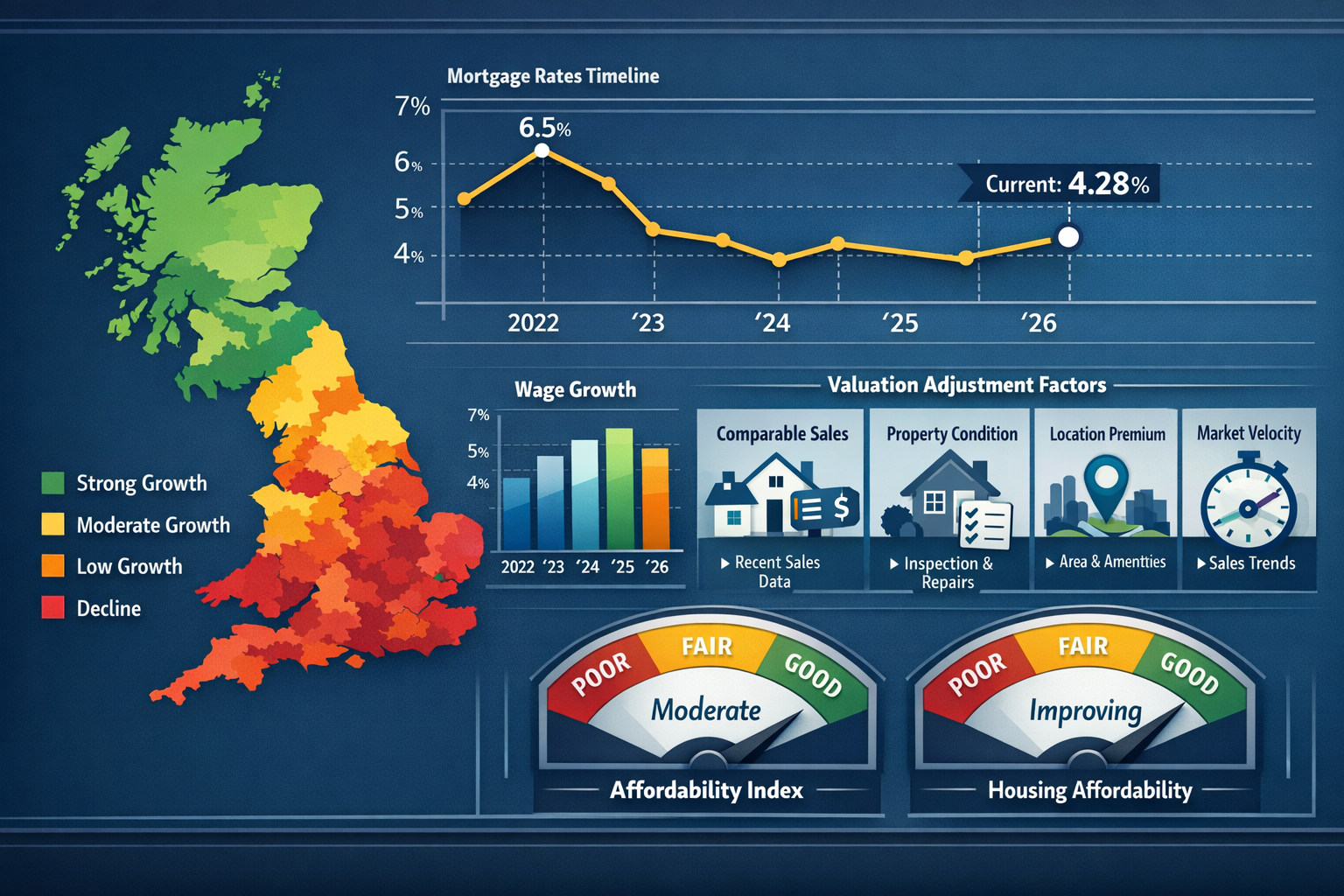

The UK property market has entered 2026 with renewed optimism after years of uncertainty, yet surveyors face a delicate balancing act. With asking prices hitting £368,019 in February 2026 and mortgage rates dropping to their lowest levels since September 2022, the market is showing signs of stabilisation—but not uniformity[2]. As regional variations intensify and buyer behaviour shifts in response to improved affordability, valuing UK properties in a recovering 2026 market demands precision, adaptability, and a deep understanding of the evolving economic landscape.

