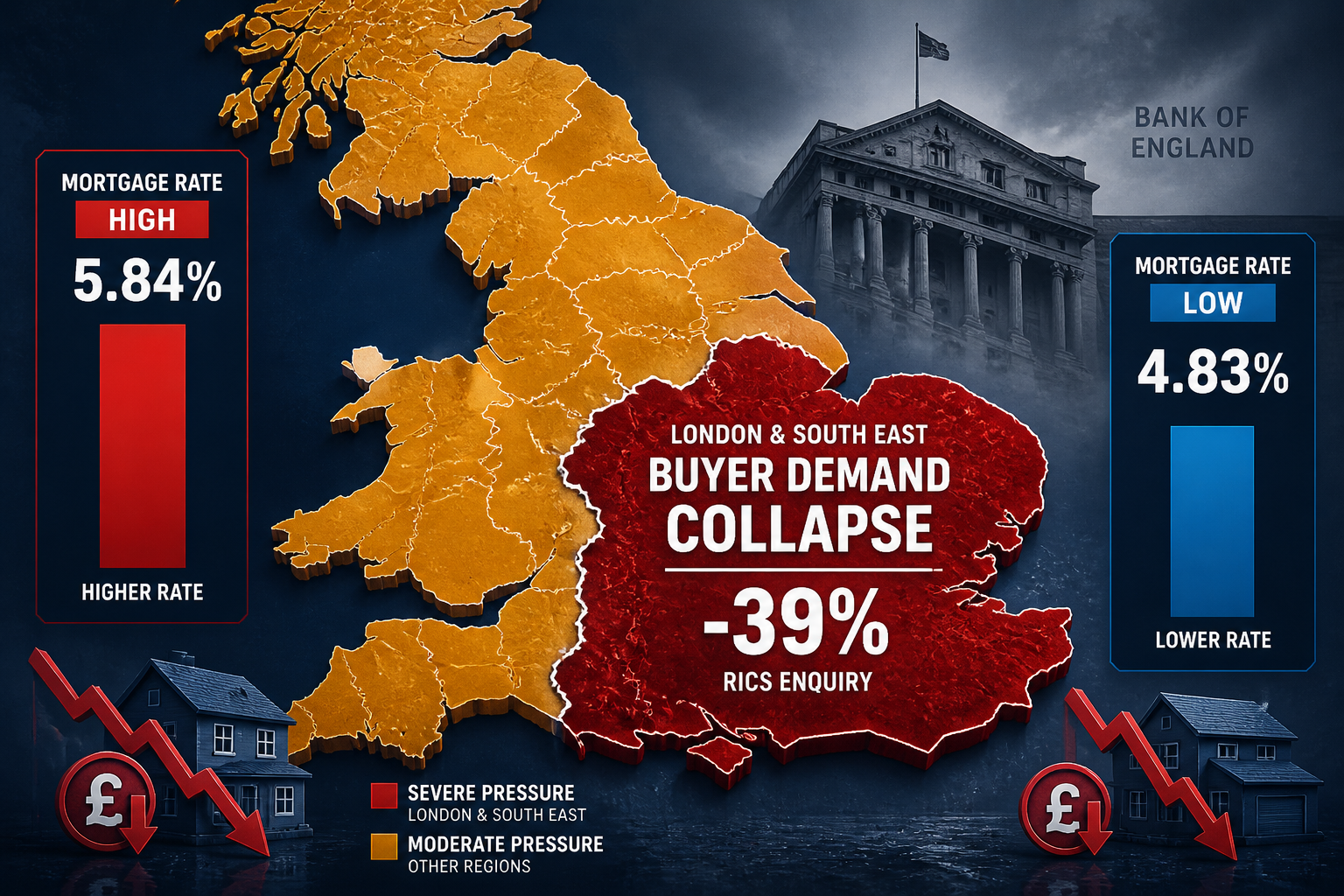

New buyer enquiries in the UK plummeted to a net balance of -39% in the RICS March 2026 survey — one of the sharpest single-quarter drops recorded outside of a full recession. Geopolitical shockwaves from the Middle East conflict, combined with a mortgage rate surge that added 101 basis points in just four weeks, have created a valuation environment that standard RICS Red Book methodology was not designed to navigate alone. For building surveyors, the challenge is not simply academic. Clients are making six- and seven-figure decisions based on appraisals produced in a market where comparable sales data is rapidly becoming stale, buyer pools are shrinking, and macroeconomic signals are contradicting each other daily.

Navigating Middle East Conflict Impacts on 2026 UK Housing: Valuation Strategies for Building Surveyors Amid Rising Borrowing Costs is now the defining professional challenge for practitioners across London, the South East, and beyond. This article sets out a structured, actionable framework to help surveyors produce defensible, market-reflective valuations in these volatile conditions.

