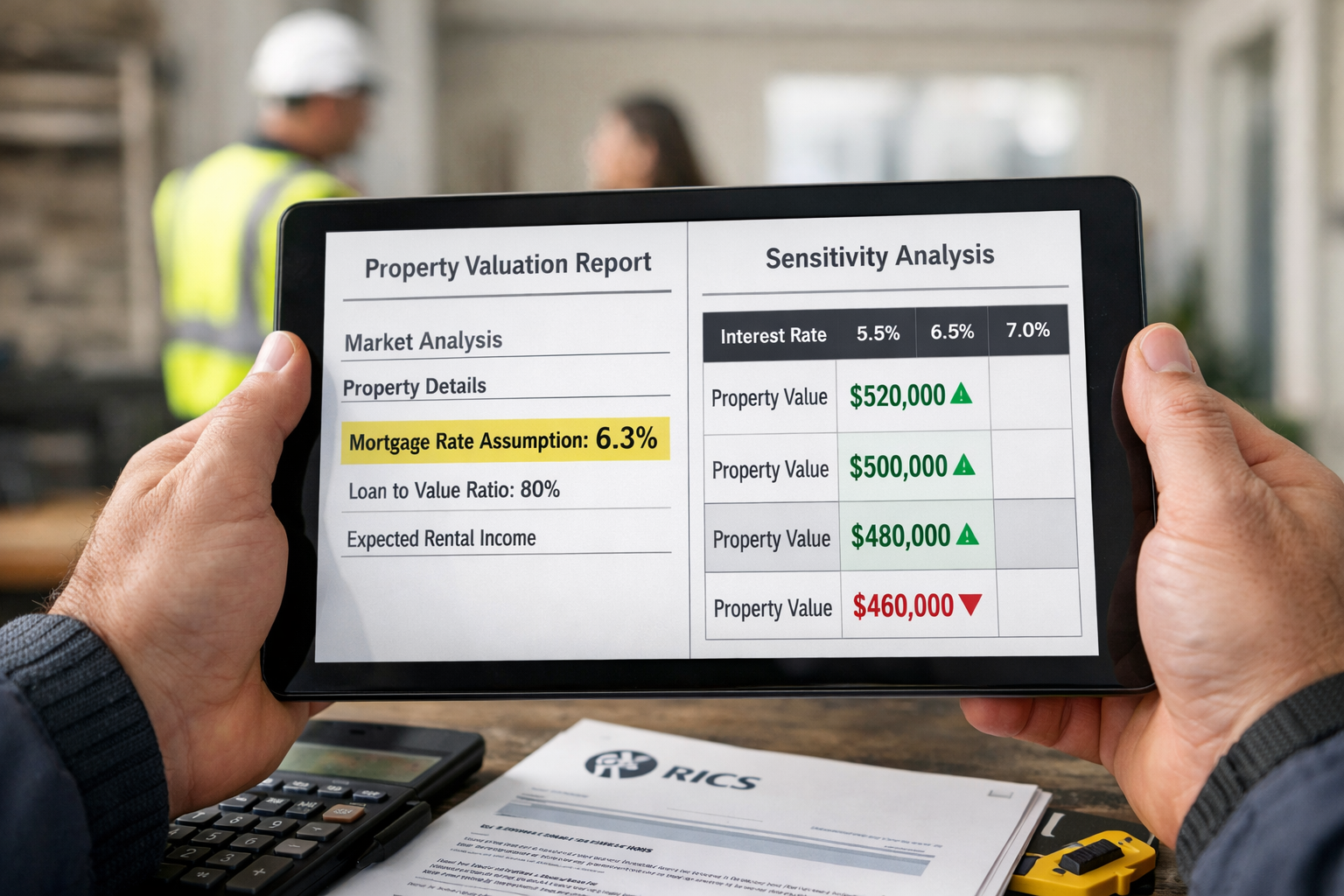

Professional surveyors in 2026 must move beyond static valuation approaches to incorporate dynamic rate sensitivity analysis into their assessments. This involves creating models that demonstrate how property values respond to rate fluctuations—a practice that has become standard in commercial property surveys and is now essential for residential work.