Professional surveyors must now navigate a complex terrain where 2% growth forecasts from major lenders mask significant regional disparities, where rising buyer enquiries don't always translate to completed sales, and where easing mortgage rates compete with lingering economic caution. The RICS January 2026 survey data reveals a market in transition—one that requires surveyors to employ sophisticated strategies that account for northern versus southern price dynamics, wage growth patterns, and the psychological impact of recent policy changes.

Key Takeaways

- 📊 February 2026 prices remained virtually flat at £368,019, following the strongest January growth since 2020 (2.8% increase), indicating market stabilisation after post-Budget recovery[2]

- 💰 Mortgage rates have improved significantly to 4.28% for two-year fixed products, down from 4.96% a year earlier, creating improved affordability conditions for buyers[2]

- 🏘️ Regional variations require differentiated valuation approaches, with northern markets showing different momentum compared to southern regions based on RICS survey data

- 📈 Major forecasters predict modest 2% growth for 2026, with Nationwide (2-4%), Halifax (1-3%), and Savills (around 2%) providing consensus guidance for valuation benchmarks[3][5]

- 🔧 Surveyors must integrate multiple data sources including wage growth, buyer enquiry trends, inventory levels, and comparative market analysis to deliver accurate, market-aligned valuations

Understanding the 2026 UK Property Market Recovery Context

The UK property market's journey into 2026 reflects a narrative of cautious optimism built on improving fundamentals. After experiencing the turbulence of 2022's mini-budget crisis and the subsequent interest rate surge, the market has found firmer footing as mortgage rates retreat from their peaks.

The January Surge and February Stabilisation

The 2.8% increase in asking prices during January 2026 represented the largest January jump on record, signalling pent-up demand and seller confidence returning after the November 2025 Autumn Budget uncertainty[2]. This remarkable start to the year demonstrated that when economic conditions align—even modestly—the UK property market can respond with vigour.

However, February's virtual standstill (down just £12 or -0.0%) tells an equally important story[2]. This pause reflects:

- Price sensitivity among buyers who remain cautious despite improved mortgage rates

- High inventory levels creating competitive pressure among sellers

- Strategic seller behaviour where homeowners are consolidating January gains rather than pushing for further increases

- Subdued buying activity compared to the same period in previous years

For surveyors conducting valuations, this pattern suggests a market that has found a temporary equilibrium—neither surging ahead nor retreating, but consolidating recent gains.

Mortgage Rate Improvements Driving Affordability

The decline in two-year fixed mortgage rates to 4.28% in February 2026 from 4.96% a year earlier represents a substantial improvement in affordability[2]. While current rates remain elevated compared to the ultra-low environment of 2020-2021, they mark a significant retreat from the peaks experienced in late 2022 and early 2023.

| Mortgage Product | February 2026 Rate | Year Earlier Rate | Change |

|---|---|---|---|

| Two-Year Fixed | 4.28% | 4.96% | -0.68% |

| Five-Year Fixed | 4.94% | ~5.2% | ~-0.26% |

| Average UK Rate | 4.91% | ~5.3% | ~-0.39% |

These rate improvements translate directly into enhanced purchasing power for buyers. For a £300,000 mortgage, the difference between a 4.96% and 4.28% rate equates to approximately £120 per month in savings—a meaningful reduction that expands the pool of qualified buyers and supports property values.

Professional chartered surveyors in London must factor these affordability improvements into their valuation models, recognising that properties previously priced out of reach for many buyers may now attract renewed interest.

Regional Disparities in Market Performance

The RICS January 2026 survey data reveals significant regional variations that challenge the notion of a uniform national market. While aggregate statistics show stabilisation, the underlying dynamics differ markedly between northern and southern regions.

