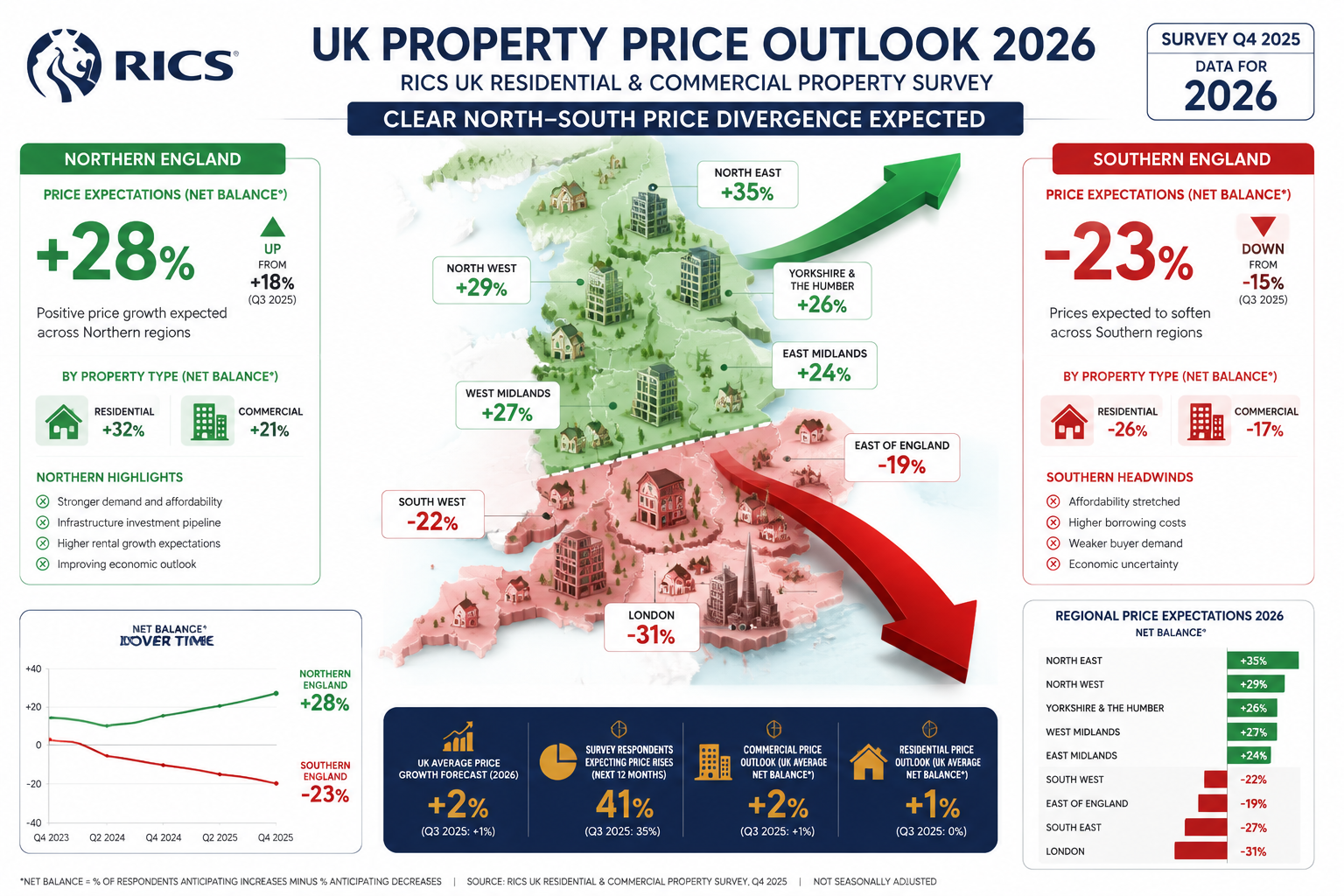

A 39% decline in buyer enquiries recorded in the February 2026 RICS survey does not affect every region equally — and that gap is precisely where valuation errors are made. The divergence between Northern growth momentum and Southern market caution has created a two-speed recovery that demands region-specific methodology, not a single national approach. Understanding Valuation Adjustments for 2026 Two-Speed Recovery: North-South Strategies from RICS Insights is now a core professional requirement for any chartered surveyor operating across England's contrasting property markets.

