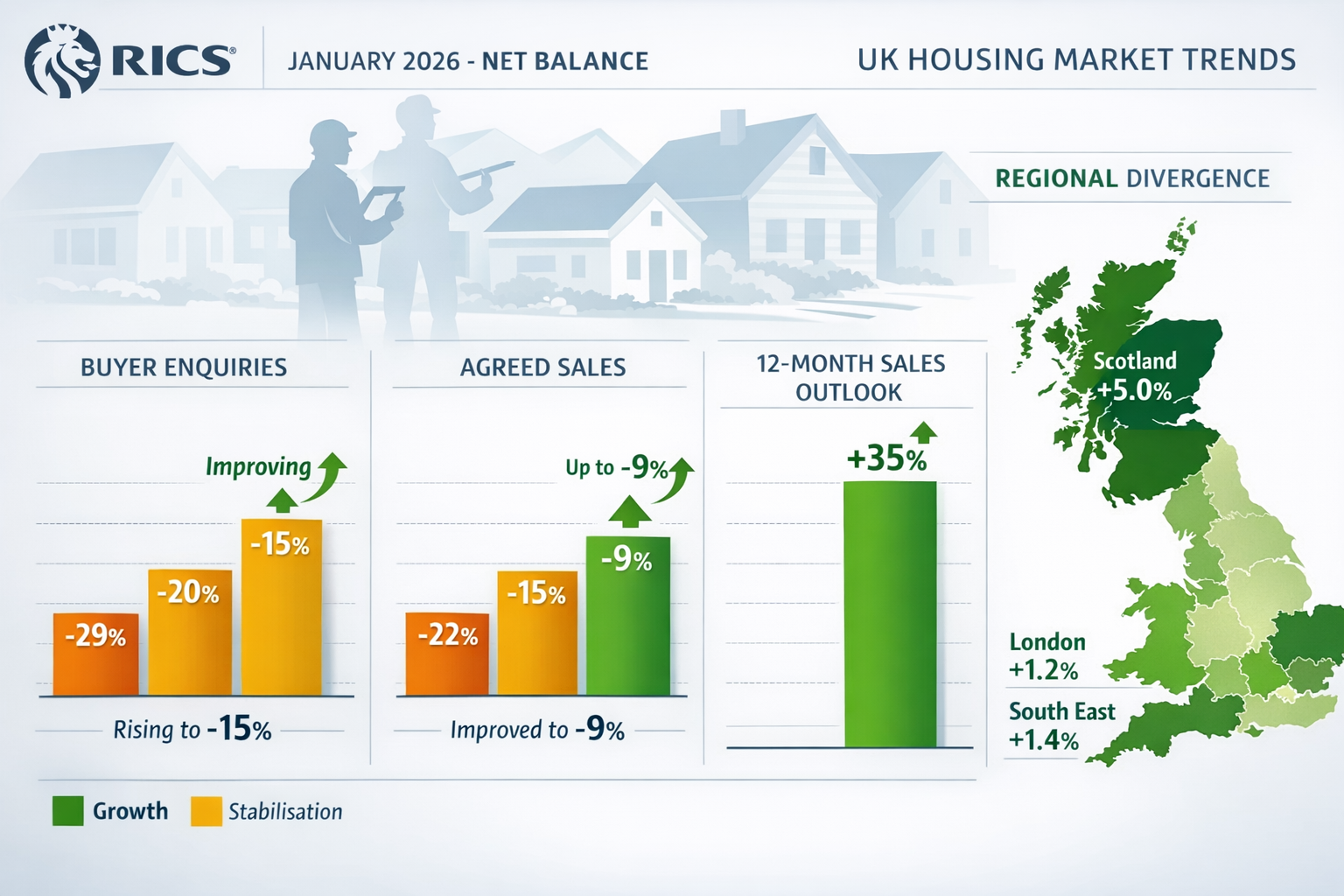

The UK housing market is showing its first genuine signs of recovery in over a year, and surveyors who adapt quickly will capture the opportunity. Preparing Building Surveys for UK Housing Market Recovery 2026: Lessons from RICS January Data reveals a dramatic shift in market sentiment, with the Royal Institution of Chartered Surveyors (RICS) reporting a 12-month sales outlook that surged to +35% net balance—the strongest reading since December 2024.[1] This transformation demands that building surveyors recalibrate their approach to risk assessment, regional analysis, and volume management as transaction momentum accelerates across the UK.

