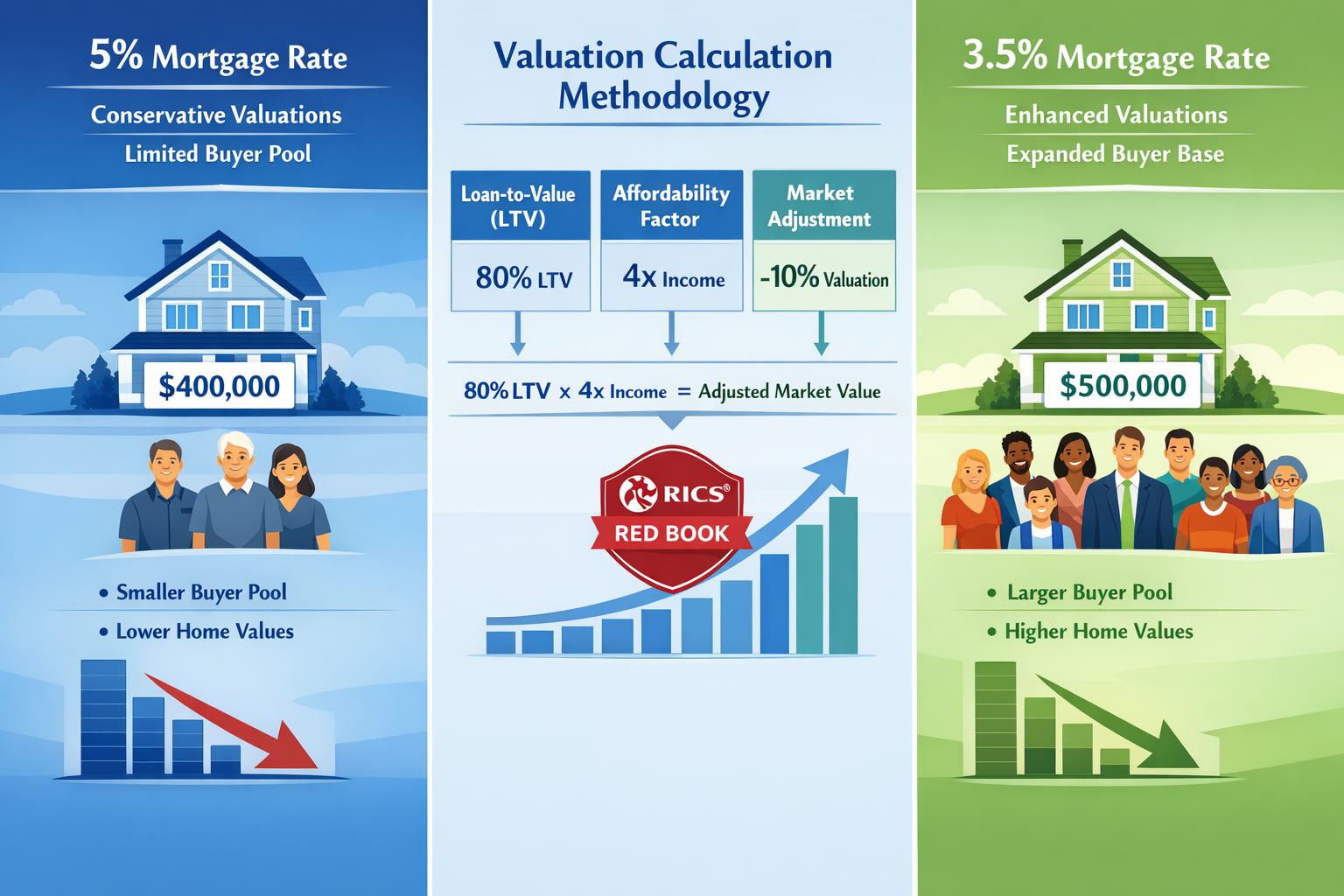

Mortgage rates hovering near 3.5% in 2026 are reshaping the UK property market in ways not seen since before the pandemic. For chartered surveyors, this dramatic shift presents both opportunity and challenge: how do you accurately value properties when buyer purchasing power has suddenly expanded by 20-30%? The answer lies in understanding Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves and applying proven methodologies that balance optimism with prudent professional standards.

As rates have tumbled from their 2023 peaks above 6%, the valuation landscape has transformed. Properties that seemed overpriced just months ago now appear reasonable, while sellers' expectations lag behind the improving affordability picture. Surveyors must navigate this tentative recovery with precision, drawing on the latest RICS guidance to recalibrate valuations that reflect genuine market conditions rather than outdated assumptions.