Key Takeaways

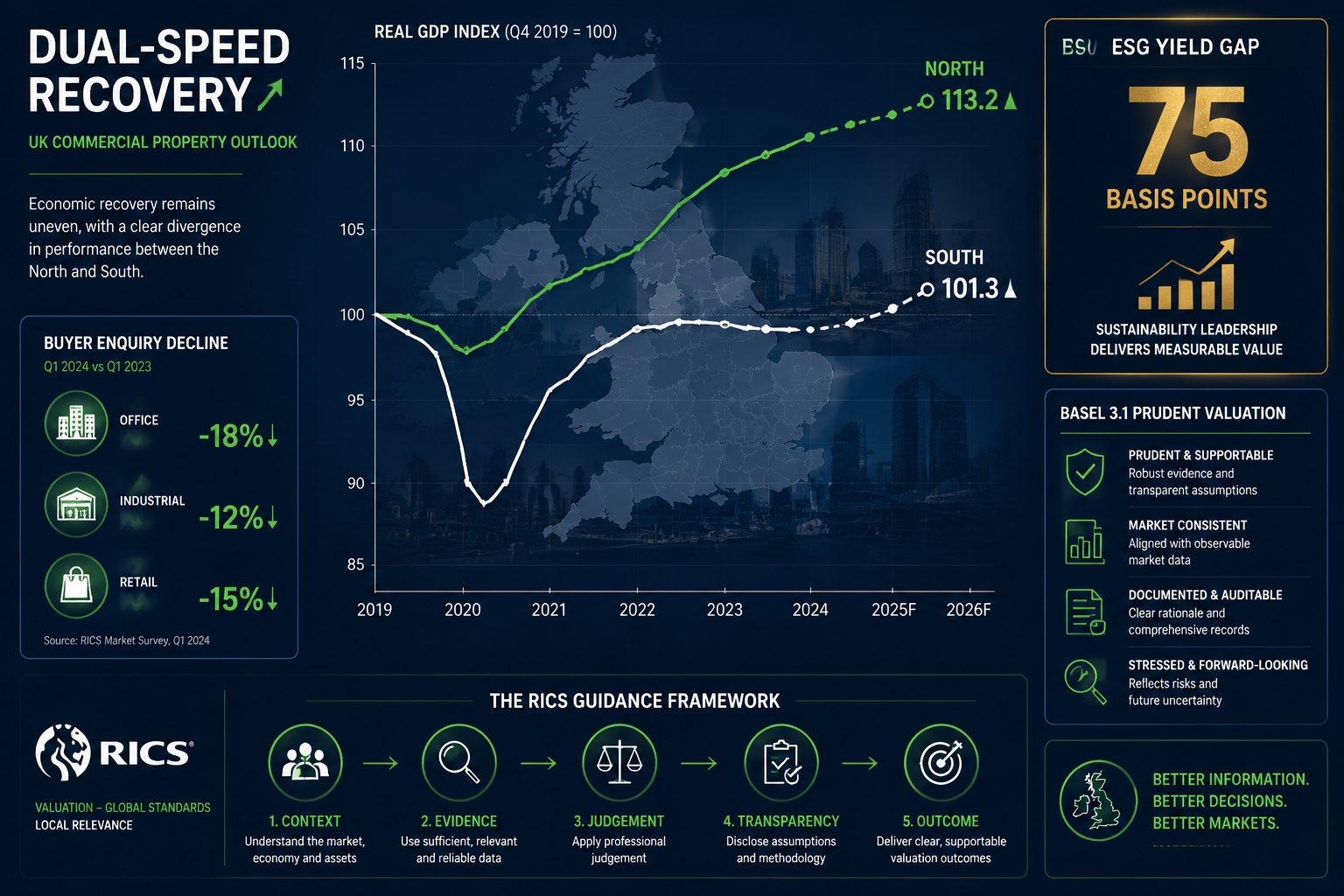

- The 2026 UK property market is recovering at two distinct speeds, with Northern regions showing stronger price growth while Southern markets — including London — face downward pressure and declining buyer activity.

- RICS February 2026 data recorded a -1.9% monthly price decline in London, requiring surveyors to apply downward time adjustments and prioritise very recent comparables.

