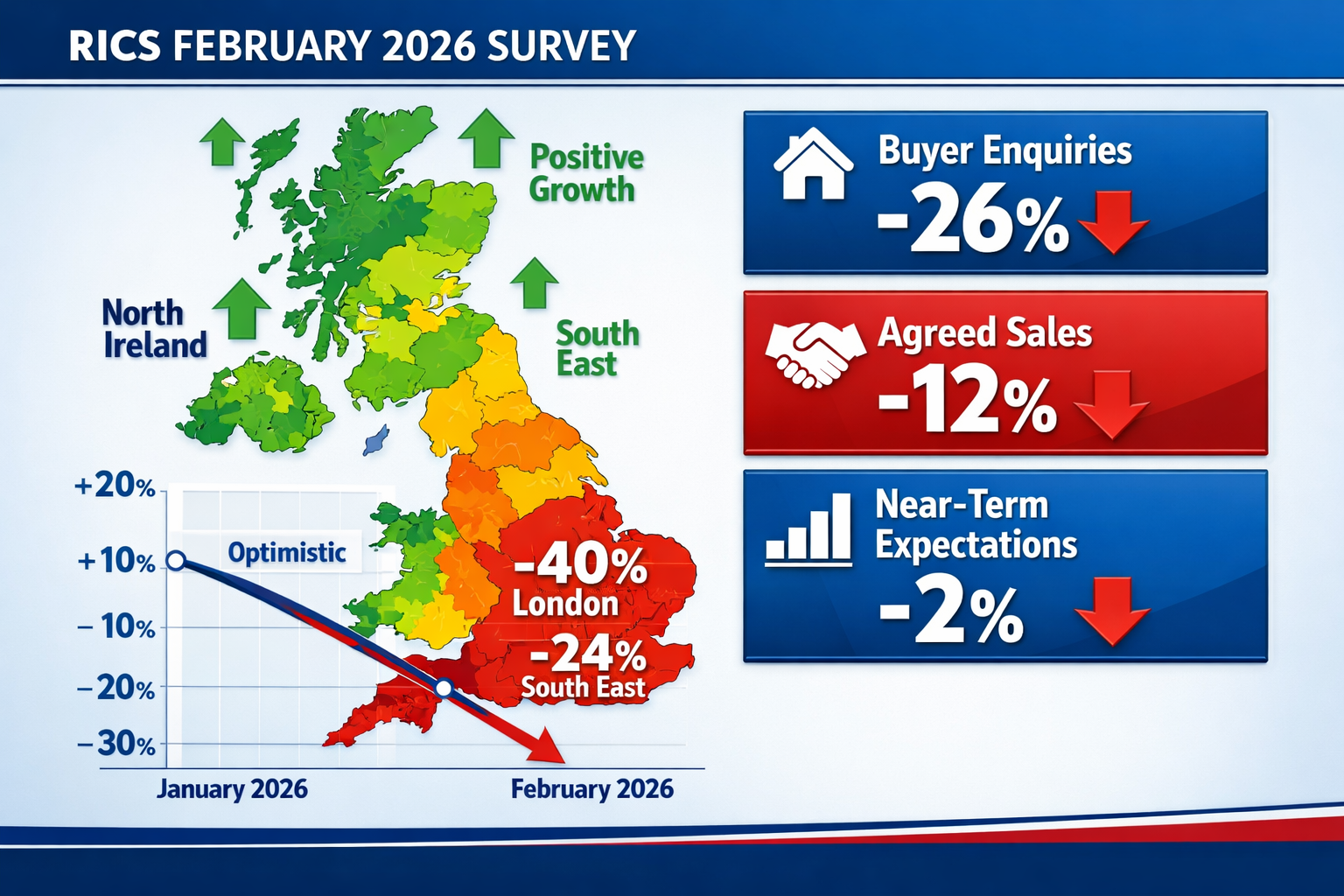

New buyer enquiries plummeted to -26% in February 2026—the sharpest monthly decline in over a year—yet 12-month price expectations remain stubbornly positive at +33% across the UK.[1][2] This paradox defines the current valuation challenge: how do chartered surveyors reconcile immediate market weakness with persistent long-term optimism while navigating unprecedented regional divergence?