Key Takeaways

- 📈 New buyer enquiries improved to -15% net balance in January 2026, up from -21% in December, signaling sustained demand recovery across most UK regions.[1]

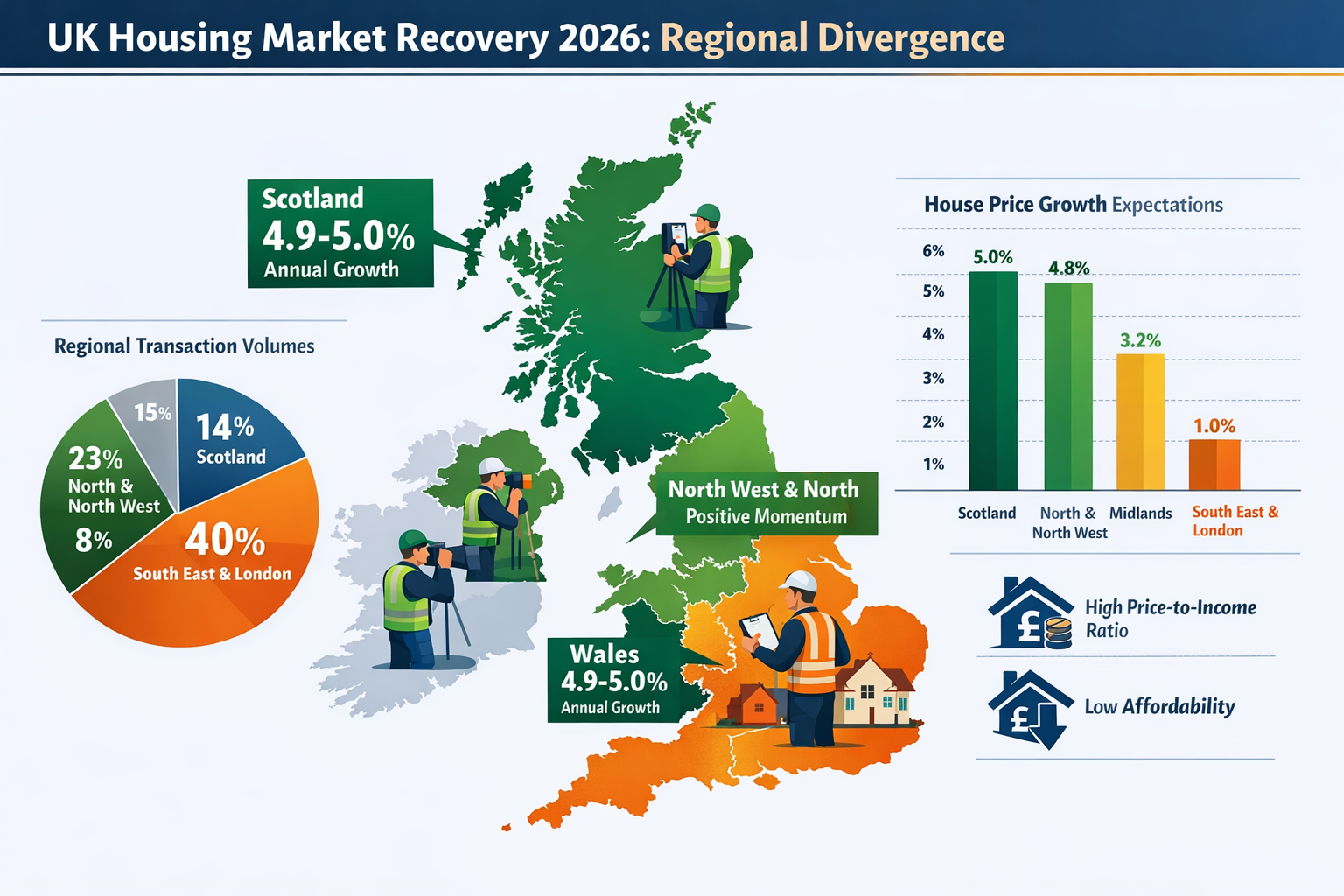

- 🏘️ Regional divergence is widening, with Scotland and Wales leading at 4.9-5.0% annual growth while London and the South East continue to underperform due to affordability challenges.[1][4]

