{"cover":"Professional landscape format (1536x1024) hero image featuring bold text overlay 'Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors' in extra large 72pt white sans-serif font with dark shadow effect, centered in upper third. Background shows modern British chartered surveyor conducting property inspection with tablet device, architectural blueprints, and residential property in soft focus. Color scheme: deep navy blue, professional white, gold accents representing RICS standards. High contrast, magazine cover quality, editorial style with professional authority. Composition includes subtle overlay of government reform documents and survey report graphics to represent regulatory transformation.","content":["Detailed landscape format (1536x1024) infographic showing timeline transformation of homebuying process, split-screen comparison of 'Current 2026 Process' versus 'Proposed Reformed Process' with survey positioning highlighted in bright yellow. Left side shows traditional timeline with survey occurring mid-transaction, right side shows upfront mandatory survey at beginning. Include calendar icons, percentage statistics showing 30-50% demand increase, clock symbols representing timeline shifts, and professional surveyor silhouettes. Clean modern design with blue and white color scheme, arrow graphics showing workflow progression, RICS compliance badges, and data visualization elements representing volume spikes in survey requests.","Professional landscape format (1536x1024) conceptual illustration depicting surveyor workflow transformation with three-panel progression showing 'preparation,' 'adaptation,' and 'implementation' phases. Central panel features chartered surveyor with modern digital tools including drone technology for roof surveys, thermal imaging equipment, and tablet-based reporting systems. Background includes training certification symbols, technology integration icons, capacity planning charts showing staffing projections, and quality assurance checkmarks. Color palette of professional blues, greens representing growth, and white highlights. Include subtle overlay of UK map showing regional demand variations with heat-map styling indicating stronger activity in North and Midlands regions.","Detailed landscape format (1536x1024) data visualization dashboard showing market recovery indicators and survey demand projections for 2026. Features multiple chart types: line graph showing RICS sentiment index climbing to +35%, bar chart comparing buyer enquiry improvements from -29% to -15%, pie chart illustrating 80% buyer support for binding offers, and upward trending arrow showing mortgage rate improvements from 5% to 3.5%. Include professional financial aesthetic with navy blue backgrounds, gold accent highlights, percentage annotations clearly visible, property transaction icons, and first-time buyer demographic symbols. Clean modern infographic style with clear data hierarchy and professional typography suitable for surveying industry context."]}

The British property market stands on the brink of its most significant transformation in decades. 🏠 As government consultations advance toward making property condition assessments a mandatory upfront requirement, chartered surveyors face an unprecedented shift in how, when, and at what volume they deliver their services. The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors represents not merely an incremental change but a fundamental restructuring of the profession's operational landscape.

With projections indicating a 30-50% surge in survey demand[6], the surveying profession must prepare for volume spikes, timeline shifts, and new service delivery models that align with RICS standards while meeting accelerated market expectations. This comprehensive analysis examines how these reforms will reshape surveyor workflows, what preparation strategies professionals should implement now, and how to position practices for success in this transformed regulatory environment.

Key Takeaways

- Mandatory upfront surveys could increase demand by 30-50%, representing the most significant growth driver for the surveying profession in years[6]

- Timeline transformation shifts surveys from mid-transaction to initial steps, fundamentally restructuring when surveyors are commissioned and how quickly reports must be delivered[1]

