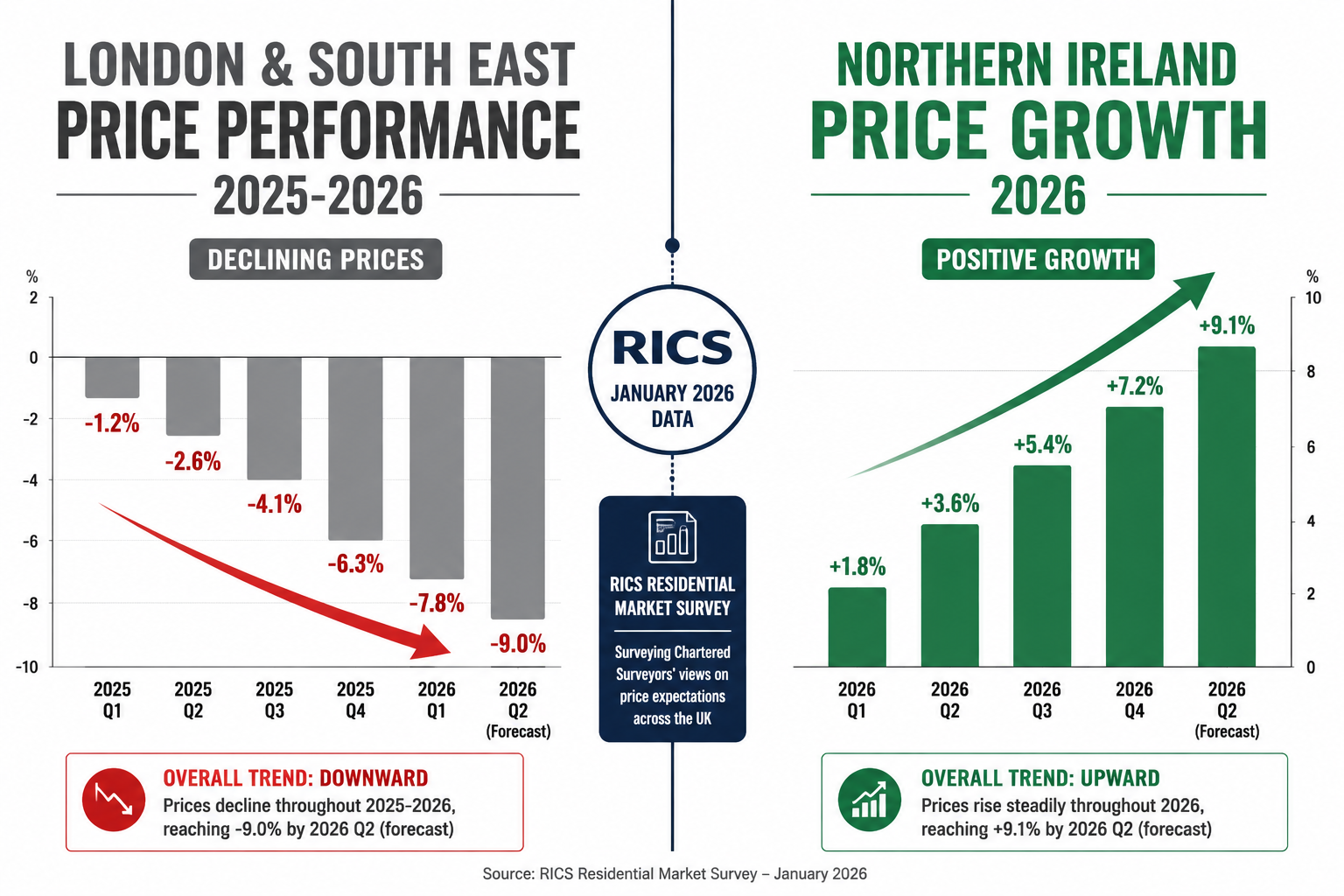

Northern Ireland stands as one of only two UK regions reporting consistent upward price trends in the RICS UK Residential Market Survey for January 2026 — a striking contrast to the stagnation gripping London and the South East [1]. For buyers, sellers, and surveyors operating in this accelerating market, the Northern Ireland property boom post-RICS Jan 2026 demands building survey strategies for valuation accuracy in upward markets that go well beyond standard practice. Getting the survey and valuation right in a rising market is not just good professional practice — it is financial protection.