Northern England has demonstrated:

- Stronger buyer enquiry levels relative to inventory

- More resilient price growth supported by better affordability ratios

- Continued interest from first-time buyers accessing improved mortgage products

- Less dramatic price corrections from 2022 peaks

Southern England and London have experienced:

- Higher price sensitivity due to elevated absolute property values

- Slower recovery in buyer enquiries despite rate improvements

- Greater inventory accumulation creating buyer leverage

- More pronounced impact from stamp duty considerations

These regional differences necessitate differentiated valuation approaches. A chartered surveyor in Surrey must apply different adjustment factors compared to colleagues working in Hertfordshire or Sussex, even when properties share similar characteristics.

Surveyor Strategies for Valuing UK Properties in a Recovering 2026 Market

Professional property valuation in 2026 requires surveyors to move beyond simple comparable sales analysis and embrace a multi-dimensional approach that accounts for market velocity, affordability dynamics, and regional variations. The following strategies enable accurate pricing aligned with current market realities.

Implementing Dynamic Comparable Sales Analysis

Traditional comparable sales analysis remains foundational, but valuing UK properties in a recovering 2026 market demands enhanced sophistication in selecting and adjusting comparables.

Time-Adjusted Comparables

Given the January surge and February stabilisation pattern, surveyors must apply careful time adjustments to comparable sales. Properties that sold in December 2025 may require upward adjustments of approximately 2.8% to reflect January's growth, while February sales may need minimal or no adjustment depending on property type and location[2].

Best practices include:

- ✅ Prioritising comparables from the most recent 3-month period to capture current market sentiment

- ✅ Applying monthly adjustment factors based on local market data rather than assuming linear annual growth

- ✅ Weighting recent comparables more heavily in final valuation calculations

- ✅ Documenting the rationale for time adjustments in valuation reports

Location-Specific Premium Adjustments

The recovering market has amplified the importance of micro-location factors. Properties in areas with:

- Superior transport links (particularly Elizabeth Line accessibility)

- High-quality school catchments

- Green space proximity

- Low crime rates

…command premiums that have widened during the recovery period as buyers prioritise quality over quantity.

Surveyors conducting valuations in Richmond or Kingston must quantify these premiums through detailed comparative analysis of similar properties in adjacent, less desirable locations.

Integrating Mortgage Rate Impact on Buyer Capacity

The improvement in mortgage rates to 4.28% for two-year fixed products fundamentally alters buyer purchasing power[2]. Surveyors must understand how this translates into property valuations through affordability-driven demand.

Affordability Ratio Analysis

Professional valuations should incorporate affordability ratio calculations that assess:

- Local average earnings relative to property asking prices

- Mortgage payment-to-income ratios at current lending rates

- Deposit requirements and their impact on buyer pool size

- Stress test rates applied by lenders (typically 1-2% above product rate)

For example, in areas where average household income is £50,000:

- At 4.28% mortgage rate, a buyer can typically afford a property of approximately £225,000 (4.5x income multiplier with 10% deposit)

- At the previous 4.96% rate, the same buyer's capacity was approximately £215,000

- This £10,000 increase in purchasing power supports modest price growth in the £200,000-£250,000 segment

Surveyors should adjust valuations upward for properties that have entered affordability range for larger buyer pools due to rate improvements, while remaining cautious about properties at the upper end of affordability thresholds.

Factoring Wage Growth and Economic Indicators

The 2026 market recovery occurs against a backdrop of moderate wage growth that supports property values through improved buyer capacity. Surveyors must integrate these macroeconomic factors into valuation frameworks.

Real Income Growth Considerations

When nominal wage growth exceeds inflation, real income growth enhances buyer purchasing power even without mortgage rate changes. Current economic data suggests:

- Nominal wage growth of approximately 4-5% annually

- Inflation running at approximately 2-3%

- Real wage growth of approximately 1-2%

This real income improvement supports the 2% property price growth forecasts from major lenders[3][5], creating a sustainable foundation for modest appreciation rather than speculative gains.

