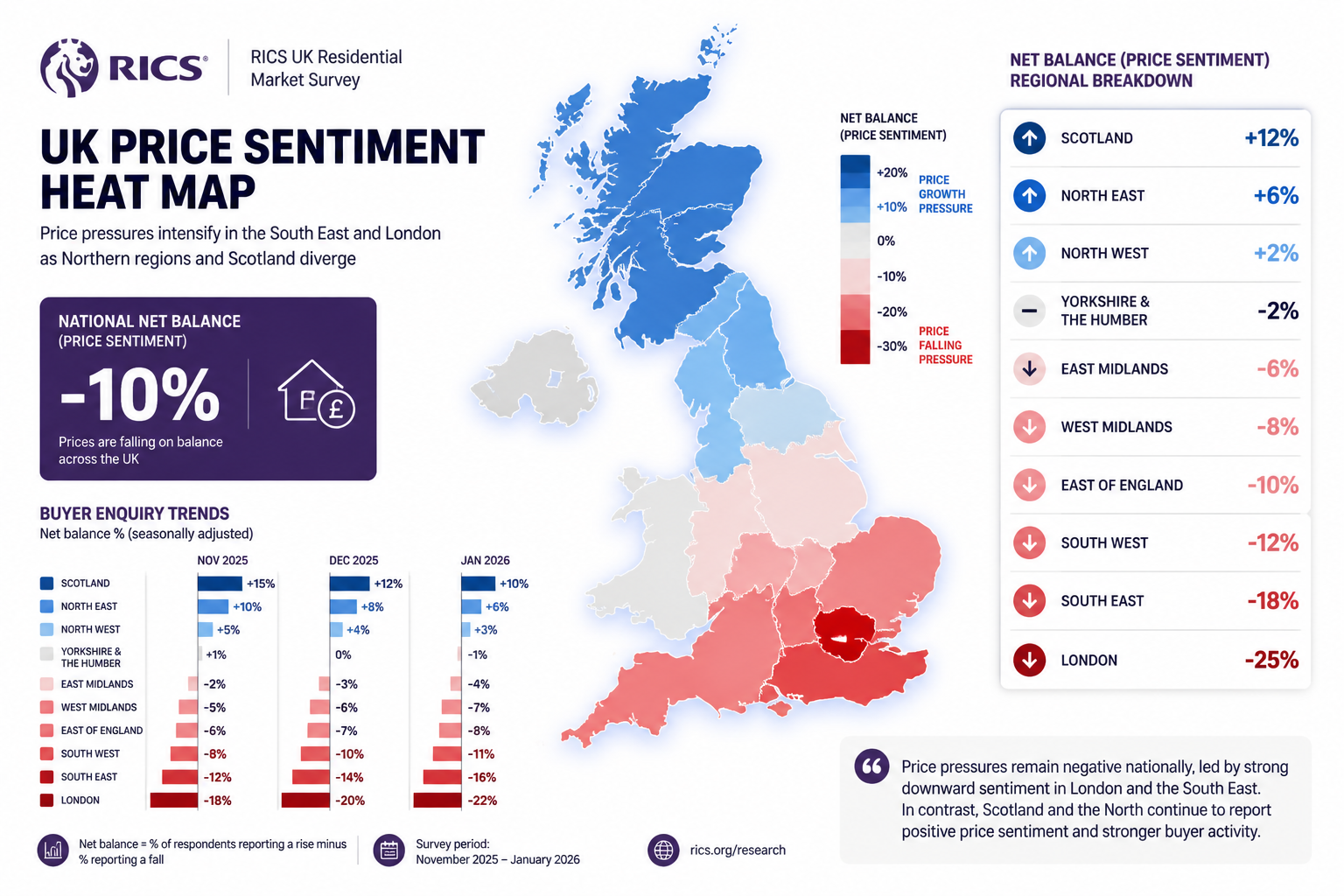

A net balance of -10% on national house prices sounds alarming — until you compare it to where the market sat just three months earlier. That single data point, drawn from the RICS UK Residential Market Survey January 2026, tells a story of cautious stabilisation at the national level while masking something far more significant underneath: a deepening regional fault line that is reshaping how building surveyors must approach valuations, Level 3 inspections, and expert witness work across the UK.

