The UK buy-to-let market stands at a critical crossroads in 2026. With steeper tax bills forcing thousands of landlords to exit the market, property investors face unprecedented challenges in assessing portfolio viability. The convergence of mandatory Making Tax Digital (MTD) requirements, significant income tax increases, and the Renters' Rights Act has fundamentally altered the economics of rental property ownership. Understanding Valuation Challenges from Landlord Tax Pressures: Assessing Buy-to-Let Viability in Shrinking Supply 2026 has become essential for investors, surveyors, and property professionals navigating this transformed landscape.

As rental supply contracts and tenant demand remains robust, the paradox of rising rents alongside declining landlord participation creates unique valuation complexities. Professional surveyors must now integrate tax burden analysis, regulatory compliance costs, and market supply dynamics into their assessment methodologies.

Key Takeaways

- 📊 Making Tax Digital becomes mandatory from April 6, 2026 for over 860,000 landlords with combined gross income above £50,000, requiring quarterly digital submissions to HMRC

- 💰 Rental income tax rates increase by 2 percentage points from April 2027, with basic rate rising from 20% to 22%, higher rate from 40% to 42%, and additional rate from 45% to 47%

- 🏘️ The Renters' Rights Act eliminates Section 21 evictions from May 1, 2026, converting all fixed-term tenancies to rolling contracts and restricting landlord flexibility

- 📉 Landlord exodus continues as cumulative tax pressures force portfolio sales, paradoxically creating valuation challenges amid shrinking supply but sustained tenant demand

- 🔍 Professional valuation methodologies must evolve to incorporate tax burden modeling, compliance costs, and regulatory risk factors when assessing buy-to-let viability

Understanding the 2026 Tax Pressure Landscape

Making Tax Digital: The Administrative Burden

The Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) represents one of the most significant operational changes for landlords in 2026. From April 6, 2026, more than 860,000 sole traders and landlords with combined gross income exceeding £50,000 must adopt digital record-keeping and submit quarterly updates to HMRC[7].

The quarterly submission deadlines create a new administrative rhythm:

- First quarter: August 7, 2026

- Second quarter: November 7, 2026

- Third quarter: February 7, 2027

- Fourth quarter: May 7, 2027

Each quarterly update requires digital submission through MTD-compatible software, representing both direct costs (software subscriptions, accountant fees) and indirect costs (time investment, learning curves). For landlords managing multiple properties, this administrative burden compounds significantly.

The penalty structure adds further pressure. Late quarterly updates accumulate penalty points, with a £200 fine triggered once four points are reached[7]. While the government has provided a 12-month grace period without penalty points for those joining in April 2026, this temporary relief does little to address the ongoing compliance burden.

The Expanding MTD Net

The income threshold for MTD compliance follows a phase-down schedule that will progressively capture more landlords:

| Implementation Date | Income Threshold | Estimated Additional Landlords Affected |

|---|---|---|

| April 6, 2026 | £50,000+ | 860,000+ |

| April 6, 2027 | £30,000+ | Additional hundreds of thousands |

| April 6, 2028 | £20,000+ | Majority of buy-to-let landlords |

This cascading implementation means that even landlords currently below the threshold must plan for future compliance requirements. For professional property valuations in London, this forward-looking compliance burden must factor into investment viability assessments.

Income Tax Rate Increases: The 2027 Shock

Beyond administrative burdens, substantive tax rate increases take effect from April 2027. Rental income tax rates will rise by 2 percentage points across all bands[1]:

- Basic rate: 20% → 22%

- Higher rate: 40% → 42%

- Additional rate: 45% → 47%

Combined with frozen income tax thresholds until 2030/31, this creates a phenomenon known as fiscal drag—where inflation pushes more landlords into higher tax brackets without any real income increase.

Government Justification and Political Context

The government has publicly defended these tax increases with a fairness argument. Labour officials have stated that "it's not fair" that landlords pay less in tax than their tenants, positioning the reforms as making the tax system "fairer" by having "the wealthiest contribute the most"[4].

This political framing reveals the challenging environment for buy-to-let investors. Rather than viewing rental property as a legitimate investment class contributing to housing supply, the government narrative increasingly portrays landlords as undertaxed beneficiaries requiring correction.

For surveyors conducting Red Book valuations in London, this political environment introduces regulatory risk that must be factored into long-term investment assessments.

