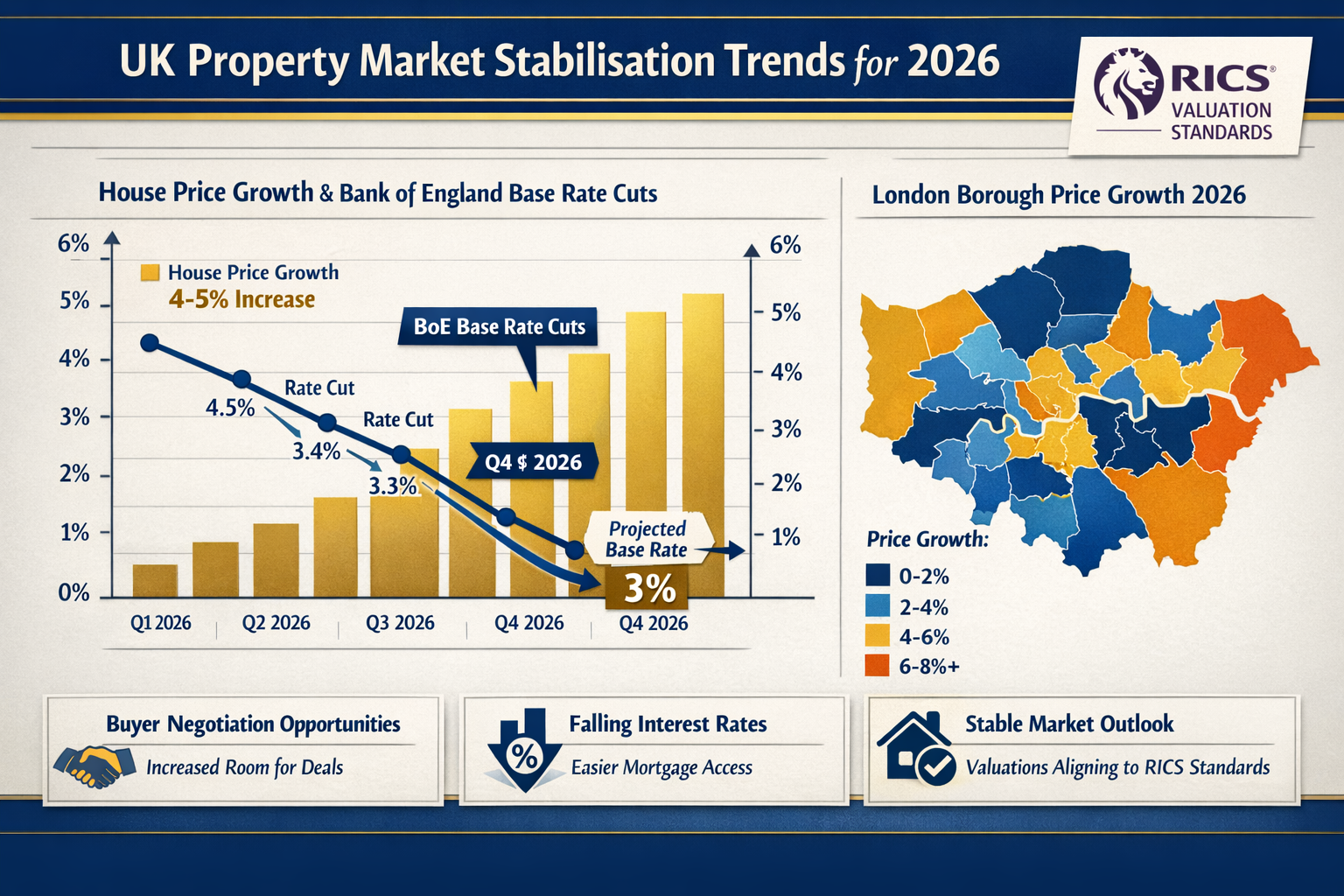

The UK property market in 2026 presents a unique challenge for buyers: how do you negotiate effectively when growth has stabilised at modest levels but prices remain elevated? With national property price growth projected at just 4-5% and the Bank of England implementing gradual rate cuts, buyers now have unprecedented leverage in negotiations—but only if they understand how to value properties in this new stabilising environment.