Key Takeaways

- 📉 Mortgage rates near 3.5% in 2026 have increased buyer purchasing power by approximately 25-30% compared to 2023 peak rates

- 📋 RICS Red Book standards require surveyors to incorporate current affordability metrics and recent comparable evidence when adjusting valuations

- 🏠 Market value adjustments must balance improved buyer capacity with realistic market absorption rates during the tentative recovery phase

- 💰 Loan-to-value ratios and affordability multipliers are critical factors in determining appropriate valuation adjustments for falling rate environments

- ⚖️ Conservative methodology remains essential even during improving conditions, as RICS guidance emphasizes sustainable lending practices over optimistic projections

Understanding the 2026 Mortgage Rate Environment and Its Impact on Property Values

The mortgage rate environment in 2026 represents a significant departure from the high-rate period of 2022-2024. With average fixed-rate mortgages now available at approximately 3.5%, compared to peaks exceeding 6% just two years ago, the financial landscape for property purchases has fundamentally shifted. This transformation directly impacts how surveyors must approach RICS valuation cost assessments and methodology.

The Mathematics of Affordability Improvement

When mortgage rates decline from 6% to 3.5%, the impact on monthly payments and borrowing capacity is substantial. Consider a typical scenario:

| Mortgage Rate | Monthly Payment (£300k loan) | Maximum Borrowing (£1,500/month) |

|---|---|---|

| 6.0% | £1,799 | £250,000 |

| 4.5% | £1,520 | £296,000 |

| 3.5% | £1,347 | £334,000 |

This table illustrates why Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves has become such a critical topic. The same buyer who could only afford a £250,000 property at 6% rates can now potentially purchase a property valued at £334,000—a 33.6% increase in purchasing power.

Market Dynamics in the Tentative Recovery

The 2026 property market exhibits characteristics of a tentative recovery rather than a full-blown boom. While affordability has improved dramatically, several factors temper enthusiasm:

- Buyer caution following years of rate volatility

- Economic uncertainty regarding inflation and employment

- Lender prudence maintaining conservative lending criteria

- Seller expectations that haven't fully adjusted to new market realities

According to recent RICS survey data, surveyors report increased transaction activity but note that valuations must remain grounded in actual comparable evidence rather than theoretical affordability calculations [5]. This balanced approach ensures that valuation reports reflect genuine market conditions.

RICS Standards for Rate-Sensitive Valuations

The RICS Red Book provides the foundational framework for all property valuations, but specific guidance on rate-sensitive adjustments requires careful interpretation. The Bank Lending Valuations and Market Lending Value (MLV) guidance emphasizes that valuations must be "prudently conservative" and based on sustainable market conditions [1].

Key principles include:

✅ Market evidence primacy: Recent comparable sales trump theoretical affordability models

✅ Time-adjusted analysis: Comparables from high-rate periods require adjustment

✅ Buyer pool assessment: Expanded affordability must translate to actual demand

✅ Lender criteria consideration: Banks' lending standards influence achievable prices

✅ Economic context: Broader economic factors beyond rates affect values

RICS Techniques for Adjusting Valuations in Falling Rate Environments

Professional surveyors employ several specific techniques when conducting Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves assessments. These methodologies balance improved affordability with the need for conservative, defensible valuations that protect both lenders and borrowers.

Comparable Sales Adjustment Methodology

The cornerstone of any Red Book valuation remains comparable evidence, but falling rates require nuanced adjustments to historical data:

Time-Based Rate Adjustments

When comparable sales occurred during higher-rate periods, surveyors must consider whether current market conditions justify upward adjustments. The process involves:

- Identify the comparable sale date and prevailing mortgage rates at that time

- Calculate the affordability differential between then and now

- Assess market absorption to determine if demand has actually increased

- Apply conservative adjustment factors typically ranging from 2-8% depending on rate differential

For example, a comparable sale from six months ago at £400,000 when rates were 4.5% might justify a 3-5% upward adjustment now that rates have fallen to 3.5%, assuming other market factors remain constant.

Geographic Market Segmentation

Different property segments respond differently to rate changes. RICS guidance suggests segmenting analysis by:

- First-time buyer properties (£200k-£350k): Most sensitive to rate changes

- Mid-market properties (£350k-£600k): Moderate sensitivity

- Premium properties (£600k+): Less rate-sensitive, more influenced by wealth effects

This segmentation ensures that valuation factors are appropriately weighted for each property type.

Affordability Multiplier Recalibration

Traditional income multipliers (typically 4-4.5x household income) may require adjustment in falling rate environments. However, RICS standards emphasize that lender criteria—not theoretical affordability—should guide valuations [1].

