The British property market is experiencing a significant shift in 2026. As mortgage rates ease from their recent peaks, prospective buyers are returning to the market with renewed confidence—but also heightened caution. The Impact of Falling Mortgage Rates on 2026 Building Surveys: Pre-Purchase Checks for Buyer Confidence represents a fundamental change in how buyers approach property purchases. With more favorable financing conditions drawing buyers back into the market, the scrutiny applied to property condition has intensified dramatically. 🏠

This resurgence in buyer activity, fueled by mortgage rates hovering around 6% to 6.2% for 30-year fixed mortgages, has created a price-sensitive market where every defect matters.[2][3] Buyers who previously accepted properties "as-is" during the competitive peak years are now demanding comprehensive building surveys to justify their investment. The Royal Institution of Chartered Surveyors (RICS) has reported substantial improvements in property enquiries as rates have eased, but this increased activity comes with a critical caveat: buyers are more informed, more cautious, and more demanding of detailed pre-purchase assessments than ever before.

Key Takeaways

- Mortgage rates projected at 6-6.2% in 2026 are driving increased buyer enquiries, with the Federal Reserve expected to make two 25 basis point rate cuts throughout the year[3][4]

- Building survey demand has surged as price-sensitive buyers leverage improved affordability to negotiate based on property defects and condition issues

- RICS checklists have been updated for 2026 to address critical areas including damp penetration, energy efficiency standards, and structural risks that directly impact property valuations

- Approximately 40% of builders are cutting prices and offering incentives, creating a buyer's market where comprehensive surveys provide crucial negotiating leverage[2]

- Inventory improvements of 8.9% projected for 2026 mean buyers have more options and time to conduct thorough due diligence before committing to purchases[3]

Understanding the 2026 Mortgage Rate Landscape and Its Market Impact

Current Rate Projections and Federal Reserve Policy

The mortgage rate environment in 2026 represents a welcome relief from the elevated rates that characterized 2023-2025. Multiple authoritative forecasts project 30-year fixed mortgage rates will stabilize in the 6% to 6.2% range throughout 2026.[2][3][4] Fannie Mae's economic outlook forecasts rates at approximately 6% for most of the year, while the National Association of Home Builders predicts an average of 6.17%.[4][7]

Recent market movements have demonstrated the immediate impact of policy interventions. The 30-year fixed mortgage rate dropped 13 basis points to 6.2% following the announcement of $200 billion in mortgage-backed securities buybacks by Fannie Mae and Freddie Mac.[3] This government-sponsored enterprise intervention signals a commitment to maintaining accessible financing conditions.

The Federal Reserve's monetary policy trajectory plays a crucial role in these projections. The Fed is expected to implement two 25 basis point rate cuts in 2026, bringing the terminal federal funds rate to 3.25% by year-end.[3] However, industry experts caution that sustained sub-6% mortgage rates are unlikely until 2027, tempering expectations for dramatic rate declines.

Builder Sentiment and Market Dynamics

The psychological shift in the market is perhaps as significant as the numerical rate changes. The share of builders viewing high interest rates as a serious problem has declined substantially from 84% in 2025 to 65% in 2026—a 19-percentage-point drop reflecting improved market sentiment.[1][5][8]

This cautious optimism, as characterized by the National Association of Home Builders, comes with important caveats. Builders continue facing significant challenges beyond interest rates, including:

- 81% of buyers expecting prices or interest rates to decline further (creating hesitation in purchase decisions)

- 65% concerned about employment and economic conditions (affecting buyer confidence)

- 63% facing cost and availability issues with developed lots (limiting new construction)

- 62% noting negative media reports making buyers cautious (dampening market enthusiasm)[1]

These persistent challenges mean that while falling rates are creating opportunities, they're also creating a more discerning, cautious buyer pool that demands comprehensive property assessments before committing.

The Direct Connection Between Rate Improvements and Building Survey Demand

Why Falling Rates Intensify Survey Scrutiny

The relationship between mortgage rates and building survey demand might seem counterintuitive at first. One might expect that easier financing conditions would make buyers less concerned about property defects. The reality in 2026 is precisely the opposite.