Valuing Stabilising Markets: Low Single-Digit Growth Strategies for 2026 Buyer Negotiations has become essential knowledge for anyone looking to purchase property this year. Unlike the volatile boom-and-bust cycles of previous decades, 2026's market is characterised by measured growth, regional divergences, and data-driven pricing expectations. This creates opportunities for informed buyers who can demonstrate realistic valuations backed by professional surveyor analysis.

The economic backdrop supports this cautious optimism. Major developed economies are experiencing low single-digit growth driven primarily by productivity improvements rather than employment expansion[2][4]. This productivity-led growth pattern means that while the economy continues to advance, the pace is measured and sustainable—exactly the conditions that favour strategic property buyers who take the time to understand true market values.

Key Takeaways

- 📊 Modest growth expectations: UK property markets are stabilising with 4-5% annual growth, creating negotiation opportunities for data-driven buyers

- 💷 Rate cuts enhance affordability: Gradual Bank of England rate reductions improve mortgage accessibility while maintaining market stability

- 🏘️ Regional divergence matters: London boroughs and surrounding areas show varying appreciation rates, requiring localised valuation expertise

- 📋 Professional valuations provide leverage: RICS-accredited surveyor reports offer concrete evidence for price negotiations in stabilising markets

- 🎯 Strategic timing is critical: 2026's productivity-led economic growth creates sustainable conditions for long-term property investment

Understanding Market Stabilisation in 2026

The Shift from Volatility to Measured Growth

The property market landscape has fundamentally changed. After years of dramatic price swings, interest rate shocks, and pandemic-driven distortions, 2026 represents a return to sustainable, predictable growth patterns. This stabilisation doesn't mean stagnation—it means the market is maturing into a more rational pricing environment.

Economic forecasters anticipate sustained resilience across major markets, with growth expectations tempered by realistic productivity assessments[2]. For property buyers, this translates into markets where prices increase gradually rather than explosively, creating windows of opportunity for those who can accurately assess value.

The Bank of England's monetary policy plays a crucial role in this stabilisation. With inflation largely under control and economic growth steady, gradual rate cuts are being implemented to support continued expansion without overheating the market. This creates a "Goldilocks" scenario for property buyers: improving affordability through lower borrowing costs, combined with moderate price appreciation that doesn't outpace income growth.

Regional Divergences Create Valuation Challenges

While national averages suggest 4-5% growth, the reality on the ground is far more nuanced. Different regions—and even different neighbourhoods within London—are experiencing vastly different market conditions. Areas like Battersea and Fulham may see stronger appreciation due to infrastructure improvements and regeneration projects, while other locations remain flat or decline slightly.

This regional divergence makes professional valuation services more critical than ever. A chartered surveyor in Richmond will have intimate knowledge of local market conditions that national statistics simply cannot capture. They understand which streets command premium prices, which developments are affecting nearby property values, and how local planning decisions impact future appreciation potential.

| Market Characteristic | 2024-2025 | 2026 Projection |

|---|---|---|

| National Price Growth | 2-3% | 4-5% |

| Interest Rate Trend | Holding steady | Gradual cuts |

| Market Volatility | High | Moderate-Low |

| Regional Variation | Moderate | High |

| Buyer Negotiation Power | Limited | Enhanced |

Productivity-Led Growth and Property Values

One of the most significant economic trends shaping 2026 is the shift toward productivity-led rather than employment-led growth[4]. This distinction matters enormously for property valuation. When growth comes from productivity improvements—automation, efficiency gains, technological advancement—it tends to be more sustainable and less inflationary than growth driven by simply adding more workers.

For property buyers, this means:

✅ Wage growth remains steady without sparking inflation that forces rate increases

✅ Corporate profitability improves without overheating the economy

✅ Mortgage affordability gradually improves as rates decline while incomes rise

✅ Property price appreciation stays moderate and aligned with fundamental economic conditions

This economic environment creates ideal conditions for strategic property purchases. Buyers aren't competing in frenzied bidding wars, but they also aren't facing a collapsing market. Instead, they're operating in a rational environment where accurate valuation and skilled negotiation determine who gets the best deals.