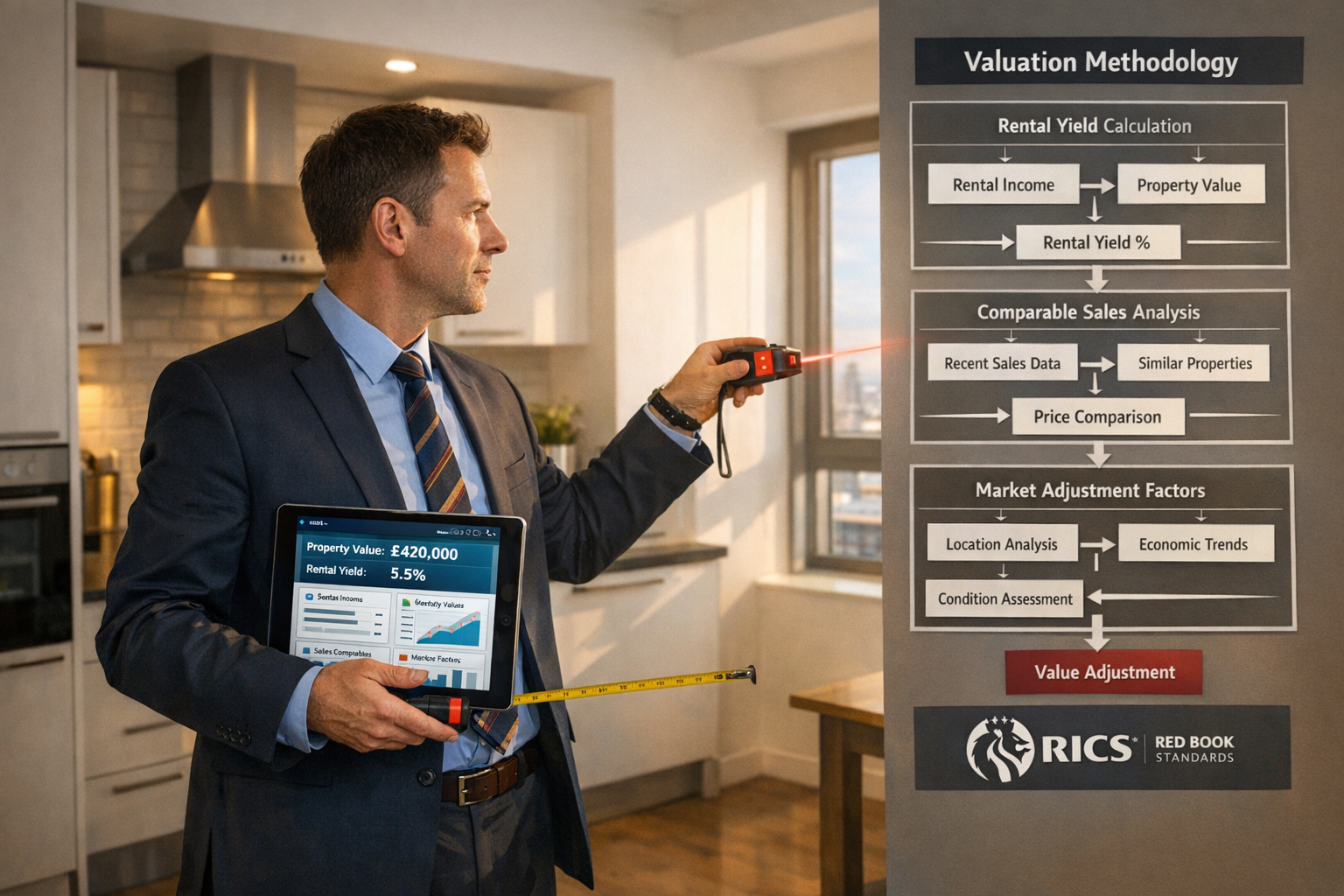

Valuation Challenges from Landlord Tax Pressures in Practice

Integrating Tax Burden into Valuation Models

Traditional property valuation methodologies focused primarily on comparable sales, rental yield, and capital appreciation potential. However, the 2026 tax landscape demands a more sophisticated approach that integrates net-of-tax returns into viability assessments.