The RICS January 2026 Survey Insights: Building Surveyor Playbooks for Stabilising National Prices and Widening Regional Divides provides a timely framework for professionals navigating this two-speed property market. Whether operating in London's high-pressure micro-markets or assessing period terraces in the North, surveyors who understand the data — and adapt their playbooks accordingly — will be best positioned to serve clients and protect their professional credibility.

Key Takeaways 📌

- National house prices are stabilising at a net balance of -10%, but regional divergences are accelerating — creating distinct valuation environments across the UK.

- Buyer enquiries and agreed sales are recovering, with the 12-month sales outlook hitting +35%, the strongest reading since December 2024. [1]

- 43% of respondents expect prices to rise over the next year — the most optimistic reading since February 2025. [1]

- The lettings market faces a structural supply crisis: tenant demand is rising while landlord instructions remain firmly negative, pushing rents higher. [1]

- Workforce upskilling — not automation — is the top productivity driver for construction professionals, with upskilling averaging 47% high-impact ratings across regions. [2]

Understanding the RICS January 2026 Data: What the Numbers Actually Mean

National Stabilisation: Reading Beyond the Headline

The headline price balance of -10% represents a market that is contracting, but contracting far more slowly than in previous months. More importantly, the direction of travel is clear. New buyer enquiries improved to a net balance of -15% in January 2026, up from -21% in December and -29% in November — a consistent three-month trajectory of easing downward pressure. [1]

Agreed sales reached their least negative reading since June 2025, recording a net balance of -9%. [1] For building surveyors, this matters because transaction volumes directly influence instruction levels. A recovering sales pipeline means more homebuyer reports and full building surveys coming through the door.

💬 "The twelve-month sales sentiment of +35% is the strongest reading since December 2024 — a signal that market participants are beginning to look past near-term uncertainty." [1]

The short-term three-month sales outlook sits at a more cautious +4%, reflecting that confidence is building but has not yet fully translated into immediate transaction activity. [1]