A comprehensive rate sensitivity model should include:

| Rate Scenario | Monthly Payment Impact | Buyer Pool Effect | Estimated Value Adjustment |

|---|---|---|---|

| Base (6.3%) | £0 (baseline) | Standard market | £0 (current valuation) |

| -0.5% (5.8%) | -£150 per £250k | +15% buyer pool | +3-5% value increase |

| +0.5% (6.8%) | +£150 per £250k | -15% buyer pool | -3-5% value decrease |

| +1.0% (7.3%) | +£300 per £250k | -25% buyer pool | -6-9% value decrease |

These models help clients understand the valuation risk inherent in rate uncertainty and provide lenders with the scenario analysis they need for prudent lending decisions.

Adjusting Comparable Sales Analysis

Traditional comparable sales analysis assumes relatively stable financing conditions. In the 2026 environment, surveyors must adjust their approach to account for:

Temporal Rate Adjustments: Properties sold when rates were significantly different (even 3-6 months prior) may not provide accurate comparables without adjustment. A property that sold at £500,000 when rates were 5.8% might only command £475,000-£485,000 at 6.8%, assuming similar market conditions.

Financing-Dependent Buyer Behavior: The proportion of cash buyers versus financed purchases affects comparable validity. Markets with higher cash buyer percentages (such as prime London locations) show less rate sensitivity than heavily mortgaged markets.

Regional Rate Impact Variations: According to the National Association of Realtors, some regional markets are experiencing price declines despite stable national trends, largely due to inventory increases and rate sensitivity [3]. Chartered surveyors in Surrey may encounter different rate impacts than those working in central London.

Documentation Standards for Rate Assumptions

The RICS Valuation – Global Standards (Red Book) emphasizes the importance of transparent assumption disclosure. In 2026, this extends to explicit documentation of:

✅ Base Rate Assumptions: Clearly state the mortgage rate assumption underlying the valuation (e.g., "This valuation assumes prevailing mortgage rates of approximately 6.3% for standard residential mortgages")

✅ Sensitivity Ranges: Provide commentary on how the valuation might adjust with rate movements (e.g., "A sustained increase in mortgage rates to 7% could reduce market value by approximately 4-6%")

✅ Market Conditions Date: Specify the exact date of rate data used, as even monthly variations can be significant

✅ Financing Assumption Clarity: Distinguish between valuations assuming typical financing versus cash purchases or specialized lending arrangements

Professional RICS registered valuers recognize that this enhanced documentation protects both the surveyor and the client by establishing clear parameters for the valuation's validity.

How Surveyors Navigate Valuation Risk Through Enhanced Methodologies

Risk-Adjusted Valuation Frameworks

Navigating Mortgage Rate Sensitivity in Building Surveys: How Surveyors Navigate Valuation Risk in Uncertain 2026 Environment requires adopting risk-adjusted frameworks that go beyond traditional approaches. Leading practitioners are implementing:

Probabilistic Valuation Ranges: Rather than providing a single point estimate, surveyors increasingly offer a confidence range that reflects rate uncertainty. For example: "Market value estimated at £450,000 with 80% confidence range of £435,000-£465,000 based on current rate environment."

Buyer Profile Analysis: Assessing the likely buyer demographic for a property and their rate sensitivity. First-time buyers stretching affordability show higher rate sensitivity than downsizers with substantial equity.

Liquidity Adjustments: Properties requiring longer marketing periods in rate-sensitive markets may warrant modest valuation discounts to reflect increased holding costs and uncertainty.

Accounting for Buyer Risk Perception

Beyond mathematical models, surveyors must recognize that buyer psychology has fundamentally shifted in the elevated rate environment. Research from the National Association of Home Builders indicates that demand uncertainty is changing homebuilding strategy in 2026 [5], reflecting broader market caution.

Key psychological factors affecting valuations include:

🏠 Payment Shock Aversion: Buyers who previously rented or owned with low-rate mortgages experience significant payment shock at current rates, reducing their willingness to pay premium prices

📊 Rate Lock Anxiety: Fear of rates rising further creates urgency, while expectations of potential decreases create hesitation—surveyors must gauge local market sentiment

💰 Equity Preservation Focus: Buyers are more concerned about protecting their down payment investment, leading to increased scrutiny of property condition and value stability

When conducting building surveys, surveyors should note property features that either mitigate or exacerbate buyer risk perception—such as energy efficiency (which reduces operating costs and offsets rate impacts) or deferred maintenance (which amplifies buyer caution in uncertain markets).