Improved affordability creates negotiating power. For the first time since 2020, monthly mortgage payments are projected to account for less than 30% of household income—a key affordability benchmark that signals a healthier market.[2][6] This improved affordability doesn't translate to buyers accepting lower-quality properties; instead, it empowers them to be more selective and demanding.

When buyers have breathing room in their budgets, they can afford to:

✅ Walk away from properties with significant defects

✅ Negotiate price reductions based on survey findings

✅ Request repairs before completion

✅ Factor remediation costs into their offers

The shift from a seller's market to a more balanced market fundamentally changes the leverage dynamic. With inventory increasing 8.9% in 2026 and months' supply reaching 4.6 months (within the balanced market range of 4-6 months), buyers no longer feel pressured to waive contingencies or accept properties without thorough inspection.[3]

The Price Sensitivity Factor

Real home prices (adjusted for inflation) are expected to decline in 2026, even as nominal prices grow approximately 2%.[6] This creates a price-sensitive environment where buyers scrutinize every pound of their investment.

With average wage increases of 3.5% outpacing inflation at 2.6% (as of January 2026), buyers have genuine purchasing power gains.[2] However, this doesn't translate to willingness to overpay for properties with hidden defects. Instead, buyers are leveraging their improved financial position to demand transparency and comprehensive disclosure.

The prevalence of builder incentives reinforces this dynamic. Approximately 40% of builders are cutting prices on new construction homes by about 5% and offering mortgage rate buydowns that temporarily lower rates for 2-3 years.[2] When even new construction comes with discounts and incentives, buyers of existing properties naturally expect similar flexibility—and comprehensive surveys provide the evidence needed to negotiate effectively.