"The 2026 market is characterised by fundamentals-driven growth rather than speculative exuberance. Wage growth, improved mortgage rates, and stabilising buyer confidence create conditions for sustainable, modest appreciation that surveyors can confidently incorporate into valuations." – Industry Analysis

Employment Stability and Regional Economic Health

Surveyors should assess local employment conditions when valuing properties, particularly in regions dependent on specific industries. Areas with:

- Diverse employment bases support more stable property values

- Growing sectors (technology, professional services, healthcare) attract buyers with higher incomes

- Declining industries face headwinds that may suppress values despite national trends

Professional commercial property surveyors in London regularly analyse employment data as part of valuation methodology—residential surveyors should adopt similar practices.

Applying RICS Red Book Standards in Uncertain Markets

The RICS Valuation – Global Standards (Red Book) provides the professional framework for all property valuations, but applying these standards during market transitions requires careful judgment.

Market Value Definition and Assumptions

The Red Book defines Market Value as:

"The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

In the 2026 recovering market, surveyors must carefully consider:

- "Proper marketing" timeframes may be extending as buyer activity remains subdued compared to historical norms[2]

- "Willing buyer" availability varies significantly by price point and region

- "Knowledgeable" parties may have different expectations about future price movements

Surveyors should document their assumptions about marketing periods, buyer motivation, and market conditions explicitly in valuation reports to provide transparency and professional defensibility.

Special Assumptions and Departures

When market conditions create uncertainty, surveyors may need to employ special assumptions or departures from Red Book standards (with appropriate disclosure). Common scenarios in 2026 include:

- Valuing properties with limited comparable evidence due to low transaction volumes

- Assessing properties in rapidly changing micro-markets where recent sales may not reflect current conditions

- Valuing unique properties where standardised approaches prove inadequate

All special assumptions must be clearly stated, justified, and their impact on the valuation explained. For complex cases, surveyors may recommend Red Book valuations with detailed commentary on market uncertainties.

Advanced Valuation Techniques for Accurate Pricing in 2026

Beyond fundamental approaches, professional surveyors can employ advanced techniques that enhance accuracy when valuing UK properties in a recovering 2026 market characterised by regional variations and evolving buyer behaviour.

Hedonic Pricing Models for Property Characteristics

Hedonic pricing models decompose property values into constituent characteristics, allowing surveyors to quantify the specific contribution of each feature to overall value. This approach proves particularly valuable in transitional markets where buyer preferences shift.

Key Variables in Hedonic Analysis

Modern hedonic models for UK residential properties typically include:

Structural Characteristics:

- Square footage (£ per square foot varies by region and property type)

- Number of bedrooms and bathrooms

- Property age and construction quality

- Energy Performance Certificate (EPC) rating

- Outdoor space (gardens, balconies, terraces)

- Parking availability

Location Factors:

- Distance to transport links

- School quality ratings

- Crime statistics

- Green space proximity

- Retail and amenity accessibility

Market Timing Variables:

- Seasonal effects

- Local market velocity

- Days on market trends

- Buyer enquiry levels

By quantifying these variables through regression analysis of recent sales data, surveyors can generate property-specific valuations that account for unique combinations of features rather than relying solely on crude comparable adjustments.

Market Velocity and Absorption Rate Analysis

Market velocity—the speed at which properties sell—provides crucial context for valuations in the recovering 2026 market. Properties in fast-moving markets can sustain higher asking prices, while those in slow markets require conservative pricing.

Calculating Absorption Rates

The absorption rate measures how quickly available inventory would sell at current sales pace:

Absorption Rate = Current Inventory ÷ Average Monthly Sales

For example:

- If a local market has 120 properties listed for sale

- And 10 properties sell per month on average

- The absorption rate is 12 months

Interpretation for valuations:

- 0-3 months: Seller's market—properties may achieve or exceed asking prices

- 4-6 months: Balanced market—asking prices generally achieved with modest negotiation

- 7-12 months: Buyer's market—properties may sell below asking prices

- 12+ months: Strongly buyer-favoured—significant discounting likely required

Surveyors should adjust valuations downward in high-absorption (slow) markets and may support premium pricing in low-absorption (fast) markets, particularly when combined with rising buyer enquiry data from RICS surveys.