Valuing Stabilising Markets: Low Single-Digit Growth Strategies for 2026 Buyer Negotiations—Core Valuation Methods

Comparative Market Analysis in Slow-Growth Environments

When markets are stabilising with low single-digit growth, traditional valuation methods must be applied with greater precision. Comparative Market Analysis (CMA) becomes the foundation of effective buyer negotiations, but it requires more sophisticated application than in high-growth markets.

The key to effective CMA in 2026 is understanding that recent comparable sales may not accurately reflect current market conditions if they occurred during different rate environments. A property that sold six months ago when mortgage rates were 50 basis points higher may have sold at a discount that no longer applies—or conversely, a sale during a brief rate dip may have captured an artificial premium.

Professional RICS registered valuers adjust comparable sales data for:

- Time of sale and prevailing interest rates

- Property condition differences requiring repair cost adjustments

- Location micro-variations within the same postcode

- Market momentum at the time of transaction

- Seller motivation factors that may have influenced pricing

A homebuyer report provides the detailed property condition assessment needed to make accurate comparisons. If comparable properties were in better condition, the asking price for your target property should reflect necessary repairs and updates.

Discounted Cash Flow Adjustments for Modest Growth

For investment properties or buyers considering long-term value, Discounted Cash Flow (DCF) analysis must be recalibrated for low single-digit growth scenarios. The optimistic 8-10% annual appreciation assumptions that might have been reasonable in previous cycles are no longer appropriate.

In 2026's stabilising market, DCF models should incorporate:

Conservative growth assumptions: 4-5% annual appreciation aligned with economic fundamentals[2]

Realistic rental yield projections: Based on current market rents rather than optimistic future increases

Appropriate discount rates: Reflecting current and projected interest rate environments

Maintenance and upgrade costs: More significant as a percentage of value in slow-growth markets

"In stabilising markets with low single-digit growth, the margin for error in valuation shrinks dramatically. Buyers who overestimate future appreciation by even 2-3% annually can find themselves overpaying by tens of thousands of pounds over a typical holding period."

This precision matters because in a 4-5% growth environment, overpaying by 10% takes more than two years of appreciation just to break even—compared to less than one year in a 15% growth market. The stakes of accurate valuation are higher when growth is modest.

Replacement Cost and Reinstatement Valuations

Another critical valuation approach in stabilising markets is replacement cost analysis. This method asks: "What would it cost to rebuild this property from scratch?" When market prices are rising slowly, replacement cost often provides a floor value below which properties rarely fall.

A reinstatement cost valuation calculates the full cost of rebuilding a property to its current standard, including:

- Construction costs at current labour and material rates

- Professional fees for architects, engineers, and planning

- Demolition and site preparation expenses

- Temporary accommodation during rebuilding

- Additional costs like landscaping and boundary features

For buyers negotiating in 2026, understanding replacement cost provides powerful leverage. If an asking price significantly exceeds what it would cost to build an equivalent new property, you have concrete evidence for negotiation. This is particularly relevant for older properties requiring substantial modernisation.

The Role of Professional Survey Reports in Price Negotiations

The most powerful tool in a buyer's negotiation arsenal is a comprehensive professional survey report. In stabilising markets where every percentage point matters, the detailed evidence provided by chartered surveyors can justify price reductions that save buyers substantial sums.

Types of survey reports that strengthen negotiation positions:

🔍 Building Survey: Comprehensive assessment identifying all defects and required repairs

🏠 Homebuyer Report: Balanced evaluation of condition with traffic-light rating system

⚠️ Specific Defect Report: Targeted investigation of particular concerns like subsidence or damp

📋 Snagging Report: For new builds, identifying construction defects requiring developer remedy

When a survey reveals issues like structural movement, roof deterioration, or outdated electrical systems, buyers can obtain repair cost estimates and present these as evidence for price reductions. In a market growing at only 4-5% annually, a £30,000 repair bill represents 6-12 months of appreciation on a typical London property—a significant negotiating point.