- 💼 Surveyor confidence reached a 14-month high, with 12-month sales expectations at +35% and price expectations showing +43% of respondents anticipating higher values.[1]

- 🔍 Building survey volume is set to increase as agreed sales reached -9% net balance—the least negative reading since June 2025—requiring enhanced capacity planning.[1]

- ⚠️ Risk spotting becomes critical in early recovery phases when buyers rush to secure properties before anticipated price increases, potentially overlooking structural defects.

Understanding the RICS January 2026 Data Landscape

The RICS Residential Market Survey for January 2026 represents a watershed moment for the UK housing sector. After months of persistent negativity, the data reveals three consecutive months of improvement in buyer enquiries, with the net balance climbing from -29% in November to -15% in January.[1] This steady progression indicates genuine momentum rather than a temporary spike.

Decoding Net Balance Metrics

Net balance measures the difference between surveyors reporting increases versus decreases. A reading of -15% for buyer enquiries means that while more surveyors still report falling enquiries than rising ones, the gap has narrowed significantly. For building surveyors, this translates to:

- Stabilizing workload projections after a prolonged downturn

- Improved client confidence leading to more comprehensive survey requests

- Greater willingness to proceed with purchases despite identified defects

The agreed sales net balance of -9% represents particularly encouraging news.[1] This metric directly correlates with building survey demand, as most lenders and prudent buyers commission detailed inspections before exchange.

Price Stabilization Across the UK

National house prices have entered a stabilization phase, with the net balance for the past three months standing at -10%, a marked improvement from -19% in October 2025.[1] The average UK property asking price reached £368,019 as of February 2026, with month-on-month growth of 0.3% and annual growth at 1%.[2][3]

This stabilization creates a critical environment for surveyors:

| Metric | October 2025 | January 2026 | Trend |

|---|---|---|---|

| Price Net Balance | -19% | -10% | ⬆️ Improving |

| Buyer Enquiries | -29% | -15% | ⬆️ Improving |

| Agreed Sales | -17% | -9% | ⬆️ Improving |

| 12-Month Sales Outlook | +18% | +35% | ⬆️ Strong Growth |

"The 12-month sales outlook surged to +35% net balance—the strongest reading since December 2024—indicating substantially improved surveyor confidence in medium-term market conditions."[1]

Preparing Building Surveys for Regional Market Divergence

One of the most significant insights from Preparing Building Surveys for UK Housing Market Recovery 2026: Lessons from RICS January Data is the pronounced regional performance gap. Understanding these geographical variations is essential for surveyors adapting their risk assessment protocols and resource allocation.

High-Growth Regions: Scotland, Wales, and Northern England

Scotland and Wales have emerged as unexpected champions of the 2026 recovery, with annual growth rates of 4.9% and 5.0% respectively.[1][4] Northern Ireland, the North West, and North of England also report upward price trends.[1]

Why these regions are outperforming:

- ✅ Relative affordability compared to southern markets

- ✅ Strong local employment in key sectors

- ✅ Migration patterns from high-cost areas

- ✅ First-time buyer accessibility with lower deposit requirements

For surveyors operating in these markets, the implications are clear:

Volume Management: Expect increased demand for homebuyer reports and building surveys as transaction velocity accelerates. Survey backlogs of 3-4 weeks are becoming common in Scottish cities.

Property Type Focus: Terraced houses and semi-detached properties in these regions attract significant first-time buyer interest. These properties often require detailed subsidence surveys due to age and construction methods.