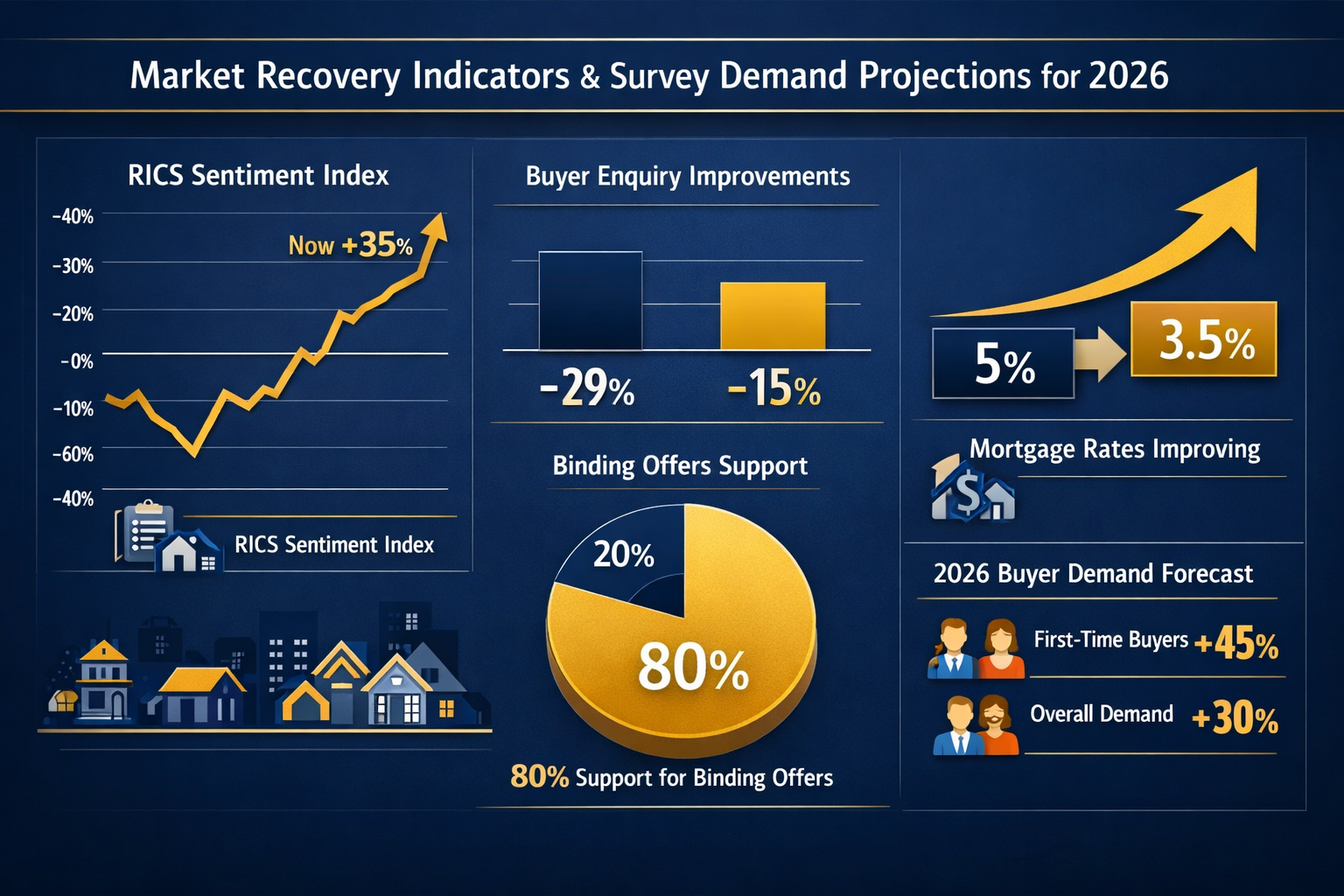

- Strong public support (80% for binding offers, 90% of sellers willing to pay for upfront packs) provides political momentum for reform implementation[2]

- Market recovery indicators strengthen the case for expansion, with RICS sentiment reaching +35% and buyer enquiries improving consistently through early 2026[3]

- Surveyors must invest in capacity planning, technology integration, and standardized workflows to handle increased volume while maintaining RICS-compliant quality standards

Understanding the Proposed Homebuying Reforms and Their Survey Implications

The government's consultation on homebuying reforms centers on a fundamental premise: making property condition assessments a standard upfront requirement rather than an optional mid-transaction consideration[1]. This shift addresses a systemic inefficiency that has plagued the UK property market for years—nearly half of all buyers and sellers have experienced property fall-throughs, with 34% of collapses attributed simply to parties changing their minds[2].