Implementing Valuing Stabilising Markets: Low Single-Digit Growth Strategies for 2026 Buyer Negotiations

Strategic Timing and Market Entry Points

In stabilising markets, timing your entry becomes more nuanced than simply "buying when prices are low." With modest, predictable growth, the focus shifts to identifying micro-market opportunities and seasonal patterns that create temporary advantages.

The 2026 market presents several strategic timing considerations:

Post-holiday periods (January-February, September) typically see reduced competition and more motivated sellers willing to negotiate. With low single-digit growth, the difference between buying in peak season versus off-peak can represent 3-5% of the purchase price—nearly a full year's appreciation.

Interest rate announcement cycles create windows of opportunity. When the Bank of England signals upcoming rate cuts, buyer activity often pauses as people wait for improved mortgage terms. Buyers who move decisively during these waiting periods face less competition and stronger negotiating positions.

Local market events such as infrastructure completions, planning decisions, or major employer relocations create timing opportunities. Professional surveyors with local expertise in areas like Putney or Hammersmith can identify these opportunities before they're reflected in asking prices.

Data-Driven Negotiation Frameworks

Successful negotiations in 2026 require evidence-based approaches rather than emotional appeals or aggressive tactics. Sellers in stabilising markets are more sophisticated and less desperate than in declining markets, so they respond better to logical, well-documented arguments for price adjustments.

The Data-Driven Negotiation Framework:

Step 1: Establish Market Context

Present recent comparable sales data showing actual transaction prices (not asking prices) for similar properties in the immediate area. Demonstrate that asking prices often exceed final sale prices by specific percentages.

Step 2: Document Property-Specific Issues

Use professional survey findings to identify condition issues, required repairs, and modernisation needs. Obtain contractor quotes for major work to establish concrete cost figures.

Step 3: Calculate Adjusted Fair Value

Combine comparable market data with property-specific adjustments to arrive at a justified offer price. Show your calculations transparently.

Step 4: Present Growth-Adjusted Scenarios

In a 4-5% growth market, demonstrate how overpaying affects long-term returns. Show the seller that accepting a realistic price today is better than holding out for an unrealistic price that may take months to achieve.

Step 5: Maintain Flexibility on Terms

If price negotiation reaches an impasse, consider negotiating on other terms: completion timeline, fixtures and fittings included, or repair completion before exchange.

Leveraging Professional Valuation Reports

The credibility of your negotiating position depends heavily on the quality of your supporting evidence. This is where professional RICS valuation services provide maximum value—not just in identifying issues, but in presenting them in a format that sellers and their agents must take seriously.

A RICS-accredited valuation carries weight because:

✅ It's prepared by qualified professionals bound by strict ethical standards

✅ It follows standardised methodologies recognised across the industry

✅ It provides defensible evidence that estate agents and solicitors respect

✅ It can be used for mortgage purposes, ensuring lender agreement with your position

When presenting a professional valuation in negotiations, emphasise that this isn't just your opinion—it's an independent expert assessment. In stabilising markets where emotion has been largely removed from pricing, this objectivity is particularly persuasive.

For properties with specific complexities, specialised valuations add even more credibility. A matrimonial valuation or probate valuation demonstrates that professional valuers have assessed the property in formal legal contexts, further validating your negotiating position.

Regional Strategy Variations

While the national market shows 4-5% growth, implementing effective negotiation strategies requires understanding regional and local variations. What works in central London may not work in surrounding counties, and vice versa.

London-Specific Strategies:

In prime central London locations, buyers face more sophisticated sellers and agents who are well-versed in market conditions. Here, professional valuations from central London surveyors with specific local expertise become essential. These professionals understand the nuances of conservation areas, listed building considerations, and the premium commanded by specific streets or garden squares.

Outer London and Home Counties:

Areas like Weybridge, Epsom, and Guildford present different dynamics. These markets often lag central London trends by 6-12 months, creating opportunities for buyers who understand where the market is heading. Commuter patterns, school catchment areas, and local employment centres drive values more than in central locations.