Key valuation adjustments required:

- Net yield calculations: Gross rental yield must be adjusted for the increased tax burden, particularly for higher and additional rate taxpayers

- Compliance cost deductions: Annual MTD software subscriptions (£150-£500) and accountancy fees (£500-£2,000+) reduce net returns

- Time-cost valuations: Administrative time requirements for quarterly submissions represent opportunity costs

- Risk premiums: Regulatory uncertainty and potential future tax increases warrant higher discount rates

For example, consider a London rental property generating £30,000 annual rental income. Under the previous 40% higher rate tax regime, the landlord retained £18,000 after tax. Under the new 42% rate (from April 2027), this drops to £17,400—a £600 annual reduction (3.3% decline in net income).

When capitalized over a typical 10-year investment horizon and discounted appropriately, this represents a material reduction in property value that professional valuers must quantify.

The Section 24 Mortgage Interest Restriction Legacy

While not new in 2026, the Section 24 mortgage interest restriction continues to amplify tax pressures. Since 2017, mortgage interest relief has been restricted to the basic rate (20%), regardless of the landlord's marginal tax rate.

For highly leveraged portfolios, this creates a double squeeze:

- Mortgage interest only receives 20% tax relief

- Rental income faces 42% or 47% tax rates (from April 2027)

This asymmetry can push properties into negative cash flow territory, particularly in high-value London markets where mortgage costs are substantial. Surveyors must model these financing costs explicitly when assessing buy-to-let viability.

Renters' Rights Act: Valuation Impact of Reduced Flexibility

The Renters' Rights Act, implemented May 1, 2026, fundamentally alters landlord-tenant dynamics[2]. All existing fixed-term Assured Shorthold Tenancies automatically convert to rolling, periodic tenancies without end dates.

Key valuation implications:

- ✋ Elimination of Section 21 "no-fault" evictions reduces landlord flexibility to regain possession

- 📈 Rent increases restricted to Section 13 process, which allows tenant challenges and tribunal reviews

- ⏱️ Extended void periods when possession is needed, as landlords must rely on Section 8 grounds requiring specific justifications

- 🏠 Property condition requirements increase, as disrepair becomes a stronger tenant defense

For professional chartered surveyors in London, these regulatory changes introduce illiquidity risk. Properties that cannot be readily repossessed for sale or refurbishment command lower valuations due to reduced optionality.

Portfolio vs. Single-Asset Valuation Considerations

The cumulative tax pressures create divergent valuation dynamics between portfolio sales and individual property transactions.

Portfolio sales may command discounts due to:

- Urgent exit motivations from tax-pressured landlords

- Bulk transaction complexities

- Limited buyer pool for large acquisitions

Individual property sales may achieve premiums due to:

- Shrinking rental supply increasing scarcity value

- Owner-occupier buyers competing with investors

- Specific location or property characteristics

Surveyors conducting probate valuations in London for inherited rental portfolios must carefully assess whether portfolio disposal or phased individual sales maximizes estate value.

Assessing Buy-to-Let Viability in Shrinking Supply

The Supply-Demand Paradox

The UK rental market in 2026 presents a fascinating paradox: landlord numbers are declining while tenant demand remains robust. This creates upward pressure on rents even as the investment case for new landlords deteriorates.

Supply-side factors:

- 📉 Landlord exits accelerating due to tax pressures

- 🏗️ Limited new rental property construction

- 🔄 Properties converting from rental to owner-occupation

Demand-side factors:

- 👥 Population growth in urban centers, particularly London

- 🏡 Homeownership barriers (high prices, mortgage qualification difficulties)

- 🌍 International student and worker demand

This supply-demand imbalance supports rental growth projections that partially offset increased tax burdens. For surveyors assessing viability, the critical question becomes: do rental increases sufficiently compensate for tax rises and compliance costs?

Rental Growth Modeling in Valuation

Professional valuation of buy-to-let properties in 2026 requires dynamic rental growth modeling rather than static yield assumptions. Key considerations include:

- Local market analysis: London submarkets exhibit varying rental growth trajectories based on transport links, employment hubs, and demographic trends

- Property type differentials: Family homes, young professional apartments, and HMOs (Houses in Multiple Occupation) face different demand dynamics

- Quality premiums: Well-maintained, energy-efficient properties command rental premiums and lower void periods

Example rental growth scenario:

A landlord in Southwest London holds a property generating £24,000 annual rent in 2026. If rental growth averages 4% annually (above general inflation), the property generates £28,800 by 2029. However, if tax rates increase from 40% to 42% in 2027, the net-of-tax income trajectory shows:

- 2026: £24,000 × 60% = £14,400 net

- 2027: £24,960 × 58% = £14,477 net (42% tax rate)

- 2028: £25,958 × 58% = £15,056 net

- 2029: £26,997 × 58% = £15,658 net

The rental growth provides only modest net income improvement, highlighting why many landlords are exiting despite rising rents.