The February 2026 RICS Residential Market Survey reveals a housing market split along geographic and temporal fault lines. Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment requires surveyors to abandon one-size-fits-all approaches and adopt nuanced methodologies that account for London's -40% price sentiment alongside Northern Ireland's continued growth.[2] With agreed sales posting -12% and near-term expectations falling to -2%, the softest reading since November 2025, valuation professionals face the complex task of balancing subdued transaction activity against anticipated recovery once geopolitical volatility stabilizes.[3]

This comprehensive guide examines the February 2026 RICS data through a valuation lens, providing practical adjustment tactics for surveyors working across divergent regional markets.

Key Takeaways

- Buyer enquiries declined sharply to -26% in February 2026, driven by renewed interest rate concerns and geopolitical uncertainty, requiring valuation adjustments for reduced market liquidity

- Regional price sentiment varies dramatically: London (-40%), South East (-24%), and East Anglia (-26%) face downward pressure while Northern Ireland, Scotland, and North West show resilience

- 12-month expectations remain positive at +33% despite near-term weakness at -2%, creating a valuation tension between current transaction evidence and forward-looking sentiment

- Rental market dynamics with landlord instructions at -27% and rental price expectations at +20% significantly impact investment property valuations

- Valuation methodology must incorporate regional adjustment factors, comparable evidence weighting, and sentiment-based risk premiums to reflect mixed market conditions accurately

Understanding the February 2026 RICS Survey Data Landscape

The February 2026 RICS Residential Market Survey presents a complex picture that challenges traditional valuation assumptions. The headline figures reveal a market experiencing significant short-term headwinds while maintaining cautious optimism about medium-term prospects.

Core Market Indicators and Their Valuation Implications

New buyer enquiries deteriorated from -15% in January to -26% in February, marking the most significant monthly decline since early 2025.[1] This sharp contraction signals reduced market liquidity—a critical factor when determining appropriate valuation adjustments. Properties in markets with declining enquiry levels typically require longer marketing periods, which should influence valuation judgments regarding achievable prices within reasonable timeframes.

Agreed sales posted a net balance of -12%, indicating that transaction volumes remain subdued.[3] While this represents an improvement over the preceding six months' trend, it nonetheless suggests a market where buyers maintain negotiating leverage. For RICS registered valuers, this creates challenges in establishing reliable comparable evidence, particularly in areas with thin transaction volumes.

The near-term sales expectations figure of -2% represents the softest reading since November 2025, suggesting minimal immediate market momentum.[2] This metric is particularly valuable for valuers conducting forward-looking assessments for development appraisals or investment analysis, as it indicates that market participants anticipate continued sluggish conditions over the next three months.

The Long-Term Optimism Paradox

Despite near-term weakness, 12-month sales expectations stand at +17%, with a modest majority of surveyed property professionals anticipating recovery once geopolitical volatility stabilizes.[3] This creates a fundamental tension for valuation professionals: should current valuations reflect depressed transaction evidence or incorporate expectations of recovery?

The 12-month price expectations of +33% (down from +43% in January) further complicate valuation judgments.[2] This moderation suggests that while optimism persists, it is becoming more cautious—a sentiment shift that should influence risk adjustments in valuation reports.

Regional Divergence: The Critical Valuation Variable

The February 2026 data reveals that headline house prices remain broadly flat at -12% net balance, but this national figure masks dramatic regional variation.[1] For surveyors conducting valuations across multiple markets, understanding these regional dynamics is essential for Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment.

Southern regions face the strongest downward pressure:

- London: -40% price sentiment

- South East: -24% price sentiment

- East Anglia: -26% price sentiment[2]

Northern and peripheral regions demonstrate resilience:

- Northern Ireland: Positive price growth

- Scotland: Continued price increases

- North West: Rising prices[2]

This geographic split reflects fundamental differences in affordability constraints, entry-price market dynamics, and regional economic conditions. Chartered surveyors in Hampstead face entirely different valuation challenges compared to professionals working in northern markets.