Key Takeaways 📋

- Northern Ireland is outperforming most UK regions on price growth, confirmed by RICS January 2026 data, making robust building surveys essential for accurate valuations.

- A Level 3 Building Survey (formerly Full Structural Survey) is the gold standard for buyers in upward markets where hidden defects can be masked by price momentum.

- Valuation adjustments must reflect local comparables, not national averages — Northern Ireland's divergence from southern markets makes this critical.

- 12-month price expectations are strongly positive, with +43% of RICS respondents anticipating higher prices, but surveyors must avoid "market optimism bias" in their assessments [1].

- Survey demand is rising alongside transaction volumes, meaning early instruction of a qualified surveyor is more important than ever.

Understanding the Northern Ireland Market in 2026

What the RICS January 2026 Data Actually Shows

The January 2026 RICS UK Residential Market Survey confirmed what many Belfast estate agents had already sensed on the ground: Northern Ireland's housing market is moving in a fundamentally different direction from much of England [1]. The national house price net balance improved from -19% in October 2025 to -10% by January 2026, signalling broad stabilisation [4]. But Northern Ireland and Scotland are the outliers — they are not stabilising. They are actively growing.

Key headline figures from the January 2026 RICS survey:

| Indicator | National Net Balance | Northern Ireland Trend |

|---|---|---|

| House Price Balance | -10% | Positive / Upward |

| New Buyer Enquiries | -15% (improved from -29%) | Improving |

| Agreed Sales | -9% (least negative since June 2025) | Recovering strongly |

| 12-Month Price Expectations | +43% | Above national average |

Sources: [1][4]

New buyer enquiries improved from -29% in November 2025 to -15% in January 2026 — a significant easing of downward pressure [1]. Agreed sales recovered to their least negative reading since June 2025, at a net balance of -9% [2]. This increased transaction volume directly drives demand for survey and valuation services across Northern Ireland.

💬 "Recovery depends heavily on the trajectory of mortgage rates and broader macro confidence over the coming months." — RICS Chief Economist [2]

More affordable borrowing rates compared to 12–24 months prior are motivating buyers to act, particularly for smaller houses — a property type where survey respondents noted "considerably" improved activity since the start of 2026 [2]. This matters for surveyors: the type of property being transacted shapes which survey level is most appropriate.

Why Northern Ireland Diverges from Southern England

Regional disparities are widening across the UK. While Northern Ireland posts gains, London and the South East continue to lag [1]. This divergence has a direct practical implication: comparable property selection for Northern Ireland valuations must be rigorously local. Applying national averages or drawing on southern market data will distort valuations in either direction.

Understanding the key valuation factors that drive regional pricing — including local employment, infrastructure investment, and housing supply constraints — is essential context for any surveyor working in Northern Ireland's current market.

Northern Ireland Property Boom Post-RICS Jan 2026: Building Survey Strategies for Valuation Accuracy in Upward Markets

Why Standard Surveys Fall Short in Rising Markets

In a rising market, there is a dangerous psychological dynamic at play: buyers feel pressure to move quickly, and sellers feel confident enough to disclose less. The result is that structural defects, damp issues, and maintenance backlogs can be overlooked in the rush to transact. A HomeBuyer Report (Level 2) may satisfy a mortgage lender but will not provide the depth of investigation needed when paying a premium price in a competitive market.

Understanding the difference between a HomeBuyer Report and a Building Survey is the first strategic decision any buyer in Northern Ireland's 2026 market must make. The short version: in an upward market with rising prices, a Level 3 Building Survey is almost always the better investment.

The Level 3 Building Survey Checklist for Northern Ireland Properties 🏠

Northern Ireland's housing stock has particular characteristics — Victorian and Edwardian terraces in Belfast, rural farmhouses in County Down and Antrim, and a significant proportion of pre-1919 construction with solid walls rather than cavity walls. Each property type carries specific survey priorities.