Risk Calibration: Buyers in growth markets may exhibit greater risk tolerance, accepting minor defects to secure properties quickly. Surveyors must ensure comprehensive reporting despite client pressure to expedite.

Underperforming Regions: London and the South East

London, the South East, South West, and East Anglia continue to lag behind the national average, reflecting ongoing affordability challenges.[1] However, conditions have improved modestly even in these areas.

Challenges facing southern markets:

- ⚠️ High price-to-income ratios limiting buyer pools

- ⚠️ Mortgage affordability stress at current interest rates

- ⚠️ Stamp duty burden disproportionately affecting higher-value properties

- ⚠️ Competition from rental market as buying becomes less accessible

Survey Strategy Adjustments:

Building surveyors in these regions should anticipate:

- More cautious buyers requesting detailed structural surveys to justify significant financial commitments

- Increased negotiation leverage when defects are identified, as buyers have more bargaining power

- Greater scrutiny of older properties where renovation costs could tip affordability calculations

- Higher demand for specialist reports including drone roof surveys and specific defect assessments

Regional Divergence Impact on Survey Protocols

The widening gap between high-growth and underperforming regions requires surveyors to adopt location-specific risk frameworks:

Scotland/Wales Protocol:

- Prioritize rapid turnaround times (5-7 working days)

- Focus on deal-breaking defects rather than comprehensive minor issues

- Prepare for higher volumes with streamlined reporting templates

- Maintain quality standards despite pressure for speed

London/South East Protocol:

- Allow extended investigation time for complex properties

- Provide detailed cost estimates for identified defects

- Include market context in valuation commentary

- Offer follow-up consultations to support buyer negotiations

Risk Spotting in Early Recovery Phases: Critical Defects Surveyors Must Prioritize

The +35% net balance in 12-month sales expectations[1] signals that surveyors should prepare for increased transaction volumes throughout 2026. However, early recovery phases present unique challenges for building survey professionals. When market sentiment shifts from pessimism to optimism, buyer behavior changes dramatically—often to their detriment.

The Recovery Rush Phenomenon

Historical patterns show that as confidence returns, buyers become less risk-averse and more time-sensitive. The fear of missing out (FOMO) on price increases can lead to:

- 📉 Reduced due diligence periods

- 📉 Acceptance of survey findings without price renegotiation

- 📉 Pressure on surveyors to expedite reports

- 📉 Skipping comprehensive surveys in favor of basic valuations

This creates a professional and ethical imperative for surveyors to maintain rigorous standards. Understanding what survey you need becomes crucial for both surveyors advising clients and buyers making informed decisions.

Priority Defect Categories for 2026 Recovery

Based on RICS data and market conditions, surveyors should prioritize these critical defect categories:

1. Structural Integrity Issues 🏗️

With UK house prices expected to rise by 3% in 2026[3], buyers may overlook significant structural concerns. Surveyors must thoroughly investigate:

- Foundation movement and subsidence: Particularly critical in clay soil areas experiencing climate-related ground movement

- Roof structure deterioration: Many properties deferred maintenance during the downturn

- Wall tie failure: Common in 1920s-1970s cavity wall construction

- Timber decay in load-bearing elements: Hidden issues that worsen during market downturns

Residential structural engineers should be recommended for any property showing signs of progressive movement or structural compromise.

2. Damp and Water Ingress 💧

The UK's challenging weather conditions during 2024-2025 have exacerbated moisture-related problems:

- Rising damp from failed or absent damp-proof courses

- Penetrating damp through deteriorated pointing and render

- Condensation issues in poorly ventilated properties

- Roof leaks from deferred maintenance

These issues often worsen exponentially if left unaddressed, making early identification critical.