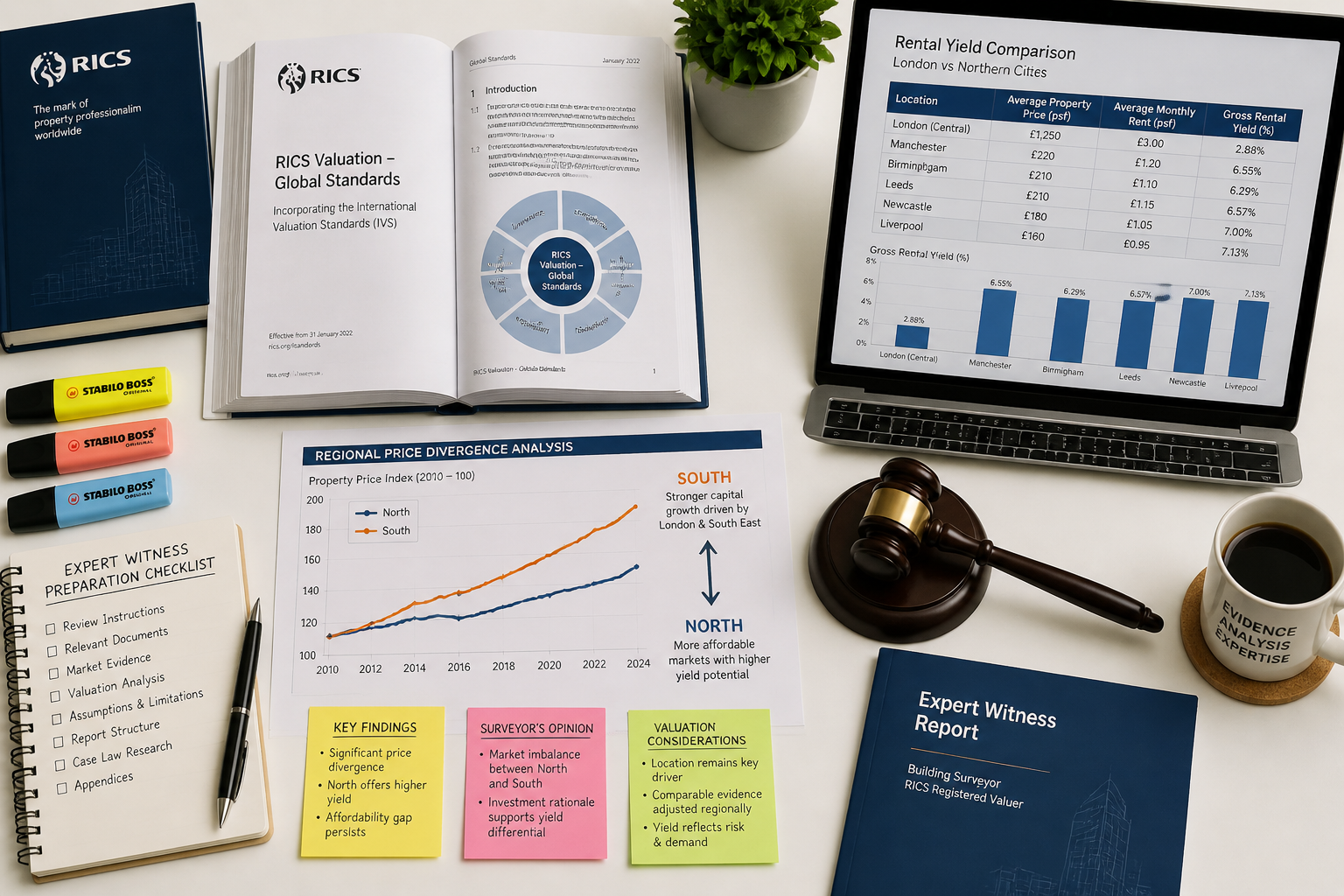

The Regional Divide: Where the Real Story Lives

The national figure smooths over a picture that is considerably more complex at the regional level. Surveyors operating across different geographies are reporting markedly different conditions:

| Region | Price Sentiment | Key Driver |

|---|---|---|

| London & South East | Relatively resilient | International demand, supply constraints |

| Midlands | Mixed/neutral | Affordability improving, local employment |

| Northern England | Softer sentiment | Wage growth lagging price recovery |

| Scotland & Wales | Variable | Policy divergence, stamp duty changes |

This divergence is not merely academic. It has direct implications for how surveyors calibrate comparable evidence, structure valuation reports, and advise clients on realistic price expectations. A chartered surveyor in London faces a fundamentally different evidence base than a colleague operating in the North East. [6]

For those working across South West London or in high-demand zones like Chelsea, the stabilisation story is more nuanced — premium stock continues to attract competitive interest, while mid-market properties show the most sensitivity to mortgage rate movements.

Building Surveyor Playbooks: Practical Adjustments for a Diverging Market

Adapting Level 3 Survey Methodology for Regional Conditions

The RICS January 2026 Survey Insights: Building Surveyor Playbooks for Stabilising National Prices and Widening Regional Divides are not just about pricing data — they are about how surveyors translate market intelligence into better professional outputs.

Level 3 Building Surveys (formerly known as Full Structural Surveys) require surveyors to provide context on market conditions as part of their overall assessment. In a diverging market, this means:

✅ Adjusting comparable selection — Using tighter geographic boundaries when regional divergence is high. A comparable from 15 miles away may now be less reliable than it was 18 months ago.

