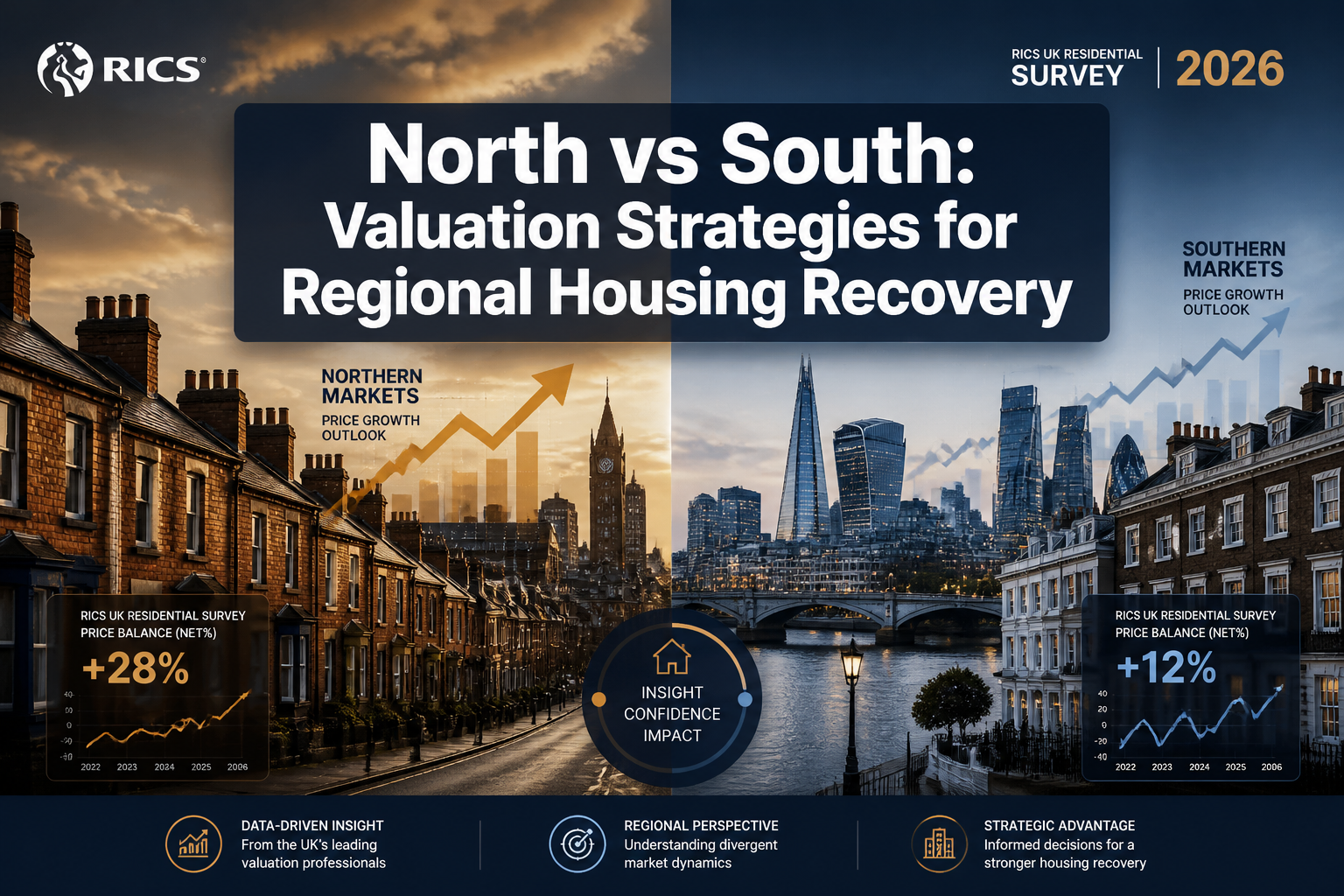

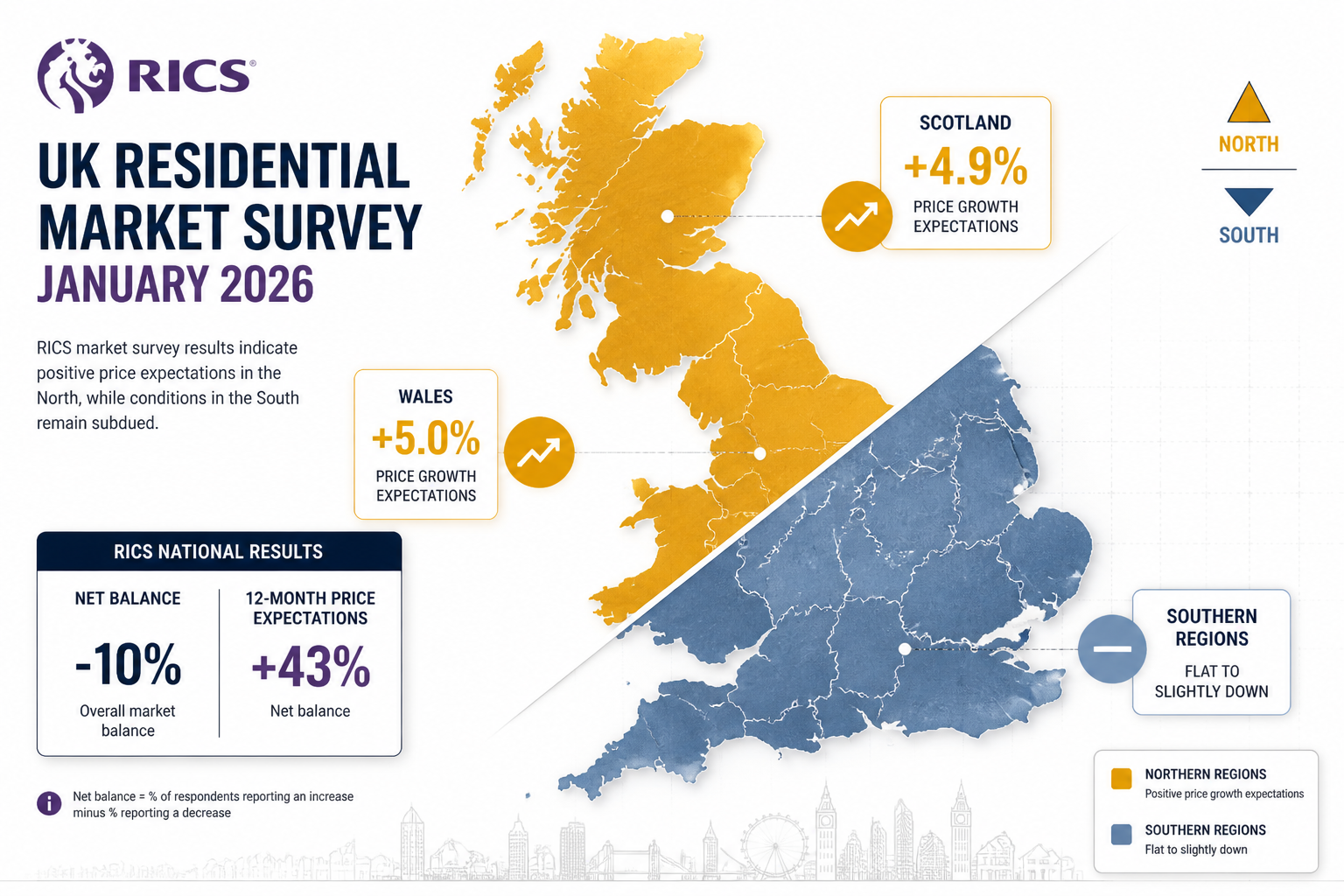

Scotland and Wales are outpacing London's housing market by a margin that would have seemed implausible just two years ago — posting annual price growth of 5.0% and 4.9% respectively while Southern England continues to drag behind the national average. This stark divergence sits at the heart of the Valuation Strategies for Regional Housing Recovery: North vs South Insights from RICS January 2026 Survey, and it is reshaping how chartered surveyors, buyers, and investors approach property appraisals across the UK in 2026.