- From April 2026, RICS mandates that ESG factors be treated as explicit valuation criteria, creating a yield gap of up to 75 basis points between energy-efficient and less efficient assets.

- Prudent valuation models aligned with Basel 3.1/CRR3 now distinguish formally between Market Value, Mortgage Lending Value, and conservative prudential adjustments.

- Surveyors must adopt dual-horizon valuation methods, segmenting by buyer financing certainty, property type, and regional supply-demand dynamics.

Understanding the Two-Speed Recovery in 2026

Morgan Stanley's April 2026 real estate outlook confirmed what many practitioners had already observed on the ground: the global real estate recovery is uneven, with industrial and residential sectors outperforming while office and life sciences markets continue to struggle [2]. In England, this global pattern maps closely onto a North-South geographic divide.

Northern cities — particularly Manchester, Leeds, and Sheffield — have benefited from continued infrastructure investment, population growth, and relative affordability compared to the South. Buyer demand has remained comparatively resilient, supported by first-time buyer activity and investor interest in higher-yielding stock. Southern markets, particularly Greater London and the Home Counties, face a different set of pressures: elevated price-to-income ratios, sensitivity to mortgage rate movements, and a buyer pool that has grown markedly more cautious.

The core challenge for valuers is this: applying a single national methodology to a market behaving in two distinct ways produces inaccurate appraisals. Overvaluing in a softening Southern market creates lending risk. Undervaluing in a recovering Northern market disadvantages sellers and distorts comparable evidence for future instructions.

What the RICS February 2026 Data Shows

The RICS February 2026 residential survey provided granular evidence of this divergence:

- London recorded a -1.9% monthly price movement, with surveyors reporting that recent comparables were rapidly becoming stale [3].

- Northern regions showed positive survey balances, with net positive readings on both new buyer enquiries and agreed sales.

- Nationally, buyer enquiries fell by a net balance of 39%, but this aggregate figure masked significant regional variation [4].

For surveyors preparing valuation reports in London, the practical implication is clear: comparable evidence from even three to four months prior may no longer reflect current market conditions. Time adjustments — typically applied as a percentage correction to older comparables — must be applied more aggressively in softening markets and calibrated carefully in rising ones.

Techniques for Handling North-South Divergences in Valuation Practice

Applying Valuation Adjustments for 2026 Two-Speed Recovery: North-South Strategies from RICS Insights in practice requires a structured set of methodological choices. The following techniques reflect current RICS guidance and emerging best practice.

Dual-Horizon Comparable Analysis

In a two-speed market, the standard approach of selecting three to five recent comparables within a 12-month window is insufficient. Surveyors are now advised to adopt a dual-horizon approach:

| Horizon | Timeframe | Weighting | Application |

|---|---|---|---|

| Short-horizon | 0-3 months | Primary (60-70%) | Active market conditions |

| Medium-horizon | 3-12 months | Secondary (30-40%) | Trend confirmation only |

| Long-horizon | 12+ months | Excluded or heavily discounted | Background context |

In Northern markets with positive price momentum, medium-horizon comparables may still be usable but should be adjusted upward to reflect current conditions. In London and the wider South East, the opposite applies: older comparables must be adjusted downward, and surveyors should prioritise evidence from the most recent weeks rather than months [3].

Segmenting by Buyer Financing Certainty

The 39% decline in buyer enquiries nationally reflects not just reduced demand but a shift in the composition of remaining buyers [4]. Cash buyers and those with mortgage agreements in principle represent a more reliable demand signal than speculative enquiries. Surveyors are advised to:

- Identify the likely buyer profile for the subject property (cash purchaser, mortgaged first-time buyer, investor).

- Weight comparables accordingly, favouring transactions completed by buyers with similar financing profiles.

- Apply a supply-demand adjustment where local stock levels are materially above or below the long-run average.

This segmentation approach is particularly relevant for shared ownership valuations, where the buyer pool is restricted and financing structures differ significantly from the open market.

Time Adjustments: Quantifying the Correction

RICS guidance does not prescribe a fixed time adjustment percentage, but the February 2026 data provides a basis for calibration. A -1.9% monthly movement in London implies that a comparable from six months ago may require a downward adjustment of approximately 10-12% to reflect current conditions — a material correction that can shift a valuation by tens of thousands of pounds on an average London property [3].