Scenario-Based Valuation Approaches

Given the uncertainty inherent in any market recovery, scenario-based valuations provide clients with a range of potential outcomes rather than a single point estimate.

Three-Scenario Framework

Professional surveyors can present valuations under three scenarios:

Optimistic Scenario (Probability: 25-30%):

- Mortgage rates continue declining to 3.5-4.0%

- Wage growth accelerates to 5-6%

- Buyer confidence strengthens significantly

- Implied annual appreciation: 3-4%

Base Case Scenario (Probability: 50-60%):

- Mortgage rates stabilise around 4.0-4.5%

- Wage growth continues at 4-5%

- Buyer activity remains steady but cautious

- Implied annual appreciation: 2% (aligned with consensus forecasts)[3][5]

Pessimistic Scenario (Probability: 15-20%):

- Economic headwinds emerge (recession, unemployment rise)

- Mortgage rates increase due to inflation concerns

- Buyer confidence deteriorates

- Implied annual appreciation: 0% to -2%

This approach, commonly used for probate valuations and matrimonial valuations, provides stakeholders with realistic expectations and supports informed decision-making.

Technology-Enhanced Valuation Tools

Modern surveyors can leverage technology to enhance accuracy and efficiency when valuing UK properties in a recovering 2026 market.

Automated Valuation Models (AVMs) as Supporting Evidence

While AVMs should never replace professional judgment, they provide useful supporting data, particularly for:

- Initial valuation ranges before detailed inspection

- Comparable property identification across wider geographic areas

- Market trend analysis showing price movements over time

- Quality assurance checks against professional valuations

Leading AVMs incorporate:

- Land Registry transaction data

- Property characteristics databases

- Postcode-level market trends

- Machine learning algorithms that improve over time

Surveyors should use AVMs as one input among many, particularly valuable for identifying outliers or confirming preliminary assessments.

Geographic Information Systems (GIS) for Location Analysis

GIS technology enables sophisticated location analysis that quantifies proximity benefits and environmental factors:

- Transport accessibility mapping showing walking times to stations

- School catchment overlays with performance ratings

- Flood risk visualisation from Environment Agency data

- Planning application tracking showing development activity

- Crime heat mapping from police data

By integrating GIS analysis into valuation reports, surveyors provide clients with visual, data-driven evidence supporting location-based adjustments. This proves particularly valuable for expert witness reports where valuation methodology must withstand scrutiny.

Regional Considerations: Northern vs Southern Market Dynamics

The RICS January 2026 survey data highlights significant regional variations that demand differentiated approaches when valuing UK properties in a recovering 2026 market. Understanding these dynamics enables surveyors to apply appropriate adjustments and provide accurate, market-aligned valuations.

Northern England: Stronger Fundamentals and Affordability

Northern regions including Yorkshire, the North West, and North East have demonstrated relatively stronger market fundamentals in the 2026 recovery period.

Key Characteristics of Northern Markets

Affordability Advantages:

- Average property prices of £180,000-£250,000 remain accessible to median-income households

- Mortgage payment-to-income ratios typically range from 25-35%, well within sustainable levels

- First-time buyer activity remains robust, supported by improved mortgage rates[2]

Employment and Wage Growth:

- Public sector employment provides stability in many northern cities

- Technology and digital sectors growing in Manchester, Leeds, and Newcastle

- Wage growth often matching or exceeding national averages in urban centres

Market Velocity:

- Properties typically selling within 6-10 weeks in desirable areas

- Buyer enquiry levels showing consistent growth through early 2026

- Lower inventory levels relative to demand compared to southern regions

Valuation Strategies for Northern Properties

When valuing properties in northern markets, surveyors should:

- Apply modest positive adjustments (0.5-1.5% quarterly) reflecting stronger local demand dynamics

- Emphasise location premiums for properties in regeneration areas or near major transport improvements

- Consider first-time buyer appeal as a value driver, particularly for properties under £250,000

- Factor in rental yield potential as buy-to-let investors increasingly target northern markets

Professional chartered surveyors in areas like Hertfordshire working on northern properties must ensure they're using genuinely comparable evidence rather than extrapolating from southern market dynamics.