The RICS January 2026 Residential Market Survey delivered a cautiously optimistic picture: a national price net balance of -10%, improving from -19% in October 2025, alongside a 12-month price expectation of +43% — the most positive forward-looking reading since February 2025 [1][3]. Yet beneath these headline figures lies a market that is anything but uniform. Understanding the regional fault lines is no longer optional for accurate valuation — it is essential.

Key Takeaways 📌

- Scotland and Wales lead price growth at ~5% annually, while London and the South East continue to underperform the national average.

- National sentiment is improving: the January 2026 net balance of -10% marks a meaningful recovery from -19% in October 2025 [3].

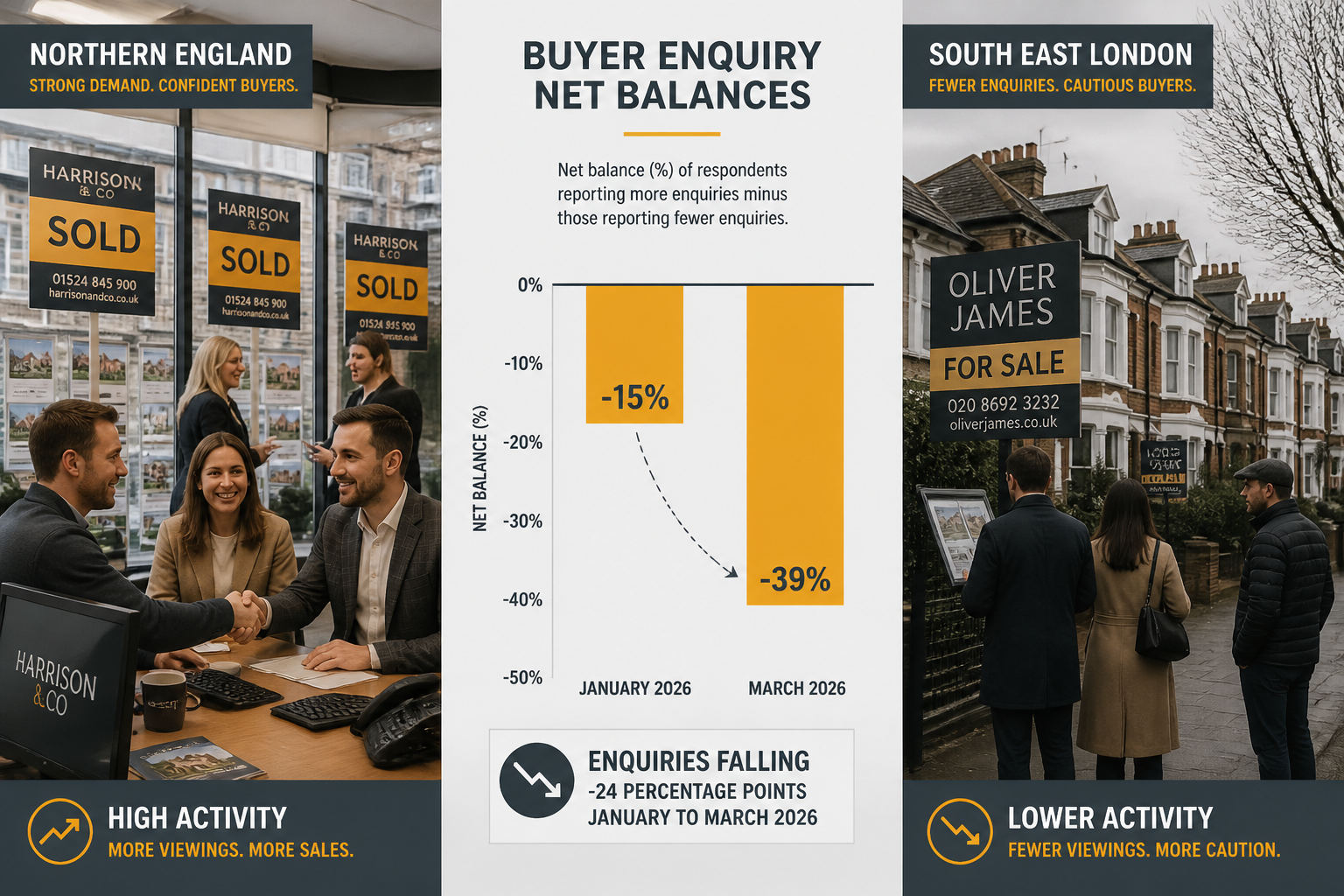

- Buyer demand is recovering slowly — enquiries rose from -29% in November to -15% in January, though March 2026 saw a sharp reversal to -39% [1][5].

- 12-month price expectations hit +43%, signalling strong medium-term confidence despite near-term volatility [3].

- Accurate regional valuation now requires surveyors to apply distinct methodologies for Northern growth markets versus Southern affordability-constrained zones.

The North-South Divide: What the RICS Data Actually Shows

The RICS January 2026 survey makes one thing unmistakably clear: the UK housing market is not recovering uniformly. It is recovering in patches — and the North is leading the charge.

Northern Regions: Momentum Builds

Scotland, Wales, and the North West of England are reporting consistent upward price pressure that contrasts sharply with the national picture [1][4]. Scotland's 4.9% and Wales's 5.0% annual growth rates reflect a combination of relative affordability, strong local employment markets, and a structural undersupply of quality housing stock.