For Northern markets showing positive monthly movements, the adjustment direction reverses. A comparable from six months ago in a market growing at 0.5% per month may need an upward adjustment of 3-4%.

Key principle: Time adjustments must be explicitly stated in the valuation report, with the data source and calculation methodology documented. This is not optional under current RICS Red Book standards. For surveyors seeking clarity on Red Book valuation requirements in London, documenting these adjustments transparently is a professional obligation.

Applying Granular Local Data

National and regional averages are a starting point, not a conclusion. Surveyors should draw on:

- Local authority-level Land Registry data, filtered to the most recent 90 days.

- Active listing analysis, comparing asking prices to achieved prices to identify discounting trends.

- Days-on-market metrics, which signal demand strength more immediately than transaction prices.

- Mortgage approval data from the Bank of England, disaggregated where possible by region.

RICS registered valuers in London are expected to demonstrate familiarity with all of these data sources when supporting their comparable selection.

ESG Mandates and the Green Premium in 2026 Valuations

No discussion of Valuation Adjustments for 2026 Two-Speed Recovery: North-South Strategies from RICS Insights is complete without addressing the ESG dimension. From April 30, 2026, RICS published the fourth edition of its global professional standard on ESG and sustainability in commercial property valuation, establishing a clear framework for integrating environmental, social, and governance factors into valuation advice worldwide [1].

This is not a theoretical shift. Research from 2026 indicates a yield gap of up to 75 basis points between energy-efficient ("green") assets and less efficient ("brown") assets [6]. In practical terms:

- A commercial property with an EPC rating of A or B may command a lower yield (higher capital value) than an equivalent building rated D or E.

- The "brown discount" — the value penalty applied to poorly performing assets — is becoming increasingly quantifiable and must be reflected in formal valuations.

- For residential property, EPC ratings are now a material valuation factor, not merely a disclosure requirement.

North-South ESG Implications

The ESG adjustment does not apply uniformly across regions. In London and major Southern cities, where institutional buyers dominate certain sectors, the green premium is already well-established and actively priced into transactions. In Northern markets, the green premium is emerging but less consistently reflected in comparable evidence.

This creates a methodological challenge: surveyors in Northern markets may have limited comparable evidence for green-premium adjustments and must rely more heavily on income-based or cost-based approaches to quantify the ESG uplift or discount. RICS's three core valuation approaches — market, income, and cost — each offer tools for this purpose [9].

For commercial property instructions, the commercial property surveyors in London context is instructive: ESG-related adjustments are now a standard component of any institutional-grade appraisal, and surveyors who fail to address them risk producing reports that do not meet professional standards.

Prudent Valuation and Bank Lending Considerations

The Basel 3.1/CRR3 regulatory framework has introduced new requirements for how lenders assess property collateral, and RICS has responded with updated guidance on bank lending valuations [7]. Surveyors instructed by lenders must now navigate three distinct value concepts:

- Market Value (MV): The estimated amount for which a property would exchange on the date of valuation between a willing buyer and a willing seller.

- Mortgage Lending Value (MLV): A more conservative, long-term sustainable value that strips out cyclical market fluctuations.

- Prudential Valuation Adjustments: Additional conservative haircuts applied by lenders under Basel 3.1 to account for model uncertainty and market illiquidity [5].

In a two-speed market, the gap between Market Value and Mortgage Lending Value can be significant. In a softening Southern market, MLV may already be below current MV, meaning lenders are effectively applying a forward-looking discount. In a rising Northern market, the relationship may be reversed in the short term, but MLV disciplines lenders against over-lending into cyclical peaks.

Surveyors providing valuation services in London for lending purposes must be explicit about which value basis applies to each instruction and must document the rationale for any adjustments between MV and the prudential figure.

Practical Checklist for Lending Valuations in 2026

- Confirm the instructed basis of value (MV, MLV, or other) in writing before commencing.

- Apply time adjustments to all comparables older than 90 days in softening markets.

- Document ESG factors and their quantified impact on value.

- State explicitly whether the valuation reflects current market conditions or a longer-term sustainable view.

- Cross-reference against active listing data to identify any disconnect between asking prices and achieved prices.

Strategies for Specific Property Types and Scenarios

Residential Valuations in Cautious Southern Markets

For standard residential instructions in London and the South East, the cautious spring 2026 market demands a conservative approach to comparable selection [10]. Surveyors should:

- Exclude comparables where the sale was agreed more than four months ago unless a time adjustment is applied.