Regional Divergence Table:

| Location Type | Growth Expectation | Key Value Drivers | Negotiation Leverage |

|---|---|---|---|

| Prime Central London | 3-4% | Scarcity, international demand | Moderate |

| Inner London Regeneration | 5-7% | Infrastructure, development | Lower |

| Established Suburbs | 4-5% | Schools, transport links | Moderate-High |

| Commuter Belt | 3-4% | Affordability, space | Higher |

| Regional Cities | 2-3% | Local employment, affordability | Highest |

Addressing Seller Psychology in Stabilising Markets

Understanding seller psychology is crucial when implementing negotiation strategies in 2026's stabilising market. Unlike in declining markets where sellers may be desperate, or boom markets where they're unrealistically optimistic, stabilising markets create a more balanced psychological environment.

Sellers in 2026 typically fall into several categories:

The Realistic Seller: Understands current market conditions and prices appropriately. These sellers respond well to fair offers backed by evidence. Your strategy should be straightforward presentation of data and quick decision-making to secure the property.

The Optimistic Seller: Still remembers higher prices from previous years and struggles to accept modest growth reality. These sellers need education through market data, comparable sales evidence, and time on market statistics showing that overpriced properties sit unsold.

The Reluctant Seller: Not particularly motivated to sell quickly. These sellers may accept a lower price if you can offer certainty, speed, and minimal complications. Emphasise your position as a serious, qualified buyer ready to proceed.

The Motivated Seller: Needs to sell due to relocation, divorce, or financial pressure. While ethical negotiation is essential, these sellers will respond to fair offers that provide certainty and quick completion.

"In stabilising markets, the most successful buyer negotiations combine professional valuation evidence with emotional intelligence about seller motivation. Understanding both the numbers and the people behind them creates winning outcomes."

Case Study: Successful Negotiation Using Professional Valuation

Scenario: A buyer interested in a Victorian terraced house in Battersea listed at £875,000 in early 2026.

Initial Assessment: Comparable sales suggested a fair market value of £840,000-£860,000, but the buyer commissioned a comprehensive building survey before making an offer.

Survey Findings:

- Roof requiring replacement within 2-3 years (estimated cost: £18,000)

- Damp issues in basement requiring membrane installation (estimated cost: £12,000)

- Outdated electrical system needing rewiring (estimated cost: £8,000)

- Minor structural movement requiring monitoring (no immediate cost but affecting value)

Negotiation Strategy: The buyer presented the survey findings along with contractor quotes and comparable sales data. The evidence-based approach demonstrated that:

- Market value before condition adjustments: £850,000

- Required immediate and near-term repairs: £38,000

- Adjusted fair value: £812,000

- Reasonable offer accounting for market conditions: £825,000

Outcome: The seller initially rejected the offer but received no other serious interest over three weeks. After their agent reviewed the survey and comparable data, they accepted £830,000—a £45,000 reduction from the asking price, representing more than one year's appreciation in the 4-5% growth environment.

Key Success Factors:

✓ Professional survey providing credible evidence

✓ Contractor quotes establishing concrete repair costs

✓ Comparable sales data demonstrating market reality

✓ Patient approach allowing seller time to adjust expectations

✓ Fair offer that acknowledged both issues and market value

Advanced Considerations for 2026 Property Buyers

Mortgage Valuation vs. Market Valuation

An important distinction that affects buyer negotiations is the difference between mortgage valuations and market valuations. Lenders conduct their own valuations to ensure the property provides adequate security for the loan, but these valuations serve different purposes than market valuations used for negotiation.

In 2026's stabilising market, mortgage valuers are taking more conservative approaches. After years of volatility, lenders want to ensure they're not overexposed if growth remains modest or if localised corrections occur. This creates a situation where mortgage valuations may come in below asking prices, providing buyers with additional negotiating leverage.

When a mortgage valuation comes in significantly below the agreed price, buyers have several options:

Renegotiate the price based on the lender's valuation

Increase the deposit to maintain the desired loan-to-value ratio

Challenge the valuation if you believe it's unreasonably low

Walk away if the gap is too large and the seller won't negotiate

Professional Red Book valuations follow RICS standards and are accepted by all major lenders, providing consistency and credibility in these situations.