Valuation Adjustment Strategies for Mixed Regional Sentiment

Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment requires surveyors to implement sophisticated adjustment methodologies that account for both geographic variation and temporal market dynamics. The following strategies provide practical frameworks for navigating current market complexity.

Regional Risk Premium Adjustments

Given the dramatic variation in regional sentiment, valuation professionals must incorporate location-specific risk premiums when determining appropriate valuation figures. This approach recognizes that identical properties in different regions face fundamentally different market conditions.

For high-pressure southern markets (London, South East, East Anglia), consider:

📊 Increased marketing period assumptions: Properties in markets with -40% sentiment (London) typically require 20-30% longer marketing periods than historical averages. This should influence assessments of Market Value versus current achievable prices.

📊 Downward comparable adjustments: When recent comparable evidence predates the February sentiment decline, apply time-based adjustments of 2-4% to reflect deteriorating market conditions. Chartered surveyors in Camden and chartered surveyors in Fulham should pay particular attention to this factor.

📊 Buyer negotiation leverage factors: In markets with -26% enquiry levels, buyers possess significant negotiating power. Valuations should reflect realistic achievable prices rather than optimistic asking price evidence.

For resilient northern and peripheral markets, different considerations apply:

✅ Positive sentiment premiums: Markets showing continued price growth warrant confidence in comparable evidence without downward adjustments, provided transaction volumes support pricing levels.

✅ Supply-demand fundamentals: Northern regions with stronger entry-level affordability benefit from sustained demand. Valuations can reflect this structural advantage through reduced risk premiums.

✅ Rental yield advantages: Northern markets typically offer superior rental yields, enhancing investment property valuations relative to southern equivalents.

Comparable Evidence Weighting Methodology

The mixed sentiment environment requires careful consideration of which comparable transactions receive greatest weight in valuation analysis. Traditional approaches that prioritize recency may produce misleading results in rapidly shifting markets.

Implement a three-tier comparable weighting system:

Tier 1 (Highest Weight – 50-60%): Transactions completed within the past 8 weeks that reflect current market sentiment. These comparables capture the February 2026 market reality and should form the primary valuation foundation.

Tier 2 (Moderate Weight – 25-35%): Transactions from 8-16 weeks ago, adjusted for time-based market movement. Apply sentiment-based adjustments derived from RICS survey data to bridge the temporal gap.

Tier 3 (Supporting Evidence – 10-20%): Older transactions and asking price evidence, used primarily to establish longer-term value trends and identify anomalous pricing. These comparables provide context but should not drive valuation conclusions in current market conditions.

For chartered surveyors in North London and chartered surveyors in Islington, this tiered approach prevents over-reliance on pre-sentiment-shift evidence while maintaining sufficient comparable data for robust analysis.

Forward-Looking Valuation Adjustments

The tension between -2% near-term expectations and +17% 12-month sales expectations creates particular challenges for valuations with forward-looking elements, such as development appraisals or investment analysis.

For development valuations, consider:

🏗️ Phased sentiment assumptions: Apply current negative sentiment to near-term phases (0-6 months) while incorporating modest recovery assumptions for later phases (6-12 months), consistent with the +17% 12-month sales expectations.

🏗️ Extended sales period modeling: Increase assumed sales periods by 15-25% compared to historical norms to reflect -12% agreed sales environment and reduced transaction velocity.

🏗️ Sensitivity analysis: Given uncertainty around the timing and magnitude of recovery, conduct sensitivity testing across optimistic, base, and pessimistic scenarios that bracket the range of possible outcomes.

For investment property valuations, the rental market dynamics revealed in the February 2026 survey provide critical inputs:

- Landlord instructions remain firmly negative at -27%, signaling continued reduction in available rental stock[1]

- Tenant demand remained stable at +2% net balance, indicating consistent lettings activity[2]

- Rental prices expected to rise by +20% over the next three months, driven by supply-demand imbalance[2]

These factors suggest that investment property valuations should incorporate:

💰 Rental growth assumptions of 15-20% annually for 2026-2027, reflecting the structural supply shortage

💰 Yield compression in markets with strong rental fundamentals, particularly northern regions where rental demand remains robust

💰 Capital value support from rental income growth, potentially offsetting some capital value pressure in southern markets

Professional valuation reports in London should explicitly address these rental market dynamics when assessing investment properties.

