The UK property market is experiencing a dramatic regional divergence in 2026, with Northern England emerging as the unexpected champion of price growth while Southern markets stagnate. For property professionals, investors, and surveyors, understanding the Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities has become essential to capitalizing on this shifting landscape. The latest RICS data reveals that the North West and Northern regions are showing upward price trajectories that contrast sharply with negative sentiment across London, the South East, and South West.[2]

This regional transformation demands a fundamental rethinking of traditional valuation approaches. Chartered surveyors must now deploy region-specific methodologies that account for the unique dynamics driving Northern England's growth while Southern markets face affordability pressures and market stagnation. The opportunity is clear: properties in Manchester, Leeds, Liverpool, and surrounding areas are experiencing momentum that hasn't been seen in years, with 4-7% growth projections creating significant value capture opportunities for those who understand the nuances.[1]

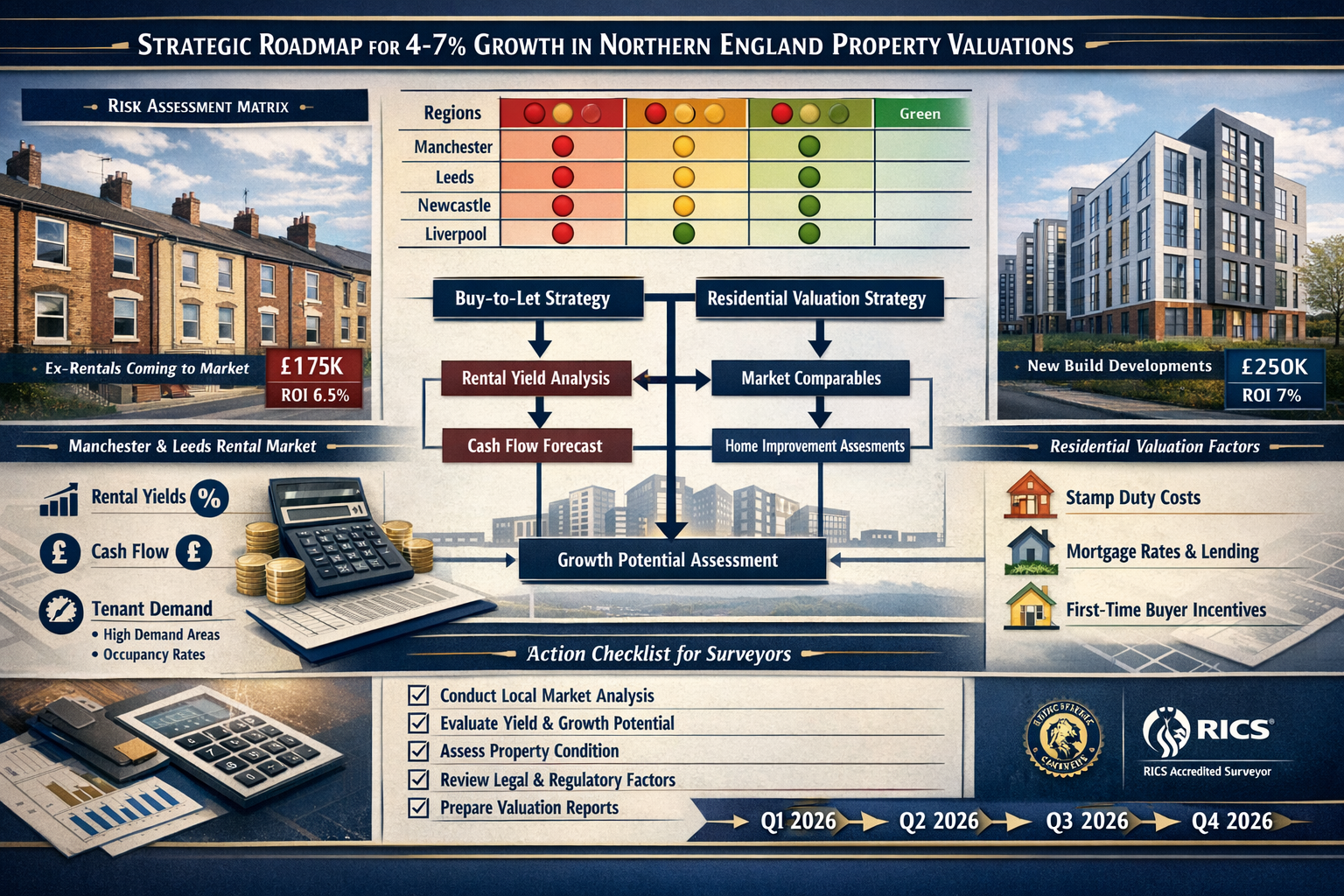

Key Takeaways

✅ Northern England is outperforming Southern markets with the North West and Northern regions showing upward price trajectories while London and the South East face stagnation, creating a 4-7% growth opportunity for properly valued properties.[2]

✅ RICS Red Book methodologies require regional adjustments including comparable sales analysis specific to Northern markets, risk premium recalibrations, and rental yield assessments that reflect local tenant demand dynamics.[1]

✅ Ex-rental properties and realistic seller pricing are expanding market opportunities in Northern England, with increased stock availability in lower and middle price brackets making properties more accessible to buyers.[2]