✅ Flagging market condition caveats — Reports should explicitly note whether the subject property sits in a strengthening or softening micro-market.

✅ Reassessing reinstatement cost assumptions — Construction cost inflation varies by region, affecting reinstatement cost valuations and insurance adequacy assessments.

✅ Defect prioritisation in context — In a softer market, the financial impact of identified defects on achievable price is proportionally greater. Surveyors should quantify remediation cost ranges with greater precision.

For properties with complex structural issues, a structural survey in London or equivalent regional assessment should include explicit commentary on how identified defects interact with current local market sentiment.

Choosing the Right Survey Type in an Uncertain Market 🔍

One of the most common questions clients ask in a stabilising market is whether they need a full Level 3 survey or whether a homebuyer report will suffice. The answer depends heavily on property type, age, and — crucially — regional market conditions.

Understanding the difference between a homebuyer report and a building survey has never been more important. In markets where prices are softening and buyers hold more negotiating power, a comprehensive Level 3 report provides the detailed defect evidence needed to support price renegotiation. In competitive markets, buyers may be tempted to cut corners — a risk that surveyors should actively counsel against.

Key factors driving survey type selection in 2026:

- Property age — Pre-1919 stock requires Level 3 as standard

- Construction type — Non-standard construction demands full investigation regardless of market conditions

- Transaction purpose — Investment purchases warrant more thorough due diligence

- Regional market temperature — Softening markets increase the financial stakes of undetected defects

The Lettings Market: A Separate Playbook for Rental Property Surveyors

The lettings sector presents its own set of challenges. Tenant demand improved across the three months to January 2026, ending two consecutive quarters of flat or negative readings. [1] However, landlord instructions remain firmly negative, creating a structural supply squeeze that is driving rental price increases across most regions. [1]

For surveyors working on rental properties, this imbalance has practical consequences:

- Dilapidations assessments become more contentious as landlords seek to maximise recovery from departing tenants in a tight market. Understanding dilapidation surveys and schedules of dilapidations is essential.

- Condition reports at the start of tenancy carry greater evidential weight when the rental market is under pressure.

- Commercial landlords face similar dynamics — commercial building surveys in London need to account for rising tenant expectations alongside tighter supply.

Expert Witness Preparation and the North-South Valuation Divide

Why Regional Divergence Creates Expert Witness Complexity

The widening regional divide identified in the RICS January 2026 Survey Insights: Building Surveyor Playbooks for Stabilising National Prices and Widening Regional Divides has significant implications for surveyors preparing expert witness reports. When price sentiment diverges sharply between regions, valuation disputes become harder to resolve using national benchmarks.

Surveyors acting as expert witnesses in 2026 must:

- Anchor opinions to hyper-local evidence — National indices are increasingly unreliable as primary comparables in contested valuations.

- Document market conditions at the date of valuation — The January 2026 data shows conditions changing month-to-month; precise dating of evidence is critical.

- Address the regional divergence explicitly — Courts and tribunals expect experts to acknowledge macro-market context and explain how it has been weighted.

- Use RICS-compliant methodology — Updated building survey quality standards for 2026 emphasise enhanced inspection requirements and clearer reporting protocols. [3]

💬 "43% of respondents anticipate higher prices over the year ahead — the most positive price outlook since February 2025. Expert witnesses must account for this forward-looking sentiment when advising on current market value." [1]

Productivity and the Surveyor Workforce: Building Better Playbooks

The RICS Construction Productivity Report 2026 adds another layer to the professional development picture. Its central finding is striking: workforce skills, not technology, remain the primary driver of productivity improvement across the construction sector. [2]

Upskilling averages 47% high-impact ratings and ranks as the top intervention in four of five regions surveyed. [2] For building surveyors, this validates investment in:

- Advanced defect diagnosis training

- Regional market specialisation

- Expert witness qualification pathways

- Digital reporting tools that support (not replace) professional judgment

Notably, automation receives only 17% high-impact ratings in the UK — the lowest of any intervention measured. [2] This suggests that surveyors who invest in deep professional expertise will outperform those who rely primarily on technology shortcuts.