Southern England and London: Price Sensitivity and Stabilisation

Southern regions including London, the South East, and South West face different dynamics characterised by higher absolute prices and greater price sensitivity.

Key Characteristics of Southern Markets

Affordability Challenges:

- Average property prices of £400,000-£700,000 (London significantly higher)

- Mortgage payment-to-income ratios often exceeding 40% for median-income households

- Dependence on dual-income households and parental support for deposits

Economic Drivers:

- Financial services and professional sectors provide high-income employment but face hybrid working pressures

- Commuter patterns shifting as hybrid work reduces premium for proximity to central London

- International buyer activity remains subdued compared to pre-Brexit levels

Market Velocity:

- Properties taking 10-16 weeks to sell in many areas

- Higher inventory levels creating buyer leverage

- Greater negotiation on asking prices (typically 3-5% below initial asking)

Valuation Strategies for Southern Properties

When valuing properties in southern markets, surveyors should:

- Apply conservative adjustments reflecting price sensitivity and longer marketing periods

- Discount for properties exceeding local affordability thresholds by 5-10%

- Premium for properties with home office potential as hybrid working becomes permanent

- Consider transport link improvements (Elizabeth Line, HS2) as significant value drivers

Surveyors working in West London, South West London, or areas like Fulham and Putney must account for micro-market variations within broader regional trends.

Commuter Belt and Home Counties: Hybrid Work Impact

The commuter belt regions including Surrey, Buckinghamshire, Oxfordshire, and Sussex occupy a middle ground with unique valuation considerations.

Evolving Value Drivers

Hybrid Working Effects:

- Properties offering home office space command 5-15% premiums

- Garden and outdoor space values sustained from pandemic period

- Station proximity less critical than previously, with buyers accepting longer commutes for fewer days

School Catchment Premiums:

- Outstanding-rated schools driving 10-20% premiums in immediate catchment

- Grammar school access in selective areas (Buckinghamshire) creating significant value differentiation

- Private school accessibility influencing buyer decisions in affluent areas

Lifestyle Amenities:

- Village locations with amenities (shops, pubs, community facilities) outperforming isolated properties

- Green space access (National Trust properties, Areas of Outstanding Natural Beauty) supporting values

- Market town proximity providing balance between rural and urban benefits

Surveyors conducting valuations in Buckinghamshire, Oxfordshire, or Surrey must carefully assess these hybrid-work-era value drivers through detailed comparable analysis.

Practical Implementation: Case Studies and Examples

Understanding theoretical approaches to valuing UK properties in a recovering 2026 market becomes most valuable when applied to practical scenarios. The following case studies illustrate how surveyors can implement these strategies.

Case Study 1: Victorian Terrace in Richmond (£850,000)

Property Characteristics:

- 3-bedroom Victorian terrace

- 1,400 sq ft

- Recently renovated kitchen and bathroom

- Small rear garden (30 ft)

- 10-minute walk to Richmond station

- Outstanding-rated primary school catchment

Valuation Approach:

The surveyor identified five comparable sales from December 2025-February 2026 ranging from £810,000 to £880,000. Key adjustments included:

- +2.8% time adjustment for December comparable (January surge)[2]

- +£25,000 for renovation quality compared to un-updated comparables

- +£15,000 for school catchment (one comparable outside catchment)

- -£10,000 for smaller garden compared to one comparable with 45 ft garden

Final Valuation: £850,000 (mid-range of adjusted comparables)

Rationale: Richmond's strong fundamentals (transport, schools, amenities) support premium pricing, but the broader London market price sensitivity prevents significant appreciation above recent comparables. The valuation reflects current market equilibrium in this micro-market.