- Flag any comparable where the original asking price was reduced before exchange, as this signals genuine market softening rather than an outlier.

- Consider the impact of leasehold reform on flats with short leases — a factor that is particularly acute in London. For context on lease-related valuation complexity, see the guidance on lease extension valuations in London.

Commercial and Mixed-Use in Northern Markets

Northern commercial markets are showing stronger fundamentals, particularly in logistics, industrial, and mixed-use regeneration schemes. However, the office sector remains challenged even in Northern cities, and surveyors should not assume that regional resilience applies uniformly across all asset classes [2].

For rent review valuations in London and Northern commercial markets alike, the income approach remains the primary methodology, but ESG adjustments to the capitalisation rate are now expected to be explicitly addressed.

Retrospective Valuations

In a market where conditions are changing rapidly, retrospective property valuations require particular care. The valuer must reconstruct the market conditions as they existed at the historic date, using only evidence that was available at that time. In a two-speed market, this means identifying which regional trend was operative at the relevant date — not applying current conditions retrospectively.

Conclusion

The two-speed recovery of 2026 is not a temporary anomaly — it reflects structural differences in affordability, demand composition, and economic fundamentals between Northern and Southern England. For surveyors, the professional response is methodological precision: granular time adjustments, dual-horizon comparable analysis, explicit ESG quantification, and clear documentation of the value basis used for each instruction.

Actionable next steps for practitioners:

- Review all active instructions to confirm that comparable evidence is within the 90-day window for softening markets, or that time adjustments are explicitly documented.

- Integrate ESG rating data into every commercial valuation report from this point forward, quantifying the green premium or brown discount where comparable evidence supports it.

- Confirm the instructed basis of value on all lending instructions, distinguishing clearly between Market Value and any prudential adjustments required under Basel 3.1.

- Build a regional data library of local authority-level transaction data, updated monthly, to support defensible comparable selection across different market conditions.

- For complex or high-value instructions, consider whether an RICS valuation cost review is warranted to ensure the fee reflects the increased analytical complexity of current market conditions.

The surveyors who will produce the most defensible, accurate appraisals in 2026 are those who treat the North-South divergence not as a complication but as a core input to their methodology — and who document every adjustment with the rigour that RICS standards demand.

References

[1] RICS Publishes Updated Global Standard ESG Sustainability Commercial Property Valuation – https://www.rics.org/news-insights/rics-publishes-updated-global-standard-esg-sustainability-commercial-property-valuation?utm_source=openai

[2] Real Estate Market Outlook 2026 Recovery – https://www.morganstanley.com/insights/articles/real-estate-market-outlook-2026-recovery?utm_source=openai

[3] Valuation Adjustments In Regional Divergences RICS February 2026 Data For Surveyors In London Vs North – https://www.canterburysurveyors.com/blog/valuation-adjustments-in-regional-divergences-rics-february-2026-data-for-surveyors-in-london-vs-north/?utm_source=openai

[4] Valuing Properties Amid February 2026 RICS Buyer Enquiry Slump North South Surveyor Strategies – https://manchestersurveyors.com/valuing-properties-amid-february-2026-rics-buyer-enquiry-slump-north-south-surveyor-strategies/?utm_source=openai

[5] Prudent Valuation – https://community.rics.org/viewdocument/prudent-valuation?utm_source=openai

[6] Germany ESG Green Premium Brown Discount 2026 – https://neospaces.de/en/insights/germany-esg-green-premium-brown-discount-2026-06-03?utm_source=openai

[7] RICS Updates Global Guidance On Bank Lending Valuations With Two Key Publications – https://www.rics.org/news-insights/rics-updates-global-guidance-on-bank-lending-valuations-with-two-key-publications?utm_source=openai

[9] APC 5 Valuation Methods – https://ww3.rics.org/uk/en/journals/property-journal/apc-5-valuation-methods.html?utm_source=openai

[10] Valuation Adjustments For Cautious Spring 2026 Housing Market RICS February Insights On Buyer Demand Dips And Regional Price Flatness – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-cautious-spring-2026-housing-market-rics-february-insights-on-buyer-demand-dips-and-regional-price-flatness?utm_source=openai