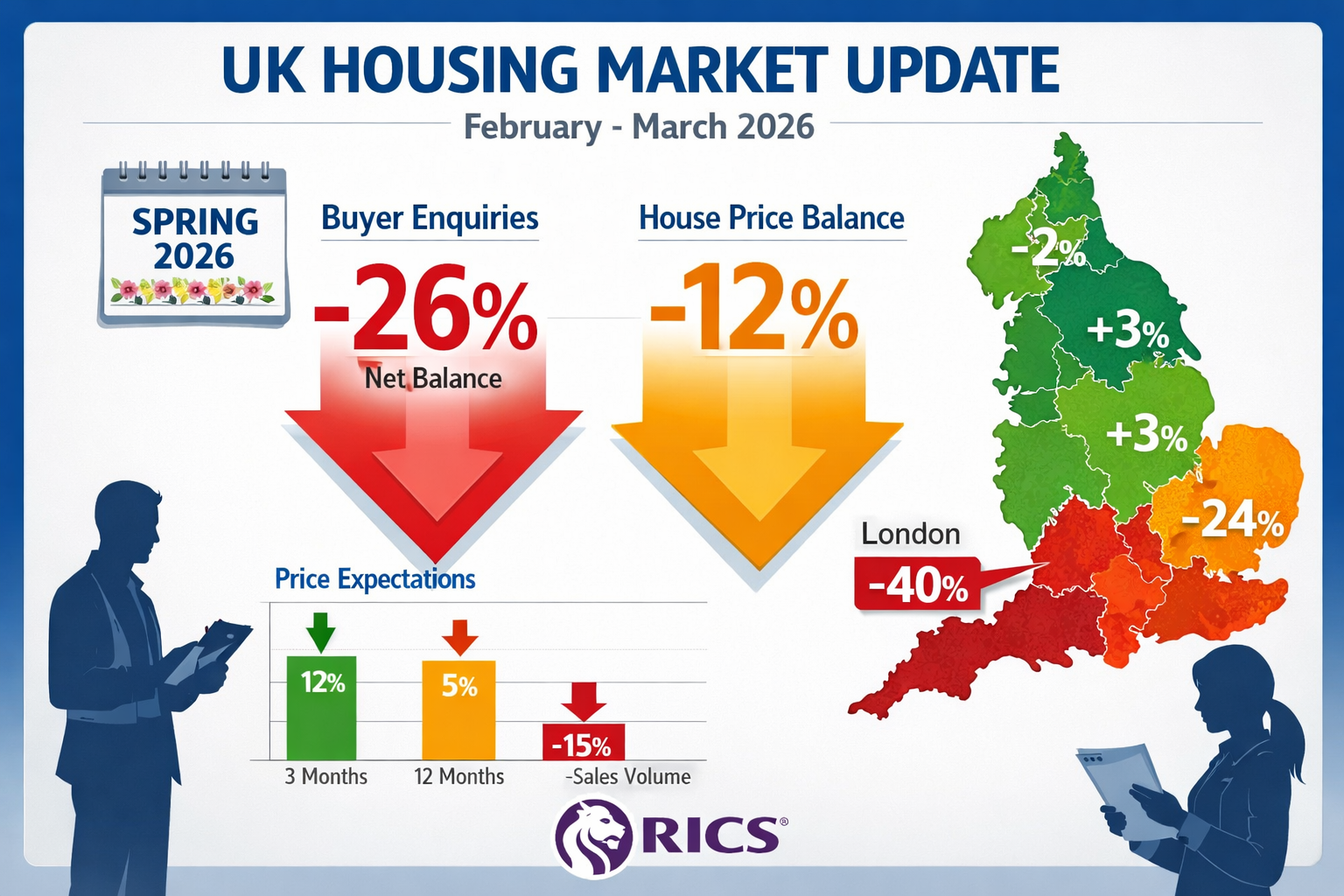

Buyer enquiries across the UK property market plummeted to a net balance of -26% in February 2026, down from -15% just one month earlier—marking one of the sharpest monthly deteriorations in buyer confidence recorded by the Royal Institution of Chartered Surveyors (RICS) in recent years [2]. This dramatic shift in sentiment, driven by escalating geopolitical tensions and economic uncertainty, has thrust building surveyors into an unprecedented challenge: how to accurately assess property values when traditional market indicators fluctuate wildly and buyer psychology shifts by the week.

Valuation Uncertainty in Spring 2026: How Building Surveyors Navigate Geopolitical Risks and Buyer Sentiment Volatility has become the defining professional challenge for chartered surveyors working across residential and commercial property markets. As median list prices decline for the fifth consecutive month and mortgage rates climb in response to international conflicts, surveyors must recalibrate their methodologies to account for macro-level risks that extend far beyond local market comparables.

Key Takeaways

- Buyer enquiries fell to -26% net balance in February 2026, with London experiencing the steepest price pressure at -40%, requiring surveyors to adjust regional valuation approaches significantly [2]

- Median list prices declined 2.2% year-over-year to $415,450 in March 2026, marking five consecutive months of annual price declines and fundamentally shifting valuation baselines [1]

- Geopolitical tensions directly impact mortgage rates, with four consecutive weeks of rate increases in early April 2026 erasing prior declines and reducing buyer purchasing power [4]

- Time on market extended to 57 days in March 2026—four days longer than the previous year—indicating protracted valuation negotiations and increased uncertainty [1]

- Building surveyors are adapting methodologies by incorporating geopolitical risk premiums, sentiment volatility adjustments, and more conservative comparable selection criteria into their assessments

Understanding the Current Market Context for Property Valuations

The Spring 2026 property market presents building surveyors with a complex web of interconnected challenges that extend beyond traditional valuation considerations. Understanding this context is essential for accurate property assessments.

The Geopolitical Dimension

Recent military conflicts involving Iran and broader Middle Eastern tensions have triggered immediate repercussions across financial markets, directly affecting mortgage-backed securities and bond yields [4]. When geopolitical shocks occur, investors rapidly adjust their risk positions, widening spreads on mortgage-backed securities and pushing borrowing costs higher. For building surveyors, this creates a moving target for valuation assessments—the financing costs that underpin buyer purchasing power can shift substantially between initial instruction and final report delivery.

Mortgage rates climbed for four consecutive weeks as of early April 2026, directly reversing modest declines that had begun to materialize in late winter [4]. This volatility makes it challenging for surveyors to confidently project market values, particularly for properties at the upper end of price brackets where financing represents a larger proportion of the transaction.

Regional Disparities in Valuation Pressure

The impact of current market conditions varies dramatically by region. According to RICS data, the headline house price net balance stands at -12% nationally, but this masks significant regional variation [2]:

| Region | Price Net Balance | Valuation Implication |

|---|---|---|

| London | -40% | Severe downward pressure |

| South East | -24% | Moderate downward pressure |

| East Anglia | -26% | Moderate downward pressure |

| Northern Regions | Positive/Neutral | Greater resilience |

For chartered surveyors working across London and the South East, this means applying more conservative valuation approaches and carefully selecting comparable evidence from recent transactions rather than relying on older data points that may no longer reflect current market realities.

Inventory and Supply Dynamics

Active inventory increased 8.1% compared to March 2025, reaching 964,477 listings as of March 2026 [1]. This reversal of prior scarcity conditions fundamentally alters the supply-demand equation that underpins property valuations. Building surveyors must now account for:

- Increased buyer choice reducing urgency premiums

- Extended negotiation periods allowing for more price discovery

- Greater price sensitivity as buyers compare multiple options

- Reduced competition for individual properties

New listings surged 21.2% from February to March, exceeding the historical seasonal norm of 18% [1]. This suggests property owners are strategically timing market entry, potentially ahead of anticipated further deterioration—a factor surveyors should consider when assessing seller motivation and realistic pricing expectations.

Valuation Uncertainty in Spring 2026: Adapting Professional Methodologies

Building surveyors must fundamentally adapt their valuation methodologies to account for the unique challenges presented by Spring 2026 market conditions. Traditional approaches require enhancement with additional risk assessment layers.

Comparative Method Adjustments

The comparative method—comparing subject properties to recent sales of similar properties—remains the foundation of residential valuation work. However, current market volatility demands more sophisticated application:

Time-based adjustments have become critical. With median time on market extending to 57 days in March 2026 (up from 53 days a year prior) [1], surveyors must carefully weight the recency of comparable evidence. A sale completed in December 2025 may reflect fundamentally different market conditions than one from March 2026.

Sentiment-adjusted comparables represent an emerging best practice. When selecting comparable evidence, surveyors should prioritize transactions where buyer motivation and market conditions closely mirror current circumstances. Properties sold under distressed conditions or during brief sentiment rebounds may not provide reliable valuation guidance.

Geographic granularity has increased in importance. Given the stark regional variations in price pressure, surveyors must narrow their comparable search radius and avoid cross-regional comparisons that might have been acceptable in more stable market periods.

Incorporating Geopolitical Risk Premiums

Professional valuation standards, including RICS Red Book requirements, emphasize the need to reflect all material factors affecting value. In Spring 2026, geopolitical risk represents such a material factor.

Building surveyors are developing frameworks to quantify geopolitical impact:

✅ Financing cost volatility adjustments – Recognizing that mortgage rate uncertainty affects buyer willingness to commit at specific price points

✅ Economic confidence discounts – Applying modest percentage adjustments (typically 2-5%) to reflect reduced buyer confidence during periods of international tension

✅ Liquidity risk premiums – Acknowledging that properties may take longer to sell and require greater price flexibility in uncertain environments

✅ Regional sensitivity factors – Applying differential adjustments based on local market resilience to macro shocks

These adjustments must be clearly documented and justified within valuation reports, providing clients with transparency about the assumptions underpinning assessed values.

Buyer Sentiment Analysis Integration

The dramatic swing in buyer enquiries from -15% to -26% net balance in just one month [2] demonstrates how rapidly sentiment can shift. Building surveyors now routinely incorporate sentiment indicators into their assessment process:

Leading indicators such as mortgage application volumes, viewing appointment trends, and offer-to-asking price ratios provide real-time insight into buyer psychology. Surveyors working with estate agents and mortgage brokers can access this intelligence to inform valuation judgments.

Sentiment-adjusted pricing strategies recognize that in negative sentiment environments, properties must be priced more competitively to attract serious interest. The data showing price reductions decreased to 16.2% of active listings (down from 17.4% a year ago) [1] suggests sellers are "pricing more accurately at the outset rather than testing the market and cutting later"—a trend surveyors should reinforce through conservative initial valuations.

Psychological price thresholds become more significant during uncertain periods. Buyers exhibit heightened sensitivity to pricing just below major psychological barriers (£500,000 vs. £525,000, for example), and surveyors should consider these dynamics when providing valuation guidance.

Enhanced Due Diligence for Valuation Factors

Beyond market conditions, surveyors must conduct more rigorous assessment of property-specific factors that might affect value during volatile periods:

When conducting a homebuyer report or building survey, particular attention should be paid to:

- Deferred maintenance issues that buyers may use as negotiation leverage in a buyer's market

- Energy efficiency ratings that affect running costs during periods of economic uncertainty

- Structural concerns that could delay transactions or reduce buyer confidence

- Lease terms and ground rent for leasehold properties, which receive greater scrutiny in cautious markets

For specialized valuation work including matrimonial valuations and capital gains tax assessments, current market volatility necessitates clear disclosure of valuation date significance and potential for material value changes over short timeframes.

Valuation Uncertainty in Spring 2026: Strategic Approaches for Different Property Sectors

Different property sectors respond uniquely to geopolitical uncertainty and buyer sentiment volatility, requiring tailored valuation approaches.

Residential Property Valuation Strategies

The residential sector shows the most direct correlation between buyer sentiment and valuation outcomes. With agreed sales recording a net balance of -12% in February and near-term transaction expectations at -2% [2], surveyors must adopt defensive valuation postures.

Prime central London properties face particular challenges, with the -40% buyer enquiry balance indicating severe demand contraction [2]. Chartered surveyors working in areas like Chelsea, Hampstead, and Fulham should:

- Extend comparable search periods to capture sufficient transaction evidence

- Apply larger downward adjustments for market condition changes

- Consider international buyer sentiment, which may be disproportionately affected by geopolitical tensions

- Emphasize property quality differentials that may preserve value better than market averages

Suburban and commuter belt properties in areas like Surrey, Hertfordshire, and Buckinghamshire show greater resilience but still require careful assessment of:

- Local employment stability and commuting pattern changes

- School catchment premium sustainability during economic uncertainty

- Buyer demographic shifts (families vs. investors vs. downsizers)

Regional markets in northern England and Scotland demonstrate relative stability, with some areas showing positive price momentum despite national headwinds [2]. Surveyors in these markets should avoid over-applying national trend data to local valuations while remaining alert to potential contagion effects if uncertainty persists.

Commercial and Specialized Valuations

Commercial property valuations face additional complexity from business confidence impacts and tenant covenant strength concerns during geopolitical uncertainty.

Retail and hospitality properties require enhanced tenant sustainability analysis, as these sectors face direct consumer confidence impacts. Surveyors should:

- Scrutinize lease covenant strength more rigorously

- Apply higher void period assumptions in cash flow projections

- Consider sector-specific vulnerability to economic downturns

- Adjust capitalization rates to reflect increased risk

Office and industrial properties show greater resilience but require assessment of tenant industry exposure to geopolitical risks (energy-intensive industries, import-dependent businesses, etc.).

Specialized valuations including insurance reinstatement assessments and ATED valuations must clearly distinguish between market value (affected by sentiment and conditions) and reinstatement cost or other statutory bases (less directly affected).

Leasehold and Investment Property Considerations

Leasehold properties require particular attention during uncertain markets. Buyers become more cautious about:

- Remaining lease terms and extension costs

- Service charge affordability during potential economic downturns

- Ground rent obligations and their impact on mortgageability

- Building safety compliance and associated costs

For properties requiring lease extension valuations or freehold acquisition assessments, current market uncertainty affects both the existing lease value and the marriage value calculation, requiring careful documentation of assumptions.

Investment properties face dual pressures from potential capital value decline and yield compression concerns. Building surveyors must assess:

- Tenant retention probability during economic uncertainty

- Rental growth assumptions in volatile environments

- Exit strategy viability and holding period flexibility

- Financing cost impacts on investment returns

Future Outlook and Long-Term Sentiment Recovery

Despite current challenges, longer-term market sentiment remains cautiously optimistic. RICS data shows a +17% net balance for sales activity expectations over twelve months [2], indicating surveyors anticipate recovery once geopolitical tensions stabilize.

This divergence between near-term caution and longer-term optimism creates a strategic opportunity for building surveyors to provide nuanced guidance to clients:

📊 For buyers: Current valuations may represent entry opportunities if geopolitical risks subside, but patience and careful due diligence remain essential

📊 For sellers: Realistic pricing aligned with current market conditions will achieve better outcomes than aspirational pricing based on pre-uncertainty valuations

📊 For investors: Selective acquisition during uncertainty can yield long-term value, but thorough assessment of property fundamentals and location resilience is critical

📊 For lenders: Conservative valuation approaches protect against downside risk while recognizing that quality properties in strong locations maintain value better than market averages

Monitoring Key Indicators

Building surveyors should establish systematic monitoring of key market indicators to adjust valuation approaches as conditions evolve:

Weekly monitoring:

- Mortgage rate movements and spread changes

- Geopolitical news flow and financial market reactions

- New listing volumes and price positioning

Monthly monitoring:

- RICS sentiment surveys and regional breakdowns

- Transaction volumes and agreed sale trends

- Time on market statistics and price reduction frequencies

- Inventory levels and supply-demand balance shifts

Quarterly monitoring:

- Completed transaction analysis and price index movements

- Regional market divergence patterns

- Lending criteria changes and mortgage availability

- Economic indicators (employment, inflation, consumer confidence)

This systematic approach enables surveyors to provide clients with current, evidence-based valuation advice that reflects rapidly changing market conditions.

Conclusion

Valuation Uncertainty in Spring 2026: How Building Surveyors Navigate Geopolitical Risks and Buyer Sentiment Volatility represents a defining professional challenge that requires building surveyors to enhance traditional methodologies with sophisticated risk assessment and sentiment analysis. The dramatic decline in buyer enquiries to -26% net balance, combined with persistent geopolitical tensions and mortgage rate volatility, has fundamentally altered the valuation landscape.

Successful navigation of this environment demands that chartered surveyors:

✅ Apply more conservative comparable selection criteria, emphasizing recent transactions under similar market conditions

✅ Incorporate geopolitical risk premiums transparently documented within valuation reports

✅ Monitor sentiment indicators systematically to adjust valuation approaches as conditions evolve

✅ Provide regional and sector-specific analysis rather than relying on national trend data

✅ Communicate uncertainty clearly to clients while providing actionable guidance

For property owners, buyers, and investors seeking professional valuation services during this uncertain period, engaging experienced chartered surveyors who understand these complex dynamics is essential. Whether you require a comprehensive building survey, specialized Red Book valuation, or guidance on valuation factors affecting your property, working with professionals who actively adapt their methodologies to current market realities will provide the confidence needed to make informed decisions.

The Spring 2026 market may present challenges, but it also offers opportunities for those who approach property transactions with realistic expectations, thorough due diligence, and expert professional guidance. As longer-term sentiment indicators suggest eventual recovery, properties acquired or valued accurately during this period of uncertainty may prove to be sound long-term investments.

Take action today: If you're considering buying, selling, or require a professional property valuation during this volatile period, consult with chartered surveyors who understand the complexities of current market conditions and can provide the expert guidance you need to navigate uncertainty successfully.

References

[1] Geopolitical Uncertainty Threatens Otherwise Promising Spring Housing Market – https://www.scotsmanguide.com/news/geopolitical-uncertainty-threatens-otherwise-promising-spring-housing-market/

[2] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[4] Geopolitical Shock Sends Mortgage Rates Higher Erasing Prior Weeks Decline – https://www.mortgage-underwriters.org/mortgage-underwriting-news/2026/3/5/geopolitical-shock-sends-mortgage-rates-higher-erasing-prior-weeks-decline