Tax Implications and Valuation Strategies

For certain buyers, tax considerations significantly affect valuation strategies. Understanding these implications helps optimise your overall financial position beyond just the purchase price.

Stamp Duty Land Tax (SDLT): In stabilising markets, negotiating a price just below a SDLT threshold can save thousands of pounds. For example, reducing a price from £625,000 to £624,999 saves £6,250 in SDLT. Buyers should calculate these thresholds and consider them in negotiation strategies.

Capital Gains Tax (CGT) Planning: For investment properties, understanding future CGT implications affects how much you should pay today. In a low-growth environment, the CGT on eventual sale will be lower than in high-growth scenarios, which may justify a slightly higher purchase price if the property has other advantages.

Inheritance Tax (IHT) Considerations: For buyers purchasing property that may eventually form part of their estate, probate valuation methodologies provide insight into how HMRC will assess the property's value in the future.

Non-Domicile Tax Planning: For international buyers with non-domicile status, specialised non-domicile tax valuations help structure purchases to minimise tax exposure while ensuring accurate market value assessment.

New Build vs. Existing Property Valuation

The stabilising market of 2026 affects new build and existing properties differently, requiring distinct valuation and negotiation approaches.

New Build Considerations:

New build properties typically carry a premium over equivalent existing properties, but this premium has compressed in stabilising markets. Developers facing slower sales are more willing to negotiate, particularly on:

- Incentives: Help to Buy schemes, furniture packages, or stamp duty contributions

- Upgrades: Better fixtures, fittings, or specification improvements

- Price reductions: Direct discounts, particularly on final units in a development

A snagging report becomes essential for new build purchases, identifying construction defects that must be remedied before completion. In negotiations, buyers can use anticipated snagging issues as leverage for price reductions or developer-funded repairs.

Existing Property Advantages:

In a low-growth environment, existing properties often represent better value because:

- Established locations: Proven neighbourhoods with mature amenities

- Character and space: Period features and larger rooms than typical new builds

- No new build premium: Immediate value without developer profit margin

- Negotiation flexibility: Individual sellers more willing to negotiate than corporate developers

Leasehold and Shared Ownership Complexities

Valuing leasehold and shared ownership properties requires specialised knowledge, particularly in 2026's stabilising market where these complexities can significantly affect negotiating positions.

Leasehold Valuations:

The length of the lease dramatically affects property value. As a general rule, properties with leases below 80 years begin to lose value exponentially. In a 4-5% growth market, a short lease can negate years of appreciation.

Professional freehold valuation services help buyers understand:

- Current market value with the existing lease

- Marriage value if extending the lease

- Costs of lease extension and their impact on total acquisition cost

- Negotiation strategies with freeholders

For properties with short leases, buyers should negotiate the purchase price to reflect the immediate cost and complexity of lease extension.

Shared Ownership Considerations:

Shared ownership valuations require understanding both the share being purchased and the total property value. In stabilising markets, the rent charged on the unpurchased share becomes more significant as a percentage of total housing costs.

Buyers should negotiate:

- Initial share percentage: Larger shares mean less rent paid to the housing association

- Staircasing terms: Conditions for purchasing additional shares in the future

- Rent review clauses: How the rent on the unpurchased share will increase over time

Commercial Property and Mixed-Use Considerations

For buyers considering commercial or mixed-use properties, 2026's stabilising market creates unique valuation challenges and opportunities.

Commercial Valuation Factors:

Commercial property values depend heavily on rental income potential and tenant quality. In a productivity-led growth environment[4], businesses are more focused on efficient use of space, affecting commercial property demand.

Commercial dilapidation surveys identify repair obligations that may transfer to buyers, while rent review analysis helps assess whether current rental income is sustainable or likely to change.

Mixed-Use Opportunities:

Properties combining residential and commercial use often present negotiation opportunities because:

- Smaller buyer pool: Fewer buyers want mixed-use, reducing competition

- Valuation complexity: Harder to find true comparables

- Financing challenges: More difficult to obtain mortgages

Buyers who understand these complexities and can secure appropriate financing often negotiate significant discounts on mixed-use properties.