Practical Implementation: Regional Valuation Case Studies

To illustrate how Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment translates into practical valuation decisions, consider these regional case studies that reflect the divergent market conditions revealed in the February 2026 data.

Case Study 1: Prime London Residential Property

Property Type: Four-bedroom Victorian terrace house in Hampstead

Regional Sentiment: London -40% price sentiment, -26% buyer enquiries

Valuation Challenge: Recent comparable evidence from December 2025 shows £2.1 million achieved price

Valuation Approach:

The chartered surveyors in Hampstead conducting this valuation must address the dramatic sentiment deterioration between December 2025 and February 2026. London's 12-month price expectations collapsed from +56% to just +7%—the most significant regional shift in the entire survey.[2]

Adjustment Strategy:

- Time-based adjustment: Apply -3.5% adjustment to December comparable to reflect four months of deteriorating sentiment

- Marketing period: Extend assumed marketing period from 12 weeks to 16-18 weeks given -26% enquiry environment

- Negotiation factor: Incorporate 2-3% buyer negotiation discount to reflect current market dynamics

- Adjusted valuation: £2,025,000 (representing 3.6% reduction from unadjusted comparable)

This approach recognizes that while the December transaction provides valuable evidence, current market conditions warrant meaningful downward adjustment. The valuation report should explicitly reference the RICS February 2026 survey data to support these adjustments and provide transparency to clients.

Case Study 2: Northern England Entry-Level Property

Property Type: Three-bedroom semi-detached house in Greater Manchester

Regional Sentiment: North West showing positive price growth, resilient demand

Valuation Challenge: Limited recent comparable evidence, but strong rental fundamentals

Valuation Approach:

For chartered surveyors in West London working with clients considering northern investment properties, the February 2026 survey reveals a fundamentally different market dynamic. The North West demonstrates resilience driven by entry-level affordability and sustained demand.[3]

Adjustment Strategy:

- Positive sentiment factor: No downward time adjustments required; market momentum supports comparable evidence

- Investment value enhancement: Rental yield of 6.5% (versus 3.2% London equivalent) supports premium valuation for investment buyers

- Rental growth projection: Incorporate +20% rental growth expectations over next 12 months into investment analysis

- Supply constraint premium: Limited landlord instructions (-27%) support capital value stability

This case demonstrates that Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment may actually support upward adjustments or confidence in comparable evidence in resilient regional markets, contrasting sharply with the cautious approach required in southern regions.

Case Study 3: Suburban Surrey Family Home

Property Type: Four-bedroom detached house in Guildford

Regional Sentiment: South East -24% price sentiment, mixed near-term outlook

Valuation Challenge: Balancing current weakness with 12-month recovery expectations

Valuation Approach:

Chartered surveyors in Guildford and chartered surveyors in Surrey face a middle-ground scenario—significant downward pressure but not as severe as London's -40% sentiment.

Adjustment Strategy:

- Moderate time adjustments: Apply -2% adjustment to Q4 2025 comparables to reflect sentiment deterioration

- Market positioning: Properties in desirable school catchments show greater resilience; apply reduced adjustments for prime locations

- Buyer profile consideration: Family buyers demonstrate more stable demand than investor/second-home buyers; adjust risk premiums accordingly

- Forward-looking note: Valuation report acknowledges 12-month expectations of +33% but prioritizes current transaction evidence for Market Value conclusion

This balanced approach recognizes regional headwinds while avoiding excessive pessimism that fails to reflect underlying demand from family buyers with genuine occupational need.

Rental Market Implications for Investment Valuations

The February 2026 RICS survey reveals rental market dynamics that significantly impact investment property valuations and require specific analytical considerations beyond simple comparable analysis.

Supply-Demand Imbalance and Valuation Implications

The persistent negative balance for landlord instructions at -27% represents a structural supply constraint that fundamentally alters investment property valuation parameters.[1] This supply shortage, combined with stable tenant demand at +2%, creates a landlord's market with direct valuation implications.