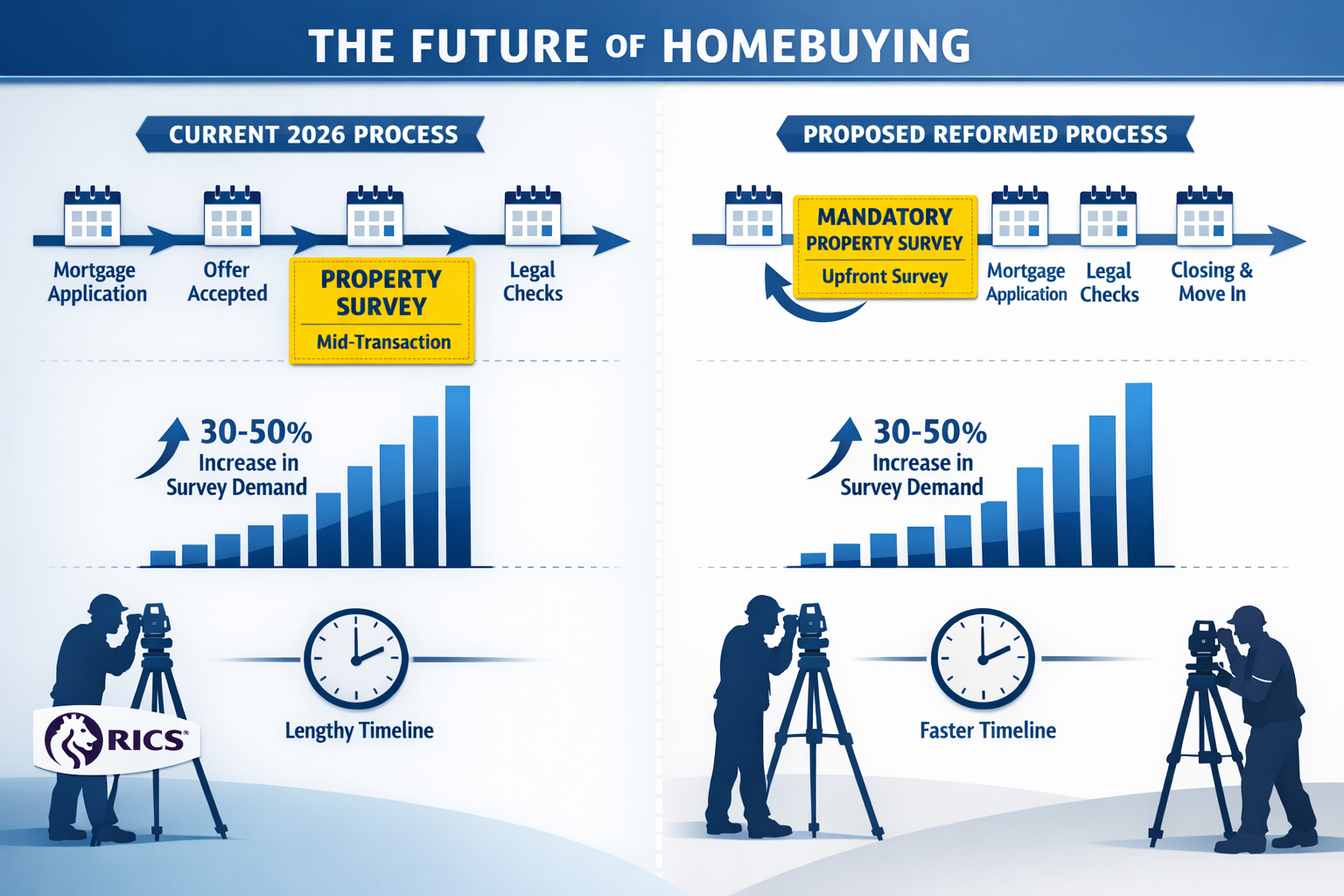

The Current vs. Reformed Timeline

Under the existing system, buyers typically commission surveys after making an offer and beginning the conveyancing process. This creates several problems:

- Delayed discovery of defects often occurs weeks into transactions

- Wasted costs accumulate when surveys reveal deal-breaking issues late in the process

- Seller uncertainty persists throughout extended negotiation periods

- Chain complications multiply when multiple transactions depend on sequential survey outcomes

The proposed reforms would fundamentally alter this sequence by requiring sellers to commission comprehensive property condition assessments before marketing their properties. This upfront approach mirrors successful models in other jurisdictions and aligns with the 90% of sellers who indicate willingness to pay for upfront information packs[2].