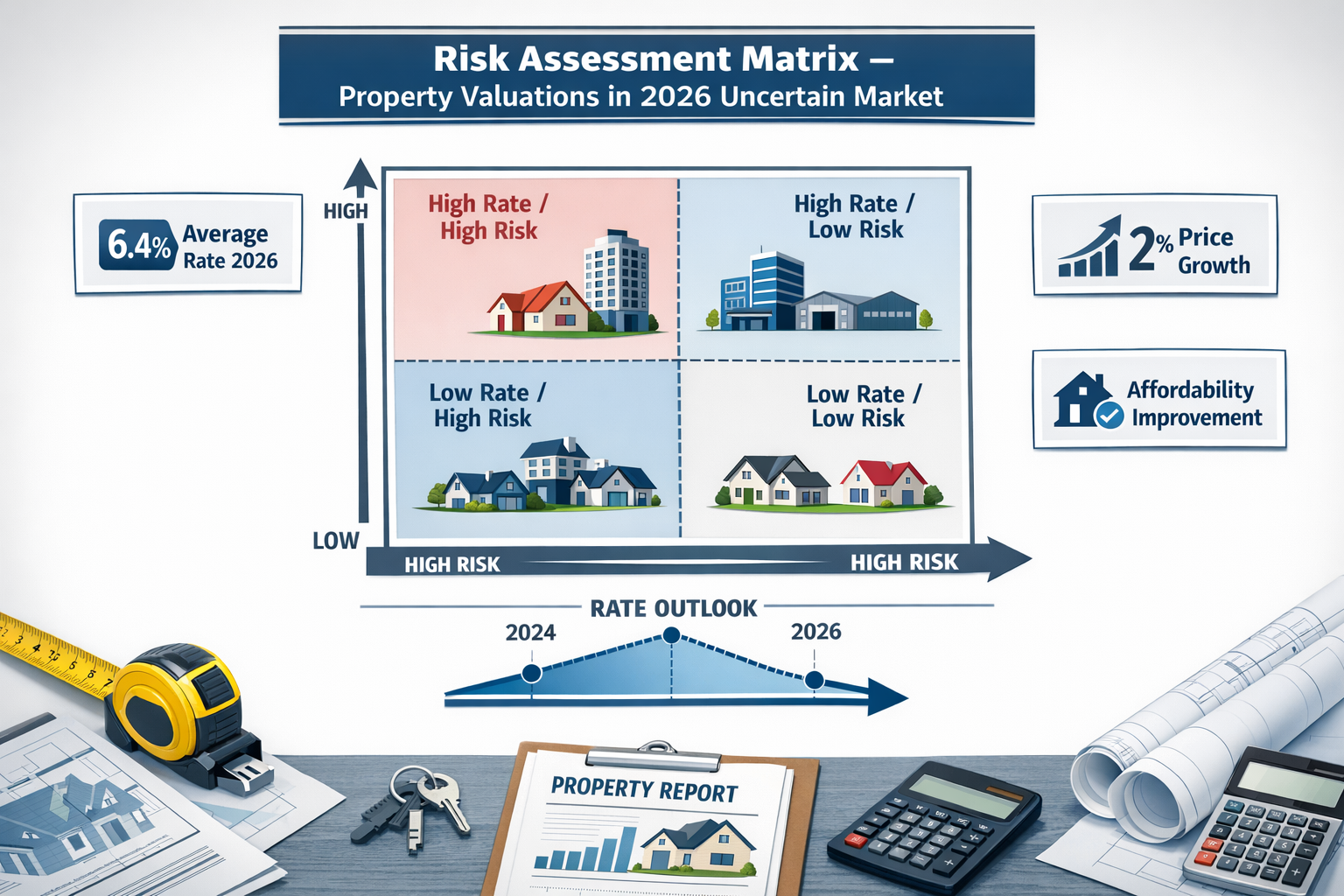

Regional Market Differentiation

The impact of mortgage rate sensitivity varies significantly across regions, requiring surveyors to develop localized expertise. S&P Global's 2026 outlook notes that while national home prices are expected to remain stagnant with approximately 2% growth, regional variations are substantial [6].