Key valuation adjustments for investment properties:

🏘️ Rental growth assumptions: The survey's +20% rental price expectations over three months translates to potential annual growth of 15-20%, substantially above historical norms. Investment valuations should incorporate these elevated growth rates when projecting future income streams.

🏘️ Void period reductions: Strong tenant demand and limited supply suggest reduced void periods. Adjust standard void assumptions downward from 4-6 weeks to 2-3 weeks for well-located properties.

🏘️ Yield compression potential: In markets where rental growth significantly outpaces capital value growth, yields may compress as investors recognize the income security. This is particularly relevant for northern markets combining positive capital growth with strong rental dynamics.

🏘️ Capital value floor: Robust rental income provides a valuation floor for investment properties, even in markets experiencing capital value pressure. The income return becomes increasingly important relative to capital appreciation in the current environment.

For chartered surveyors in Ealing and other London boroughs, the rental market strength partially offsets the -40% price sentiment, particularly for properties attractive to tenants.

Regional Rental Market Variations

While the national rental market shows strong fundamentals, regional variations require location-specific analysis:

London and South East: Despite capital value pressure, rental demand remains robust due to:

- Continued employment concentration in major urban centers

- Reduced home ownership affordability pushing households into rental sector

- International tenant demand recovery post-pandemic

Northern regions: Rental markets benefit from:

- Stronger affordability ratios making rental properties accessible to broader tenant base

- Limited new rental supply due to landlord exit from sector

- Growing recognition of northern cities as employment hubs

Investment property valuations must reflect these regional rental dynamics through location-specific yield and growth assumptions. A Red Book valuation in London for an investment property requires fundamentally different rental assumptions than an equivalent northern property.

Technical Valuation Reporting Considerations

The complex market environment revealed by the February 2026 RICS survey creates specific technical requirements for valuation reports that meet professional standards while providing clients with transparent, defensible conclusions.

Assumptions and Special Assumptions

Valuation reports prepared in the current environment should explicitly address market uncertainty through carefully crafted assumptions:

Standard assumptions requiring emphasis:

- Marketing period assumptions should be explicitly stated and justified with reference to regional enquiry levels

- Purchaser profile assumptions (owner-occupier versus investor) significantly impact achievable prices in current market

- Condition assumptions carry heightened importance given reduced buyer appetite for properties requiring work

Special assumptions to consider:

- In development valuations, consider special assumptions regarding phased sales rates reflecting evolving market sentiment

- For portfolio valuations, special assumptions regarding disposal strategy (simultaneous versus phased) materially impact aggregate value

Market Uncertainty Clauses

The tension between near-term weakness (-2% expectations) and 12-month optimism (+17% expectations) justifies inclusion of market uncertainty clauses that:

✔️ Reference the RICS February 2026 survey data explicitly

✔️ Acknowledge the elevated uncertainty regarding timing and magnitude of recovery

✔️ Note that valuations may require review if market conditions materially change

✔️ Distinguish between current Market Value and potential future value trajectories

These clauses protect both valuer and client by establishing appropriate context for valuation conclusions in an uncertain environment.

Regional Context and Comparables Commentary

Given the dramatic regional variation in sentiment, valuation reports must provide robust regional context:

Essential report elements:

- Explicit statement of regional price sentiment from RICS survey (-40% London, positive Northern Ireland, etc.)

- Commentary on how regional sentiment influences comparable selection and weighting

- Analysis of local market transaction volumes and their impact on comparable reliability

- Discussion of regional rental market dynamics for investment properties

Professional chartered surveyors in London should ensure their reports distinguish between London-specific conditions and broader national trends, given London's uniquely negative sentiment profile in the February 2026 data.

Long-Term Strategic Considerations for Valuation Practice

Beyond immediate valuation adjustments, the February 2026 RICS survey data suggests longer-term strategic considerations for valuation practices navigating mixed regional sentiment environments.