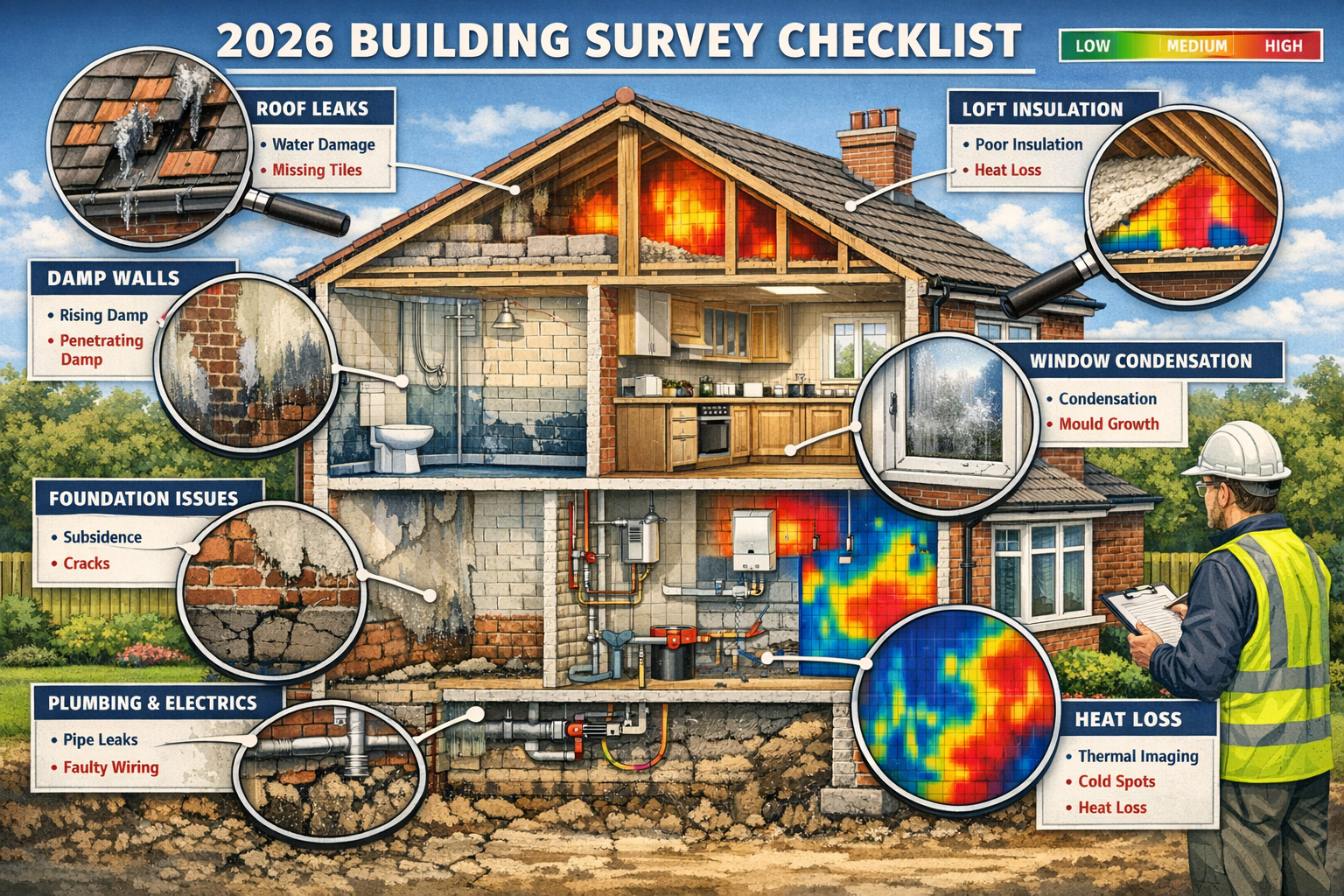

Essential Updates to RICS Building Survey Checklists for 2026

Critical Focus Areas for Damp and Moisture Penetration

Damp remains one of the most significant defects identified in building surveys, and 2026 has brought renewed focus to this perennial issue. Modern survey protocols now incorporate advanced detection methods that go beyond visual inspection.

Key damp assessment updates include:

| Assessment Type | Traditional Method | 2026 Enhanced Protocol |

|---|---|---|

| Rising Damp | Visual inspection, moisture meter readings | Thermal imaging, salt analysis, long-term monitoring recommendations |

| Penetrating Damp | External wall inspection | Drone surveys for roof and high-level defects, water ingress testing |

| Condensation | Visual mold identification | Humidity monitoring, ventilation adequacy assessment, insulation evaluation |

The integration of drone roof survey technology has revolutionized how surveyors assess high-level moisture risks. Drones equipped with thermal imaging cameras can identify heat loss patterns and moisture accumulation in roof structures without the safety risks and access limitations of traditional methods.

For properties showing signs of moisture issues, surveyors now routinely recommend specific defect reports that focus exclusively on damp-related concerns, providing buyers with detailed remediation cost estimates that inform negotiation strategies.

Energy Efficiency and Sustainability Standards

The 2026 building survey landscape places unprecedented emphasis on energy performance. With energy costs remaining elevated and environmental regulations tightening, a property's Energy Performance Certificate (EPC) rating has moved from an administrative formality to a critical valuation factor.

Updated energy efficiency assessment criteria:

🔋 Insulation adequacy – Loft, wall cavity, and floor insulation thickness and condition

🔋 Heating system efficiency – Boiler age, smart thermostat integration, zoning capabilities

🔋 Window performance – Double/triple glazing, air leakage, thermal bridging

🔋 Renewable energy potential – Solar panel feasibility, heat pump suitability

🔋 Air tightness – Draft identification, ventilation balance

Properties with EPC ratings below C now face significant market resistance, as buyers calculate the cost of upgrades required to meet emerging minimum standards. Surveyors are increasingly providing upgrade cost estimates within their reports, enabling buyers to factor these expenses into their purchase decisions.

The structural survey process now routinely includes energy efficiency commentary, recognizing that thermal performance issues often indicate underlying structural defects such as inadequate insulation or air leakage through building fabric failures.

Structural Integrity and Subsidence Risks

Structural concerns remain at the core of building survey assessments, but 2026 protocols reflect evolved understanding of risk factors and more sophisticated diagnostic approaches.