The North West of England is similarly posting positive price movements, driven by cities like Manchester and Liverpool where regeneration investment has attracted younger buyers priced out of Southern markets. For surveyors operating in these regions, the challenge is not finding evidence of value — it is ensuring comparable evidence keeps pace with rapidly moving benchmarks.

💬 "The North is no longer playing catch-up — in many metrics, it is setting the pace."

Southern Regions: Affordability Continues to Bite

London, the South East, South West, and East Anglia continue to underperform the national average [1][3]. The reasons are well-documented: stretched affordability ratios, elevated mortgage costs relative to local incomes, and a buyer pool that remains cautious despite improving sentiment.

That said, conditions have improved modestly. The national net balance of -10% in January 2026 — up from -19% in October 2025 — suggests even Southern markets are finding a floor [3]. For surveyors working across South West London or South East London, this stabilisation matters: it signals that downward pressure on valuations may be easing, even if meaningful price growth remains some way off.

| Region | Price Trend (Jan 2026) | Relative to National Average |

|---|---|---|

| Scotland | +4.9% annually | Significantly above |

| Wales | +5.0% annually | Significantly above |

| North West England | Positive | Above |

| London | Negative/flat | Below |

| South East | Negative/flat | Below |

| South West | Negative/flat | Below |

Source: RICS UK Residential Market Survey, January 2026 [3]

Valuation Strategies for Regional Housing Recovery: North vs South Insights from RICS January 2026 Survey — Surveyor Tactics in Practice

Understanding the data is one thing. Translating it into accurate, defensible valuations is where professional skill separates good surveyors from great ones. The regional divergence captured in the Valuation Strategies for Regional Housing Recovery: North vs South Insights from RICS January 2026 Survey demands distinct approaches depending on geography.