Building Regional Market Intelligence

The dramatic regional divergence revealed in the survey underscores the importance of developing deep local market knowledge. Valuation practices should:

📈 Establish regional data tracking systems that monitor local sentiment indicators beyond national survey data

📈 Develop relationships with local agents across multiple regions to supplement formal market data

📈 Create regional adjustment matrices that systematically capture location-specific factors influencing valuations

📈 Invest in local market presence through regional offices or associate networks, particularly for practices serving multiple geographic markets

Firms providing services across diverse markets—from chartered surveyors in Oxfordshire to chartered surveyors in Hampshire—require robust systems for translating regional market intelligence into valuation adjustments.

Technology and Data Analytics

The complexity of Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment suggests opportunities for enhanced data analytics:

- Automated comparable adjustment tools that incorporate real-time sentiment data from RICS and other sources

- Regional risk modeling that quantifies uncertainty ranges around valuation conclusions

- Rental market analytics that track supply-demand indicators and project rental growth trajectories

- Portfolio-level analysis tools that aggregate regional variations for multi-property valuations

Investment in these capabilities positions valuation practices to navigate future market complexity more effectively.

Client Communication and Education

The divergence between near-term weakness and longer-term optimism creates client communication challenges. Effective practices should:

💬 Proactively educate clients about regional market variations and their valuation implications

💬 Provide scenario analysis showing valuation ranges under different market evolution paths

💬 Distinguish between valuation advice and market timing advice, maintaining professional boundaries

💬 Reference authoritative data sources like the RICS survey to support valuation conclusions and build client confidence

Clear communication about market complexity builds client trust and reduces disputes over valuation conclusions that may differ from client expectations.

Conclusion: Navigating Mixed Sentiment Through Rigorous Methodology

The February 2026 RICS Residential Market Survey presents valuation professionals with one of the most challenging market environments in recent years: sharp near-term weakness with buyer enquiries at -26%, dramatic regional divergence spanning from London's -40% sentiment to positive northern growth, and persistent long-term optimism at +33% despite immediate headwinds.[1][2][3]

Valuing Properties Under RICS February 2026 Residential Survey: Strategies for Mixed Regional Sentiment requires abandoning simplistic national approaches in favor of sophisticated methodologies that:

✅ Incorporate regional risk premiums reflecting location-specific sentiment and market dynamics

✅ Weight comparable evidence according to recency and market relevance, with time-based adjustments for sentiment shifts

✅ Balance near-term transaction evidence with forward-looking market expectations in a transparent, defensible manner

✅ Recognize rental market strength as a critical factor supporting investment property valuations despite capital value pressure

✅ Provide robust reporting that explicitly addresses market uncertainty and regional variation

The rental market dynamics—with landlord instructions at -27% and rental price expectations at +20%—offer a silver lining for investment property valuations, particularly in northern regions where capital growth and rental strength combine favorably.[1][2]

Actionable Next Steps for Valuation Professionals

- Review and update regional adjustment matrices to reflect February 2026 sentiment data across all markets served

- Implement tiered comparable weighting systems that prioritize recent transaction evidence while maintaining sufficient data for robust analysis

- Enhance valuation reports with explicit market uncertainty clauses and regional context referencing RICS survey data

- Develop rental market analysis capabilities to properly value investment properties in the current supply-constrained environment

- Invest in continuing professional development focused on valuation in uncertain markets and regional market analysis

- Establish regular review cycles for valuation methodologies as market conditions evolve throughout 2026

For chartered surveyors working across London and the South East—from chartered surveyors in Richmond to chartered surveyors in Weybridge—the current environment demands particular vigilance given the severe sentiment deterioration in these regions.

The path forward requires rigorous methodology, transparent reporting, and recognition that valuation is both art and science—particularly when navigating the mixed regional sentiment that defines the UK residential property market in 2026. By implementing the strategies outlined in this guide, valuation professionals can provide clients with defensible, professional advice that acknowledges market complexity while maintaining the highest standards of the surveying profession.

References

[1] Rics Update On The Rental Market February 2026 – https://www.oakwoodpropertyservices.co.uk/rics-update-on-the-rental-market-february-2026/

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/