✅ Timing and market momentum matter significantly as early 2026 data shows the Essex and Northern markets picking up drastically in January, requiring surveyors to adjust their valuation dates and comparable timeframes accordingly.[2]

✅ Buy-to-let valuations need specialized approaches in Northern England markets where rental yields remain stronger than Southern equivalents, demanding different capitalization rates and income-based valuation methods.[3]

Understanding the 2026 Northern England Property Surge

The Regional Divergence Phenomenon

The UK property market has entered an unprecedented period of regional polarization. While traditionally, London and the South East have led property price appreciation, 2026 has flipped this dynamic entirely. The North West and Northern England regions are now experiencing the strongest upward momentum in residential property prices across the entire United Kingdom.[2]

This divergence stems from several interconnected factors:

Affordability Constraints in the South 🏘️

Southern markets, particularly London and the South East, have reached price points that exceed the purchasing power of average buyers, even with improved mortgage availability. The median property price in London now requires income multiples that are simply unattainable for most households, creating demand suppression.

Northern Value Proposition

In contrast, Northern England offers properties at price points that remain accessible to first-time buyers, young families, and investors seeking rental yields. A three-bedroom Victorian terrace in Manchester or Leeds might cost £250,000-350,000, compared to £600,000+ for equivalent properties in outer London boroughs.[1]

Economic Investment and Infrastructure

Government infrastructure projects, including Northern Powerhouse initiatives and HS2 developments (despite modifications), continue to drive economic confidence in Northern cities. Major employers are establishing or expanding Northern operations, creating employment growth that supports housing demand.

Rental Market Dynamics

The Northern rental market remains robust, with tenant demand consistently outstripping supply in major cities. This creates a compelling investment case for buy-to-let purchasers, who can achieve gross rental yields of 5-7% in Northern markets compared to 3-4% in London.[3]

RICS Survey Data: What the Numbers Reveal

The January 2026 RICS UK Residential Market Survey provides compelling evidence of this regional shift. Key findings include:

| Region | Price Sentiment | Trend Direction | Growth Estimate |

|---|---|---|---|

| North West | Positive (+15) | ⬆️ Upward | 4-7% |

| Northern England | Positive (+12) | ⬆️ Upward | 4-6% |

| Scotland | Positive (+8) | ⬆️ Upward | 3-5% |

| London | Negative (-22) | ⬇️ Downward | 0-2% |

| South East | Negative (-18) | ⬇️ Downward | 0-1% |

| South West | Negative (-14) | ⬇️ Downward | 1-2% |

The survey suggests that market conditions may be "starting to turn a corner" with several activity-related measures tentatively signaling a potential turning point, though further confirmation is needed in subsequent months.[2]

Surveyor commentary from the RICS report emphasizes critical themes:

"Accurate market pricing is essential to create purchaser interest and facilitate sales momentum. Properties priced realistically are achieving sales within 8-12 weeks, while overpriced properties languish."[2]

This insight is particularly relevant for Northern England, where seller expectations are becoming more realistic after years of hoping for London-style appreciation that never materialized. The result is a healthier market with proper price discovery.

The Ex-Rental Property Opportunity

One of the most significant developments in Northern England's 2026 market is the influx of ex-rental properties coming to market. East Lancashire surveyors report that more landlords are exiting the rental sector due to regulatory changes, taxation adjustments, and energy efficiency requirements, making their properties available for purchase.[2]

This trend creates multiple opportunities:

Expanded Inventory in Affordable Brackets

Ex-rental properties typically fall into the £150,000-300,000 range in Northern markets, precisely the price point where first-time buyer demand is strongest. This inventory expansion helps address the chronic shortage of affordable housing.

Builder Part-Exchange Deals

Developers in Northern regions are increasingly offering part-exchange arrangements, particularly for new-build developments in suburbs and satellite towns. These deals facilitate chain-free transactions that complete more quickly.[2]

Value-Add Investment Opportunities

Ex-rental properties often require cosmetic updating or minor improvements, creating opportunities for investors to add value through strategic refurbishment before re-letting or reselling at higher valuations.

For surveyors conducting RICS valuations, these ex-rental properties require careful assessment of deferred maintenance, tenant wear-and-tear, and potential improvement costs when determining market value.

RICS Valuation Methodologies for Northern England Markets

Red Book Compliance and Regional Adaptations

The RICS Valuation – Global Standards (commonly known as the Red Book) provides the framework that all chartered surveyors must follow when conducting formal property valuations. However, the Red Book's principles require thoughtful adaptation to capture the specific dynamics of Northern England's 2026 market surge.

The Five Pillars of RICS Valuation

- Act with integrity – Maintain objectivity despite market enthusiasm

- Always provide a high standard of service – Deploy region-specific expertise

- Act in a way that promotes trust – Use transparent comparable evidence

- Treat others with respect – Consider all stakeholder perspectives

- Take responsibility – Stand behind valuation conclusions with data

When applying these principles to Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities, surveyors must recognize that standard London-centric approaches may not capture Northern market nuances.[1]

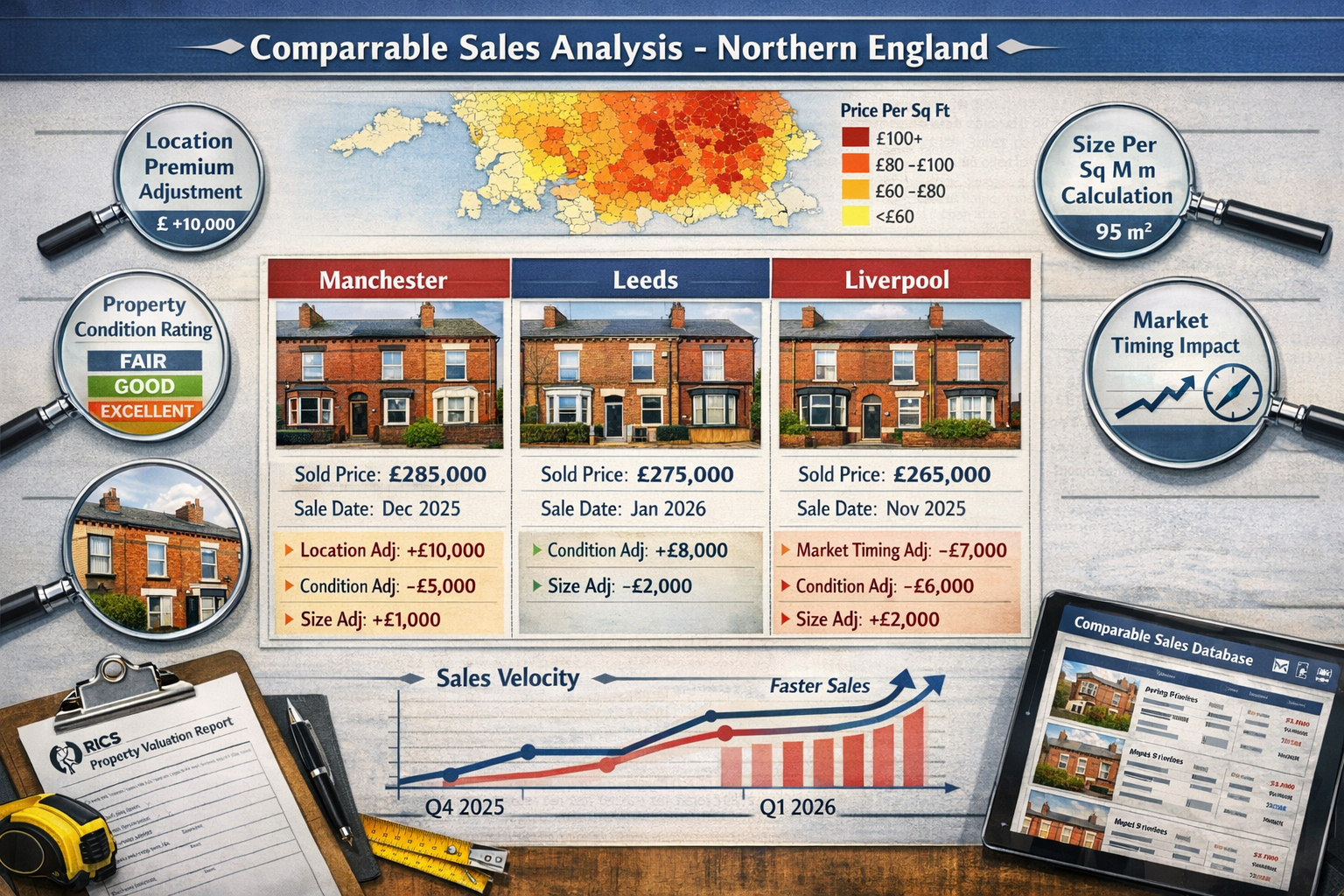

Comparable Sales Analysis: Northern England Specifics

Comparable sales analysis forms the foundation of residential property valuation. However, the methodology requires careful calibration for Northern England's current market conditions.

Geographic Boundaries for Comparables 🗺️

In Northern cities, micro-market variations can be dramatic. A property in Manchester's Northern Quarter commands significantly different values than one in Salford, despite being only two miles apart. Surveyors should:

- Limit comparable searches to 0.5-mile radius in urban centers

- Expand to 1-2 mile radius in suburban areas with consistent characteristics

- Consider postcode districts carefully, as LS6 (Headingley, Leeds) differs markedly from LS9 (Harehills)

Temporal Considerations

Given the rapid momentum in Northern England markets during early 2026, the recency of comparable sales becomes critical. The RICS guidelines suggest:

- Primary comparables: Sales completed within the last 3 months

- Secondary comparables: Sales from 3-6 months ago with appropriate time adjustments

- Historical comparables: Only use sales older than 6 months if adjusted for market movement

With 4-7% annual growth, a property sold six months ago may need a 2-3.5% upward adjustment to reflect current market conditions.[2]

Adjustment Factors Specific to Northern Markets

When analyzing comparable sales, surveyors must apply adjustments for differences between the subject property and comparables:

| Adjustment Factor | Typical Range | Northern England Considerations |

|---|---|---|

| Location Premium | ±5-15% | Proximity to city centers, universities, transport hubs |

| Property Condition | ±10-20% | Victorian/Edwardian properties vary widely in modernization |

| Size Variations | £100-150/sq ft | Price per square foot more consistent than Southern markets |

| Parking/Garden | ±3-8% | Higher value in suburban areas; less critical in city centers |

| Period Features | ±5-10% | Original features (fireplaces, cornicing) add premium |

| Energy Efficiency | ±3-7% | Increasingly important with EPC regulations |

Understanding valuation factors that influence property prices helps surveyors make appropriate adjustments that reflect market realities rather than theoretical calculations.

Income Capitalization for Buy-to-Let Properties

Northern England's strong rental market makes income-based valuation approaches particularly relevant for buy-to-let properties. The income capitalization method estimates property value based on the income it generates.

The Basic Formula:

Property Value = Net Annual Income ÷ Capitalization Rate

For Northern England buy-to-let properties in 2026:

Net Annual Income Calculation

- Gross annual rent: £12,000-18,000 (typical 2-bed terrace)

- Less: Void periods (5-8%): £600-1,440

- Less: Management fees (10-12%): £1,200-2,160

- Less: Maintenance reserve (8-10%): £960-1,800

- Net Annual Income: £9,240-12,600

Capitalization Rate Selection

Northern England buy-to-let properties typically warrant capitalization rates of 5.5-7%, depending on:

- Location quality: Prime city center locations = 5.5-6%

- Property condition: Fully refurbished = 6-6.5%

- Tenant profile: Professional tenants = 6-6.5%

- Management intensity: Hands-off investments = 6.5-7%

Example Valuation:

A well-maintained 2-bedroom terrace in Leeds generating £14,400 gross annual rent:

- Net income after all costs: £10,800

- Appropriate cap rate: 6.25%

- Indicated value: £172,800

This income approach should be reconciled with comparable sales to ensure the valuation reflects both investment fundamentals and market realities.[3]

Risk Adjustments for Regional Divergence

The dramatic divergence between Northern and Southern markets in 2026 introduces valuation risk that surveyors must address transparently.

Market Momentum Risk ⚠️

When markets are rising rapidly (4-7% annually), there's risk of:

- Overheating: Prices rising faster than fundamentals support

- Sentiment-driven pricing: Buyers paying premiums based on FOMO (fear of missing out)

- Correction potential: Rapid rises can lead to subsequent corrections

Prudent surveyors should:

- Apply conservative comparable adjustments (use lower end of ranges)

- Include market conditions commentary in valuation reports

- Consider 90-day marketing periods rather than assuming immediate sales

- Highlight sensitivity analysis showing value ranges under different scenarios

Liquidity Considerations

Northern England properties generally take longer to sell than London properties, despite current momentum. The RICS survey notes that "sales are taking significantly longer to complete" even in active markets.[2]

This liquidity difference should influence:

- Mortgage valuation approaches: Lenders may apply conservative adjustments

- Forced sale scenarios: Divorce, probate, or matrimonial valuations may need 10-15% discounts

- Investment valuations: Factor in potential 3-6 month marketing periods

Economic Concentration Risk

Some Northern cities have economies concentrated in specific sectors (manufacturing, education, healthcare). Surveyors should consider:

- Employment diversity: Cities with varied employment bases carry less risk

- Major employer dependence: Towns reliant on single large employers face higher risk

- Infrastructure delivery: Valuations dependent on planned transport improvements need contingency considerations

Implementing Valuation Tactics for Northern England Price Surge 2026

Strategic Approaches for Different Property Types

The Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities vary significantly depending on property type and intended use.

Victorian and Edwardian Terraced Houses 🏘️

These properties form the backbone of Northern England's housing stock and are experiencing strong demand in 2026.

Valuation Tactics:

- Emphasize modernization quality: Properties with updated kitchens, bathrooms, and heating systems command 15-25% premiums over unmodernized equivalents

- Assess structural integrity carefully: Many Victorian properties have had extensions, loft conversions, or cellar conversions that may or may not have proper building control approval

- Consider period feature retention: Original features (fireplaces, cornicing, stained glass) add value in gentrifying areas

- Evaluate energy efficiency: EPC ratings increasingly affect marketability and value, with C-rated properties commanding premiums

Comparable Selection:

Focus on properties within the same terrace type (through-terrace, end-terrace, back-to-back) as layout differences significantly affect value.

New-Build Developments

Northern cities are experiencing significant new-build activity, particularly in city centers and regeneration zones.

Valuation Tactics:

- Apply new-build premium cautiously: New-builds typically carry 10-15% premiums over equivalent second-hand properties, but this premium can erode quickly

- Consider Help to Buy implications: Properties purchased with Help to Buy schemes may have equity loan complications affecting future valuations

- Assess build quality and developer reputation: Snagging issues and developer financial stability affect long-term value

- Factor in service charges: Leasehold new-builds with high service charges may have constrained appreciation potential

Market Evidence:

New-build comparables should be separated from second-hand comparables in analysis, as they represent different market segments with distinct buyer profiles.

Buy-to-Let Investment Properties

With Northern England offering superior rental yields compared to Southern markets, buy-to-let properties require specialized valuation approaches.

Valuation Tactics:

- Dual methodology: Use both comparable sales and income capitalization, reconciling the two approaches

- Tenant situation assessment: Properties with sitting tenants may have different values than vacant possession properties

- Licensing requirements: Check whether properties require HMO licenses or selective licensing, affecting costs and values

- Rental market positioning: Properties in student areas, professional areas, or family areas have different risk-return profiles

Growth Capture Strategies:

To capture the 4-7% growth opportunity, surveyors should:

- Identify emerging areas: Neighborhoods experiencing gentrification or infrastructure improvements

- Assess rental demand indicators: University enrollment, major employer announcements, transport improvements

- Calculate yield compression potential: As areas improve, cap rates may compress from 7% to 6%, creating capital appreciation beyond rental growth

Timing Considerations and Market Momentum

The timing of valuations has become critically important in Northern England's dynamic 2026 market.

Valuation Date Significance 📅

RICS standards require that valuations are accurate as of a specific valuation date. In rapidly moving markets:

- Retrospective valuations: May need to reference market conditions 3-6 months ago, requiring careful comparable selection from that period (see retrospective valuation guidance)

- Current valuations: Should use the most recent comparables available, ideally from the last 30-60 days

- Prospective valuations: For development projects or forward funding, must include assumptions about future market conditions

Market Momentum Indicators

Surveyors should monitor several indicators to gauge whether Northern England's momentum is sustainable:

- Sales velocity: Time from listing to offer acceptance

- Offer-to-asking price ratios: Percentage of asking price achieved

- Mortgage approval rates: Indicating buyer financing ability

- New instruction volumes: Supply coming to market

- Viewer-to-offer conversion: Buyer commitment levels

The RICS survey notes that the Essex market "picked up drastically in January 2026 and is gathering momentum, with sellers' expectations becoming more realistic."[2] This suggests that realistic pricing is driving activity, not speculative overpricing.

Documentation and Reporting Standards

Professional valuation reports for Northern England properties should include specific elements that address the regional dynamics:

Market Context Section 📊

Include a dedicated section addressing:

- Regional market conditions (North vs. South divergence)

- Local market trends (city-specific dynamics)

- Economic indicators (employment, infrastructure, demographics)

- Comparable market evidence (sales volumes, price trends)

Comparable Sales Schedule

Present comparables in a structured format:

| Address | Sale Date | Price | Size (sq ft) | £/sq ft | Adjustments | Adjusted Price |

|---|---|---|---|---|---|---|

| 123 Oak Street | Jan 2026 | £245,000 | 1,100 | £223 | +5% location | £257,250 |

| 456 Elm Road | Dec 2025 | £238,000 | 1,050 | £227 | +2% time, -3% condition | £240,380 |

| 789 Ash Avenue | Feb 2026 | £252,000 | 1,150 | £219 | -4% size | £242,080 |

Assumptions and Limitations

Clearly state:

- Market conditions assumptions (continuation of current trends, potential risks)

- Inspection limitations (areas not accessed, assumed conditions)

- Information reliance (seller disclosures, third-party reports)

- Special assumptions (vacant possession, completion of works)

Sensitivity Analysis

For investment properties or high-value assets, include sensitivity tables showing how value changes with different assumptions:

Example: Buy-to-Let Sensitivity Analysis

| Scenario | Rental Income | Cap Rate | Indicated Value |

|---|---|---|---|

| Base Case | £11,400 | 6.25% | £182,400 |

| Optimistic | £12,600 | 5.75% | £219,130 |

| Conservative | £10,200 | 6.75% | £151,111 |

This transparency helps clients understand the range of potential outcomes and the factors driving value conclusions.

Advanced Tactics for Capturing Growth Opportunities

Identifying Value-Add Opportunities

Sophisticated investors and developers use value-add strategies to capture more than the baseline 4-7% market growth in Northern England.

Refurbishment and Modernization 🔨

Victorian and Edwardian properties often present significant value-add potential:

Kitchen and Bathroom Updates

- Investment: £8,000-15,000

- Value increase: £15,000-25,000

- ROI: 60-100%

Energy Efficiency Improvements

- Investment: £5,000-12,000 (insulation, boiler, double glazing)

- Value increase: £8,000-18,000

- Additional benefit: Improved EPC rating, lower running costs, higher rental appeal

Space Optimization

- Loft conversions: £25,000-40,000 investment, £35,000-60,000 value increase

- Basement conversions: £30,000-50,000 investment, £40,000-70,000 value increase

- Extensions: £20,000-35,000 investment, £30,000-50,000 value increase

When valuing properties with development potential, surveyors should:

- Provide existing use value (current condition)

- Estimate improved value (post-development)

- Consider development costs and planning probability

- Apply appropriate risk adjustments (planning risk, cost overrun risk)

Conversion Opportunities

Northern England's commercial property market includes buildings suitable for residential conversion:

- Former offices: City center offices converting to apartments

- Industrial buildings: Warehouse and mill conversions in Manchester, Leeds, Sheffield

- Retail spaces: Ground floor retail with upper floor residential conversion potential

Valuation approaches for conversions require:

- Residual valuation methodology: Gross development value minus costs minus profit

- Planning assessment: Likelihood of obtaining change of use permission

- Market demand analysis: Buyer appetite for converted properties vs. traditional housing

Leveraging Market Intelligence

Data Sources for Northern England Valuations 📈

Professional surveyors should utilize multiple data sources:

Primary Sources:

- Land Registry Price Paid Data: Actual transaction prices (free, comprehensive)

- EPC Register: Energy performance data for comparables

- Planning portals: Development activity in the area

- Rental listing sites: Current rental market evidence (Rightmove, Zoopla)

Professional Sources:

- RICS Market Surveys: Monthly sentiment and trend data

- Hometrack/TwentyCi: Professional comparable sales databases

- Local estate agents: Market intelligence, buyer profiles, emerging trends

- Mortgage lenders: Lending criteria, valuation policies, risk assessments

Economic Indicators:

- ONS Regional Economic Data: Employment, wages, demographics

- Transport infrastructure announcements: HS2, Northern Powerhouse Rail, local schemes

- University enrollment data: Student housing demand indicators

- Major employer announcements: Job creation, relocations, expansions

Synthesizing Intelligence into Valuations

The most effective Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities involve synthesizing multiple data streams:

- Quantitative foundation: Comparable sales data, price indices, rental yields

- Qualitative overlay: Market sentiment, buyer profiles, emerging trends

- Forward-looking adjustments: Infrastructure plans, economic forecasts, demographic shifts

- Risk calibration: Downside scenarios, sensitivity testing, assumption validation

This multi-layered approach produces valuations that are both defensible (grounded in comparable evidence) and insightful (capturing market dynamics that pure historical data might miss).

Specialized Valuation Scenarios

Capital Gains Tax Valuations

Northern England property owners who purchased years ago may face significant capital gains tax liabilities when selling in 2026's appreciating market.

Valuation Tactics:

- Establish baseline value: Retrospective valuation at acquisition date or April 2015 (rebasing date)

- Document improvements: Separate capital improvements from maintenance, as improvements increase base cost

- Consider timing: Spreading sales across tax years may optimize tax position

- Apply principal private residence relief: Careful calculation of exempt periods

Shared Ownership Valuations

Northern England's affordable housing sector includes significant shared ownership properties.

Valuation Tactics:

- Full market value assessment: Value the property as if sold with vacant possession

- Staircasing calculations: Value the percentage share being purchased

- Rent review implications: Consider the rent charged on the retained share

- Lease terms: Assess remaining lease length and terms

Right to Buy Valuations

Social housing tenants in Northern England exercising Right to Buy need accurate valuations.

Valuation Tactics:

- Open market value: Assess value assuming vacant possession

- Discount application: Apply statutory discounts (up to £87,200 in 2026)

- Comparable selection: Use private sales of similar ex-council properties

- Condition assessment: Many Right to Buy properties require modernization

Regional Sub-Market Analysis

Manchester and Greater Manchester

Market Characteristics:

Manchester represents Northern England's most dynamic property market in 2026, with strong fundamentals supporting the 4-7% growth projection.

Key Growth Drivers:

- Economic diversification: Finance, technology, creative industries, education

- Infrastructure investment: Metrolink expansions, city center developments

- Population growth: Young professional in-migration from London and internationally

- Rental demand: Strong student and professional rental markets

Valuation Considerations:

- Micro-market variations: Northern Quarter, Ancoats, Spinningfields command premiums

- New-build supply: Significant apartment development requires careful comparable selection

- Leasehold ground rents: Many new apartments have concerning ground rent terms

- Service charge inflation: High-rise apartments facing significant service charge increases

Comparable Sales Evidence (Q1 2026):

- City center 1-bed apartments: £180,000-240,000

- City center 2-bed apartments: £240,000-350,000

- Suburban 2-bed terraces: £180,000-250,000

- Suburban 3-bed semi-detached: £250,000-350,000

Leeds and West Yorkshire

Market Characteristics:

Leeds combines strong professional employment with more affordable housing than Manchester, creating compelling value propositions.

Key Growth Drivers:

- Financial and professional services: Major employers including banks, law firms, accountancies

- Education sector: Multiple universities driving student accommodation demand

- Transport connectivity: Rail connections to London, Manchester, and Scotland

- Regeneration projects: South Bank, Aire Park, and other major developments

Valuation Considerations:

- Student area dynamics: LS2, LS6 areas have different characteristics than family areas

- Victorian housing stock: Significant terrace housing requiring condition assessment

- Parking premiums: Properties with parking command notable premiums

- Commuter belt growth: Surrounding towns (Harrogate, Wetherby, Ilkley) showing strength

Comparable Sales Evidence (Q1 2026):

- City center apartments: £160,000-280,000

- Headingley 2-bed terraces: £220,000-280,000

- Chapel Allerton 3-bed semi-detached: £280,000-380,000

- Roundhay 4-bed detached: £400,000-600,000

Liverpool and Merseyside

Market Characteristics:

Liverpool offers the most affordable entry points in Northern England's major cities while experiencing significant regeneration momentum.

Key Growth Drivers:

- Tourism and culture: UNESCO World Heritage status, cultural attractions

- Regeneration projects: Baltic Triangle, Lime Street, waterfront developments

- Education expansion: University growth driving student housing demand

- Transport improvements: Liverpool2 port expansion, connectivity enhancements

Valuation Considerations:

- Regeneration area premiums: Properties in regeneration zones showing accelerated growth

- Terraced housing dominance: Extensive Victorian terrace stock

- Rental yield strength: Some of the highest yields in Northern England (6-8%)

- Affordability advantage: Lowest price points among major Northern cities

Comparable Sales Evidence (Q1 2026):

- City center apartments: £140,000-220,000

- Georgian Quarter 2-bed terraces: £180,000-240,000

- Sefton Park 3-bed semi-detached: £240,000-320,000

- Crosby 4-bed detached: £350,000-500,000

Emerging Markets: Sheffield, Newcastle, Preston

Sheffield:

- Strengths: University demand, advanced manufacturing, green space

- Growth rate: 3-5% projected for 2026

- Price points: £150,000-280,000 for typical family homes

- Valuation focus: Student areas vs. professional areas require different approaches

Newcastle:

- Strengths: Regional employment hub, culture, affordability

- Growth rate: 4-6% projected for 2026

- Price points: £160,000-300,000 for typical family homes

- Valuation focus: Quayside regeneration creating value uplift

Preston:

- Strengths: Affordability, commuter access to Manchester, university

- Growth rate: 5-7% projected for 2026

- Price points: £130,000-220,000 for typical family homes

- Valuation focus: Commuter demand driving suburban growth

Risk Management and Professional Standards

Avoiding Common Valuation Errors

Over-reliance on Automated Valuation Models (AVMs) ⚠️

In rapidly changing markets like Northern England in 2026, AVMs often lag reality:

Problems with AVMs:

- Historical data bias: Based on past transactions, missing current momentum

- Algorithm limitations: Cannot assess property condition, improvements, or local nuances

- Regional calibration: Often calibrated for Southern markets, not Northern dynamics

Best Practice:

Use AVMs as cross-checks rather than primary valuation tools. Always conduct physical inspections and apply professional judgment.

Insufficient Comparable Adjustments

Failing to properly adjust comparables for differences leads to inaccurate valuations:

Common Errors:

- Ignoring condition differences: A modernized property vs. original condition property

- Overlooking location nuances: Same postcode but different street quality

- Missing temporal adjustments: Using 6-month-old comparables without time adjustment

- Size adjustment errors: Applying linear adjustments when per-square-foot values vary

Best Practice:

Document every adjustment with clear reasoning. When uncertain about adjustment quantum, provide a range of values rather than false precision.

Inadequate Market Context

Valuations that ignore broader market dynamics risk being quickly outdated:

Context Requirements:

- Regional trends: North vs. South divergence

- Local supply/demand: New instructions, sales volumes, time on market

- Economic factors: Employment, wages, mortgage availability

- Regulatory changes: Stamp duty, energy efficiency requirements, rental regulations

Best Practice:

Include a comprehensive market context section in every valuation report, citing sources like RICS surveys, Land Registry data, and local market intelligence.

Professional Indemnity and Liability Considerations

Valuation Liability Exposure 📋

Chartered surveyors conducting valuations in Northern England's dynamic 2026 market face potential liability if valuations prove inaccurate:

Common Liability Scenarios:

- Over-valuation: Lender suffers loss if borrower defaults and property sells for less than valuation

- Under-valuation: Seller claims loss of sale proceeds due to conservative valuation

- Negligent methodology: Failure to follow RICS standards or use appropriate comparables

- Scope limitations: Failing to identify defects or issues affecting value

Risk Mitigation Strategies:

- Comprehensive inspections: Never rely solely on desktop valuations for formal RICS reports

- Clear assumptions and limitations: Document what was and wasn't inspected

- Conservative approach in rising markets: Better to slightly under-value than over-value

- Robust comparable evidence: Maintain detailed files with comparable analysis

- Professional indemnity insurance: Ensure adequate coverage for valuation work

Regulatory Compliance

RICS members must comply with multiple regulatory frameworks:

- RICS Valuation – Global Standards (Red Book): Mandatory for all formal valuations

- Money Laundering Regulations: Client identification and verification

- Data Protection (GDPR): Proper handling of client and property data

- Conflicts of interest: Disclosure and management of any conflicts

Best Practice:

Maintain a compliance checklist for every valuation engagement, ensuring all regulatory requirements are met before issuing reports.

Technology and Innovation in Valuation

Digital Tools Enhancing Valuation Accuracy

Comparable Sales Databases 💻

Professional-grade databases provide comprehensive transaction data:

- TwentyCi/Hometrack: Extensive UK sales data with filtering and analysis tools

- Land Registry: Free access to Price Paid data

- EIG/Landmark: Environmental and planning data integration

- CoStar: Commercial property data (relevant for mixed-use valuations)

Valuation Software

Specialized software streamlines the valuation process:

- Argus Enterprise: Investment property valuation and cash flow modeling

- RICS Valuation Management System: Workflow and compliance management

- Spreadsheet templates: Custom-built models for specific property types

Geographic Information Systems (GIS)

GIS technology enables sophisticated location analysis:

- Heat mapping: Visualize price variations across neighborhoods

- Proximity analysis: Measure distance to transport, schools, amenities

- Demographic overlays: Understand buyer profiles in different areas

- Development tracking: Monitor planning applications and completions

Remote Valuation Considerations

The COVID-19 pandemic accelerated adoption of remote valuation techniques, which remain relevant in 2026:

Desktop Valuations

Conducted without physical inspection, relying on:

- Photographs: Provided by owners, agents, or previous inspections

- Floor plans: EPC data, estate agent materials

- Third-party reports: Previous surveys, building control certificates

- Street view imagery: Google Street View, aerial photography

Limitations and Risks:

- Cannot verify condition: Hidden defects, structural issues, damp

- Limited liability: Lenders may not accept for mortgage purposes

- RICS restrictions: Must clearly state assumptions and limitations

Best Practice:

Desktop valuations should be clearly labeled as such, with explicit assumptions about property condition. They're appropriate for low-risk scenarios (remortgages of recently surveyed properties) but not for purchase valuations or high-value properties.

Hybrid Approaches

Combining remote and physical elements:

- External inspection only: Assess external condition, location, comparable evidence

- Video inspection: Client conducts video walkthrough under surveyor guidance

- Drone surveys: External condition assessment, roof inspection

These hybrid approaches offer middle ground between full inspections and pure desktop valuations, appropriate for specific scenarios like insurance reinstatement valuations or preliminary assessments.

Conclusion: Implementing Effective Valuation Tactics for Northern England Price Surge 2026

The Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities represent a fundamental shift in how property professionals approach regional UK markets. The clear divergence between Northern England's upward momentum and Southern stagnation demands region-specific methodologies that go beyond traditional London-centric approaches.

Key Implementation Steps

For Chartered Surveyors:

- Recalibrate comparable databases to emphasize recent Northern England transactions over historical or Southern comparables

- Adjust risk premiums to reflect the improving fundamentals in Northern markets rather than applying outdated regional discounts

- Incorporate market momentum indicators including sales velocity, offer-to-asking ratios, and new instruction volumes

- Deploy dual methodologies for investment properties, reconciling comparable sales with income capitalization approaches

- Document regional context comprehensively in every valuation report, citing RICS survey data and local market intelligence

For Property Investors:

- Target emerging neighborhoods in Manchester, Leeds, Liverpool, and secondary cities where infrastructure investment is driving value

- Focus on value-add opportunities including ex-rental properties requiring modernization and properties with development potential

- Emphasize rental yield strength in Northern markets where 5-7% gross yields remain achievable compared to 3-4% in London

- Commission professional RICS valuations rather than relying on estate agent estimates or automated models

- Consider timing strategically as early 2026 momentum suggests optimal entry points before prices fully reflect fundamentals

For Homebuyers and Sellers:

- Price realistically based on recent comparable evidence rather than aspirational pricing from stagnant Southern markets

- Understand micro-market variations as values can vary 20-30% between neighborhoods in the same city

- Invest in property presentation as condition differences significantly affect values in competitive markets

- Obtain professional valuations for significant decisions including capital gains tax planning, divorce settlements, or estate planning

- Monitor market indicators including the monthly RICS surveys to understand whether momentum is accelerating or moderating

The Broader Context

Northern England's 2026 price surge reflects more than temporary market fluctuations. It represents a structural rebalancing of UK property markets driven by:

- Affordability constraints in Southern markets reaching breaking points

- Economic investment in Northern infrastructure and employment

- Demographic shifts with young professionals seeking value and quality of life

- Rental market dynamics favoring higher-yielding Northern investments

- Regulatory changes affecting buy-to-let economics differently across regions

These structural factors suggest that the 4-7% growth opportunity in Northern England may be sustainable rather than a brief anomaly, though prudent professionals will continue monitoring for signs of overheating or correction.

Professional Development

Surveyors seeking to excel in Northern England valuations should invest in:

- Regional market expertise: Regular visits to Northern cities, relationship building with local agents and professionals

- Continuing professional development: RICS courses on regional markets, investment valuation, and market analysis

- Technology adoption: Professional databases, GIS tools, and valuation software

- Network building: Connections with Northern England surveyors, agents, developers, and investors

- Specialization: Developing expertise in specific property types (Victorian terraces, new-build apartments, buy-to-let portfolios)

The chartered surveyors who thrive in 2026 and beyond will be those who combine technical RICS methodology with deep regional market understanding and forward-looking analysis of economic and demographic trends.

Final Thoughts

The Valuation Tactics for Northern England Price Surge 2026: RICS Methods to Capture 4-7% Growth Opportunities outlined in this guide provide a comprehensive framework for professional property valuation in a dynamic regional market. By applying rigorous RICS standards while adapting to Northern England's specific characteristics, surveyors can deliver valuations that are both technically defensible and commercially insightful.

The opportunity is clear: Northern England's property markets are experiencing momentum not seen in years, creating value capture opportunities for those who understand the nuances. Whether you're a chartered surveyor conducting formal valuations, an investor seeking returns, or a homeowner making property decisions, the tactics outlined here provide a roadmap for navigating this evolving landscape.

As the RICS January 2026 survey suggests, market conditions may be "starting to turn a corner."[2] Those who position themselves correctly—with accurate valuations, realistic pricing, and strategic timing—will be best placed to benefit from Northern England's continued growth trajectory.

For professional valuation services that understand these regional dynamics and apply RICS methodologies appropriately, consider consulting with experienced chartered surveyors who specialize in Northern England markets and can provide the expertise needed to capture these growth opportunities effectively.

References

[1] Valuing Northern England Properties In 2026 Surveyor Tactics For Outpacing Southern Affordability Pressures – https://nottinghillsurveyors.com/blog/valuing-northern-england-properties-in-2026-surveyor-tactics-for-outpacing-southern-affordability-pressures

[2] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[3] Valuation Strategies For The 2026 Uk Housing Recovery Regional Price Divergence And Surveyor Tactics – https://nottinghillsurveyors.com/blog/valuation-strategies-for-the-2026-uk-housing-recovery-regional-price-divergence-and-surveyor-tactics