High-Sensitivity Markets typically feature:

- High percentage of first-time buyers

- Lower median incomes relative to property prices

- Limited cash buyer presence

- Recent rapid price appreciation that has outpaced income growth

Lower-Sensitivity Markets often include:

- Established areas with high equity homeowner base

- Strong cash buyer presence (retirees, downsizers, international buyers)

- Diverse property price points

- Stable employment and income growth

Surveyors operating across multiple regions—such as those covering both West London and Hertfordshire—must calibrate their rate sensitivity assumptions to local conditions rather than applying uniform national models.

Professional Standards and Best Practices for 2026

RICS Guidance on Uncertain Market Valuations

The Royal Institution of Chartered Surveyors has enhanced its guidance for valuations conducted in uncertain market conditions. Key principles for addressing Mortgage Rate Sensitivity in Building Surveys: How Surveyors Navigate Valuation Risk in Uncertain 2026 Environment include:

Material Uncertainty Clauses: When appropriate, surveyors should include material uncertainty declarations that acknowledge the potential for greater-than-normal valuation variance due to rate volatility and market uncertainty.

Assumption Transparency: All assumptions regarding market conditions, financing availability, and rate environments must be explicitly stated and justified with reference to current market data.

Regular Revalidation: Valuations should include clear statements about their validity period, which may be shorter in volatile rate environments (e.g., 30-60 days rather than 90 days).

Competence Requirements: Surveyors must demonstrate current knowledge of mortgage market conditions, financing trends, and economic factors affecting property values in their operating regions.

Integration with Lender Requirements

Mortgage lenders in 2026 have heightened expectations for valuation reports that address rate sensitivity and market risk. Professional surveyors should ensure their reports include:

Loan-to-Value Sensitivity Commentary: Explicit discussion of how the property's value might respond to rate changes, particularly relevant for higher LTV mortgages where small value decreases can create equity concerns.

Market Absorption Analysis: Assessment of how quickly the property could be sold in current market conditions, considering rate-driven demand fluctuations.

Comparable Financing Verification: Where possible, confirmation of financing terms for comparable sales to ensure true comparability.

Forward-Looking Market Commentary: Brief analysis of local market trends and rate impact expectations, drawing on authoritative sources like the Mortgage Bankers Association forecasts [2].

Technology and Data Integration

Leading surveyors are leveraging technology to enhance their rate sensitivity analysis:

- Real-time rate data feeds integrated into valuation software

- Automated sensitivity calculators that generate scenario analyses

- Market data platforms providing financing statistics for comparable properties

- Geographic information systems mapping rate sensitivity by neighborhood or postcode

These tools enable more sophisticated analysis while maintaining the professional judgment that remains central to surveying practice.

Practical Implementation for Surveying Professionals

Survey Report Enhancements

When conducting commercial building surveys or residential assessments, surveyors should enhance their reports with dedicated sections addressing:

Section 1: Market Context and Rate Environment

- Current mortgage rate levels and recent trends

- Comparison to historical averages

- Forecast outlook from authoritative sources

Section 2: Rate Sensitivity Analysis

- Property-specific sensitivity assessment

- Buyer demographic considerations

- Comparable sales financing analysis

Section 3: Valuation Assumptions and Limitations

- Explicit rate assumptions

- Validity period and revaluation triggers

- Material uncertainty disclosures (if applicable)

Section 4: Risk Factors and Mitigation

- Property features affecting rate sensitivity

- Market positioning relative to rate impacts

- Recommendations for buyers/sellers

Client Communication Strategies

Effective communication about rate sensitivity requires translating technical analysis into accessible language. When discussing Mortgage Rate Sensitivity in Building Surveys: How Surveyors Navigate Valuation Risk in Uncertain 2026 Environment with clients:

For Buyers: Explain how rate changes could affect their monthly payments and long-term equity position. Provide context about current rates relative to forecasts, helping them make informed timing decisions.