Tactic 1: Recalibrate Comparable Evidence Timelines

In fast-moving Northern markets, relying on comparable sales from six or twelve months ago can significantly undervalue a property. Surveyors should:

- ✅ Prioritise comparables from the last 90 days wherever possible

- ✅ Apply upward adjustment factors where evidence of continued price growth is documented

- ✅ Cross-reference with active listing prices to sense-check sold data

In Southern markets, the opposite risk applies. Stale comparables from 2024 peaks may overstate current value, particularly in affordability-constrained zones. A comprehensive property valuation must account for where the market actually is, not where it was.

Tactic 2: Weight Forward-Looking Sentiment Appropriately

The RICS January 2026 survey recorded 12-month price expectations at +43% — the strongest reading since February 2025 [3]. This is a significant data point, but surveyors must be careful not to conflate sentiment with current market value.

Red-book valuations are anchored to current market evidence. However, for investment appraisals, development viability assessments, and freehold valuations, forward-looking expectations form a legitimate part of the analytical framework. The key is transparency: clearly distinguish between current market value and projected value based on recovery assumptions.

Tactic 3: Monitor Supply Signals Closely

New instructions recorded a near-neutral net balance of +1% in January (rising to +2% in February), indicating minimal fresh supply entering the market [1][5]. This supply constraint is particularly acute in the rental sector, where landlord instructions stood at -24% in January — improving from -34% but still deeply negative [3].

For surveyors advising landlords or buy-to-let investors, this data supports rental income assumptions that factor in continued upward pressure: +28% of respondents expect rental prices to rise in the near term [3]. This is relevant context for lease extension valuations and investment-grade appraisals alike.

Tactic 4: Account for Mortgage Rate Sensitivity by Region

Northern buyers typically purchase at lower absolute price points, meaning mortgage rate changes have a proportionally smaller cash impact on monthly payments than in the South. This makes Northern markets more resilient to rate fluctuations — a factor that should inform risk adjustments in valuation models.

Southern markets, particularly London and the South East, remain highly sensitive to borrowing cost movements. The March 2026 RICS survey — showing new buyer enquiries collapsing to -39% from January's -15% — demonstrates just how quickly sentiment can reverse when economic uncertainty rises [5]. Surveyors should build scenario-based sensitivity analysis into appraisals for higher-value Southern properties.

Demand, Supply, and the Recovery Timeline: Reading the RICS Signals

Buyer Enquiries: A Fragile Recovery

The trajectory of buyer enquiries tells a story of tentative recovery followed by renewed caution:

- November 2025: -29% net balance

- December 2025: -21% net balance

- January 2026: -15% net balance ✅ (improving)

- March 2026: -39% net balance ⚠️ (sharp deterioration)

This pattern — captured across the RICS survey series [1][3][5] — underscores why surveyors cannot rely on a single data point. The January improvement was real, but the March reversal, driven by rising borrowing costs and geopolitical uncertainty, demonstrates the fragility of early-stage recovery.

For buyers and sellers navigating this environment, working with expert surveyor advice becomes especially valuable. A skilled surveyor can contextualise market noise and provide grounded, evidence-based assessments rather than reactive appraisals.

Agreed Sales: Slow but Steady Progress

Agreed sales reached a net balance of -9% in January 2026 — the strongest reading since June 2025, with each monthly report showing progressive improvement [1][3]. This is meaningful: even in a market where demand is fragile, transactions are completing.

The twelve-month sales outlook surged to +35% — the strongest reading since December 2024 — reflecting growing confidence that the recovery, while uneven, has genuine legs [3].

What This Means for Valuation Timing

For clients considering when to commission a valuation, the data suggests:

| Scenario | Recommended Approach |

|---|---|

| Buying in Northern England/Scotland | Act promptly — prices moving upward |

| Buying in London/South East | Negotiate carefully — market still soft |

| Selling in Northern markets | Price at or slightly above recent comps |

| Selling in Southern markets | Price realistically; avoid 2024 peak assumptions |

| Investment/BTL anywhere | Factor rental supply constraints into yield models |

Applying Valuation Strategies for Regional Housing Recovery: North vs South Insights from RICS January 2026 Survey to Specific Property Types

New-Build and Development Appraisals

The near-neutral supply reading (+1% new instructions in January) masks an important nuance: new-build completions are adding to stock in Northern regeneration zones while Southern pipeline projects face viability pressures from elevated build costs [1][5].