Priority structural assessment areas:

Foundation movement and subsidence – The UK's increasingly variable weather patterns, with periods of drought followed by intense rainfall, have elevated subsidence risks. Surveyors now employ historical data analysis, examining previous survey reports and insurance claims to identify properties in high-risk areas. Specialized subsidence surveys utilize crack monitoring technology and ground investigation techniques to differentiate between historic settlement and active movement.

Roof structure integrity – Beyond surface tile condition, modern surveys assess roof timber condition, particularly in properties built before 1960 where timber treatment standards were less rigorous. Thermal imaging identifies areas of moisture accumulation that may indicate structural timber decay before visible symptoms appear.

Wall tie failure – Properties constructed with cavity walls between 1920-1980 are particularly vulnerable to wall tie corrosion. Updated survey protocols include specific wall tie assessment, with recommendations for borescope inspection when visual indicators suggest potential failure.

Load-bearing alterations – With many properties having undergone modifications over decades, surveyors pay particular attention to structural alterations, especially removed walls or enlarged openings. Buyers purchasing properties with obvious alterations now routinely request verification that appropriate structural calculations and building control approvals were obtained.

Modern Construction Defects and New Build Considerations

The assumption that new construction eliminates the need for thorough surveys has been comprehensively debunked. In fact, new build properties in 2026 face particular scrutiny due to well-publicized defects in recent developments.

For new construction purchases, snagging report lists have become essential tools. These detailed inventories identify finishing defects, installation errors, and compliance issues before completion, providing buyers with leverage to ensure developers remedy issues before final payment.

Common new build concerns in 2026 include:

- Inadequate sound insulation between properties (particularly in converted buildings)

- Ventilation system deficiencies leading to condensation

- Incorrect installation of insulation materials

- Plumbing and heating system commissioning issues

- External drainage inadequacies

The prevalence of these issues has led to increased demand for pre-completion inspections, even on properties covered by NHBC or similar warranties. Buyers recognize that identifying defects before completion is far easier than pursuing remedies afterward.

Choosing the Right Survey Type for Your 2026 Property Purchase

Understanding Survey Level Options

The question "what survey do you need?" has become more complex in 2026 as survey offerings have evolved to meet diverse buyer requirements. Understanding the different survey types available is essential for making informed decisions.

RICS Home Survey Level 1 (Condition Report) – Suitable only for conventional, newer properties in good condition. This basic assessment provides an overview of condition but lacks the detail necessary for most 2026 buyers who are leveraging improved affordability to negotiate based on defects.

RICS Home Survey Level 2 (HomeBuyer Report) – The most popular option for standard properties built from conventional materials and in reasonable condition. This survey identifies significant defects and provides guidance on necessary repairs, offering the detail most buyers need to make informed decisions.

RICS Home Survey Level 3 (Building Survey) – Previously called a "Full Structural Survey," this comprehensive assessment is recommended for older properties (pre-1900), properties of unusual construction, properties in poor condition, or where significant alterations are planned. Given the price-sensitive 2026 market, many buyers are opting for this level even for standard properties to maximize their negotiating position.

Specialist Survey Considerations

Beyond standard survey levels, specific property characteristics or buyer intentions may require specialist assessments:

Boundary disputes – Properties with unclear boundary definitions or known neighbor disputes benefit from boundary surveys that provide definitive legal clarity before purchase completion.

Planned alterations – Buyers intending to modify leasehold properties should understand licence to alter requirements before committing to purchase, as some lease terms severely restrict modification rights.

Pre-purchase condition baseline – For properties that will undergo immediate renovation, a schedule of condition report creates a definitive record of the property's state at purchase, protecting buyers from future disputes about pre-existing conditions.

Cost-Benefit Analysis in the 2026 Market

The improved affordability environment of 2026 changes the cost-benefit calculation for building surveys. When buyers have more negotiating power and time to conduct due diligence, the investment in comprehensive surveys generates substantial returns.

