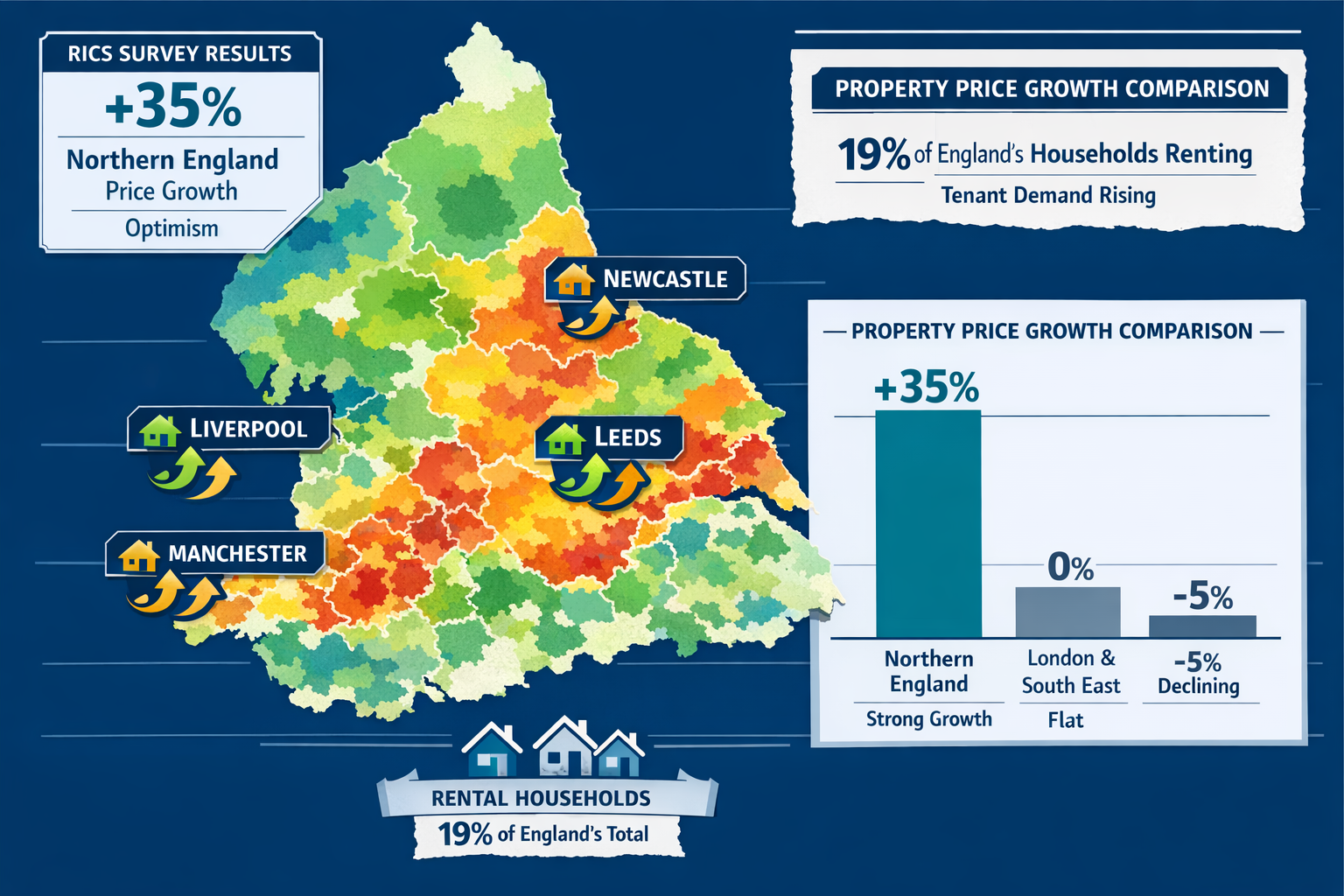

The Northern England property market is experiencing a remarkable transformation in 2026, with price momentum surging while southern regions struggle with affordability pressures and market stagnation. For institutional investors eyeing the buy-to-let sector, this regional divergence presents an unprecedented opportunity—but only for those armed with precise, professional Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand.

As respondents in the North West and North of England report house prices on an upward trajectory, contrasting sharply with pessimistic outlooks in London and the South East[1], institutional landlords must leverage sophisticated valuation strategies to capitalize on this growth while navigating the complexities of sustained tenant demand and evolving market dynamics.

Key Takeaways

✅ Northern regions lead the 2026 recovery: The North West and North of England show upward price momentum while southern markets remain flat or declining, creating prime opportunities for institutional buy-to-let investors[1]

✅ Tenant demand remains robust: With 4.7 million people in the private rented sector (19% of English households) and landlord exits creating supply constraints, rental demand continues to strengthen across Northern England[3]

✅ Professional valuations are essential: Accurate RICS-compliant valuation surveys enable institutional investors to assess portfolio potential, calculate rental yields, and make data-driven acquisition decisions in divergent regional markets

✅ Property type strategy matters: Two-bedroom city centre properties, one-bedroom units for single-person households, and HMOs each offer distinct advantages requiring tailored valuation approaches[3]

✅ Long-term optimism prevails: A net balance of +35% of market participants anticipate increased sales activity over the next 12 months, signaling recovering confidence for strategic investors[1]

Understanding the 2026 Northern England Property Market Landscape

Regional Price Divergence Creates Strategic Opportunities

The 2026 UK housing market has entered a period of pronounced regional divergence, with Northern England emerging as the clear winner in terms of price growth and investment potential. According to the latest RICS UK Residential Market Survey from January 2026, respondents in the North West and North of England report house prices on a distinctly upward trajectory[1]. This stands in stark contrast to more pessimistic outlooks dominating London, the South West, the South East, and East Anglia.