3. Building Services and Systems ⚡

Aging infrastructure presents significant cost implications:

- Electrical installations beyond their 25-30 year safe lifespan

- Heating systems with declining efficiency and safety concerns

- Drainage systems with root ingress or structural failure

- Insulation deficiencies affecting energy performance certificates (EPCs)

4. Regulatory Compliance Gaps 📋

Post-Grenfell awareness has heightened focus on:

- Fire safety measures in converted flats and HMOs

- Building regulation compliance for previous alterations

- EPC ratings below minimum rental standards (E rating or above)

- Asbestos presence in pre-2000 properties

Enhanced Reporting for Recovery Markets

Surveyors should adapt their reporting approach to match market conditions:

Standard Elements:

- Clear executive summary highlighting deal-breaking defects

- Categorized defect severity (urgent, significant, minor)

- Cost estimates for remediation works

- Prioritized action plan for buyers

Enhanced Recovery Elements:

- Market context commentary: How identified defects compare to typical properties in the area

- Investment risk assessment: Long-term implications of deferring repairs

- Negotiation guidance: Reasonable price adjustments based on defect severity

- Future-proofing recommendations: Energy efficiency and climate resilience upgrades

Operational Strategies for Surveying Firms: Scaling for Volume Growth

The RICS data pointing to +35% improved sales expectations[1] and +43% of surveyors anticipating higher prices[1] creates a clear mandate: firms must prepare for significant volume increases throughout 2026.

Capacity Planning and Resource Allocation

Immediate Actions (Q1-Q2 2026):

- Workforce expansion: Recruit additional qualified surveyors or partner with chartered surveyors across London and high-growth regions

- Technology investment: Implement digital survey tools, thermal imaging equipment, and drone survey capabilities

- Streamlined scheduling: Develop efficient booking systems to manage 20-30% volume increases

- Template optimization: Create region-specific report templates that maintain quality while improving turnaround

Medium-Term Strategies (Q3-Q4 2026):

- Training programs: Upskill junior surveyors to handle routine inspections independently

- Specialist development: Build expertise in high-demand areas like commercial building surveys

- Geographic expansion: Establish presence in high-growth regions (Scotland, Wales, North West)

- Client relationship management: Develop partnerships with estate agents and mortgage brokers in growth markets

Quality Control in High-Volume Environments

Maintaining professional standards during volume surges requires systematic approaches:

✅ Peer review protocols: Implement mandatory second-surveyor reviews for complex properties

✅ Standardized checklists: Ensure comprehensive coverage despite time pressures

✅ Continuous professional development: Regular training on emerging defect patterns and construction methods

✅ Client communication frameworks: Clear expectations on turnaround times and report scope

✅ Professional indemnity insurance: Review coverage limits to match increased exposure

Pricing Strategy for Recovery Markets

The improving market conditions create opportunities for strategic pricing:

Regional Pricing Differentiation:

- High-growth regions (Scotland/Wales): Premium pricing justified by tight capacity and strong demand

- Underperforming regions (London/SE): Competitive pricing to maintain market share

- Volume discounts: Structured packages for repeat clients (estate agents, developers)

Service Tier Optimization:

- Express service: 20-30% premium for 48-hour turnaround

- Standard service: 5-7 working days at base rates

- Comprehensive service: Extended investigations with specialist input

Technology and Innovation in Building Surveys for 2026

The market recovery coincides with rapid technological advancement in surveying practices. Firms that embrace innovation will capture disproportionate market share.

Digital Survey Tools

Modern surveying increasingly relies on:

- Thermal imaging cameras: Identifying hidden damp, insulation defects, and heat loss

- Moisture meters: Quantifying damp severity beyond visual inspection

- Drone technology: Safe, cost-effective roof surveys for tall or dangerous-access properties

- 3D laser scanning: Creating detailed property models for complex structures

- Digital reporting platforms: Client portals with interactive reports and photo annotations

Data-Driven Risk Assessment

Leveraging market data improves survey accuracy:

- Regional defect databases: Tracking common issues by property age and location

- Price trend integration: Contextualizing findings within local market conditions

- Predictive analytics: Identifying high-risk property characteristics

- Comparative analysis: Benchmarking against similar properties

Client Experience Enhancement

Technology improves service delivery:

- Online booking systems: 24/7 scheduling with instant confirmation

- Real-time updates: SMS/email notifications of survey progress

- Digital report delivery: Interactive PDFs with video walkthroughs

- Follow-up consultation: Video calls to discuss findings and recommendations

Commercial and Specialized Survey Opportunities

The residential recovery creates spillover demand in related sectors:

Commercial Property Surveys

Business confidence typically follows residential market improvements. Surveyors should prepare for increased demand in:

- Retail premises: High street recovery as consumer spending improves

- Office conversions: Continued residential conversion projects

- Industrial units: E-commerce logistics expansion

- Mixed-use developments: Urban regeneration projects

Understanding commercial building survey requirements positions firms for diversified revenue streams.

Specialist Survey Services

Niche expertise commands premium fees:

- Schedule of condition reports: For lease negotiations and tenant protections

- Boundary surveys: Resolving property line disputes before purchase

- Snagging inspections: New-build quality assurance

- Energy performance assessments: EPC upgrades and retrofit planning

Future Outlook: Sustaining Success Beyond 2026

While the RICS January data provides encouraging signals, surveyors must maintain perspective on longer-term market dynamics.

Potential Headwinds

⚠️ Interest rate volatility: Mortgage affordability remains sensitive to Bank of England policy

⚠️ Economic uncertainty: Inflation, employment, and geopolitical factors could dampen recovery

⚠️ Regulatory changes: Building safety legislation and EPC requirements may increase compliance costs

⚠️ Climate risks: Extreme weather events affecting property insurability and values

Sustainable Growth Strategies

Successful firms will:

- Diversify service offerings across residential, commercial, and specialist surveys

- Build regional presence in multiple markets to balance geographic risks

- Invest in professional development maintaining RICS standards and emerging expertise

- Develop strategic partnerships with estate agents, solicitors, and mortgage brokers

- Embrace technology while maintaining personal client relationships

- Monitor market indicators adjusting capacity and pricing proactively

Conclusion

Preparing Building Surveys for UK Housing Market Recovery 2026: Lessons from RICS January Data reveals a market at an inflection point. The dramatic improvement in surveyor confidence—with 12-month sales expectations at +35% and price expectations showing +43% anticipating increases[1]—creates both opportunity and responsibility for building survey professionals.

The regional divergence between high-growth markets (Scotland, Wales, Northern England) and underperforming areas (London, South East) demands location-specific strategies for risk assessment, pricing, and service delivery. Surveyors who adapt quickly to these geographical variations will capture disproportionate market share.

Most critically, the early recovery phase requires enhanced vigilance in identifying critical defects. As buyer confidence returns and transaction velocity accelerates, the temptation to rush due diligence increases. Professional surveyors must maintain rigorous standards, ensuring clients understand the long-term implications of structural, damp, and compliance issues.

Actionable Next Steps

For surveying firms positioning for 2026 growth:

✅ Review capacity planning: Assess current staffing against projected 20-35% volume increases

✅ Invest in technology: Implement digital tools that improve efficiency without compromising quality

✅ Develop regional expertise: Build knowledge of high-growth markets and their specific defect patterns

✅ Enhance reporting standards: Create templates that balance comprehensive coverage with rapid turnaround

✅ Monitor RICS data: Track monthly indicators to adjust strategy proactively

✅ Strengthen professional networks: Build relationships with estate agents and mortgage brokers in growth regions

The UK housing market recovery of 2026 presents a generational opportunity for building surveyors who prepare systematically. By combining data-driven insights from RICS with operational excellence and unwavering professional standards, surveying firms can achieve sustainable growth while protecting buyer interests in an accelerating market.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] House Prices – https://moneyweek.com/investments/house-prices/house-prices

[3] Landlord Press Review February 2026 – https://www.rentila.co.uk/blog/landlord-press-review-february-2026/

[4] Valuation Strategies For The 2026 Uk Housing Recovery Regional Price Divergence And Surveyor Tactics – https://nottinghillsurveyors.com/blog/valuation-strategies-for-the-2026-uk-housing-recovery-regional-price-divergence-and-surveyor-tactics