For surveyors, this timeline transformation means:

✅ Earlier engagement in the sales process

✅ Seller-commissioned work rather than predominantly buyer-driven requests

✅ Compressed delivery timeframes to avoid delaying property marketing

✅ Standardized reporting requirements to ensure consistency across the market

Regulatory Framework and RICS Standards

The reforms will likely strengthen existing home survey standards and provide clarification reflecting consumer insights and technological changes[3]. RICS has already indicated that some areas of home surveys need strengthening, suggesting that the Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors will include not just volume increases but also enhanced quality expectations.

Chartered surveyors must prepare for:

- Updated survey templates incorporating new mandatory elements

- Enhanced digital reporting standards for easier sharing and integration

- Stricter turnaround time requirements to support upfront commissioning

- Increased professional indemnity considerations given broader reliance on upfront reports

Professional building survey services will need to evolve to meet these enhanced standards while maintaining the thoroughness that distinguishes comprehensive assessments from basic condition reports.

Projected Demand Increases: Quantifying the 2026 Surge

The 30-50% projected increase in survey demand[6] represents an extraordinary growth opportunity for the profession, but understanding the drivers behind this projection is essential for effective capacity planning.

Primary Demand Drivers

1. Mandatory Upfront Requirement Impact

If reforms mandate upfront surveys, the conversion rate from property listings to survey commissions will approach 100% for participating properties. Currently, many transactions proceed without comprehensive surveys, particularly in competitive markets where buyers waive survey contingencies. The mandatory requirement eliminates this gap entirely.

2. Market Recovery Momentum

The January 2026 RICS survey demonstrates strengthening market sentiment with the 12-month outlook reaching +35%—the strongest reading since December 2024[3]. Additionally:

- 43% of respondents anticipate higher house prices over the coming year

- Agreed sales show recovery with a net balance of -9% (the least negative since June 2025)

- New buyer enquiries improved to -15% (up from -21% in December and -29% in November)[3]

This improving market sentiment translates directly to higher transaction volumes, which when combined with mandatory survey requirements, creates a multiplicative effect on demand.

3. Mortgage Rate Improvements

Forecast mortgage rates around 3.5% (down from previous 5% levels) with expected further Bank of England cuts through 2026[4] are improving affordability and enabling more buyers to enter the market. Better affordability directly correlates with higher transaction volumes across all price bands.

4. First-Time Buyer Activity

First-time buyers are fueling market momentum with extended mortgage terms of 30-35 years becoming more common to improve affordability[5]. This demographic expansion brings more entry-level properties into the market, each requiring survey assessments under the reformed system.

Regional Demand Variations

The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors will not distribute evenly across all regions. Analysis indicates that the North and Midlands are experiencing stronger growth momentum than the South[4], meaning surveyors in different regions will experience varying workload increases.

| Region | Projected Demand Increase | Key Drivers |

|---|---|---|

| North & Midlands | 40-55% | Strong buyer activity, affordability advantages, Manchester/Birmingham growth |

| London & South East | 25-40% | Higher baseline volumes, constrained by affordability challenges |

| South West | 30-45% | Lifestyle migration, professional landlord investment |

| Scotland & Wales | 35-50% | Regional recovery patterns, distinct regulatory environments |

Chartered surveyors operating across multiple regions, such as those serving South East London and Central London, must develop flexible capacity allocation strategies to address these regional variations.

Buy-to-Let and Professional Landlord Contribution

Professional landlords continue investing heavily in the buy-to-let sector, with institutional and professional landlords remaining bullish and demonstrating understanding of the value of proper surveys[1]. This segment represents additional sustained demand independent of broader homebuying reforms, as sophisticated investors recognize that comprehensive condition assessments protect their capital investments and inform maintenance planning.

Workflow Transformations: Operational Adaptations for Surveyors

The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors requires comprehensive operational restructuring across multiple dimensions of surveying practice.

Timeline Compression and Turnaround Expectations

Under the reformed system, surveys shift from being requested partway through a transaction to becoming an initial step before marketing[1]. This creates new timeline pressures:

Traditional Timeline:

- Offer accepted → Survey commissioned → 7-14 day turnaround → Report delivered → Negotiations proceed

Reformed Timeline:

- Listing decision → Survey commissioned → 3-7 day turnaround → Report included in marketing materials → Offers proceed with full information

This compression demands:

🔧 Streamlined scheduling systems for rapid deployment

🔧 Expanded surveyor capacity to handle volume spikes without timeline delays

🔧 Technology integration for faster data collection and report generation

🔧 Standardized reporting templates that maintain quality while reducing production time

Professional practices offering structural surveys must balance thoroughness with efficiency, ensuring that accelerated timelines don't compromise the comprehensive assessments that protect both buyers and sellers.

Technology Integration Requirements

Meeting the dual challenges of increased volume and compressed timelines necessitates significant technology investment:

Digital Data Collection

- Tablet-based inspection protocols with real-time data entry

- Drone roof survey technology for faster, safer roof assessments

- Thermal imaging for efficient identification of insulation and moisture issues

- Digital measurement tools reducing manual calculation time

Automated Reporting Systems

- Template-based report generation with customizable sections

- Photograph integration and annotation tools

- Automated compliance checking against RICS standards

- Digital delivery platforms for immediate client access

Practice Management Software

- Capacity planning dashboards showing surveyor availability

- Automated scheduling optimizing geographic routing

- Client communication systems providing status updates

- Quality assurance workflows ensuring consistent standards

Surveyors serving diverse areas from Hertfordshire to Surrey must implement systems that coordinate multi-region operations efficiently.

Capacity Planning and Staffing Strategies

A 30-50% demand increase[6] requires proportional capacity expansion through multiple strategies:

1. Direct Hiring

- Recruit additional RICS-qualified surveyors

- Develop apprenticeship programs for pipeline development

- Offer competitive compensation reflecting increased demand

2. Associate Networks

- Build relationships with independent surveyors for overflow capacity

- Establish quality standards and training for associate surveyors

- Create geographic coverage networks for regional demand variations

3. Productivity Enhancement

- Implement technology reducing time per survey by 15-25%

- Standardize workflows eliminating redundant processes

- Optimize scheduling to maximize surveys per surveyor per day

4. Service Tier Differentiation

- Develop tiered survey products (basic, standard, comprehensive)

- Price differentiation based on property value and complexity

- Fast-track options for time-sensitive requirements

Quality Assurance in High-Volume Environments

Maintaining RICS-compliant quality standards while scaling operations represents a critical challenge. Effective quality assurance systems include:

- Peer review protocols for new or complex properties

- Standardized checklists ensuring consistent coverage across all surveys

- Continuing professional development keeping surveyors current on standards and technology

- Client feedback systems identifying areas for improvement

- Professional indemnity insurance reviews ensuring adequate coverage for expanded operations

Preparation Strategies: Positioning Your Practice for Reform Implementation

The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors creates both opportunities and risks. Proactive preparation determines which practices thrive and which struggle under the new regime.

Immediate Action Steps (Q1-Q2 2026)

Assess Current Capacity

- Calculate maximum surveys per month under current staffing

- Identify bottlenecks in current workflows

- Evaluate technology infrastructure readiness

- Review professional indemnity coverage limits

Develop Technology Roadmap

- Research and trial digital inspection tools

- Implement or upgrade practice management systems

- Establish digital reporting platforms

- Train staff on new technology systems

Strengthen RICS Compliance

- Review current survey templates against latest RICS standards

- Participate in RICS consultation processes on reform implementation

- Attend professional development courses on regulatory changes

- Document quality assurance procedures

Build Strategic Partnerships

- Establish relationships with estate agents for early referral arrangements

- Connect with conveyancing firms to understand integrated workflow requirements

- Network with other surveyors for capacity-sharing arrangements

- Engage with technology providers for early adopter advantages

Medium-Term Positioning (Q3-Q4 2026)

Capacity Expansion

- Initiate recruitment for additional qualified surveyors

- Launch apprenticeship or training programs

- Formalize associate surveyor networks

- Expand geographic coverage to capture regional demand variations

Practices serving areas like Buckinghamshire and Oxfordshire should consider cross-regional capacity sharing to balance demand fluctuations.

Marketing and Positioning

- Develop seller-focused marketing materials explaining upfront survey benefits

- Create educational content on reformed homebuying process

- Establish thought leadership through industry commentary

- Build digital presence for online discovery by sellers and agents

Service Product Development

- Design tiered survey products aligned with different property types and values

- Create package offerings combining surveys with related services

- Develop fast-track options for time-sensitive requirements

- Establish pricing structures reflecting new market dynamics

Long-Term Strategic Planning (2027 and Beyond)

Business Model Evolution

- Consider specialization in specific property types or regions

- Evaluate commercial property survey opportunities as residential model proves successful

- Explore value-added services (maintenance planning, reinstatement valuations, etc.)

- Assess merger or acquisition opportunities for rapid scaling

Technology Leadership

- Invest in proprietary technology providing competitive advantages

- Explore AI-assisted defect identification and report generation

- Develop data analytics capabilities for market intelligence

- Create client portals for enhanced service delivery

Professional Development

- Achieve advanced RICS accreditations and specializations

- Contribute to industry standard development

- Mentor next-generation surveyors

- Participate in regulatory consultation processes

Market Dynamics Supporting Reform Implementation

Beyond the regulatory drivers, several market dynamics create favorable conditions for reform implementation and sustained survey demand growth in 2026.

Improving Affordability Metrics

Mortgage rate improvements to approximately 3.5%[4] represent a significant affordability enhancement compared to the 5%+ rates that constrained the market in previous years. Combined with expected further Bank of England cuts through 2026, financing costs are becoming more manageable for a broader range of buyers.

This affordability improvement translates to:

- Higher transaction volumes across all price bands

- Increased first-time buyer participation with extended mortgage terms

- Greater investor confidence in buy-to-let opportunities

- Reduced transaction fall-through rates as buyers have more financial certainty

Consumer Sentiment and Reform Support

The strong public support for proposed reforms—80% supporting binding offers and 90% of sellers willing to pay for upfront information packs[2]—provides crucial political momentum for implementation. This level of support indicates that:

- Sellers recognize the value proposition of upfront information reducing fall-throughs

- Buyers appreciate the transparency and reduced risk of informed decision-making

- Industry stakeholders understand the efficiency gains from streamlined processes

- Political leaders have public mandate for reform implementation

Regional Market Variations

While national trends show improvement, regional disparities create uneven survey demand patterns[4]. The North and Midlands are experiencing stronger growth momentum than the South, with northern cities like Manchester and Birmingham seeing particularly strong buyer activity.

Surveyors must develop regional intelligence to:

- Allocate capacity where demand is strongest

- Adjust pricing strategies reflecting local market conditions

- Build partnerships with regional estate agents and conveyancers

- Understand local property characteristics affecting survey requirements

Practices operating across multiple regions, from West London to Hampshire, benefit from diversified geographic exposure that balances regional variations.

Stamp Duty Considerations

While reforms promise significant improvements, stamp duty remains a limiting factor on transaction volumes[2]. Survey demand growth may not reach its full potential until broader stamp duty reform occurs, potentially capping the immediate impact to the 30-50% projection range rather than higher levels.

This constraint means:

- Demand increases will be substantial but not unlimited

- Higher-value properties face greater transaction friction

- First-time buyer relief provisions remain critical for entry-level activity

- Future stamp duty reforms could trigger additional demand surges beyond 2026 projections

Challenges and Risk Mitigation

The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors presents challenges alongside opportunities. Effective risk mitigation strategies are essential.

Quality vs. Quantity Balance

Challenge: Pressure to increase volume while maintaining RICS-compliant quality standards

Mitigation Strategies:

- Implement robust quality assurance protocols with peer review

- Use technology to enhance efficiency without compromising thoroughness

- Establish clear service tiers with appropriate pricing for complexity levels

- Maintain adequate professional indemnity insurance coverage

- Document all decisions and recommendations comprehensively

Capacity Constraints

Challenge: Insufficient qualified surveyors to meet 30-50% demand increase[6]

Mitigation Strategies:

- Begin recruitment and training programs immediately

- Build associate networks for flexible capacity

- Implement technology reducing time per survey

- Develop partnerships with other practices for overflow referrals

- Consider geographic specialization to optimize resource allocation

Technology Investment Requirements

Challenge: Significant capital requirements for digital transformation

Mitigation Strategies:

- Prioritize highest-impact technology investments first

- Explore leasing or subscription models reducing upfront costs

- Seek industry partnerships for technology access

- Apply for professional development grants or funding

- Calculate ROI based on increased capacity and efficiency gains

Regulatory Uncertainty

Challenge: Final reform details and implementation timeline remain uncertain

Mitigation Strategies:

- Participate in RICS and government consultation processes

- Develop flexible implementation plans adaptable to various scenarios

- Monitor regulatory developments through professional associations

- Build relationships with policymakers and industry leaders

- Prepare multiple capacity scenarios (conservative, moderate, aggressive)

Competitive Pressures

Challenge: Increased demand attracting new market entrants and pricing competition

Mitigation Strategies:

- Differentiate through service quality and specialization

- Build strong relationships with estate agents and conveyancers

- Invest in brand development and thought leadership

- Focus on value proposition beyond price competition

- Develop unique service offerings difficult for competitors to replicate

Conclusion

The Impact of Proposed Homebuying Reforms on Building Survey Demand: 2026 Workflow Transformations for Surveyors represents a watershed moment for the profession. With projected demand increases of 30-50%[6], mandatory upfront survey requirements fundamentally restructuring transaction timelines[1], and strong public support providing political momentum for implementation[2], chartered surveyors face unprecedented growth opportunities alongside significant operational challenges.

Success in this transformed landscape requires proactive preparation across multiple dimensions:

✅ Technology investment enabling efficient high-volume operations while maintaining quality

✅ Capacity expansion through hiring, training, and associate networks

✅ Workflow optimization compressing turnaround times without compromising thoroughness

✅ Quality assurance systems ensuring RICS compliance at scale

✅ Strategic positioning differentiating practices in an increasingly competitive market

The favorable market conditions supporting these reforms—improving mortgage affordability, strengthening buyer sentiment with RICS outlook at +35%[3], and recovering transaction volumes—create an ideal environment for implementation. Regional variations from South West London to Guildford require flexible capacity allocation strategies, while professional landlord investment provides sustained demand independent of broader reforms[1].

Actionable Next Steps

For Individual Surveyors:

- Assess current capacity and identify workflow bottlenecks

- Invest in professional development on latest RICS standards and technology

- Build relationships with estate agents and conveyancers in your region

- Research and trial digital inspection and reporting tools

- Review professional indemnity insurance coverage for expanded operations

For Surveying Practices:

- Develop comprehensive capacity expansion plans for 30-50% demand growth

- Implement technology roadmap prioritizing highest-impact investments

- Establish quality assurance protocols for high-volume environments

- Create tiered service offerings aligned with different market segments

- Build strategic partnerships for geographic coverage and capacity sharing

For Industry Stakeholders:

- Participate actively in RICS and government consultation processes

- Contribute to development of updated survey standards and templates

- Share best practices for technology integration and workflow optimization

- Support professional development programs building next-generation capacity

- Advocate for implementation timelines allowing adequate preparation

The transformation ahead is substantial, but the profession has the expertise, standards, and commitment to quality necessary for successful adaptation. By preparing now, investing strategically, and maintaining focus on RICS-compliant service delivery, chartered surveyors can position themselves not merely to survive these reforms but to thrive in the expanded, more efficient property market they will create.

The question is not whether these reforms will transform surveyor workflows—the evidence strongly suggests they will. The question is whether individual surveyors and practices will prepare proactively to capitalize on the opportunities or react defensively to the challenges. Those who choose the former path will find 2026 and beyond to be among the most rewarding periods in the profession's history.

References

[1] Surveying In 2026 Reform Recovery And Renewed Demand – https://www.lrg.co.uk/news-and-insights/surveying-in-2026-reform-recovery-and-renewed-demand/

[2] What The Agents Say 2026 Housing Market Predictions – https://mortgagesoup.co.uk/what-the-agents-say-2026-housing-market-predictions/

[3] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[4] Forecasting The Future What To Expect From House Prices In 2026 – https://surveyingcorp.com/2026/01/forecasting-the-future-what-to-expect-from-house-prices-in-2026/

[5] Seven Trends That Will Shape The Regional Housing Market In 2026 – https://www.struttandparker.com/blog/seven-trends-that-will-shape-the-regional-housing-market-in-2026

[6] Homebuying Process Reforms 2026 How Mandatory Upfront Surveys Will Transform Building Surveyor Workloads – https://nottinghillsurveyors.com/blog/homebuying-process-reforms-2026-how-mandatory-upfront-surveys-will-transform-building-surveyor-workloads