Consider this scenario:

A buyer purchases a £400,000 property and invests £1,200 in a comprehensive Level 3 Building Survey. The survey identifies:

- Roof repairs required: £8,000

- Damp treatment and replastering: £5,000

- Electrical system upgrade: £3,500

- Total identified defects: £16,500

In the balanced market conditions of 2026, the buyer successfully negotiates a £12,000 price reduction based on these findings—a 10:1 return on the survey investment. Even if only partial price reduction is achieved, the buyer enters the purchase with full knowledge of required expenditure and can budget accordingly.

This calculation becomes even more favorable when considering the 40% of builders offering price reductions and incentives.[2] Buyers armed with comprehensive survey findings can negotiate not just price reductions but also builder remediation of identified defects before completion.

Maximizing Buyer Confidence Through Strategic Survey Use

Leveraging Survey Findings in Negotiations

The strategic value of building surveys extends far beyond defect identification. In 2026's more balanced market, survey reports have become powerful negotiation tools that shift leverage toward buyers.

Effective negotiation strategies include:

Prioritized defect categorization – Distinguish between critical structural issues requiring immediate attention, medium-term maintenance needs, and cosmetic concerns. This categorization allows buyers to focus negotiations on genuinely significant issues rather than diluting their position with minor complaints.

Remediation cost quantification – Obtain contractor quotes for identified repairs before entering negotiations. Vague references to "damp issues" carry less weight than documented evidence that remediation will cost £5,000-£7,000.

Alternative resolution proposals – Rather than simply demanding price reductions, consider proposing that sellers complete specific repairs before completion, or requesting retention of funds in escrow until remediation is verified.

Comparative market analysis – In the improved inventory environment (with 15.2% increase in 2025 and 8.9% projected growth in 2026), buyers can reference similar properties without the identified defects to justify price adjustments.[3]

Timeline Considerations for Survey Commissioning

The months' supply of inventory reaching 4.6 months in 2026 means buyers generally have more time to conduct thorough due diligence than in recent years.[3] However, strategic timing remains important for maximizing survey value.

Optimal survey commissioning timeline:

- Offer acceptance – Commission survey within 48 hours of offer acceptance

- Survey completion – Allow 5-10 working days for surveyor access and report preparation

- Review period – Allocate 3-5 days to review findings, obtain remediation quotes, and formulate negotiation strategy

- Renegotiation window – Approach sellers with findings 2-3 weeks after initial offer, allowing time for productive discussion before conveyancing deadlines pressure decisions

This timeline assumes standard mortgage offer validity periods and typical conveyancing progression. Buyers should coordinate with their solicitors to ensure survey findings can be incorporated into contract negotiations before exchange of contracts.

Post-Survey Decision Framework

Survey reports often reveal unexpected defects that require buyers to make difficult decisions. A structured decision framework helps navigate these situations:

For minor defects (total remediation cost <2% of purchase price):

- Proceed with purchase as planned

- Budget for repairs post-completion

- Consider requesting small goodwill price reduction

For moderate defects (remediation cost 2-5% of purchase price):

- Obtain detailed remediation quotes

- Negotiate price reduction equivalent to 50-75% of remediation costs

- Consider requesting seller completion of specific repairs

- Reassess property value relative to alternatives

For major defects (remediation cost >5% of purchase price):

- Commission specialist surveys for detailed assessment

- Obtain comprehensive remediation proposals

- Seriously consider withdrawing from purchase

- If proceeding, negotiate substantial price reduction (75-100% of remediation costs)

- Ensure mortgage lender is informed and property remains mortgageable

For structural concerns or undisclosed material defects:

- Engage expert witness services if misrepresentation is suspected

- Consider legal advice regarding potential misrepresentation claims

- Reassess whether property meets your requirements even with remediation

Regional Variations and Local Market Considerations

Geographic Survey Focus Differences

Property characteristics and associated survey priorities vary significantly across regions, requiring surveyors to adapt their assessment focus accordingly.