Key Considerations:

💡 Lender stress testing: Banks still stress-test affordability at rates 2-3% above current levels

💡 Income verification: Tighter lending standards post-2008 mean not all theoretical buyers can access credit

💡 Deposit requirements: Even with lower rates, deposit availability constrains many buyers

💡 Loan-to-value limits: Conservative LTV ratios may prevent buyers from maximizing borrowing capacity

Market Value vs. Mortgage Lending Value Distinction

An important RICS concept when dealing with Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves is the distinction between Market Value (MV) and Mortgage Lending Value (MLV).

Market Value reflects the estimated amount for which a property should exchange on the valuation date between a willing buyer and seller in an arm's-length transaction.

Mortgage Lending Value represents a more conservative figure, typically 5-15% below market value, designed to protect lenders against market downturns [1].

In falling rate environments, this distinction becomes crucial:

| Scenario | Market Value Adjustment | MLV Adjustment |

|---|---|---|

| Strong comparable evidence | +5-8% from high-rate comparables | +3-5% from high-rate comparables |

| Limited recent sales | +2-4% cautious adjustment | 0-2% minimal adjustment |

| Volatile market conditions | 0-3% conservative approach | -2-0% maintain prudence |

Forward-Looking vs. Backward-Looking Analysis

RICS standards require valuations to be based on current market conditions, not future speculation. However, when rates have recently fallen, this creates a methodological challenge:

Backward-looking comparables may undervalue properties because they reflect higher-rate market conditions.

Forward-looking projections risk overvaluation by assuming sustained low rates and continued demand growth.

The professional solution involves:

- Primary reliance on the most recent 3-6 months of comparable data

- Secondary consideration of market momentum indicators

- Explicit disclosure of market uncertainty in valuation reports

- Conservative bias when evidence is ambiguous or contradictory

This approach aligns with RICS guidance on bank lending valuations, which emphasizes that valuations should be "realistic and achievable" rather than optimistic [3].

Practical Application: Implementing Valuation Adjustments for Falling Mortgage Rates

Translating RICS theory into practical Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves requires a systematic approach that surveyors can apply consistently across different property types and market conditions.

Step-by-Step Valuation Adjustment Framework

Professional surveyors should follow this structured methodology when conducting valuations in the current falling-rate environment:

Step 1: Establish the Baseline Comparable Evidence

Begin by identifying 3-5 comparable properties that have sold within the past 6-12 months. For each comparable:

- Record the sale date and price

- Note the prevailing mortgage rates at sale date

- Document any special circumstances affecting the sale

- Assess the comparability (location, size, condition, features)

Step 2: Calculate the Rate Differential Impact

Determine the mortgage rate environment for each comparable versus current conditions:

- If comparable sold when rates were 4.5% and current rates are 3.5%, the differential is 1.0%

- Each 1% rate reduction typically improves buyer purchasing power by approximately 10-12%

- However, actual market adjustment is typically only 30-50% of theoretical improvement due to market friction

Step 3: Apply Conservative Adjustment Factors

Based on the rate differential and market conditions, apply adjustment factors:

🔹 Strong market with high demand: 4-6% upward adjustment per 1% rate decline

🔹 Balanced market conditions: 2-4% upward adjustment per 1% rate decline

🔹 Uncertain or volatile market: 0-2% upward adjustment per 1% rate decline

These adjustments should be explicitly documented in the valuation report with clear justification.

Step 4: Cross-Reference with Current Market Activity

Validate adjustments against current market indicators:

- Recent asking prices for similar properties

- Time on market for comparable listings

- Offer-to-asking price ratios

- Surveyor feedback from recent instructions

If adjusted valuations significantly exceed current asking prices or recent sales, reconsider the adjustment magnitude.

Step 5: Apply Lender-Specific Considerations

When conducting valuations for mortgage purposes, incorporate lender-specific factors:

- Maximum LTV ratios the lender will accept

- Income multiplier limits

- Property type restrictions (e.g., ex-local authority, high-rise)

- Geographic lending restrictions

These constraints may limit achievable values regardless of theoretical affordability improvements.

Special Considerations for Different Valuation Types

Different valuation purposes require tailored approaches to Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves:

Mortgage Valuations

For standard mortgage valuations, the primary concern is ensuring the property provides adequate security for the loan. Adjustments should be:

- Conservative and defensible

- Supported by recent comparable evidence

- Consistent with lender risk appetite

- Documented with explicit reasoning

Probate and Tax Valuations

Probate valuations and capital gains tax valuations require market value at a specific date. Rate adjustments must reflect conditions on that valuation date, not current conditions.

Shared Ownership Valuations

Shared ownership valuations present unique challenges as they involve both market value and staircasing calculations. Improved affordability may increase demand for shared ownership schemes, potentially supporting higher valuations.

Right to Buy Valuations

Right to buy valuations must follow statutory guidance, but improved mortgage affordability may influence the open market value component of the assessment.