Level 3 Building Survey Checklist — Northern Ireland Focus:

Structural Integrity

- ✅ Foundation condition and evidence of settlement or subsidence

- ✅ Roof structure — rafters, purlins, ridge board, and sarking felt

- ✅ Chimney stacks and flashings (common in older Belfast stock)

- ✅ Wall ties in cavity wall properties (1930s–1980s construction)

- ✅ Lintel condition above door and window openings

Moisture and Dampness

- ✅ Rising damp at ground floor level

- ✅ Penetrating damp through solid walls (pre-1919 properties)

- ✅ Roof space condensation and ventilation adequacy

- ✅ Subfloor void condition and ventilation (suspended timber floors)

Services and Installations

- ✅ Electrical installation age and condition (pre-2000 wiring)

- ✅ Heating system — oil-fired central heating is common in rural NI

- ✅ Plumbing condition including lead pipework in older properties

- ✅ Drainage — including septic tanks in rural locations

External Elements

- ✅ Boundary walls and outbuildings

- ✅ Render condition on external walls

- ✅ Guttering, downpipes, and surface water drainage

- ✅ Evidence of previous extensions or alterations

For complex structural concerns identified during a survey, a residential structural engineer's report provides the specialist depth that a general building survey cannot always offer.

Valuation Accuracy Strategies in an Upward Market

Valuation in a rising market carries its own set of professional risks. The core challenge: comparable evidence always lags the market. Completed sales used as comparables may be 3–6 months old, potentially understating current values — but also potentially masking a short-term spike that will correct.

Five Valuation Adjustment Strategies for Northern Ireland's 2026 Market:

-

Time-adjust comparables — Apply a percentage uplift to sales evidence older than 3 months, using RICS-endorsed local price indices to calibrate the adjustment.

-

Weight local over regional — Given Northern Ireland's divergence from UK-wide trends, comparables within a 1-mile radius carry significantly more weight than broader regional data.

-

Distinguish property type — With smaller houses showing stronger activity than flats [2], ensure the comparable pool matches the subject property type precisely. Flat-to-house comparisons will distort figures.

-

Account for condition premium — In a rising market, well-maintained properties command a disproportionate premium. Survey findings that reveal deferred maintenance should trigger a downward condition adjustment.

-

Avoid market optimism bias — The +43% positive 12-month price expectation from RICS respondents [1] is sentiment data, not evidence. Valuations must be grounded in completed transactions, not forecasts.

For a deeper understanding of how professional valuations are structured and priced, the RICS valuation cost guide provides useful context on what a robust valuation instruction should include.

Protecting Buyers: Survey and Valuation Integration in Practice

When Survey Findings Should Trigger Valuation Renegotiation

One of the most underused buyer protections in any property transaction is the survey-to-valuation feedback loop. A building survey that identifies significant defects should directly inform the valuation figure — and, where appropriate, trigger a renegotiation of the agreed purchase price.

In Northern Ireland's current upward market, sellers may resist price reductions. But a detailed specific defect report quantifying the cost of remedial works provides objective evidence that is difficult to argue against. Common defects that justify price adjustments in Northern Ireland properties include:

- Roof replacement — £8,000–£20,000+ depending on property size

- Damp-proof course installation — £2,500–£8,000

- Rewiring — £4,000–£12,000 for a typical terrace

- Structural repairs — highly variable; specialist quotes essential

- Septic tank replacement (rural properties) — £5,000–£15,000

The Role of RICS Red Book Valuations in Upward Markets

For mortgage purposes, a RICS Red Book valuation provides the lender's security assessment. In a rising market, there is a real risk of mortgage valuation shortfall — where the agreed sale price exceeds the lender's valuation. This is particularly relevant for Northern Ireland buyers stretching to compete in a hot market.

Understanding how RICS registered valuers approach market value assessment — including their obligation to reflect current market evidence rather than aspirational pricing — helps buyers set realistic expectations before exchange.