Risk Management and Due Diligence

Identifying Hidden Costs and Liabilities

In stabilising markets with modest growth, hidden costs can eliminate years of appreciation, making thorough due diligence essential for protecting your negotiating position and investment.

Structural and Building Risks:

Beyond obvious defects identified in surveys, buyers should investigate:

- Japanese knotweed: Can cost £5,000-£20,000 to treat and affects mortgageability

- Subsidence history: Even if currently stable, affects insurance costs and future saleability

- Asbestos: Common in pre-2000 properties, expensive to remove safely

- Boundary disputes: Can cost tens of thousands in legal fees to resolve

Professional boundary surveys clarify property lines and identify potential disputes before they become expensive problems.

Planning and Legal Risks:

- Unauthorised alterations: Extensions or conversions without proper planning permission

- Building regulation compliance: Work completed without required approvals

- Restrictive covenants: Limitations on property use or modifications

- Rights of way: Access rights that may affect privacy or future development

Party Wall Considerations

For terraced or semi-detached properties—common in London and surrounding areas—party wall matters can significantly affect value and should inform negotiation strategies.

Understanding Party Wall Implications:

If you plan renovations, party wall agreements may be required for:

- Loft conversions

- Basement excavations

- Shared chimney work

- Wall insulation improvements

The cost of party wall surveyors and potential party wall disputes should be factored into your valuation and negotiation strategy. If significant party wall work will be needed, this represents a legitimate basis for price negotiation.

Insurance and Reinstatement Costs

Understanding insurance implications helps buyers avoid properties with hidden ongoing costs that affect long-term affordability.

High-Risk Properties:

Certain properties carry significantly higher insurance premiums:

- Flood risk areas: Premiums can be 3-5x normal rates

- Listed buildings: Specialist insurance required at premium rates

- Non-standard construction: Timber frame, thatched roofs, etc.

- Subsidence history: Even if resolved, affects premiums for years

Reinstatement cost assessments determine the full rebuilding cost, which directly affects insurance premiums. If reinstatement costs are disproportionately high relative to market value, this indicates potential ongoing cost issues.

Market Liquidity and Exit Strategy

In a low-growth environment, market liquidity—how quickly you could sell the property if needed—becomes more important than in boom markets where everything sells rapidly.

Liquidity Factors to Assess:

- Property type popularity: Terraced houses typically sell faster than unusual layouts

- Price point: Properties at common price points have larger buyer pools

- Location desirability: Transport links, schools, amenities affect sale speed

- Condition: Properties requiring significant work have smaller buyer pools

When negotiating, consider that properties with lower liquidity deserve a valuation discount. If you might need to sell quickly in the future, this discount protects you from forced sales at unfavourable prices.

Future-Proofing Your Purchase

Climate Change and Sustainability Considerations

Looking ahead in 2026, climate change and energy efficiency increasingly affect property values and should inform valuation strategies.

Energy Performance Certificates (EPCs):

Properties with poor EPC ratings (E, F, or G) face increasing challenges:

- Rental restrictions: Minimum EPC requirements for rental properties

- Mortgage availability: Some lenders restricting loans on inefficient properties

- Buyer demand: Younger buyers particularly focused on sustainability

- Improvement costs: Upgrading from G to C can cost £20,000-£50,000+

Buyers should negotiate price reductions for properties requiring substantial energy efficiency improvements, as these costs will be necessary to maintain marketability.

Flood Risk and Climate Resilience:

With climate change increasing flood risk in many areas, properties in flood zones require careful valuation adjustment. Insurance costs, potential damage, and increasing buyer awareness all affect long-term value.

Technology and Smart Home Integration

The productivity-led growth characterising 2026[4] extends to residential property, where technology integration increasingly affects desirability and value.

Technology Value Factors:

- Broadband infrastructure: Fibre availability essential for home working

- Smart home systems: Integrated heating, security, lighting add value

- EV charging: Properties with charging points command premiums

- Solar panels and battery storage: Reduce running costs and increase appeal

When negotiating, consider whether the property can accommodate modern technology needs or whether significant upgrades will be required.

Demographic Trends and Long-Term Demand

Understanding demographic trends helps buyers assess whether a property will remain in demand as the market evolves.