This geographical split represents more than just statistical variation—it signals a fundamental rebalancing of the UK property market. For decades, southern regions commanded premium valuations driven by employment concentration, infrastructure investment, and international capital flows. However, affordability pressures, changing work patterns, and government levelling-up initiatives have shifted the calculus for both owner-occupiers and investors.

| Region | Price Trend 2026 | Investor Sentiment | Key Driver |

|---|---|---|---|

| North West England | ⬆️ Upward | Optimistic | Affordability + Employment Growth |

| North of England | ⬆️ Upward | Positive | Regeneration + Tenant Demand |

| London | ➡️ Flat/Declining | Pessimistic | Affordability Crisis |

| South East | ➡️ Flat/Declining | Cautious | High Entry Costs |

| South West | ➡️ Flat/Declining | Mixed | Saturation Concerns |

Market Confidence Indicators Point to Sustained Growth

Beyond immediate price movements, forward-looking confidence metrics suggest the Northern England advantage will persist throughout 2026 and beyond. A remarkable net balance of +35% of survey participants anticipate an increase in sales activity over the next 12 months[1], representing a significant vote of confidence in market recovery.

However, institutional investors must distinguish between short-term volatility and long-term trends. The 3-month sales expectations series recorded a more modest net balance of +4% in January 2026, down from +22% in December 2025[1]. This flattening of short-term expectations indicates market participants are exercising caution about immediate conditions while maintaining optimism for the year ahead.

For buy-to-let investors, this dynamic creates an advantageous entry window. Properties can be acquired before the anticipated sales surge drives prices higher, while rental demand remains consistently strong regardless of short-term sales fluctuations.

The Private Rented Sector's Expanding Role

The private rented sector has undergone dramatic expansion over the past two decades, fundamentally altering the UK housing landscape. As of 2024-2025, the sector accounts for 4.7 million people, representing 19% of all households in England[3]—roughly double the 9-11% recorded during the 1980s-1990s.

This growth reflects structural changes in the UK economy and society:

- 🏠 Homeownership barriers: Deposit requirements and mortgage stress testing have made ownership increasingly difficult for younger households

- 💼 Employment flexibility: Modern careers require geographic mobility that favors renting over ownership

- 🎓 Extended education: Higher education participation delays household formation and ownership

- 👥 Demographic shifts: Changing household composition and delayed family formation support rental demand

"With stable house prices, competitive mortgage rates, and sustained rental demand, buy-to-let property investment continues to offer a strong source of income for investors in 2026."[3]

For institutional investors conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, understanding these structural drivers is essential. Unlike cyclical market fluctuations, these factors represent long-term tailwinds supporting rental demand regardless of short-term economic conditions.

Valuation Surveys for Institutional Buy-to-Let in Northern England: Essential Components and Methodologies

RICS Red Book Valuation Standards for Investment Properties

Professional valuation surveys form the cornerstone of successful institutional buy-to-let investment. Unlike residential purchase valuations, institutional portfolio assessments require comprehensive analysis aligned with RICS Red Book valuation standards, ensuring consistency, transparency, and regulatory compliance.

For Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, RICS-registered valuers must address several critical components:

1. Market Value Assessment

The valuer determines the estimated amount for which an asset should exchange on the valuation date between a willing buyer and willing seller in an arm's-length transaction. In Northern England's dynamic 2026 market, this requires analyzing recent comparable sales, adjusting for property-specific factors, and accounting for regional price momentum.

2. Investment Value Calculation

Beyond market value, institutional investors need investment value assessments—the value of an asset to a particular investor based on individual investment requirements. This incorporates rental yield expectations, portfolio diversification benefits, and strategic positioning within the investor's overall holdings.

3. Rental Income Potential Analysis

Accurate rental income projections drive buy-to-let investment decisions. Valuers must assess:

- Current market rents for comparable properties

- Tenant demand indicators in the specific location

- Void period expectations based on property type

- Rental growth forecasts aligned with regional economic trends

4. Capital Appreciation Forecasts

Given Northern England's upward price trajectory[1], capital appreciation represents a significant component of total return. Professional valuations incorporate regional price trend analysis, infrastructure development plans, and employment growth forecasts to project medium-term value appreciation.