London and Southeast considerations – Properties in dense urban areas face particular challenges with subsidence risks due to clay soil conditions and mature tree proximity. Victorian and Edwardian terraced properties, which dominate much of inner London, require particular attention to structural movement, damp penetration, and roof condition. The prevalence of leasehold properties in London also necessitates careful review of lease terms and service charge obligations.

Period property considerations – Historic properties require specialist knowledge of traditional construction methods, appropriate repair techniques, and conservation area restrictions. Modern damp-proof courses, cement renders, and synthetic materials can cause significant damage when inappropriately applied to traditional buildings constructed to "breathe."

Conversion and subdivision concerns – The proliferation of property conversions, particularly in urban areas, requires careful assessment of sound insulation, fire safety provisions, and structural adequacy of alterations. Many conversions completed in the 1980s-2000s utilized substandard sound insulation that fails to meet current buyer expectations.

New Build Developments and Estate Considerations

The 40% of builders offering price reductions and incentives in 2026 reflects increased competition in the new build sector.[2] This competitive environment creates opportunities for buyers but also necessitates careful due diligence.

New build survey priorities:

- Verification of build quality against specification

- Assessment of estate management arrangements and service charges

- Review of adoption status for roads, sewers, and communal areas

- Evaluation of acoustic performance (particularly in apartment developments)

- Inspection of external works, drainage, and landscaping completion

For new build properties, the timing of survey commissioning is critical. Pre-completion snagging inspections (ideally 2-4 weeks before legal completion) provide maximum leverage for ensuring developers remedy defects before final payment.

Future-Proofing Your Property Investment Through Comprehensive Assessment

Long-Term Value Protection

The improved affordability environment of 2026, with mortgage payments consuming less than 30% of household income for the first time since 2022, creates opportunities for buyers to think beyond immediate purchase concerns and consider long-term value protection.[2][6]

Forward-looking survey considerations:

Climate resilience – Assess flood risk, drainage adequacy, and climate adaptation measures. Properties in areas with increasing flood risk face insurance challenges and potential value depreciation.

Adaptability and lifecycle needs – Evaluate whether the property can adapt to changing household needs, including potential for extensions, loft conversions, or accessibility modifications.

Maintenance projection – Request surveyor guidance on anticipated major expenditure over 5-10 years (roof replacement, heating system renewal, external redecoration) to budget for ownership costs beyond the purchase price.

Regulatory compliance trajectory – Consider how the property aligns with evolving energy efficiency standards and whether achieving compliance will require substantial investment.

Building Survey Documentation for Future Reference

Survey reports serve not only as pre-purchase assessment tools but as valuable reference documents throughout property ownership. Buyers should:

✅ Retain comprehensive records – Store survey reports, specialist assessments, and remediation documentation securely

✅ Track recommended monitoring – Follow surveyor recommendations for monitoring identified issues (crack monitoring, moisture level tracking)

✅ Document completed works – Maintain records of repairs and improvements for future sale disclosure

✅ Update assessments periodically – Consider follow-up surveys after significant weather events or when planning major works

This documentation proves invaluable when selling the property, as comprehensive records demonstrating proactive maintenance and issue resolution provide buyer confidence and support asking prices.

Integration with Broader Property Due Diligence

Building surveys represent one component of comprehensive property due diligence. Buyers should ensure survey findings are integrated with:

Legal searches and enquiries – Coordinate with solicitors to ensure survey findings align with seller disclosures and that any identified issues are addressed through contract terms or indemnity insurance.

Mortgage valuation – While separate from building surveys, mortgage valuations may identify issues affecting lending decisions. Ensure your mortgage broker is informed of significant survey findings that might impact the lender's assessment.

Insurance assessment – Discuss survey findings with insurance providers before completion, particularly regarding subsidence history, flood risk, or non-standard construction, as these factors significantly impact insurance availability and premiums.

Local authority planning and building control – Verify that identified alterations have appropriate planning permissions and building regulation approvals, requesting indemnity insurance where documentation is absent.