Surveyor Techniques for Viability Assessment

Professional surveyors employ several specialized techniques when assessing Valuation Challenges from Landlord Tax Pressures: Assessing Buy-to-Let Viability in Shrinking Supply 2026:

1. Discounted Cash Flow (DCF) Analysis

DCF modeling projects future rental income, operating expenses, tax liabilities, and terminal value, then discounts to present value using an appropriate risk-adjusted rate. This technique explicitly captures:

- Year-by-year tax rate changes

- Rental growth trajectories

- Exit timing and capital gains tax implications

- Compliance cost escalation

2. Comparative Yield Analysis

Surveyors compare net rental yields (after tax and compliance costs) against alternative investments such as:

- REITs (Real Estate Investment Trusts)

- Dividend-paying equities

- Bond yields

- Commercial property

If buy-to-let net yields fall below alternative investments with similar risk profiles, the investment case weakens significantly.

3. Scenario Stress Testing

Given regulatory and tax uncertainty, robust valuations incorporate scenario analysis:

- Base case: Current tax regime with moderate rental growth

- Optimistic case: Strong rental growth offsetting tax increases

- Pessimistic case: Additional tax increases or rent controls

This approach provides valuation ranges rather than single-point estimates, better reflecting the uncertainty inherent in the 2026 landscape.

4. Portfolio Optimization Analysis

For multi-property landlords, surveyors can conduct portfolio optimization to identify:

- Properties with strongest viability metrics to retain

- Underperforming assets to dispose

- Geographic or property-type concentration risks

- Tax-efficient restructuring opportunities (e.g., limited company ownership)

The Limited Company Consideration

One potential mitigation strategy involves transferring properties to limited company ownership. Limited companies face Corporation Tax (currently 25% for profits above £250,000) rather than income tax rates, potentially offering tax advantages.

Advantages:

- Lower effective tax rate for higher-rate taxpayers

- Full mortgage interest deductibility

- More tax-efficient profit extraction through dividends

Disadvantages:

- Stamp Duty Land Tax on transfer (unless structured as incorporation relief)

- Capital Gains Tax on transfer from personal ownership

- More complex accounting and compliance requirements

- Mortgage refinancing typically required

For surveyors conducting retrospective valuations on property in London, understanding the ownership structure history is essential for accurate assessment.

Geographic Considerations: London vs. Regional Markets

Valuation Challenges from Landlord Tax Pressures: Assessing Buy-to-Let Viability in Shrinking Supply 2026 manifest differently across UK regions.

London characteristics:

- ✅ Strongest rental demand and growth potential

- ✅ Most resilient capital values

- ❌ Highest entry costs and leverage requirements

- ❌ Greatest mortgage interest restriction impact

Regional market characteristics:

- ✅ Lower entry costs and better gross yields

- ✅ Potentially positive cash flow despite tax pressures

- ❌ More variable rental demand

- ❌ Slower capital appreciation

Surveyors must calibrate their viability assessments to specific market dynamics. A property yielding 4% gross in Central London faces different viability calculus than a property yielding 7% gross in a regional city.

Strategic Responses for Landlords and Investors

Exit Strategies and Timing Considerations

For landlords concluding that buy-to-let viability has deteriorated irreversibly, exit strategy becomes paramount. Key considerations include:

Timing factors:

- 🕐 Pre-April 2027 sales avoid the higher income tax rates on final year rental income

- 📅 Capital Gains Tax planning to utilize annual exemptions and potentially lower rates

- 🏠 Market conditions balancing urgent exit against maximizing sale price

Disposal methods:

- Open market sales to owner-occupiers (potentially achieving premiums)

- Sales to sitting tenants (faster transactions, potentially discounted)

- Portfolio sales to institutional investors or other landlords

- Phased disposals spreading capital gains across multiple tax years

Professional expert witness reports in London may be required when disposal decisions involve disputes, partnership dissolutions, or divorce proceedings.