Documentation and Report Writing Best Practices

Proper documentation is essential when applying rate-related valuation adjustments. RICS standards require clear, transparent reporting that allows readers to understand the valuation reasoning [1].

Essential Report Elements:

📝 Market context section: Describe current mortgage rate environment and recent trends

📝 Comparable analysis: Present unadjusted comparable evidence with dates and rates

📝 Adjustment methodology: Explain the basis for any rate-related adjustments

📝 Uncertainty disclosure: Acknowledge market uncertainty and adjustment limitations

📝 Assumptions and limitations: State explicitly any assumptions regarding future rates or market conditions

This transparency protects both the surveyor and the client, ensuring that valuations can withstand scrutiny in the event of disputes or market changes.

Common Pitfalls to Avoid

When implementing Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves, surveyors should avoid these common errors:

❌ Over-reliance on theoretical affordability: Just because buyers can borrow more doesn't mean properties will immediately achieve higher prices

❌ Ignoring market absorption rates: The market needs time to adjust to new affordability levels

❌ Excessive optimism: The tentative nature of the 2026 recovery requires conservative approaches

❌ Inconsistent methodology: Adjustment factors should be applied consistently across similar properties

❌ Inadequate documentation: Failure to explain adjustment reasoning creates professional liability

❌ Neglecting lender criteria: Theoretical buyer capacity must align with actual lending standards

Quality Assurance and Peer Review

Given the complexity of rate-related adjustments, quality assurance processes become particularly important:

- Internal review: Senior surveyors should review valuations involving significant rate adjustments

- Peer comparison: Compare adjustment factors with those applied by colleagues in similar cases

- Market testing: Monitor subsequent sales to validate adjustment accuracy

- Continuous learning: Update methodologies based on market feedback and outcomes

This systematic approach ensures that valuations remain credible and defensible while appropriately reflecting improved affordability conditions in 2026.

Conclusion: Navigating the 2026 Valuation Landscape with Confidence

The dramatic improvement in mortgage affordability during 2026, with rates approaching 3.5%, presents both opportunity and responsibility for RICS-qualified surveyors. Valuation Adjustments for Falling Mortgage Rates: RICS Techniques as 2026 Affordability Improves is not merely an academic exercise—it represents a critical professional skill that directly impacts lending decisions, property transactions, and market stability.

The key to successful valuations in this environment lies in balancing optimism with prudence. While improved affordability genuinely expands buyer purchasing power and supports higher property values, surveyors must remain grounded in comparable evidence, conservative methodology, and transparent documentation. The tentative nature of the 2026 recovery means that excessive optimism could expose lenders and borrowers to unnecessary risk.

Actionable Next Steps for Surveyors

To ensure your valuations appropriately reflect current market conditions:

-

Update your comparable database with recent sales data from the past 3-6 months, noting prevailing mortgage rates at each sale date

-

Develop a standardized adjustment framework for rate-related modifications, ensuring consistency across your practice

-

Enhance your market intelligence by monitoring mortgage rate trends, lender criteria changes, and local market absorption rates

-

Invest in continuing professional development focused on RICS Red Book standards and bank lending valuation guidance

-

Strengthen your documentation practices to ensure all rate-related adjustments are clearly explained and justified

-

Engage with lender clients to understand their specific risk appetite and lending criteria in the current environment

-

Monitor your valuation outcomes by tracking subsequent sales to validate your adjustment methodology

The property market in 2026 offers genuine reasons for optimism, with improved affordability creating opportunities for buyers who were previously priced out. However, professional surveyors must ensure that valuations reflect realistic, achievable prices supported by market evidence rather than theoretical calculations alone.

By applying rigorous RICS techniques, maintaining conservative standards, and documenting methodology transparently, surveyors can provide valuations that serve all stakeholders effectively—protecting lenders, informing buyers, and supporting a sustainable property market recovery. The falling mortgage rate environment demands not just technical skill but professional judgment that balances opportunity with prudence, ensuring that today's valuations remain defensible in tomorrow's market conditions.

References

[1] Bank Lending Valuations And Mlv 2nd Edition Final – https://www.rics.org/content/dam/ricsglobal/documents/standards/Bank-lending-valuations-and-MLV_2nd-edition-Final.pdf

[2] Mortgage Valuations Below Asking Price – https://millionplus.com/mortgage-valuations-below-asking-price/

[3] Rics Updates Global Guidance On Bank Lending Valuations With Two Key Publications – https://www.rics.org/news-insights/rics-updates-global-guidance-on-bank-lending-valuations-with-two-key-publications

[5] Valuation Techniques For Stabilising National House Prices Rics January 2026 Survey Insights For Surveyors – https://nottinghillsurveyors.com/blog/valuation-techniques-for-stabilising-national-house-prices-rics-january-2026-survey-insights-for-surveyors