Property-Specific Valuation Considerations

Different property types within institutional buy-to-let portfolios require tailored valuation approaches. The Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand must account for these variations:

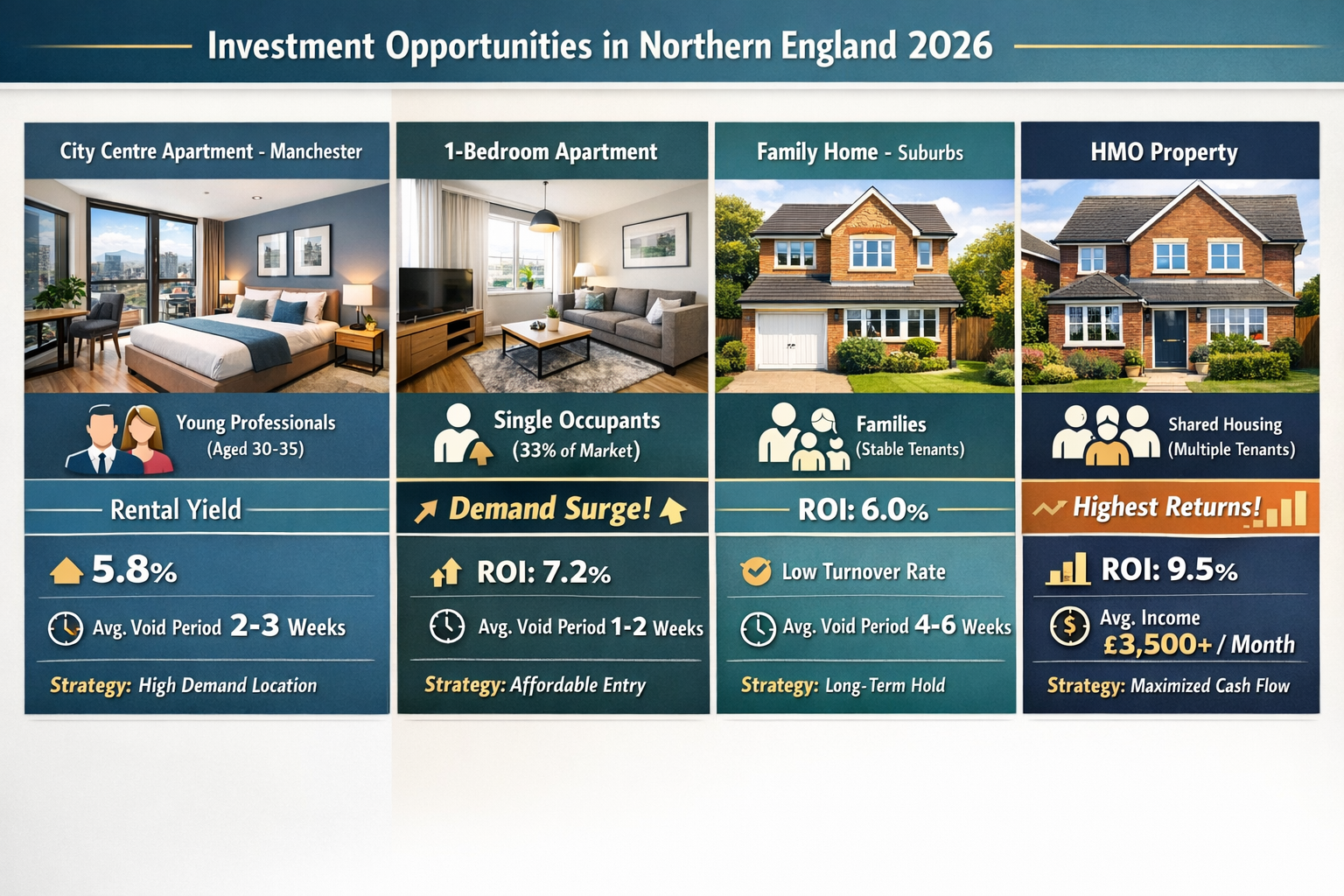

Two-Bedroom City Centre Properties

These properties are experiencing particularly strong tenant demand in 2026, especially from young professional tenants aged 30-35[3]. Valuation surveys must assess:

- Proximity to employment hubs and transport links

- Quality of fixtures and modern amenities

- Competition from new-build developments

- Rental premium potential versus suburban alternatives

One-Bedroom Properties for Single-Person Households

With single-person households rising to 33% of all households (up from approximately 28% six years prior)[3], one-bedroom properties represent a growth segment. Valuers should evaluate:

- Layout efficiency and space optimization

- Suitability for remote working (home office space)

- Building amenities and security features

- Neighborhood characteristics attracting single professionals

Three to Four-Bedroom Family Properties

Suburban and family-oriented areas offer lower tenant turnover, providing stability for long-term investment strategies[3]. However, void periods may extend longer than city centre properties. Valuation considerations include:

- School catchment area quality

- Garden and parking provision

- Condition of family-oriented features

- Local amenity access (parks, shops, healthcare)

Houses in Multiple Occupation (HMOs)

HMOs with three or more bedrooms demonstrate the strongest monthly returns of any property type[3], though they carry additional regulatory complexity. Specialized valuation surveys must address:

- Licensing compliance and regulatory costs

- Room configuration and tenant capacity

- Shared facility quality and maintenance requirements

- Local HMO market saturation levels

Incorporating Regional Economic Data

Professional Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand extend beyond individual property assessment to incorporate broader economic intelligence. Valuers must analyze:

📊 Employment Growth Indicators: Regional job creation, particularly in knowledge economy sectors, drives tenant demand and supports rental growth

📈 Infrastructure Investment: Transport improvements, regeneration projects, and public sector investment enhance location desirability and long-term value appreciation

🏗️ New Supply Pipeline: Understanding planned residential development helps forecast competition and rental market dynamics

💰 Affordability Metrics: The relationship between local earnings and property prices influences the owner-occupier versus renter split

Working with RICS registered valuers who understand Northern England's specific market dynamics ensures institutional investors receive actionable intelligence rather than generic property assessments.