Reinstatement Cost Assessments: Don't Overlook Insurance Accuracy 🔥

Rising property values in Northern Ireland also affect buildings insurance reinstatement costs. As market values increase, many homeowners fail to update their reinstatement cost assessment, leaving themselves underinsured. A reinstatement cost valuation ensures insurance cover reflects the actual rebuild cost — which is driven by construction costs, not market prices.

This is especially important for older Northern Ireland properties where construction methods (solid brick, natural slate, lime mortar) make reinstatement costs significantly higher than standard modern build equivalents.

Northern Ireland Property Boom Post-RICS Jan 2026: Practical Guidance for Surveyors and Buyers

Timing Your Survey Instruction

With agreed sales recovering and transaction volumes increasing [2], the practical reality in 2026 is that surveyors in Northern Ireland are busier. Instructing a survey early — ideally immediately after an offer is accepted — reduces the risk of delays that could jeopardise a transaction in a competitive market.

The Q1 2026 characterisation of Northern Ireland's housing market as "stable and resilient" [3] suggests this elevated demand is not a short-term spike. Buyers should plan for survey turnaround times of 2–3 weeks for a Level 3 Building Survey, and factor this into their transaction timeline.

Choosing the Right Survey Level: A Quick Decision Guide

| Property Type | Age | Recommended Survey |

|---|---|---|

| Modern new-build | Post-2000 | Snagging Report |

| Standard terrace/semi | 1930s–1980s | Level 2 HomeBuyer Report |

| Victorian/Edwardian terrace | Pre-1919 | Level 3 Building Survey |

| Rural farmhouse/cottage | Pre-1919 | Level 3 Building Survey |

| Converted flat | Any age | Level 2 minimum; Level 3 if older |

| Extended/altered property | Any age | Level 3 Building Survey |

For properties with specific concerns — particularly older roofs — a dedicated drone roof survey can provide detailed visual evidence without the need for scaffolding, reducing cost and time while improving inspection quality.

Key Questions to Ask Your Surveyor Before Instruction

Before appointing a surveyor in Northern Ireland's current market, buyers should ask:

- Are you RICS-regulated? — Non-regulated surveyors offer no professional indemnity protection.

- What level of survey do you recommend for this property? — A good surveyor will tailor their recommendation to the specific property, not default to the cheapest option.

- Will your report include reinstatement cost guidance? — Useful for insurance purposes.

- How will you handle defects that require specialist investigation? — The report should clearly flag items needing further expert assessment.

- What is your turnaround time? — Critical in a fast-moving market.

Conclusion: Navigating Northern Ireland's Rising Market with Confidence

The Northern Ireland property boom post-RICS Jan 2026 presents real opportunities — but also real risks for buyers who move too quickly without proper due diligence. The RICS January 2026 data is unambiguous: Northern Ireland is one of the UK's strongest-performing regions, with positive price momentum, recovering transaction volumes, and strongly positive 12-month expectations [1][4]. That is good news for the market. But rising prices do not make buildings structurally sound.

Actionable Next Steps for Buyers in Northern Ireland's 2026 Market:

- ✅ Instruct a Level 3 Building Survey for any property built before 1980 or showing signs of alteration

- ✅ Use a RICS-regulated surveyor with demonstrable experience in Northern Ireland's specific housing stock

- ✅ Request a reinstatement cost assessment alongside the survey to protect insurance adequacy

- ✅ Ensure valuation comparables are hyper-local — national data will not reflect Northern Ireland's divergent performance

- ✅ Build survey time into your transaction timeline — allow 2–3 weeks minimum for a quality Level 3 report

- ✅ Use survey findings as a negotiation tool — defect costs are objective evidence in any price renegotiation

The combination of a thorough building survey and a carefully calibrated RICS valuation is the most powerful protection any buyer can have in a rising market. In Northern Ireland in 2026, that protection is not optional — it is essential.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Residential Market Shows Signs Of Early Recovery In January 2026 RICS – https://theintermediary.co.uk/2026/02/residential-market-shows-signs-of-early-recovery-in-january-2026-rics/

[3] Report Points To Stable And Resilient Housing Market – https://www.insidermedia.com/news/ireland/report-points-to-stable-and-resilient-housing-market

[4] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf