The UK housing market stands at a pivotal crossroads in 2026. After years of volatility, uncertainty, and affordability pressures, surveyors across the nation are witnessing the early signs of market stabilisation—but not uniformly. While Scotland and Northern Ireland surge ahead with robust price growth, London languishes in stagnation. Mortgage rates hover near 5%, yet forecasters predict modest 2–4% national growth. For chartered surveyors tasked with delivering accurate, defensible valuations, navigating 2026 house price forecasts: valuation impacts for UK surveyors in a recovering market requires a sophisticated understanding of regional disparities, evolving buyer sentiment, and macroeconomic shifts.

This comprehensive guide synthesises the latest RICS data, regional market intelligence, and forecaster consensus to equip surveyors with actionable strategies for valuing properties in a market characterised by recovery—but one where the recovery looks dramatically different depending on postcode.

Key Takeaways

- 📈 National house prices are stabilising with the RICS net balance improving to -10% (up from -19% in October 2025), signalling a clear turning point after prolonged decline.[3]

- 🏴 Regional divergence is extreme: Scotland and Northern Ireland lead with strong growth momentum, while London remains the only major region experiencing price falls or stagnation.[1][3]

- 💷 Modest growth forecasted nationally: Market consensus projects 2–4% house price growth across the UK in 2026, with mortgage rates expected to fall from current levels of approximately 4.83–4.95%.[1][2]

- 🔍 Surveyor confidence is rebounding: 43% of RICS respondents anticipate higher prices over the next 12 months—the most positive outlook since February 2025.[3]

- 🎯 Valuation strategies must adapt: Surveyors need region-specific approaches, enhanced comparable analysis, and careful consideration of affordability metrics to deliver accurate valuations in this bifurcated market.

Understanding the 2026 Market Recovery: National Trends and Forecaster Consensus

The Stabilisation Signal: RICS Data Points to Turning Point

The RICS UK Residential Market Survey for January 2026 provides the most authoritative professional sentiment indicator available to surveyors. The headline figure—a net balance of -10% for house prices over the past three months—represents a substantial improvement from the -19% recorded in October 2025.[3] While still technically negative, this trajectory indicates that the proportion of surveyors reporting price falls is diminishing rapidly.

More significantly, 43% of RICS survey respondents anticipate higher house prices over the next 12 months, representing the most positive forward-looking outlook since February 2025.[3] This professional confidence, grounded in direct market observation, suggests that surveyors on the ground are witnessing tangible signs of recovery in transaction activity, buyer interest, and pricing power.

Forecaster Consensus: Modest but Meaningful Growth

Major forecasters have converged on a 2–4% house price growth projection for 2026 across the UK, providing surveyors with a national baseline for valuation adjustments:[1][2]

| Forecaster | 2026 Growth Projection |

|---|---|

| Hamptons | 2.5% (by Q4 2026) |

| Halifax | 1–3% |

| Nationwide | 2–4% |

| Savills | 2% |

| Zoopla | 1.5% |

This consensus is particularly valuable for surveyors preparing valuation reports that must withstand scrutiny from lenders, solicitors, and clients. The consistency across independent forecasters provides defensible support for moderate upward valuation adjustments, particularly when combined with local market evidence.

Current Valuation Benchmarks: February 2026 Price Indices

Understanding current price levels is essential for accurate valuation work. As of February 2026, the major indices show:[2]

- HM Land Registry (December 2025 data): £270,259 average UK house price

- Rightmove asking prices (February 2026): £368,019

- Halifax valuations: Breached £300,000 for the first time

The divergence between these figures reflects different methodologies—Land Registry tracks completed transactions, Rightmove captures asking prices, and Halifax measures mortgage valuations. For surveyors, this emphasises the importance of using multiple data sources and local comparable evidence rather than relying on a single national average.

Rightmove's recording of the greatest January rise in 25 years—a 2.8% increase from £358,138 to £368,031—signals strong early-year momentum driven by post-Christmas buyer activity.[2] This seasonal surge provides surveyors with evidence of renewed market confidence, particularly relevant for valuations conducted in Q1 2026.

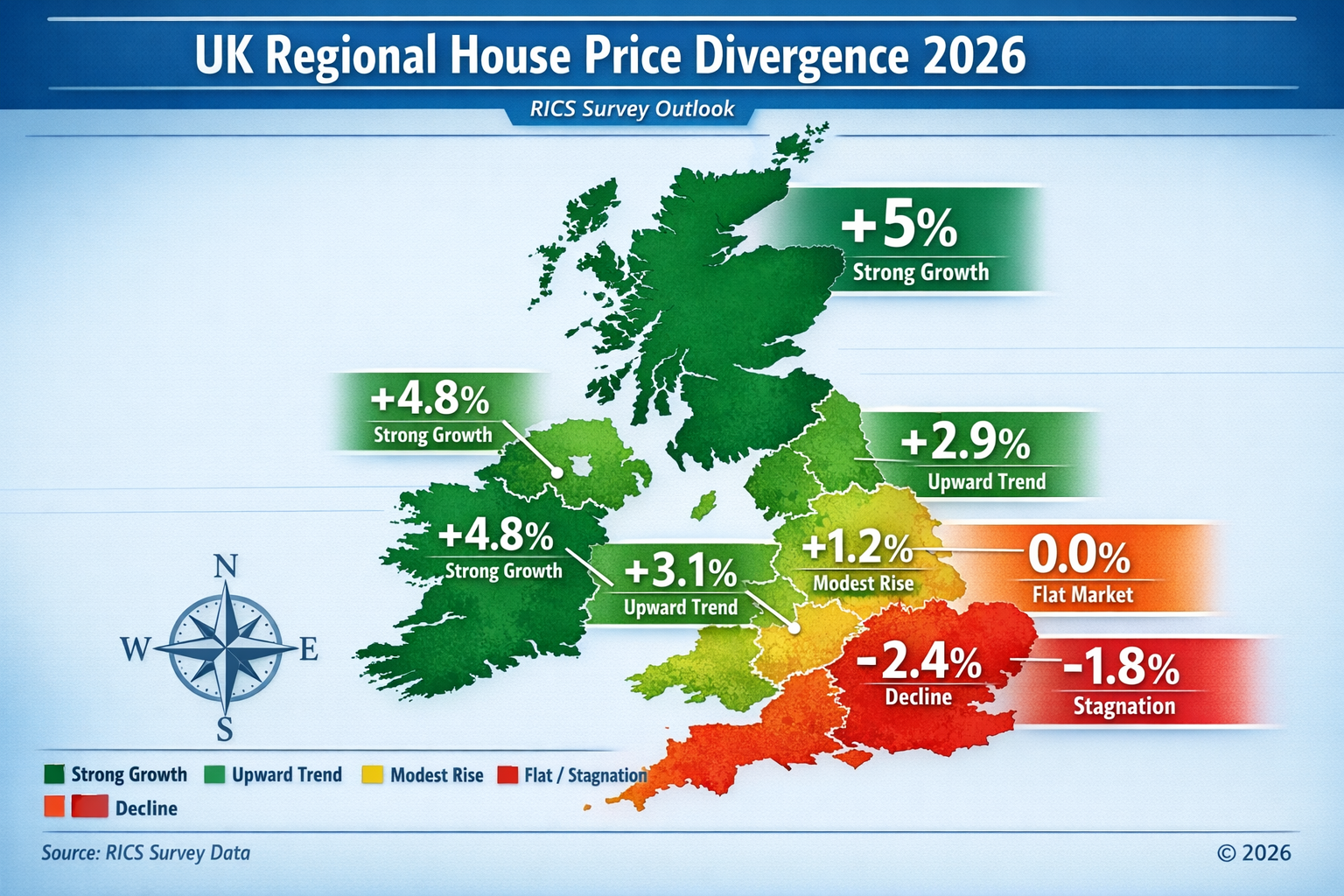

Regional Divergence: Navigating 2026 House Price Forecasts Across the North-South Divide

The Geographic Split: Winners and Laggards

Navigating 2026 house price forecasts: valuation impacts for UK surveyors in a recovering market requires acute awareness of regional performance disparities. The RICS January 2026 survey reveals a stark geographic divide:[3]

Strong Growth Regions:

- 🏴 Scotland: Leading national growth with sustained positive momentum

- 🇮🇪 Northern Ireland: Strong upward price trends

- 🏭 North West England: Displaying consistent upward movement

- 🏴 North of England: Positive price trajectory

- 🏴 Wales: Affordable regions seeing accelerated activity

Stagnant or Declining Regions:

- 🏙️ London: The only major region experiencing price falls (-2.4% in 2025)[6]

- 🌳 South East: Continued affordability pressures limiting growth

- 🌊 South West: Lagging behind national average

- 📍 East Anglia: Persistent challenges

The North East England specifically recorded 5% price growth in 2025, creating a dramatic 7.4 percentage point differential with London's -2.4% decline.[6] For surveyors operating across multiple regions, this necessitates fundamentally different valuation approaches depending on location.

Affordability: The Driving Force Behind Regional Performance

The regional divergence is not random—it's driven by affordability fundamentals. Northern regions and Wales offer substantially lower price-to-income ratios, enabling first-time buyers and families to participate actively in the market. In contrast, London and the South East face persistent affordability constraints that suppress demand despite falling mortgage rates.

For surveyors conducting valuations in London versus those working with chartered surveyors in Surrey or chartered surveyors in Hampshire, the comparable selection process must reflect these fundamentally different market dynamics.

London: The Exceptional Outlier

London is the only major UK region where prices have fallen or stagnated, with properties taking longer to sell than elsewhere.[1] This creates distinct challenges for surveyors valuing London properties:

- Extended marketing periods must be factored into liquidity assessments

- Downward price adjustments may be appropriate even while national trends are positive

- Micro-market analysis becomes critical—prime central London performs differently than outer boroughs

- Comparable evidence must be recent and location-specific given rapid localised shifts

Surveyors working with chartered surveyors in Central London, chartered surveyors in North London, or chartered surveyors in West London must exercise particular caution in applying national growth forecasts to their local valuations.

Valuation Methodology Adjustments: Surveyor Strategies for a Bifurcated Market

Enhanced Comparable Analysis in Regional Markets

Navigating 2026 house price forecasts: valuation impacts for UK surveyors in a recovering market demands refinement of traditional comparable analysis. The standard approach of selecting three to five comparable sales within the past six months remains foundational, but additional layers of analysis are now essential:

1. Time-Adjusted Comparables

Given the rapid market shifts between late 2025 and early 2026, surveyors should apply time adjustments to older comparables. The RICS data showing improvement from -19% to -10% net balance over three months suggests approximately 3% quarterly adjustment may be appropriate in recovering markets.[3]

2. Regional Performance Weighting

When valuing properties in strong-growth regions (Scotland, Northern Ireland, North West), surveyors should:

- Weight recent comparables more heavily

- Consider pending sales as additional market evidence

- Apply upward adjustments where clear momentum exists

- Document regional forecaster projections in valuation reports

For properties in stagnant regions (London, South East), the approach differs:

- Emphasise achieved prices over asking prices

- Extend comparable search period to capture sufficient evidence

- Apply conservative adjustments or no adjustment where uncertainty exists

- Highlight extended marketing periods in market commentary

3. Micro-Market Segmentation

National and even regional averages mask significant micro-market variation. Surveyors should segment by:

- Property type: Detached homes vs. flats show different trajectories

- Price bracket: First-time buyer properties vs. premium homes

- Location quality: Prime vs. secondary locations within the same town

- Condition: Turnkey vs. renovation properties

Understanding valuation factors specific to each segment enables more nuanced and defensible valuations.

Incorporating Mortgage Rate Expectations

Current mortgage rates—4.83% for two-year fixed and 4.95% for five-year fixed products—remain elevated but are expected to fall as inflation moderates and the Bank of England implements anticipated rate cuts.[2] This creates a valuation challenge: should surveyors reflect current financing costs or anticipated future conditions?

Best Practice Approach:

- Primary valuation should reflect current market conditions and financing costs

- Market commentary should acknowledge expected rate trajectory and potential impact

- Sensitivity analysis can be provided for clients requiring forward-looking scenarios

- Affordability calculations should use current rates but note improvement trajectory

For specialist valuations such as RICS valuation cost assessments or Red Book valuation work, adherence to current market conditions remains paramount, with forward-looking commentary clearly separated from the formal valuation conclusion.

Transaction Volume and Liquidity Considerations

The RICS survey reveals 35% net balance of respondents expect sales activity to strengthen over the next 12 months—the strongest reading since December 2024—though short-term expectations (next three months) remain more cautious at +4% net balance.[3]

This improving but still-modest transaction outlook affects valuation in several ways:

Market Liquidity Assessment:

- Properties in high-demand segments (affordable northern regions) enjoy strong liquidity

- Premium and London properties face extended marketing periods

- Liquidity risk should be explicitly addressed in valuation reports

Inventory Levels:

Zoopla reported 6% more homes on sale in January 2026 compared to January 2025, suggesting improved market supply.[2] Increased inventory moderates price growth expectations and provides surveyors with richer comparable evidence.

For surveyors preparing probate valuations or capital gains tax valuations, understanding current inventory levels and typical marketing periods is essential for defensible open market value conclusions.

Practical Surveyor Tactics: Adapting Professional Practice for 2026

Client Communication and Expectation Management

The bifurcated nature of the 2026 recovery creates communication challenges. Clients reading national headlines about "market recovery" and "2–4% growth" may have unrealistic expectations for their specific property, particularly in London or the South East.

Effective Communication Strategies:

✅ Contextualise national forecasts with local market evidence

✅ Provide regional comparison data to illustrate geographic variation

✅ Explain methodology transparently, including comparable selection criteria

✅ Distinguish between asking prices and achieved prices in market commentary

✅ Offer realistic marketing period estimates based on current local conditions

For clients in recovering regions, manage expectations around the pace of growth—2–4% annual growth is modest and may not offset recent declines. For clients in stagnant regions, provide evidence-based reassurance that stabilisation represents progress after prolonged falls.

Leveraging Professional Resources and Data

Surveyors navigating this complex market should maximise use of available professional resources:

RICS Resources:

- Monthly UK Residential Market Survey for sentiment tracking

- Regional market reports for local intelligence

- Red Book guidance for methodology compliance

- Professional standards updates for emerging issues

Data Platforms:

- Land Registry price paid data for verified transactions

- Rightmove and Zoopla for current market listings and trends

- Local estate agent intelligence for micro-market insights

- Mortgage lender panels for financing condition updates

Professional Networks:

Engagement with fellow surveyors through RICS local chapters, professional forums, and regional networks provides invaluable ground-level intelligence that supplements formal data sources. Surveyors working with chartered surveyors in Kingston, chartered surveyors in Richmond, or chartered surveyors in Guildford benefit from sharing local market observations.

Specialist Valuation Considerations

Different valuation purposes require adapted approaches in the 2026 market:

Mortgage Valuations:

- Lenders remain cautious despite market improvement

- Conservative comparable selection appropriate

- Highlight any regional weakness or extended marketing periods

- Ensure valuation supports lending criteria given elevated rates

Purchase Valuations:

- Buyers benefit from independent verification of asking prices

- Compare asking price to recent achieved prices in locality

- Assess whether property is priced for current market or reflects seller's outdated expectations

- Consider what survey you need alongside valuation advice

Lease Extension and Enfranchisement:

- Lease extension valuations require particular care in stagnant markets

- Growth assumptions for future value must reflect regional reality

- London properties may warrant conservative growth projections

- Northern properties may support more optimistic trajectories

Tax-Related Valuations:

- ATED valuations and shared ownership valuations require specific compliance

- Market conditions at valuation date must be accurately reflected

- Regional performance differential should be documented

- Professional skepticism regarding national averages is appropriate

Technology and Valuation Tools

Modern surveying practice increasingly incorporates technology to enhance accuracy and efficiency:

Automated Valuation Models (AVMs):

- Useful for initial screening and sense-checking

- Should not replace professional judgment in current volatile market

- Particularly unreliable in regions with rapid change or limited transactions

- Best used as supporting evidence rather than primary methodology

Geographic Information Systems (GIS):

- Mapping comparable locations for visual analysis

- Identifying micro-market boundaries

- Assessing local amenity changes affecting value

Data Analytics:

- Tracking regional price trends over time

- Identifying seasonal patterns in local markets

- Comparing current performance to historical norms

While technology enhances capability, the professional judgment of experienced surveyors remains irreplaceable—particularly when navigating 2026 house price forecasts: valuation impacts for UK surveyors in a recovering market where regional divergence and rapid shifts demand nuanced interpretation.

First-Time Buyers and Affordability: The Demand Driver for 2026

The First-Time Buyer Recovery

First-time buyer market recovery represents a critical demand driver for 2026. Improved affordability combined with falling mortgage rates could enable first-time buyers to participate more actively, particularly in competitive regional markets where wage growth may outpace property price growth for the first time in several years.[1]

For surveyors, this demographic shift has valuation implications:

Entry-Level Property Segments:

- Likely to see strongest demand and price support

- Flats and smaller homes in affordable regions benefit most

- Starter homes in northern regions particularly well-positioned

- London entry-level properties face continued affordability challenges

Comparable Selection:

When valuing entry-level properties, surveyors should:

- Prioritise recent first-time buyer transactions

- Consider Help to Buy scheme sales with appropriate adjustments

- Assess local wage growth and affordability ratios

- Evaluate proximity to employment centres and transport links

For clients seeking Help to Buy valuations, understanding the improving but still-challenging first-time buyer landscape is essential for accurate market value conclusions.

Affordability Metrics and Regional Analysis

Affordability improvements in northern regions and Wales create the foundation for sustained growth in these markets.[1] Surveyors should incorporate affordability analysis into valuation reports:

Key Affordability Metrics:

- Price-to-income ratio: Local house prices relative to median household income

- Mortgage affordability: Monthly payment as percentage of income at current rates

- Deposit requirements: Typical deposit needed for local first-time buyers

- Rental equivalence: Purchase cost vs. rental cost comparison

Regions where affordability metrics are improving provide stronger support for positive valuation adjustments and growth projections. Regions where affordability remains stretched (London, South East) warrant more conservative approaches.

Risk Factors and Uncertainties: What Could Derail the Recovery?

Macroeconomic Headwinds

While the consensus forecast points to modest recovery, several risk factors could derail progress:

Interest Rate Trajectory:

If inflation proves more persistent than expected, the Bank of England may delay anticipated rate cuts, keeping mortgage rates elevated and suppressing demand. Surveyors should monitor Bank of England communications and inflation data for early warning signs.

Economic Growth:

UK economic growth remains modest. A recession or significant slowdown could undermine buyer confidence and employment security, reducing transaction volumes and price support.

Global Economic Shocks:

International events—geopolitical tensions, financial market disruptions, or trade policy changes—could create uncertainty that freezes the UK housing market as buyers and sellers adopt wait-and-see approaches.

Political and Regulatory Factors

Government Housing Policy:

Changes to stamp duty, Help to Buy schemes, planning regulations, or rental market rules could significantly impact demand and pricing. Surveyors should stay informed of policy developments and assess potential impacts on local markets.

Lending Standards:

If mortgage lenders tighten lending criteria in response to economic uncertainty, transaction volumes could decline even if prices stabilise, affecting market liquidity and valuation evidence availability.

Market-Specific Risks

London Stagnation Persistence:

If London's underperformance continues longer than expected, it could create negative sentiment spillover to surrounding regions and undermine national confidence.

Regional Divergence Acceleration:

Further widening of the north-south divide could create political pressure for intervention, potentially introducing policy changes that affect valuation fundamentals.

Supply-Demand Imbalance:

The 6% increase in inventory provides more choice for buyers but could moderate price growth more than forecasters expect.[2] Surveyors should monitor local supply levels and adjust growth expectations accordingly.

Conclusion: Professional Excellence in a Recovering but Divided Market

Navigating 2026 house price forecasts: valuation impacts for UK surveyors in a recovering market demands professional excellence, regional expertise, and methodological rigour. The market presents a paradox: national stabilisation and modest growth projections coexist with extreme regional divergence, creating fundamentally different valuation environments depending on location.

Key Professional Imperatives for 2026

1. Embrace Regional Differentiation

Abandon one-size-fits-all approaches. Valuations in Scotland require different assumptions than valuations in London. Northern properties warrant different growth projections than southern properties. Micro-market analysis trumps national averages.

2. Enhance Comparable Analysis

The rapidly shifting market demands more sophisticated comparable selection, time adjustments, and weighting methodologies. Recent evidence matters more than historical norms. Local transactions trump regional averages.

3. Communicate Transparently

Clients need clear, evidence-based explanations of how national forecasts apply—or don't apply—to their specific property. Transparent methodology, comprehensive market commentary, and realistic expectations build trust and professional credibility.

4. Monitor Continuously

The market is evolving month-by-month. Regular engagement with RICS surveys, regional data, mortgage rate trends, and local market intelligence enables surveyors to adjust approaches as conditions change.

5. Maintain Professional Standards

Adherence to Red Book standards, RICS guidance, and professional ethics remains paramount. In uncertain markets, professional rigour provides the foundation for defensible valuations that withstand scrutiny.

Actionable Next Steps

For surveyors seeking to excel in the 2026 market:

✅ Review your regional market data sources and identify gaps in coverage

✅ Establish systematic monitoring of RICS monthly surveys and regional forecaster reports

✅ Audit your comparable databases to ensure sufficient recent evidence across all property types

✅ Develop region-specific valuation templates that incorporate appropriate local adjustments

✅ Enhance client communication materials with regional context and market commentary

✅ Engage with professional networks to share intelligence and validate local observations

✅ Invest in continuing professional development focused on valuation in volatile markets

✅ Consider specialist training in regional market analysis and advanced comparable methodologies

The 2026 market recovery offers significant opportunities for surveyors who adapt their practice to reflect regional realities, maintain methodological rigour, and communicate effectively with clients. Those who continue to rely on outdated national averages or fail to differentiate between strong-growth and stagnant regions risk delivering valuations that fail to reflect true market conditions.

For professional surveying services that understand the complexities of navigating 2026 house price forecasts and their valuation impacts, chartered surveyors in London and throughout the UK stand ready to provide expert guidance grounded in local market knowledge and professional excellence.

The recovery is here—but it's a recovery of many faces, requiring surveyors to bring their best professional judgment, regional expertise, and methodological sophistication to every valuation they undertake.

References

[1] Uk House Prices In 2026 Where The Market Is Headed What It Means For Buyers Sellers And Landlor – https://www.approvedbusinessfinance.co.uk/post/uk-house-prices-in-2026-where-the-market-is-headed-what-it-means-for-buyers-sellers-and-landlor

[2] House Prices – https://moneyweek.com/investments/house-prices/house-prices

[3] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[4] How Much Does A House Survey Cost – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/how-much-does-a-house-survey-cost/

[5] Watch – https://www.youtube.com/watch?v=jLxh-kuQaDg

[6] Valuing Northern England Properties In 2026 Surveyor Tactics For Outpacing Southern Affordability Pressures – https://nottinghillsurveyors.com/blog/valuing-northern-england-properties-in-2026-surveyor-tactics-for-outpacing-southern-affordability-pressures