Tenant Demand Dynamics Shaping Northern England Buy-to-Let Returns

Demographic Shifts Driving Rental Demand

The tenant demographic profile has undergone significant transformation, creating new opportunities for institutional buy-to-let investors who understand these evolving patterns. Research indicates that around half of tenants are now aged 35 or older, with the number of renters aged 45 and above continuing to rise[3].

This aging renter demographic carries important implications for Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand:

Longer Tenancy Periods

Older tenants typically seek stability and remain in properties longer than younger renters, reducing void periods and turnover costs. This stability enhances the predictability of rental income streams—a key consideration for institutional portfolio management.

Higher Quality Expectations

Mature tenants often have greater disposable income and prioritize property quality, modern amenities, and professional property management. Properties meeting these expectations command rental premiums and attract more reliable tenants.

Different Space Requirements

Unlike students or young professionals who may accept compact living spaces, older tenants frequently require:

- Dedicated home office space for remote working

- Storage for accumulated possessions

- Quality kitchen facilities for home cooking

- Outdoor space (balcony, garden, or terrace)

Household Composition and Property Type Alignment

The mean number of people per household has decreased significantly compared to pre-pandemic periods, with privately renting households averaging 2.3 people[3]. This trend toward smaller household sizes influences optimal property type selection for institutional portfolios.

Strategic Implications for Investors:

1️⃣ One and two-bedroom properties align with dominant household sizes and offer the broadest tenant appeal

2️⃣ Flexible layouts that accommodate couples, single parents with one child, or professional house-shares maximize marketability

3️⃣ Multi-functional spaces that serve as bedrooms, offices, or living areas appeal to evolving tenant needs

4️⃣ Efficient space utilization matters more than total square footage for smaller households

When conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, valuers must assess how well individual properties align with these household composition trends. Properties that match dominant tenant profiles command higher rents and experience shorter void periods.

Supply Constraints Amplifying Tenant Competition

A significant factor supporting strong rental demand in 2026 is the contraction of private landlord supply. Some landlords are slimming down their portfolios or exiting the market entirely[3], creating supply constraints that benefit remaining investors.

Drivers of Landlord Exits:

💷 Tax changes: Reduced mortgage interest tax relief and capital gains tax considerations have eroded returns for individual landlords

📋 Regulatory burden: Energy efficiency requirements, licensing schemes, and tenant protection legislation have increased compliance costs

⚖️ Professional management demands: Modern tenants expect responsive, professional management that many individual landlords struggle to provide

🏦 Financing challenges: Stricter buy-to-let mortgage criteria and higher interest rate sensitivity affect smaller investors disproportionately

For institutional investors with professional management infrastructure, compliance expertise, and access to competitive financing, these challenges represent competitive advantages rather than obstacles. The exit of individual landlords creates acquisition opportunities and reduces competition for tenants.

Geographic Hotspots Within Northern England

While Northern England as a whole demonstrates positive momentum, micro-market analysis reveals specific locations offering exceptional buy-to-let potential:

Manchester and Greater Manchester

- Strong employment growth in technology, media, and professional services

- Significant infrastructure investment including transport improvements

- Large student population transitioning to young professional renters

- Regeneration projects enhancing specific neighborhoods

Leeds and West Yorkshire

- Expanding financial and legal services sector

- Competitive pricing versus southern alternatives

- Strong transport connectivity (rail, motorway access)

- Growing cultural and lifestyle amenities attracting young professionals

Liverpool and Merseyside

- Ongoing waterfront and city center regeneration

- Affordable entry points for institutional portfolios

- Tourism and hospitality sector supporting employment

- Creative industries cluster development

Newcastle and the North East

- Exceptional affordability relative to earnings

- University presence supporting rental demand

- Healthcare and education sector employment stability

- Emerging technology sector growth

Professional chartered surveyors conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should provide location-specific analysis within these broader regional markets, identifying neighborhoods positioned for above-average rental growth and capital appreciation.

Strategic Portfolio Construction for Institutional Buy-to-Let Investors

Diversification Across Property Types and Locations

Sophisticated institutional investors construct diversified buy-to-let portfolios that balance risk and return across multiple dimensions. When commissioning Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, portfolio-level analysis should address:

Property Type Diversification

Combining different property types creates resilience against market-specific downturns:

- City centre apartments: High rental yields, shorter void periods, but potentially higher turnover

- Suburban family homes: Lower turnover, stable long-term tenants, but longer void periods when they occur

- HMOs: Highest monthly returns but greater management intensity and regulatory complexity

- One-bedroom units: Strong demand from growing single-person household segment

Geographic Diversification

Spreading investments across multiple Northern England cities and towns reduces exposure to location-specific economic shocks:

- Major cities (Manchester, Leeds, Liverpool) offer liquidity and scale

- Secondary cities provide value opportunities with growth potential

- Commuter towns balance affordability with connectivity

- Regeneration areas offer capital appreciation upside

Tenant Demographic Diversification

Properties appealing to different tenant segments smooth income volatility:

- Young professionals (high mobility but strong demand)

- Established professionals (stability and quality expectations)

- Families (long tenancies but specific property requirements)

- Mature renters (reliability and quality focus)

Yield Optimization Through Strategic Property Selection

Rental yield remains the primary return driver for buy-to-let investment, calculated as annual rental income divided by property value. In Northern England's 2026 market, yields vary significantly by property type and location.

Typical Yield Ranges (Northern England 2026):

| Property Type | Gross Yield Range | Net Yield Range | Tenant Profile |

|---|---|---|---|

| One-bed city centre | 5.5% – 7.0% | 4.0% – 5.5% | Young professionals, singles |

| Two-bed city centre | 5.0% – 6.5% | 3.8% – 5.2% | Couples, professional shares |

| Three-bed suburban | 4.5% – 6.0% | 3.5% – 4.8% | Families, established professionals |

| Four-bed HMO | 7.0% – 10.0% | 5.0% – 7.5% | Multiple professionals, students |

Professional valuers conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should provide both gross and net yield calculations, accounting for:

- Property management fees (typically 10-15% of rental income)

- Maintenance and repair provisions

- Void period allowances

- Insurance costs

- Regulatory compliance expenses

Capital Appreciation Potential in Growth Corridors

While rental yield provides immediate income, capital appreciation significantly enhances total return over investment holding periods. Northern England's upward price trajectory in 2026[1] positions institutional investors to benefit from both income and capital growth.

Key Appreciation Drivers to Assess:

🚄 Transport Infrastructure: HS2 connectivity, local rail improvements, and motorway access enhance location desirability and support long-term value growth

🏢 Employment Centers: Proximity to expanding business districts, technology clusters, and professional services hubs drives sustained demand

🎓 Education Institutions: Universities and colleges create stable tenant demand while attracting graduate retention and employment growth

🌳 Regeneration Projects: Public and private sector investment in neighborhood improvement, green space development, and cultural amenities

When commissioning valuations, institutional investors should request specific analysis of these appreciation drivers and their likely impact on medium-term (5-10 year) property values. This forward-looking perspective distinguishes strategic portfolio construction from opportunistic property acquisition.

Risk Management and Due Diligence

Comprehensive due diligence protects institutional investors from value-destroying acquisitions. Beyond standard building surveys, buy-to-let specific assessments should include:

Structural and Condition Analysis

- Building survey identifying major defects and repair costs

- Energy Performance Certificate (EPC) rating and improvement costs

- Compliance with rental property minimum standards

- Anticipated capital expenditure over 10-year holding period

Legal and Regulatory Compliance

- Planning permission verification for any alterations

- HMO licensing requirements and compliance status

- Leasehold terms and service charge obligations (if applicable)

- Building safety compliance (fire regulations, electrical safety)

Tenancy and Income Verification

- Current tenancy agreements and tenant quality

- Rental income verification against market comparables

- Void period history and seasonal patterns

- Tenant turnover rates and retention statistics

Title and Ownership Clarity

- Clear title verification through solicitor searches

- Identification of any restrictive covenants

- Rights of way or access issues

- Boundary disputes or party wall matters

Working with experienced professionals who provide specific defect reports and comprehensive due diligence ensures institutional investors make informed acquisition decisions based on complete property intelligence.

Financing Strategies and Tax Considerations for Institutional Investors

Competitive Mortgage Rates Supporting Buy-to-Let Investment

The 2026 mortgage market offers competitive rates that enhance buy-to-let investment returns[3]. Institutional investors typically access more favorable financing terms than individual landlords due to:

Portfolio Lending Advantages

- Lower interest rates for larger loan volumes

- Flexible loan-to-value ratios based on portfolio strength

- Cross-collateralization options reducing individual property risk

- Relationship pricing from established lender partnerships

Professional Borrower Status

- Streamlined application processes for experienced investors

- Reduced documentation requirements for established portfolios

- Access to specialist commercial lenders

- Bespoke financing structures aligned with investment strategy

When conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, accurate property valuations directly impact available financing. Lenders typically advance 60-75% loan-to-value for buy-to-let properties, with the valuation determining maximum borrowing capacity.

Tax-Efficient Ownership Structures

Institutional buy-to-let investors utilize tax-efficient ownership structures to maximize after-tax returns. Unlike individual landlords subject to income tax on rental profits, corporate and fund structures offer advantages:

Limited Company Ownership

- Corporation tax on rental profits (currently lower than higher-rate income tax)

- Full mortgage interest deductibility (unlike individual landlords)

- Capital gains tax efficiency on property disposals

- Flexibility for profit retention and reinvestment

Real Estate Investment Trust (REIT) Structures

- Tax-exempt status on rental income and capital gains (if qualifying conditions met)

- Requirement to distribute 90% of rental profits to investors

- Access to institutional capital markets

- Enhanced liquidity through share trading

Pension Fund Investment

- Tax-free rental income and capital gains within pension wrapper

- Inheritance tax advantages

- Long-term investment horizon alignment

- Regulatory compliance requirements

Professional tax advisors should work alongside valuation surveyors to ensure acquisition decisions account for tax implications and ownership structure optimization.

Valuation Requirements for Tax and Accounting Purposes

Beyond acquisition decisions, institutional investors require periodic valuations for various tax and accounting purposes:

Annual Accounting Valuations

- Fair value assessment for financial statement reporting

- Investment property revaluation for balance sheet accuracy

- Compliance with accounting standards (IFRS, UK GAAP)

- Audit documentation and verification

Capital Gains Tax Valuations

- Baseline valuations for future disposal calculations

- Capital gains tax valuation for portfolio restructuring

- Relief and exemption optimization

- Indexation allowance calculations (where applicable)

Stamp Duty Land Tax (SDLT) Considerations

- Accurate purchase price allocation for SDLT calculation

- Multiple dwelling relief optimization

- Non-residential property classification (HMOs, commercial elements)

- SDLT planning for portfolio acquisitions

Insurance Valuations

- Insurance reinstatement valuation for adequate coverage

- Protection against underinsurance penalties

- Premium optimization through accurate valuations

- Periodic revaluation to account for construction cost inflation

Technology and Data Analytics in Modern Valuation Surveys

PropTech Integration Enhancing Valuation Accuracy

Modern Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand leverage advanced technology to enhance accuracy and efficiency:

Automated Valuation Models (AVMs)

- Machine learning algorithms analyzing thousands of comparable sales

- Real-time market data integration

- Rapid preliminary valuations for portfolio screening

- Desktop valuation support for experienced surveyors

Geographic Information Systems (GIS)

- Location analysis incorporating transport links, amenities, and employment centers

- Heat mapping of rental demand and price trends

- Neighborhood characteristic assessment

- Regeneration project tracking and impact analysis

Drone and Digital Survey Technology

- Drone roof surveys for inaccessible areas

- Digital measurement tools improving accuracy

- Photographic documentation and condition recording

- 3D modeling for complex properties

Big Data and Market Intelligence

- Rental listing analysis tracking demand patterns

- Tenant demographic profiling from multiple data sources

- Employment and economic data integration

- Predictive analytics for rental growth forecasting

Market Data Sources for Northern England Analysis

Accurate Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand rely on comprehensive market data from authoritative sources:

📊 RICS Residential Market Surveys: Monthly sentiment indicators and regional price trend analysis[1]

🏠 Land Registry Price Paid Data: Transaction evidence for comparable sales analysis

📈 ONS Housing Statistics: Household composition, tenure patterns, and demographic trends

💼 Regional Economic Data: Employment statistics, wage growth, and sector composition

🏢 Local Authority Planning Data: Development pipelines, regeneration projects, and infrastructure investment

Professional valuers synthesize these diverse data sources to provide institutional investors with comprehensive market intelligence supporting acquisition decisions.

Predictive Analytics and Forward-Looking Valuations

Traditional valuations focus on current market value based on historical comparable sales. However, institutional buy-to-let investors require forward-looking analysis that incorporates predictive elements:

Rental Growth Forecasting

- Econometric modeling of rental price trends

- Correlation analysis between employment growth and rental demand

- Supply-demand imbalance quantification

- Scenario analysis for different economic conditions

Capital Appreciation Projections

- Regional price trend extrapolation with confidence intervals

- Infrastructure impact modeling on property values

- Regeneration project value uplift estimation

- Comparative regional performance analysis

Risk-Adjusted Return Calculations

- Probability-weighted return scenarios

- Volatility assessment based on historical patterns

- Stress testing for adverse market conditions

- Portfolio-level risk aggregation and correlation

These advanced analytical techniques transform Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand from static property assessments into dynamic investment decision tools.

Regulatory Compliance and Professional Standards

RICS Professional Standards and Red Book Compliance

Institutional investors must ensure valuation surveys comply with RICS Valuation – Global Standards (commonly known as the Red Book). These standards ensure consistency, transparency, and professional rigor in property valuations.

Key Red Book Requirements:

✅ Valuer Competence: Qualified RICS members with relevant experience and geographic knowledge

✅ Independence and Objectivity: Absence of conflicts of interest affecting professional judgment

✅ Terms of Engagement: Clear scope definition, basis of value, and reporting requirements

✅ Valuation Approaches: Appropriate methodology selection (comparable sales, income capitalization, residual value)

✅ Assumptions and Special Assumptions: Explicit statement of any assumptions affecting valuation

✅ Reporting Standards: Comprehensive documentation of analysis, methodology, and conclusions

For Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand, Red Book compliance provides institutional investors with confidence that valuations meet professional standards and withstand regulatory scrutiny.

Energy Efficiency and Sustainability Considerations

Energy Performance Certificate (EPC) ratings have become critical valuation factors as regulatory minimum standards tighten. Since April 2020, rental properties must achieve a minimum EPC rating of E, with future regulations likely to require higher standards.

Valuation Impact of Energy Efficiency:

🟢 EPC Rating A-B: Premium valuations reflecting lower tenant energy costs, regulatory future-proofing, and ESG alignment

🟡 EPC Rating C-D: Standard valuations with consideration of improvement potential

🟠 EPC Rating E: Valuation discounts reflecting improvement requirements and regulatory risk

🔴 EPC Rating F-G: Significant valuation discounts or deemed unlettable until improvements completed

Institutional investors focused on Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should request specific analysis of:

- Current EPC rating and certification validity

- Cost estimates for rating improvements

- Potential rental premium from energy efficiency upgrades

- Regulatory compliance timeline and risk assessment

Building Safety and Compliance Verification

Following the Building Safety Act and heightened awareness of building defects, comprehensive safety compliance verification forms an essential component of buy-to-let valuations:

Fire Safety Assessment

- Fire door compliance and certification

- Smoke alarm and carbon monoxide detector provision

- Emergency exit accessibility and signage

- Fire risk assessment completion (especially for HMOs)

Electrical Safety Compliance

- Five-year electrical installation condition report (EICR)

- Remedial work requirements and costs

- Portable appliance testing (PAT) for furnished properties

- Consumer unit and wiring condition assessment

Gas Safety Verification

- Annual gas safety certificate (CP12)

- Boiler service history and efficiency

- Gas appliance condition and safety

- Carbon monoxide detection provision

Structural Integrity

- Subsidence risk assessment

- Structural movement monitoring

- Foundation condition evaluation

- Major defect identification and cost estimation

Professional surveyors conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should coordinate with specialist engineers where structural concerns exist, ensuring institutional investors receive comprehensive risk assessment.

Case Studies: Successful Institutional Buy-to-Let Investments in Northern England

Case Study 1: Manchester City Centre Two-Bedroom Portfolio

Investment Profile:

- Location: Manchester city centre, proximity to Spinningfields business district

- Property Type: 15 two-bedroom apartments in converted Victorian warehouse

- Purchase Price: £2.8 million (£187,000 average per unit)

- Purchase Date: Q1 2025

Valuation Survey Findings:

Professional Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand identified:

- Strong comparable sales evidence supporting £185,000-£190,000 valuations

- Rental income potential of £1,200-£1,300 per month per unit

- Gross yield projection of 7.7-8.4%

- Capital appreciation forecast of 4-6% annually based on regional trends[1]

Investment Performance (12 months):

- Average rental achieved: £1,275 per month

- Occupancy rate: 97% (average 11 days void between tenancies)

- Gross yield realized: 8.2%

- Capital appreciation: 5.5% based on Q1 2026 revaluation

- Total return: 13.7%

Key Success Factors:

✅ Accurate valuation identifying value opportunity

✅ Strong tenant demand from young professionals

✅ Professional property management minimizing voids

✅ Regional price momentum exceeding initial forecasts

Case Study 2: Leeds Suburban Family Home Portfolio

Investment Profile:

- Location: Horsforth and Roundhay, family-oriented Leeds suburbs

- Property Type: 8 three-bedroom semi-detached houses

- Purchase Price: £1.92 million (£240,000 average per unit)

- Purchase Date: Q2 2025

Valuation Survey Findings:

Comprehensive valuations assessed:

- Comparable sales analysis supporting £235,000-£245,000 range

- Rental income potential of £1,100-£1,200 per month

- Gross yield projection of 5.5-6.1%

- Lower tenant turnover expectations (average 2-3 year tenancies)

- Capital appreciation forecast of 3-5% annually

Investment Performance (12 months):

- Average rental achieved: £1,150 per month

- Occupancy rate: 100% (no tenancy terminations in first year)

- Gross yield realized: 5.8%

- Capital appreciation: 4.2%

- Total return: 10.0%

Key Success Factors:

✅ Family tenant stability eliminating void periods

✅ School catchment area quality supporting rental demand

✅ Lower management intensity than city centre properties

✅ Steady capital appreciation in established neighborhoods

Case Study 3: Liverpool HMO Investment

Investment Profile:

- Location: Wavertree, Liverpool (proximity to University of Liverpool)

- Property Type: 4 five-bedroom HMOs

- Purchase Price: £720,000 (£180,000 average per unit)

- Purchase Date: Q3 2025

Valuation Survey Findings:

Specialist HMO valuations identified:

- Market value range of £175,000-£185,000 per property

- Rental income potential of £2,200-£2,400 per month (5 rooms at £440-£480)

- Gross yield projection of 14.7-16.0%

- Higher management and compliance costs

- Regulatory compliance verification essential

Investment Performance (12 months):

- Average rental achieved: £2,300 per month

- Occupancy rate: 92% (individual room voids averaging 15 days)

- Gross yield realized: 14.4%

- Management costs: 15% of rental income (higher than standard)

- Net yield: 10.9%

- Capital appreciation: 3.8%

- Total return: 14.7%

Key Success Factors:

✅ Exceptional rental yields offsetting higher management costs

✅ Strong student and young professional demand

✅ Professional HMO management expertise

✅ Regulatory compliance ensuring sustainable operation

Future Outlook: Northern England Buy-to-Let Market 2026-2030

Sustained Demand Drivers Supporting Long-Term Growth

The structural factors supporting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand extend well beyond 2026, creating a favorable long-term investment environment:

Demographic Trends

- Continued growth in single-person households requiring one-bedroom properties

- Aging renter population seeking quality, professionally managed accommodation

- Delayed homeownership among younger cohorts maintaining rental demand

- Immigration and population mobility supporting flexible housing needs

Economic Rebalancing

- Government levelling-up initiatives directing investment to Northern regions

- Technology sector growth in Manchester, Leeds, and Newcastle

- Professional services expansion outside London

- Infrastructure investment enhancing regional connectivity

Housing Supply Constraints

- Planning system limitations restricting new development

- Construction cost inflation limiting speculative building

- Individual landlord exits reducing private rented sector supply

- Social housing shortages increasing private sector reliance

Affordability Advantages

- Northern England property prices remaining significantly below southern regions

- Wage growth supporting rental affordability

- Mortgage affordability challenges maintaining rental demand

- Cost of living advantages attracting population migration

Emerging Opportunities and Market Evolution

Forward-thinking institutional investors conducting Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should monitor emerging opportunities:

🏢 Build-to-Rent Developments: Purpose-built rental properties offering institutional-grade assets with professional management infrastructure

🌱 Sustainable Housing Premium: Energy-efficient properties commanding rental premiums and attracting environmentally conscious tenants

💻 Remote Work-Optimized Properties: Homes with dedicated office space, high-speed connectivity, and flexible layouts

🏘️ Co-Living Concepts: Modern HMO alternatives offering community amenities and professional management

🔄 Regeneration Area Opportunities: Early investment in improving neighborhoods positioned for value appreciation

Risk Factors and Mitigation Strategies

While the outlook remains positive, institutional investors must address potential risks:

Regulatory Risk

- Threat: Increasing compliance requirements and tenant protection legislation

- Mitigation: Professional management infrastructure, compliance expertise, and regulatory monitoring

Interest Rate Risk

- Threat: Rising mortgage costs reducing net yields

- Mitigation: Fixed-rate financing, conservative leverage ratios, and yield buffers

Economic Downturn Risk

- Threat: Recession reducing tenant affordability and increasing arrears

- Mitigation: Tenant diversification, employment sector analysis, and cash reserves

Supply Increase Risk

- Threat: New development increasing competition and suppressing rents

- Mitigation: Location selection favoring supply-constrained markets and differentiated property offerings

Property Market Correction Risk

- Threat: House price declines reducing capital values

- Mitigation: Long-term investment horizon, income focus over capital gains, and regional diversification

Professional Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand should incorporate risk assessment and scenario analysis, enabling investors to make informed decisions accounting for potential adverse developments.

Conclusion: Actionable Steps for Institutional Investors

Northern England's buy-to-let market presents compelling opportunities for institutional investors in 2026, driven by upward price momentum, sustained tenant demand, and structural market advantages. However, success requires professional expertise, comprehensive due diligence, and strategic portfolio construction.

Key Action Steps for Institutional Investors

1. Commission Professional RICS Valuations

Engage RICS registered valuers with Northern England market expertise to conduct comprehensive Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand. Ensure valuations address:

- Current market value and investment value

- Rental income potential and yield analysis

- Capital appreciation forecasts

- Risk assessment and due diligence findings

- Portfolio-level diversification recommendations

2. Develop Clear Investment Criteria

Define specific investment parameters including:

- Target locations within Northern England

- Preferred property types and tenant demographics

- Minimum yield requirements and return expectations

- Maximum individual property and portfolio exposure limits

- Hold period and exit strategy planning

3. Build Professional Management Infrastructure

Establish or partner with professional property management providers offering:

- Tenant sourcing and vetting processes

- Responsive maintenance and repair services

- Regulatory compliance monitoring

- Financial reporting and performance tracking

- Tenant retention and relationship management

4. Optimize Financing and Ownership Structures

Work with specialist advisors to:

- Secure competitive buy-to-let mortgage financing

- Implement tax-efficient ownership structures

- Maintain appropriate leverage ratios

- Plan for periodic refinancing opportunities

- Coordinate financing with acquisition strategy

5. Monitor Market Trends and Adjust Strategy

Establish ongoing market intelligence processes:

- Review RICS market surveys and regional data[1]

- Track employment and economic indicators

- Monitor regulatory developments

- Assess competitive dynamics and supply pipelines

- Conduct periodic portfolio revaluations

6. Prioritize Regulatory Compliance and Risk Management

Implement robust compliance frameworks addressing:

- Energy efficiency standards and improvement programs

- Building safety and fire safety requirements

- Electrical and gas safety certification

- HMO licensing and management standards

- Tenant protection and deposit scheme compliance

The Strategic Advantage of Professional Valuations

In Northern England's dynamic 2026 property market, Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand represent far more than regulatory requirements or financing prerequisites. They provide the strategic intelligence enabling institutional investors to:

✅ Identify value opportunities before market consensus

✅ Avoid overpriced acquisitions that destroy returns

✅ Optimize portfolio construction across property types and locations

✅ Forecast rental income and capital appreciation with confidence

✅ Assess and mitigate investment risks systematically

✅ Demonstrate professional diligence to stakeholders and lenders

As the Northern England property market continues its upward trajectory, with a net balance of +35% of participants anticipating increased sales activity[1] and sustained tenant demand supporting rental income[3], institutional investors who leverage professional valuation expertise will be best positioned to capitalize on this exceptional opportunity.

The convergence of regional price growth, tenant demand strength, landlord supply constraints, and favorable financing conditions creates a compelling investment case. However, success requires moving beyond generic market enthusiasm to property-specific, data-driven analysis that professional Valuation Surveys for Institutional Buy-to-Let in Northern England: Capitalizing on 2026 Price Growth and Tenant Demand uniquely provide.

For institutional investors ready to capitalize on Northern England's buy-to-let opportunity, the time to act is now—armed with professional valuations, strategic clarity, and operational excellence.

References

[1] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[2] Valuing Northern England Properties In 2026 Surveyor Tactics For Outpacing Southern Affordability Pressures – https://nottinghillsurveyors.com/blog/valuing-northern-england-properties-in-2026-surveyor-tactics-for-outpacing-southern-affordability-pressures

[3] 2026 Property Investors Guide – https://www.buyassociationgroup.com/en-us/news/2026size-property-investors/

[4] Valuation Strategies For The 2026 UK Housing Recovery Regional Price Divergence And Surveyor Tactics – https://nottinghillsurveyors.com/blog/valuation-strategies-for-the-2026-uk-housing-recovery-regional-price-divergence-and-surveyor-tactics