Key 2026 Demographic Factors:

- Aging population: Increased demand for single-level living, accessible properties

- Home working: Continued importance of home office space

- Smaller households: Growing demand for one and two-bedroom properties

- Multigenerational living: Interest in properties with annexe potential

Properties aligned with these trends are more likely to maintain value in low-growth environments, while properties that don't meet evolving needs may underperform.

Conclusion: Mastering Valuation in Stabilising Markets

Valuing Stabilising Markets: Low Single-Digit Growth Strategies for 2026 Buyer Negotiations represents a fundamental shift in how property buyers should approach the market. The days of relying on rapid appreciation to correct overpayment are gone—in a 4-5% growth environment, precision in valuation and negotiation directly determines investment success.

The key insights for 2026 buyers are clear:

Professional valuation is non-negotiable 📋

In modest growth markets, the margin for error is too small to rely on amateur assessments. RICS-accredited surveyors provide the evidence-based valuations that support successful negotiations and protect against overpayment.

Regional knowledge trumps national statistics 🏘️

While national growth averages around 4-5%, your specific property's location may experience significantly different conditions. Local surveyor expertise in areas from Barnes to Hampstead provides the granular knowledge that generic data cannot.

Data-driven negotiation wins 📊

Sellers in stabilising markets respond to evidence, not emotion. Comprehensive survey reports, comparable sales analysis, and repair cost documentation create negotiating positions that sellers must take seriously.

Hidden costs matter more 💷

When appreciation is modest, unexpected expenses like party wall agreements, energy efficiency upgrades, or lease extensions can eliminate years of gains. Thorough due diligence protects your investment.

Timing and patience pay dividends ⏰

In a market growing at 4-5% annually, waiting an extra month for the right property at the right price costs less than rushing into an overpriced purchase that takes years to recover.

Actionable Next Steps

For buyers preparing to navigate 2026's stabilising property market:

1. Commission professional valuations early

Don't wait until you've fallen in love with a property. Understand valuation methodologies and establish relationships with qualified surveyors before you need them urgently.

2. Build your evidence base

Collect comparable sales data, understand local market trends, and familiarise yourself with recent transaction prices (not asking prices) in your target areas.

3. Secure mortgage agreement in principle

Understanding your borrowing capacity and having lender approval strengthens your negotiating position and speeds the transaction process.

4. Calculate your walk-away point

Before making offers, determine the maximum price you'll pay based on objective valuation, not emotional attachment. Stick to this limit.

5. Engage specialist advisors for complex situations

For leasehold properties, new builds, commercial elements, or tax planning scenarios, engage specialists who understand these nuances.

6. Plan for the long term

In low-growth markets, short-term speculation rarely succeeds. Buy properties you'd be happy to own for 7-10 years, ensuring you can weather any temporary market fluctuations.

The 2026 property market rewards informed, patient buyers who understand that accurate valuation and skilled negotiation are more valuable than ever. By applying the strategies outlined in this guide and leveraging professional surveyor expertise, buyers can secure properties at fair prices that provide sustainable long-term value—even in an environment of modest, single-digit growth.

The stabilising market isn't a limitation—it's an opportunity for strategic buyers who do their homework, present evidence-based cases, and negotiate with confidence backed by professional valuation expertise.

References

[1] Solving – https://www.nb.com/en/global/solving

[2] 2026 Macro And Private Markets Outlook Sustained Resilience – https://www.icgam.com/2026/01/23/2026-macro-and-private-markets-outlook-sustained-resilience/

[3] Investment Strategy Insights Assessing Scenarios For Our 2026 Outlook – https://www.pinebridge.com/en/insights/investment-strategy-insights-assessing-scenarios-for-our-2026-outlook

[4] 2026 Investing Outlook Navigating Uncertainty In A Changing Market – https://www.onedayinjuly.com/2026-investing-outlook-navigating-uncertainty-in-a-changing-market

[7] 2026 Us Business Leaders Outlook – https://www.jpmorgan.com/insights/markets-and-economy/business-leaders-outlook/2026-us-business-leaders-outlook