Perhaps most concerning: one in five UK firms never measure productivity at all, and no single definition of productivity commands even 30% adoption in any region. [2] For surveying practices, this fragmentation represents both a risk and an opportunity — firms that establish clear productivity metrics and invest in staff development will gain a competitive edge.

Practical Playbook: Regional Specialisation Strategies 🗺️

Given the widening North-South divide, surveyors have a genuine opportunity to build regional expertise that commands premium fees. Here is a practical framework:

For London and South East specialists:

- Focus on leasehold complexity, lease extension valuations, and high-value residential surveys

- Develop expertise in period property defects common to Victorian and Edwardian stock

- Build capacity for drone roof surveys on hard-to-access urban properties

For surveyors in transitional markets (Midlands, commuter belt):

- Develop comparative valuation skills that bridge urban and rural evidence bases

- Build expertise in mixed-use and conversion properties

- Strengthen Red Book valuation competency for lender-instruction work

For Northern and regional market specialists:

- Focus on affordability-sensitive buyer advisory services

- Develop expertise in older housing stock condition assessment

- Build relationships with local estate agents to access early comparable data

What the Construction Productivity Data Means for Survey Quality

The productivity findings from RICS 2026 research [2] have a direct application to survey quality standards. If upskilling is the highest-impact intervention, then the question becomes: what skills matter most in a diverging market?

Three capabilities stand out:

| Skill Area | Why It Matters in 2026 | Development Path |

|---|---|---|

| Regional market analysis | Price divergence requires localised expertise | RICS CPD, local market immersion |

| Defect cost quantification | Softening markets amplify defect impact on value | Contractor liaison, cost database training |

| Expert witness communication | More valuation disputes expected | RICS Expert Witness qualification |

Conclusion: Turning Market Intelligence Into Professional Advantage

The RICS January 2026 Survey Insights: Building Surveyor Playbooks for Stabilising National Prices and Widening Regional Divides present a clear message: the UK property market is not one market — it is many. National stabilisation at a -10% price balance masks accelerating regional divergence that demands a more sophisticated, localised approach from every building surveyor in practice today.

The recovery signals are genuine. Buyer enquiries are improving, agreed sales are trending upward, and 43% of respondents expect prices to rise over the next 12 months. [1] But the lettings supply crisis, the construction productivity skills gap, and the deepening North-South divide mean that complacency carries real professional risk.

Actionable Next Steps for Building Surveyors in 2026 ✅

- Audit your comparable evidence sources — Are they sufficiently localised to reflect regional divergence?

- Review your Level 3 survey template — Does it include explicit market condition commentary aligned with RICS 2026 standards? [3]

- Invest in upskilling — The RICS productivity data is unambiguous: people-focused development outperforms technology investment. [2]

- Develop a regional specialisation — The North-South divide creates genuine fee premium opportunities for recognised local experts.

- Prepare for more expert witness instructions — Valuation disputes increase in diverging markets; build your CPD record now.

- Stay current with RICS survey data — Monthly RICS residential market surveys are the most reliable leading indicator available to practitioners. [4]

The surveyors who thrive in 2026 will be those who treat market intelligence not as background reading, but as an active input into every report they write, every valuation they defend, and every client conversation they have.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] RICS Construction Productivity Report 2026 – https://www.rics.org/news-insights/rics-construction-productivity-report-2026

[3] Building Survey Quality Standards 2026 Navigating RICS Updates And Enhanced Home Inspection Requirements – https://nottinghillsurveyors.com/blog/building-survey-quality-standards-2026-navigating-rics-updates-and-enhanced-home-inspection-requirements

[4] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[6] Market View January 2026 – https://www.watsons-property.co.uk/market-view-january-2026/