For development appraisals, surveyors should apply residual land value models that reflect realistic sales rate assumptions by region. A Northern scheme may justify more optimistic absorption rates; a Southern scheme requires conservative assumptions given affordability constraints.

Leasehold Properties

With rental supply severely constrained (landlord instructions at -24%) and rental price expectations rising (+28% net balance) [3], leasehold flats in high-demand urban areas carry stronger investment appeal than their sales market performance might suggest. A thorough lease extension valuation is increasingly important for leaseholders considering whether to extend now or wait — particularly given the legislative changes reshaping the leasehold landscape.

Structural and Condition-Based Adjustments

Regional market strength does not eliminate the need for rigorous condition assessment. In Northern markets where prices are rising quickly, buyers may be tempted to overlook structural issues in competitive bidding situations. A structural survey or specific defect report provides the objective evidence needed to make informed decisions — and can be the difference between a sound investment and a costly mistake.

Similarly, in Southern markets where negotiation is more viable, a detailed survey can provide leverage to renegotiate the purchase price based on documented defects.

The February-March 2026 Warning: Don't Mistake a Pause for a Peak

One of the most important signals from the RICS survey series is the deterioration in near-term sentiment between January and March 2026. While January's data painted a picture of cautious optimism, February saw three-month sales expectations fall to +4% from the previous month's +22% [5]. March brought an even sharper reversal in buyer enquiries.

This does not invalidate the recovery narrative — 12-month expectations remain strongly positive at +43% [3]. But it does reinforce a critical principle for surveyors and their clients: recovery is rarely linear.

💬 "A market expecting +43% price growth over 12 months while recording -39% buyer enquiries in March is not contradicting itself — it is telling you that the path will be bumpy."

Valuation strategies must therefore be dynamic rather than static. Monthly RICS data should be tracked, comparable evidence refreshed regularly, and client advice updated to reflect the latest market conditions rather than a snapshot taken at a single point in time.

Conclusion: Actionable Steps for Surveyors and Property Owners in 2026

The Valuation Strategies for Regional Housing Recovery: North vs South Insights from RICS January 2026 Survey reveal a market in transition — recovering, but unevenly, and with significant volatility still in play. Here are the key actions to take right now:

For Surveyors:

- 🗺️ Segment your comparable evidence by region — do not apply national trend assumptions to local valuations.

- 📊 Update comparable databases monthly — in fast-moving Northern markets, quarterly updates are insufficient.

- 📋 Build scenario sensitivity into investment appraisals — the gap between January and March 2026 buyer enquiry data shows how quickly conditions can shift.

- 🏠 Advise clients on condition surveys proactively — rising markets can mask structural risks that only a thorough inspection reveals.

For Buyers and Sellers:

- ✅ Commission a professional valuation before committing — whether buying in a rising Northern market or negotiating in a softer Southern one, independent evidence is invaluable.

- ✅ Consider the rental market context if purchasing as an investment — constrained landlord supply and rising rents support yield assumptions in many urban areas.

- ✅ Do not anchor to 2024 or 2025 price points — the market has moved, and the direction differs significantly by region.

Whether purchasing in North West London, North London, or further afield, the most important step any buyer or investor can take in 2026 is to work with a qualified chartered surveyor who understands the regional nuances the RICS data is signalling — and can translate that intelligence into a valuation that reflects reality, not wishful thinking.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Valuation Strategies Amid January 2026 Rics Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Valuation Strategies For The 2026 Uk Housing Recovery Regional Price Divergence And Surveyor Tactics – https://nottinghillsurveyors.com/blog/valuation-strategies-for-the-2026-uk-housing-recovery-regional-price-divergence-and-surveyor-tactics

[5] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf