The luxury property market in England faces a seismic shift in 2026 as the government introduces the High Value Council Tax Surcharge (HVCTS), creating unprecedented challenges for property owners, buyers, and surveyors alike. With valuations conducted by the Valuation Office Agency (VOA) determining which properties cross the £2 million threshold, valuing high-value properties under new 2026 council tax surcharge thresholds: surveyor negotiation strategies has become a critical concern for stakeholders across the premium real estate sector.

This landmark tax reform will affect approximately 100,000 homes—fewer than 1% of English properties—yet its impact on pricing dynamics, buyer negotiations, and valuation precision cannot be overstated[4]. Property owners clustering just below the £2 million threshold are already creating "price bunching" phenomena, while buyers increasingly demand forensic accuracy in valuations to avoid unexpected tax liabilities.

Key Takeaways

- 🏛️ The VOA will conduct a targeted 2026 valuation exercise using publicly available data rather than on-site inspections, creating unique challenges for property owners seeking to influence their assessed values[1][4]

- 💰 Four surcharge bands range from £2,500 to £7,500 annually, with the £2 million entry threshold creating significant price clustering and valuation precision requirements[2]

- 📊 Strategic price bunching below tax thresholds is already affecting luxury market dynamics, making accurate property assessments essential for both sellers and buyers

- 🔍 Surveyor negotiation strategies must adapt to a desktop valuation methodology that limits traditional inspection-based evidence gathering

- ⏰ Early 2026 consultation and April 2028 implementation provide a narrow window for property owners to challenge valuations and implement tax planning strategies[1][2]

Understanding the 2026 High Value Council Tax Surcharge Framework

The HVCTS represents the most significant reform to property taxation in England since the introduction of Council Tax in 1993. Unlike standard Council Tax bands, which remain frozen at 1991 valuations, this new surcharge operates on current market values determined through a fresh 2026 assessment[1].

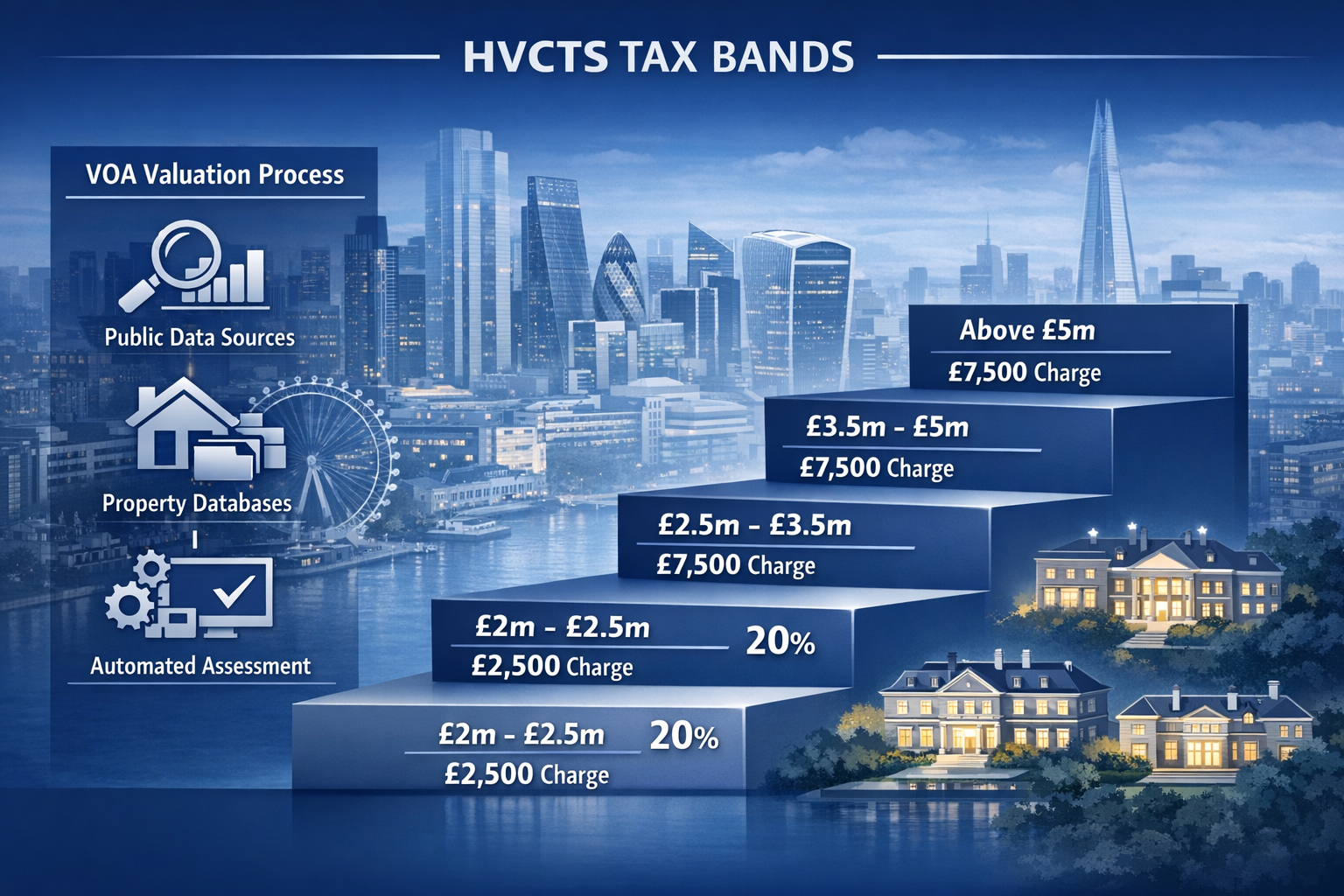

The Four-Tier Surcharge Structure

The government has established four distinct charging bands based on property values:

| Property Value Range | Annual Surcharge |

|---|---|

| £2,000,000 – £2,499,999 | £2,500 |

| £2,500,000 – £3,499,999 | £5,000 |

| £3,500,000 – £4,999,999 | £7,500 |

| £5,000,000+ | £7,500 |

These charges will increase in line with the Consumer Price Index (CPI) from 2029/30 onwards, creating long-term financial implications for affected property owners[2].

Geographic Distribution and Market Impact

The surcharge's impact is heavily concentrated in specific regions. Approximately 50% of affected properties are located in London, with most of the remainder in the southeast[4]. Areas such as Hampstead, Central London, and affluent parts of Surrey will see the highest concentration of liable properties.

This geographic concentration creates distinct regional challenges for valuing high-value properties under new 2026 council tax surcharge thresholds: surveyor negotiation strategies, particularly in markets where property values frequently hover near threshold boundaries.

Revenue Projections and Policy Objectives

Financial modelling estimates the surcharge will raise approximately £400 million per year by 2029/30, with an average additional bill of about £4,500 per affected property[4]. This revenue generation demonstrates the government's commitment to extracting additional taxation from high-value residential assets without undertaking a full Council Tax revaluation.

The VOA Valuation Methodology: Desktop Assessments and Data Limitations

Understanding how the VOA will conduct valuations is crucial for developing effective negotiation strategies. Unlike traditional surveyor assessments, the 2026 exercise will rely primarily on publicly available data rather than on-site property inspections[4].

Data Sources and Assessment Criteria

The VOA's desktop valuation approach will likely incorporate:

- Land Registry transaction data showing recent sales of comparable properties

- Property characteristics databases including floor area, number of rooms, and construction type

- Location factors such as proximity to amenities, transport links, and school catchment areas

- Planning records indicating extensions, conversions, or material alterations

- Council Tax band information providing baseline property classifications

This methodology presents both challenges and opportunities for property owners. While the absence of physical inspections may overlook certain property defects or limitations, it also means valuations could fail to account for unique features that would typically reduce market value.

Limitations of Automated Valuation Models

Desktop valuations inherently lack the nuance of professional surveyor assessments. Key limitations include:

✗ Inability to assess property condition beyond what's visible in external photographs or disclosed in public records

✗ Standardized adjustments that may not reflect unique property characteristics affecting marketability

✗ Reliance on comparable sales that may not accurately represent the subject property's specific attributes

✗ Limited consideration of internal layout, finish quality, or bespoke improvements

These limitations create opportunities for chartered surveyors to provide evidence-based challenges to VOA assessments, particularly where desktop valuations fail to capture material factors affecting property value.

Price Bunching Phenomena and Valuation Precision Requirements

The introduction of distinct tax thresholds at £2 million, £2.5 million, £3.5 million, and £5 million creates powerful incentives for price bunching—the clustering of property transactions just below threshold values to avoid higher tax bands.

Market Distortions at Threshold Boundaries

Economic theory and empirical evidence from similar tax regimes suggest several market responses:

Seller Behavior: Property owners with homes valued near thresholds may accept lower offers to facilitate sales below surcharge bands, particularly at the critical £2 million entry point.

Buyer Leverage: Purchasers gain significant negotiating power when properties are valued close to thresholds, as they can credibly argue for price reductions that avoid triggering higher tax bands.

Valuation Disputes: The financial stakes of threshold classification create heightened scrutiny of valuation accuracy, with property owners more likely to challenge assessments placing them above threshold boundaries.

Strategic Implications for Luxury Property Transactions

For properties valued between £1.9 million and £2.1 million, valuation precision becomes paramount. A difference of just £50,000—representing less than 3% of property value—can mean the difference between no surcharge liability and an additional £2,500 annual charge.

This creates specific challenges for valuing high-value properties under new 2026 council tax surcharge thresholds: surveyor negotiation strategies, particularly in areas like North London and West London where property values frequently cluster around the £2 million mark.

Evidence-Based Valuation Defense

Professional surveyors can provide critical support by:

- Documenting property-specific factors that may reduce market value below VOA assessments

- Identifying comparable sales that better reflect the subject property's characteristics

- Quantifying defects or limitations not captured in desktop valuations

- Preparing detailed valuation reports suitable for formal challenge procedures

Surveyor Negotiation Strategies for the 2026 Valuation Exercise

Effective negotiation with the VOA requires a fundamentally different approach than traditional property transactions. The following strategies provide a framework for challenging valuations and minimizing surcharge liability.

Pre-Valuation Preparation (Early 2026)

Strategy 1: Comprehensive Property Documentation

Before the VOA conducts its assessment, property owners should work with professional surveyors to document:

- All property defects, structural issues, or maintenance requirements

- Features that limit marketability or functionality

- Restrictions on use, access, or development potential

- Any factors that would reduce value in an open market transaction

This documentation creates a foundation for subsequent challenges if the VOA's desktop valuation appears inflated.

Strategy 2: Comparable Evidence Gathering

Identify and document recent sales of genuinely comparable properties, paying particular attention to:

- Similar location, size, and property type

- Comparable condition and specification

- Transactions occurring in similar market conditions

- Sales that reflect any unique characteristics of the subject property

The quality of comparable evidence directly impacts the credibility of valuation challenges.

During the Valuation Period (Mid-2026)

Strategy 3: Monitoring VOA Methodology

The early 2026 public consultation will reveal specific details about the VOA's valuation approach[1][2]. Surveyors should:

- Analyze published methodology guidance

- Identify potential weaknesses or standardization issues

- Prepare challenge strategies based on known limitations

- Develop evidence templates aligned with VOA requirements

Strategy 4: Proactive Engagement

While the VOA will not conduct on-site inspections as standard practice, property owners can proactively submit evidence demonstrating:

- Material differences from comparable properties

- Specific defects or limitations affecting value

- Planning restrictions or legal encumbrances

- Market evidence supporting lower valuations

Post-Assessment Challenge Procedures (Late 2026-2027)

Strategy 5: Formal Challenge Preparation

Once the VOA issues provisional valuations, property owners will have opportunities to challenge assessments. Effective challenges require:

📋 Detailed valuation reports from qualified RICS chartered surveyors providing independent market value opinions

📋 Comprehensive comparable evidence demonstrating that similar properties sold for lower values

📋 Photographic documentation showing property condition and specific features affecting value

📋 Expert testimony regarding unique factors not captured in desktop assessments

Strategy 6: Threshold-Specific Arguments

For properties valued near threshold boundaries, surveyors should emphasize:

- The margin of error inherent in desktop valuations

- Specific factors that could reasonably place the property below the threshold

- Market evidence showing price clustering below thresholds

- The disproportionate tax impact of marginal valuation differences

Advanced Negotiation Techniques

Leveraging Market Timing

The VOA's valuation date will be critical. Properties should be valued based on market conditions at a specific point in time. Surveyors can argue that:

- Temporary market peaks should not determine long-term tax liability

- Specific market conditions at the valuation date may not reflect typical value

- Recent market corrections should be considered in threshold determinations

Emphasizing Valuation Uncertainty

Desktop valuations inherently involve greater uncertainty than physical inspections. Professional surveyors can quantify this uncertainty and argue that:

- Properties should be classified in lower bands when valuations fall within uncertainty ranges

- The burden of proof for higher valuations should rest with the VOA

- Conservative valuations better reflect the limitations of desktop methodology

Regional Considerations and Local Market Dynamics

The impact of valuing high-value properties under new 2026 council tax surcharge thresholds: surveyor negotiation strategies varies significantly by location, requiring region-specific approaches.

Prime London Markets

Areas such as Hampstead, Islington, and Camden face unique challenges:

- High property density near threshold values creates widespread surcharge exposure

- Diverse property types complicate comparable evidence gathering

- Rapid market fluctuations make point-in-time valuations particularly contentious

- Leasehold complications require careful consideration of how lease terms affect value

Southeast England and Surrey

Affluent areas in Surrey, including Guildford, Esher, and Epsom, present different dynamics:

- Larger property sizes with more variable characteristics

- Greater reliance on land value components

- More heterogeneous property stock making standardized valuations problematic

- Rural and semi-rural locations where comparable evidence may be limited

Emerging Hotspots

Areas experiencing rapid gentrification or property value growth require particular attention:

- Properties that recently crossed threshold values due to market appreciation

- Neighborhoods where the £2 million threshold captures an unexpectedly large proportion of housing stock

- Locations where VOA valuations may lag behind or overestimate current market conditions

Timeline and Implementation Considerations

Understanding the implementation timeline is crucial for developing effective strategies.

Key Dates and Milestones

Early 2026: Public consultation on valuation methodology details[1][2]

- Opportunity to influence VOA approach

- Critical period for understanding assessment criteria

Mid-2026: VOA conducts targeted valuation exercise

- Desktop assessments completed

- Provisional valuations issued

Late 2026-2027: Challenge and appeal period

- Property owners can contest valuations

- Evidence submission and negotiation occurs

April 2028: Surcharge takes effect[1][2]

- First annual charges become payable

- Ongoing appeal mechanisms available

Strategic Planning Windows

Property owners have limited time to implement effective strategies:

✓ Immediate (2026): Document property characteristics and gather comparable evidence

✓ Short-term (2026-2027): Engage professional surveyors and prepare formal challenges

✓ Medium-term (2027-2028): Complete appeal processes and finalize tax planning

✓ Long-term (2028+): Monitor market changes and prepare for future revaluations

Professional Surveyor Engagement: When and Why

While the VOA's desktop methodology limits traditional surveyor involvement in the initial assessment, professional expertise remains invaluable throughout the process.

Value-Adding Surveyor Services

Independent Valuation Opinions

Professional valuation services provide:

- Credible alternative valuations for challenge purposes

- Detailed analysis of property-specific factors affecting value

- Expert testimony supporting lower valuations

- Documentation suitable for formal appeal procedures

Evidence Gathering and Documentation

Surveyors can systematically compile:

- Comprehensive photographic records of property condition

- Detailed property descriptions highlighting value-reducing features

- Comparable sales analysis with appropriate adjustments

- Technical reports on structural issues or defects

Challenge Preparation and Submission

Experienced surveyors understand:

- VOA challenge procedures and requirements

- Effective presentation of evidence

- Technical arguments most likely to succeed

- Negotiation strategies for threshold cases

Selecting the Right Professional

When engaging surveyors for HVCTS matters, property owners should prioritize:

🎯 RICS qualification and relevant experience in high-value property valuation

🎯 Local market knowledge in the specific area where the property is located

🎯 Experience with VOA procedures and tax-related valuations

🎯 Track record in successfully challenging property assessments

Broader Tax Planning and Property Strategy

The HVCTS doesn't exist in isolation—it interacts with other property taxes and investment decisions.

Integration with Existing Tax Obligations

Property owners must consider the surcharge alongside:

- Standard Council Tax (which remains unchanged)[1]

- Stamp Duty Land Tax on property purchases

- Capital Gains Tax on property disposals

- Inheritance Tax planning for property assets

- ATED (Annual Tax on Enveloped Dwellings) for properties held in corporate structures[5]

Strategic Property Decisions

The surcharge may influence:

Purchase Timing: Buyers may delay acquisitions until after the 2026 valuation exercise to gain certainty about tax liabilities.

Sale Considerations: Sellers of properties near thresholds may accelerate disposals before the surcharge takes effect in April 2028.

Property Improvements: Owners may defer value-enhancing renovations until after the VOA assessment to avoid higher valuations.

Ownership Structures: While the surcharge applies regardless of ownership structure, integration with other taxes may prompt structural reviews.

Case Studies: Threshold Scenarios and Negotiation Outcomes

Understanding practical scenarios helps illustrate effective negotiation strategies.

Scenario 1: The £2.05 Million London Townhouse

Situation: A Victorian townhouse in South West London receives a provisional VOA valuation of £2.05 million, triggering the £2,500 annual surcharge.

Surveyor Strategy:

- Document deferred maintenance totaling £150,000

- Identify comparable sales between £1.85-£1.95 million

- Highlight short remaining lease term (78 years)

- Emphasize property's position on busy road

Outcome: Valuation reduced to £1.95 million, eliminating surcharge liability and saving £2,500 annually.

Scenario 2: The £2.45 Million Surrey Family Home

Situation: A detached family home in Surrey is valued at £2.45 million, just £50,000 below the £2.5 million threshold for the higher £5,000 charge.

Surveyor Strategy:

- Accept the £2,500 surcharge as appropriate

- Focus on preventing upward adjustment to £2.5 million+

- Document property limitations and comparable evidence

- Emphasize margin of error in desktop valuations

Outcome: Valuation maintained at £2.45 million, avoiding the higher £5,000 charge and saving £2,500 annually.

Scenario 3: The £5.2 Million Prime Central London Apartment

Situation: A luxury apartment in Central London is valued at £5.2 million, well above the top threshold.

Surveyor Strategy:

- Acknowledge surcharge liability is unavoidable

- Challenge the specific valuation figure to reduce future CPI-linked increases

- Provide evidence supporting £4.9 million valuation

- Highlight unique factors affecting marketability

Outcome: Valuation reduced to £4.9 million, maintaining the same £7,500 annual charge but establishing a lower baseline for future CPI increases.

Common Pitfalls and How to Avoid Them

Property owners and their advisors should be aware of frequent mistakes that undermine negotiation effectiveness.

❌ Pitfall 1: Delayed Engagement

Problem: Waiting until after provisional valuations are issued to begin preparation.

Solution: Engage surveyors early in 2026 to document property characteristics and gather evidence before the VOA assessment.

❌ Pitfall 2: Inadequate Comparable Evidence

Problem: Relying on superficially similar properties without appropriate adjustments.

Solution: Work with experienced surveyors to identify truly comparable sales and make justified adjustments for differences.

❌ Pitfall 3: Emotional Rather Than Evidence-Based Arguments

Problem: Challenging valuations based on personal opinions rather than objective market evidence.

Solution: Present professional, evidence-based challenges supported by qualified surveyor opinions and market data.

❌ Pitfall 4: Ignoring Regional Market Dynamics

Problem: Applying generic strategies without considering local market conditions.

Solution: Engage surveyors with specific expertise in the relevant area, whether North West London, East London, or elsewhere.

❌ Pitfall 5: Failing to Consider Long-Term Implications

Problem: Focusing solely on the 2026 valuation without considering future revaluations or market changes.

Solution: Develop comprehensive tax planning strategies that account for ongoing surcharge liability and potential future increases.

The Future of High-Value Property Taxation

The HVCTS represents a significant policy shift that may signal broader changes to property taxation in England.

Potential Future Developments

Expanded Revaluations: The 2026 exercise may pave the way for more frequent property revaluations across all Council Tax bands.

Threshold Adjustments: Future governments may lower the £2 million threshold or introduce additional bands to capture more properties.

Integration with Council Tax Reform: The surcharge could be a stepping stone toward comprehensive Council Tax modernization based on current values.

Regional Variations: Different threshold levels or charge amounts may be introduced for different parts of England.

Preparing for Ongoing Change

Property owners should:

- Maintain updated property documentation and valuation evidence

- Monitor policy developments and consultation opportunities

- Develop relationships with professional advisors familiar with property taxation

- Consider long-term property strategies that account for evolving tax landscapes

Conclusion

Valuing high-value properties under new 2026 council tax surcharge thresholds: surveyor negotiation strategies requires a sophisticated understanding of the VOA's desktop methodology, threshold dynamics, and evidence-based challenge procedures. The introduction of the HVCTS creates unprecedented challenges for luxury property owners, particularly those with properties valued near critical threshold boundaries where price bunching and valuation precision become paramount.

The £2 million entry threshold, combined with additional bands at £2.5 million, £3.5 million, and £5 million, creates powerful incentives for accurate valuations and effective negotiation strategies. With approximately 100,000 properties affected and £400 million in annual revenue at stake, the financial implications are substantial for individual property owners and the broader luxury market[4].

Actionable Next Steps

Property owners should take the following actions immediately:

-

Engage qualified surveyors with experience in high-value property valuation and VOA procedures, particularly those with local expertise in areas like Hampstead, Central London, or Surrey

-

Document property characteristics comprehensively, including any defects, limitations, or unique features that may affect market value

-

Gather comparable evidence systematically, identifying recent sales of genuinely similar properties in the same location

-

Monitor the early 2026 consultation to understand specific VOA methodology details and identify challenge opportunities[1][2]

-

Prepare challenge strategies in advance, developing evidence-based arguments for properties likely to be valued near threshold boundaries

-

Consider broader tax planning implications, integrating the HVCTS with existing property tax obligations and investment strategies

The narrow window between the early 2026 consultation and the April 2028 implementation date demands proactive engagement. Property owners who begin preparation now will be best positioned to minimize surcharge liability through effective negotiation and evidence-based challenges to VOA valuations.

As the luxury property market adapts to this new taxation landscape, professional surveyor expertise becomes increasingly valuable—not just for challenging individual valuations, but for navigating the broader strategic implications of threshold-based taxation on property transactions, pricing dynamics, and long-term investment decisions.

References

[1] High Value Council Tax Surcharge – https://www.gov.uk/government/news/high-value-council-tax-surcharge

[2] High Value Council Tax Surcharge – https://www.uktaxpolicymap.com/taxing-work-and-wealth/high-value-council-tax-surcharge.aspx

[3] 4 Important Tax Changes Happening In 2026 And How To Prepare – https://www.sovereign-ifa.co.uk/news/4-important-tax-changes-happening-in-2026-and-how-to-prepare/

[4] The Mansion Tax Everything You Need To Know About This Landmark Shift In Council Tax – https://www.lubbockfine.co.uk/blog/the-mansion-tax-everything-you-need-to-know-about-this-landmark-shift-in-council-tax/

[5] High Value Council Tax Surcharge Reform Significant Implications – https://www.taxadvisermagazine.com/article/high-value-council-tax-surcharge-reform-significant-implications

[6] High Value Council Tax Surcharge What You Need To Know – https://www.greenwoods.co.uk/article/high-value-council-tax-surcharge-what-you-need-to-know/

[7] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[8] How Will The High Value Council Tax Surcharge Work – https://www.ross-brooke.co.uk/how-will-the-high-value-council-tax-surcharge-work/