Conclusion: Seizing the 2026 Opportunity with Informed Confidence

The Impact of Falling Mortgage Rates on 2026 Building Surveys: Pre-Purchase Checks for Buyer Confidence represents a fundamental market shift that savvy buyers are leveraging to make informed, strategic property investments. With mortgage rates stabilizing around 6-6.2%, improved affordability creating negotiating power, and inventory expanding to provide genuine choice, 2026 offers a unique window of opportunity for buyers who approach purchases with thorough due diligence.[2][3][4]

The key to maximizing this opportunity lies in recognizing that improved financing conditions don't reduce the need for comprehensive building surveys—they amplify it. When buyers have breathing room in their budgets and time to conduct proper assessments, the strategic value of detailed survey reports increases exponentially. Survey findings transform from mere information into powerful negotiation tools that can secure price reductions, seller remediation commitments, or informed decisions to walk away from problematic properties.

The updated RICS survey protocols for 2026, with enhanced focus on damp detection, energy efficiency assessment, and structural integrity evaluation, provide buyers with unprecedented insight into property condition. Combined with specialist surveys addressing specific concerns—from subsidence risks to boundary disputes—buyers can enter property ownership with genuine confidence in their investment.

Actionable Next Steps for 2026 Property Buyers

Before viewing properties:

- Research typical defects for your target property type and era

- Understand which survey level suits your requirements

- Budget for survey costs (typically £400-£1,500 depending on property value and survey type)

- Identify qualified chartered surveyors in your target area

After offer acceptance:

- Commission your building survey within 48 hours

- Request access for surveyor within one week

- Review the survey report thoroughly, seeking clarification on any unclear findings

- Obtain remediation quotes for significant identified defects

- Formulate a clear negotiation strategy based on findings

- Coordinate with your solicitor to ensure survey findings inform contract negotiations

Post-survey decision-making:

- Apply the decision framework based on defect severity and remediation costs

- Consider the property's long-term value trajectory, not just immediate condition

- Don't hesitate to withdraw if surveys reveal deal-breaking issues

- If proceeding, ensure all agreements regarding repairs or price adjustments are documented in writing

- Retain survey documentation for future reference and eventual resale

The combination of falling mortgage rates, improved inventory, and sophisticated survey protocols creates an environment where informed buyers can secure quality properties at fair prices with genuine confidence in their condition. The investment in comprehensive building surveys—typically representing less than 0.5% of purchase price—generates returns through negotiated price reductions, avoided problem purchases, and long-term value protection that far exceed the initial cost.

As the market continues evolving through 2026, with the Federal Reserve's anticipated rate cuts and builders' competitive pricing strategies, buyers who prioritize thorough due diligence will be best positioned to capitalize on opportunities while avoiding the pitfalls that await those who sacrifice assessment quality for transaction speed. The Impact of Falling Mortgage Rates on 2026 Building Surveys: Pre-Purchase Checks for Buyer Confidence isn't just a market trend—it's a fundamental shift toward more informed, strategic property investment that benefits buyers, supports market stability, and promotes higher standards across the property sector.

References

[1] Builders Top Concerns 2026 – https://www.nahb.org/blog/2026/02/builders-top-concerns-2026

[2] 2026 Mortgage Industry Outlook Key Trends Impacting Home Ownership – https://www.fnbo.com/insights/mortgage/2026/2026-mortgage-industry-outlook-key-trends-impacting-home-ownership

[3] 2026 Housing Outlook Ongoing Challenges Cautious Optimism And Incremental Gains – https://www.nahb.org/news-and-economics/press-releases/2026/02/2026-housing-outlook-ongoing-challenges-cautious-optimism-and-incremental-gains

[4] Mortgage Interest Rates Forecast – https://www.rocketmortgage.com/learn/mortgage-interest-rates-forecast

[5] Builders Top Challenges For 2026 – https://eyeonhousing.org/2026/02/builders-top-challenges-for-2026/

[6] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[7] Mortgage Rates February 11 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-11-2026/

[8] Survey Elevated Mortgage Rates Remain Home Builders Primary Challenge – https://nationalmortgageprofessional.com/news/survey-elevated-mortgage-rates-remain-home-builders-primary-challenge