Case Study 2: New-Build Apartment in Manchester (£235,000)

Property Characteristics:

- 2-bedroom new-build apartment

- 750 sq ft

- Fifth floor with balcony

- City centre location

- 5-minute walk to Piccadilly station

- Help to Buy eligible

Valuation Approach:

Limited resale comparables required the surveyor to use a combination of:

- Developer pricing for similar units in the same development (£240,000-£250,000)

- Resale comparables from nearby developments (£220,000-£245,000)

- £ per square foot analysis (£313/sq ft average for comparable new-builds)

- Affordability analysis confirming strong demand at this price point (accessible to £52,000 household income at 4.28% mortgage rate)[2]

Final Valuation: £235,000 (conservative within range)

Rationale: Strong northern market fundamentals and first-time buyer demand support new-build premiums, but the surveyor applied a conservative approach given potential oversupply of city centre apartments and the need for the valuation to hold through the typical 8-12 week purchase period.

Case Study 3: Period Cottage in Oxfordshire (£625,000)

Property Characteristics:

- 4-bedroom detached period cottage

- 2,100 sq ft

- Character features (beams, inglenook fireplace)

- Large garden (0.3 acres)

- Village location with amenities

- 15-minute drive to Oxford

- Dedicated home office/study

Valuation Approach:

The surveyor employed a hedonic pricing model to quantify specific features:

- Base value for location: £450,000 (4-bed detached in this village)

- Period features premium: +£50,000 (15-20% for authentic character)

- Large garden premium: +£75,000 (significant in this market)

- Home office value: +£30,000 (hybrid working driver)

- Condition adjustments: +£20,000 (recent updates to heating, windows)

Final Valuation: £625,000

Rationale: The home office feature and garden size align perfectly with hybrid-working buyer priorities in the commuter belt. The surveyor's hedonic approach provided transparent justification for the premium over standard 4-bed comparables, supported by evidence of similar period properties with these features achieving comparable prices.

Risk Factors and Mitigation Strategies

Professional surveyors must identify and communicate potential risks that could affect valuations when valuing UK properties in a recovering 2026 market characterised by evolving economic conditions.

Economic Uncertainty and Interest Rate Volatility

Risk: Mortgage rates could increase if inflation proves persistent or economic conditions deteriorate, reducing buyer purchasing power and suppressing property values.

Mitigation Strategies:

- Include sensitivity analysis in valuation reports showing value impact of 0.5% and 1.0% rate increases

- Recommend shorter marketing periods to reduce exposure to rate changes

- Consider conservative valuations for properties at upper affordability thresholds

- Document assumptions about interest rate stability in valuation reports

Regional Economic Divergence

Risk: Regional economic performance may diverge significantly from national trends, particularly if specific industries face headwinds or local employment conditions deteriorate.

Mitigation Strategies:

- Conduct local employment analysis as part of valuation methodology

- Monitor regional RICS survey data for early warning signs of market weakening

- Apply regional-specific growth assumptions rather than national averages

- Maintain conservative approaches in regions dependent on vulnerable industries

Policy Changes and Regulatory Shifts

Risk: Government policy changes (stamp duty, planning regulations, energy efficiency requirements) could materially affect property values.

Mitigation Strategies:

- Monitor policy announcements and incorporate known changes into valuations

- Consider EPC rating impact on value, particularly for lower-rated properties facing future regulatory pressure

- Account for planning policy changes that might affect development potential

- Include policy risk disclaimers in valuation reports where uncertainty exists

Market Liquidity and Transaction Volume

Risk: Low transaction volumes create limited comparable evidence and potential for valuation inaccuracy.

Mitigation Strategies:

- Expand geographic search radius for comparables when local evidence is limited

- Use multiple valuation methodologies (comparables, hedonic models, investment approach) for cross-validation

- Apply wider valuation ranges to reflect increased uncertainty

- Recommend professional marketing to test market appetite when evidence is thin

Professional building surveyor services increasingly incorporate these risk assessments into comprehensive valuation reports, providing clients with realistic expectations and supporting informed decision-making.

Future-Proofing Valuations: Looking Beyond 2026

While this article focuses on valuing UK properties in a recovering 2026 market, professional surveyors must also consider medium-term trends that will affect property values through the remainder of the decade.