Optimization Strategies for Continuing Landlords

Landlords committed to remaining in the market despite tax pressures can implement several optimization strategies:

- Rental maximization: Regular rent reviews aligned with market conditions, property improvements commanding premium rents

- Expense optimization: Claiming all allowable expenses, particularly repairs and maintenance

- Compliance efficiency: Investing in quality MTD software and accountancy support to minimize time burden

- Property quality enhancement: Energy efficiency improvements (reducing tenant utility costs and commanding rent premiums)

- Tenant retention: Reducing void periods and turnover costs through proactive tenant management

New Entrant Considerations

Despite the challenging landscape, new landlord entrants may find opportunities in 2026:

Potential advantages:

- 🏘️ Reduced competition from exiting landlords

- 💰 Potential property price discounts from forced sellers

- 📈 Strong rental growth prospects from supply constraints

- 🎯 Ability to structure ownership tax-efficiently from the outset (e.g., limited company)

New entrants should commission comprehensive building surveys in London before acquisition to avoid unexpected capital expenditure that further erodes viability.

Conclusion

The convergence of Making Tax Digital requirements, income tax rate increases, and the Renters' Rights Act has fundamentally transformed the UK buy-to-let landscape in 2026. Valuation Challenges from Landlord Tax Pressures: Assessing Buy-to-Let Viability in Shrinking Supply 2026 requires sophisticated analysis that extends far beyond traditional comparable sales methodologies.

Professional surveyors must now integrate net-of-tax return modeling, compliance cost quantification, regulatory risk assessment, and dynamic rental growth projections into their valuation frameworks. The paradox of declining landlord numbers alongside sustained tenant demand creates both challenges and opportunities, with rental growth partially offsetting increased tax burdens.

For existing landlords, the viability question demands honest assessment of individual circumstances: tax position, portfolio composition, financing structure, and risk tolerance. Some will conclude that exit represents the optimal strategy, while others will implement optimization measures to maintain acceptable returns.

For prospective investors, the 2026 environment requires rigorous due diligence and realistic return expectations. The days of leveraged buy-to-let generating substantial tax-advantaged returns have largely ended, but opportunities remain for well-capitalized investors in strong rental markets.

Actionable Next Steps

For current landlords:

- 📊 Commission professional property valuations incorporating tax burden analysis

- 💻 Implement MTD-compatible accounting systems before the August 7, 2026 deadline

- 📈 Model rental growth scenarios against tax increase trajectories

- 🤔 Evaluate limited company restructuring with qualified tax advisors

- 📋 Develop 3-5 year portfolio strategy: optimize, hold, or exit

For prospective investors:

- 🔍 Focus on high-demand locations with strong rental growth prospects

- 💰 Prioritize lower-leverage strategies to minimize mortgage interest restriction impact

- 🏢 Consider limited company ownership structure from acquisition

- 📝 Commission comprehensive surveys and valuations before purchase

- 🎯 Set realistic return expectations aligned with post-tax economics

For property professionals:

- 📚 Enhance valuation methodologies to incorporate tax and regulatory factors

- 🔧 Develop scenario modeling tools for client viability assessments

- 🤝 Collaborate with tax advisors to provide integrated advice

- 📊 Monitor rental market supply-demand dynamics closely

- 📖 Maintain current knowledge of evolving tax and regulatory landscape

The buy-to-let market of 2026 demands more sophisticated analysis, realistic expectations, and professional guidance than ever before. Those who adapt their strategies and valuation approaches to this new reality will be best positioned to navigate the challenges ahead.

References

[1] Tax Changes For Landlords 2026 Complete Guide – https://www.djh.co.uk/latest-news/news-insights/tax-changes-for-landlords-2026-complete-guide/

[2] Landlords 2026 – https://theindependentlandlord.com/landlords-2026/

[4] Government Defends Landlord Tax Hikes As Fairer System – https://www.property118.com/government-defends-landlord-tax-hikes-as-fairer-system/

[7] Act Now 864000 Sole Traders And Landlords Face New Tax Rules In Two Months – https://www.gov.uk/government/news/act-now-864000-sole-traders-and-landlords-face-new-tax-rules-in-two-months