For Sellers: Discuss how rate-driven buyer behavior might affect marketing strategy, pricing, and negotiation approaches. Help them understand realistic expectations in the current environment.

For Lenders: Emphasize the robustness of the valuation methodology and the transparency of assumptions, demonstrating professional competence in addressing rate-related risks.

For Investors: Provide detailed scenario analysis showing potential returns under different rate trajectories, supporting sophisticated investment decision-making.

Continuing Professional Development

Surveyors must maintain current knowledge of mortgage market dynamics through:

- Regular review of forecasts from Fannie Mae, Freddie Mac, and the MBA [1][2]

- Monitoring of Bank of England policy decisions and economic indicators

- Participation in RICS training on uncertain market valuations

- Engagement with local market data and financing trends

- Networking with mortgage brokers and lenders to understand practical financing conditions

Conclusion: Adapting Professional Practice for Long-Term Success

The 2026 property market environment demands that building surveyors fundamentally evolve their approach to valuations. With mortgage rates stabilized in the mid-6% range but uncertainty persisting about future trajectories, Mortgage Rate Sensitivity in Building Surveys: How Surveyors Navigate Valuation Risk in Uncertain 2026 Environment has become a core professional competency rather than a specialized consideration.

Surveyors who successfully adapt will distinguish themselves through:

✨ Transparent methodology that explicitly addresses rate assumptions and sensitivity

✨ Enhanced documentation that protects all parties through clear assumption disclosure

✨ Regional expertise that recognizes local market variations in rate sensitivity

✨ Client education that helps buyers, sellers, and lenders navigate uncertainty

✨ Technological integration that supports sophisticated analysis while maintaining professional judgment

Actionable Next Steps

For Surveying Professionals:

- Review and update your valuation templates to include dedicated rate sensitivity sections

- Establish data sources for current mortgage rate information and forecasts

- Develop regional rate sensitivity profiles for your primary operating areas

- Engage with lender clients to understand their evolving requirements for rate-related analysis

- Invest in continuing education focused on economic factors affecting property values

- Consider specialized software that automates sensitivity calculations while preserving professional oversight

For Property Buyers and Sellers:

- Commission surveys from RICS-qualified professionals who demonstrate understanding of current market dynamics

- Request explicit rate sensitivity analysis in your valuation reports

- Understand the validity period of valuations in the current environment

- Consider scenario planning for different rate trajectories when making purchase decisions

For Mortgage Lenders:

- Review valuation report requirements to ensure they address rate sensitivity adequately

- Establish clear standards for assumption disclosure and scenario analysis

- Engage with surveying panels about enhanced documentation expectations

- Consider shorter validity periods for valuations in volatile rate environments

The property market's future remains inherently uncertain, but professional surveyors equipped with robust methodologies for addressing rate sensitivity will continue to provide the reliable valuations that underpin confident property transactions. By embracing enhanced analytical frameworks, transparent documentation, and ongoing professional development, the surveying profession can successfully navigate the challenges of 2026 and beyond.

Whether conducting help to buy valuations, insurance reinstatement assessments, or standard market valuations, the principles of rate sensitivity analysis and risk-adjusted methodology will remain central to professional excellence in an uncertain environment.

References

[1] Mortgage Interest Rates Forecast – https://www.rocketmortgage.com/learn/mortgage-interest-rates-forecast

[2] MBA Forecast Total Single Family Mortgage Originations To Increase 8 Percent To 2.2 Trillion In 2026 – https://www.mba.org/news-and-research/newsroom/news/2025/10/19/mba-forecast–total-single-family-mortgage-originations-to-increase-8-percent-to–2.2-trillion-in-2026

[3] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[5] Survey Reveals Demand Uncertainty Is Changing 2026 Homebuilding Strategy – https://www.housingwire.com/articles/survey-reveals-demand-uncertainty-is-changing-2026-homebuilding-strategy/

[6] 2026 US Residential Mortgage And Housing Outlook Robust Issuance Growth Amid Stagnant Home Prices – https://www.spglobal.com/ratings/en/regulatory/article/2026-us-residential-mortgage-and-housing-outlook-robust-issuance-growth-amid-stagnant-home-prices-s101660033