Sustainability and Energy Efficiency

EPC ratings will increasingly influence property values as:

- Regulatory pressure increases on landlords (minimum EPC C likely for rentals by 2028)

- Buyer awareness of energy costs grows

- Mortgage products begin offering preferential rates for energy-efficient properties

- Retrofit costs for improvement become more transparent

Valuation Impact: Properties with EPC ratings of A-C may command 5-10% premiums over comparable D-G rated properties by 2027-2028, particularly in the rental sector.

Climate Risk and Flood Resilience

Climate change impacts will become more prominent in valuation considerations:

- Flood risk areas facing insurance challenges and potential value discounts

- Overheating risk in poorly designed properties affecting desirability

- Extreme weather resilience becoming a buyer consideration

Valuation Impact: Properties in Flood Zone 3 may face 10-20% discounts as insurance costs rise and buyer awareness increases. Surveyors should incorporate flood risk assessments into standard valuation methodology.

Demographic Shifts and Housing Preferences

Aging population and changing household composition will influence demand:

- Single-person households increasing, driving demand for 1-2 bed properties

- Downsizing demand from baby boomers supporting bungalow and ground-floor apartment values

- Multi-generational living increasing, creating demand for flexible accommodation

Valuation Impact: Properties offering adaptability (ground-floor bedrooms, potential for annexes, flexible spaces) may command premiums as demographic pressures intensify.

Conclusion: Navigating the 2026 Recovery with Confidence

Valuing UK properties in a recovering 2026 market requires professional surveyors to balance optimism about improving fundamentals with realism about persistent challenges. The 2% growth forecasts from major lenders reflect a market finding sustainable equilibrium after years of volatility—neither boom nor bust, but steady, fundamentals-driven appreciation[3][5].

The strategies outlined in this comprehensive guide—from dynamic comparable sales analysis and affordability ratio calculations to hedonic pricing models and regional differentiation—equip surveyors with the tools necessary for accurate, defensible valuations. The 4.28% mortgage rates and modest wage growth create conditions supporting property values, but regional variations demand localised expertise rather than one-size-fits-all approaches[2].

Actionable Next Steps for Professional Surveyors

-

Update your comparable databases monthly to capture the evolving market dynamics and ensure time adjustments reflect current conditions

-

Integrate affordability analysis into standard valuation methodology, calculating buyer capacity at current mortgage rates for different property price points

-

Develop regional expertise by monitoring RICS survey data, local employment trends, and micro-market absorption rates for your primary operating areas

-

Enhance reporting standards by incorporating sensitivity analysis, risk factors, and scenario-based valuations that provide clients with comprehensive market context

-

Invest in technology tools including GIS systems, hedonic pricing models, and AVM platforms that support (but don't replace) professional judgment

-

Maintain professional development through RICS CPD requirements, focusing on emerging areas like sustainability valuation, climate risk assessment, and technology applications

-

Build collaborative networks with other property professionals—estate agents, mortgage brokers, planning consultants—to access diverse market intelligence

The UK property market's 2026 recovery presents both opportunities and challenges for professional surveyors. Those who embrace sophisticated valuation methodologies, maintain rigorous professional standards, and communicate transparently with clients will navigate this environment successfully, providing the accurate, market-aligned valuations that underpin sound property decisions.

Whether you're seeking expert surveyor advice for a specific valuation challenge or require comprehensive valuation services across London and the South East, the principles outlined in this guide provide a robust framework for professional practice in 2026's recovering market.

References

[1] Uk House Prices Hold Steady In February After Bumper Start To 2026 – https://global.morningstar.com/en-gb/news/alliance-news/1771200097476297000/uk-house-prices-hold-steady-in-february-after-bumper-start-to-2026

[2] House Price Index – https://www.rightmove.co.uk/news/house-price-index/

[3] Whats Outlook Uk House Prices 2026 – https://global.morningstar.com/en-gb/personal-finance/whats-outlook-uk-house-prices-2026

[4] Value Of Uk Housing Continue Upward Trend But Rate Of Increase Slows – https://bebeez.eu/2026/02/16/value-of-uk-housing-continue-upward-trend-but-rate-of-increase-slows/

[5] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/