Key Takeaways 📌

- Mortgage rates surged to approximately 5.84% by late April 2026 — a 101 basis point rise in four weeks — directly compressing buyer purchasing power and suppressing comparable sale prices [3]

- House prices fell 0.5% in March 2026, dropping below the £300,000 average threshold, with annual growth collapsing from 1.2% to 0.8% [3]

- Hundreds of mortgage products have been withdrawn since conflict escalation, reducing transaction volumes and making recent comparables less reliable [3]

- Regional divergence is accelerating, with London and the South East showing the most acute demand weakness — surveyors must apply location-specific adjustments [3]

- Structural pressures — fiscal headwinds, persistent inflation, and tax policy uncertainty — will extend market weakness well beyond any geopolitical resolution [1]

How the Middle East Conflict Is Reshaping UK Housing Market Fundamentals

The transmission mechanism from Middle East conflict to UK property values is not direct — it operates through a chain of financial and economic effects that building surveyors must understand in sequence.

Stage 1: Energy and commodity price shock. Petrol prices spiked sharply following conflict escalation, and food inflation followed. Supply chain disruptions created commodity backlogs across construction materials, keeping build costs elevated [1][4].

Stage 2: Inflation expectations repriced. As inflation data came in hotter than forecast, financial markets reversed their rate-cut expectations. By late April 2026, markets had shifted from pricing two rate cuts to pricing one rate hike [1]. The five-year swap rate — the benchmark lenders use to price fixed mortgages — moved from below 3.5% in February to 4.1% in late April [1].

Stage 3: Mortgage market repricing. Lenders responded by withdrawing products and repricing upwards. The average two-year fixed rate surged from 4.83% in early March to approximately 5.84% by late April — a 101 basis point increase in under four weeks [3]. Hundreds of mortgage products disappeared from the market [3].

Stage 4: Transaction volume collapse. Buyers who had received mortgage-in-principle offers found those offers invalidated by rate repricing [2][4]. Many paused purchasing decisions entirely. The result: transaction volumes fell, sales cycles lengthened, and the pool of comparable evidence available to valuers thinned dramatically.

💬 "The effects of the conflict will persist long after any resolution — structural fiscal headwinds and persistent inflation are not geopolitical problems. They are economic ones." — Knight Frank Research [1]

The Bank of England's Constrained Position

The Bank of England held the base rate steady at its March 19 meeting, and the Monetary Policy Committee convened on April 30 with further cuts deemed unlikely in the near term [2]. Surveyors should not model for declining rates in 2026 valuation scenarios. A higher-for-longer rate environment is the operative assumption.

Compounding this, the government's constrained fiscal headroom and falling demand for UK government debt are structural issues — independent of the conflict — that will maintain upward pressure on interest rates and downward pressure on house prices for an extended period [1]. Tax speculation ahead of the autumn Budget adds a further layer of cyclical uncertainty [1].

Valuation Methodology Adjustments: A Practical Framework for Building Surveyors

Standard comparable sales analysis assumes a reasonably liquid, stable market. In 2026, neither condition holds across much of England. Navigating Middle East Conflict Impacts on 2026 UK Housing: Valuation Strategies for Building Surveyors Amid Rising Borrowing Costs requires surveyors to apply a structured set of methodological adjustments.

1. Temporal Adjustment of Comparables

With house prices falling 0.5% in March 2026 alone and annual growth collapsing to 0.8% [3], comparable sales from even three months prior may materially overstate current market value. Surveyors should:

- Apply a downward temporal adjustment to comparables older than 8–10 weeks

- Document the adjustment rationale explicitly in the valuation report, referencing current RICS market survey data

- Flag where the comparable pool is thin due to reduced transaction volumes

2. Mortgage Availability Weighting

The withdrawal of hundreds of mortgage products has created a two-tier buyer market: cash buyers and those with large deposits face a different affordability ceiling than buyers dependent on high-LTV products [3]. Valuations should reflect the realistic buyer pool for the specific property type, not the theoretical full market.

For properties typically purchased by first-time buyers or those requiring 90%+ LTV mortgages, apply a more conservative market value assumption. For prime properties in cash-rich buyer segments, the adjustment may be less severe.

3. Regional Demand Discount Application

Geographic demand weakness is not uniform. London and the South East are showing the most acute buyer hesitation [3]. Surveyors operating across these regions — whether providing chartered surveyor services in South East London or property valuations in central London — should apply a regional demand discount where RICS survey data confirms negative net balances for new buyer enquiries in that specific sub-market.

Suggested regional adjustment framework (2026):

| Region | Demand Pressure | Suggested Comparable Adjustment |

|---|---|---|

| Central London | Severe | -3% to -5% on stale comparables |

| South East London | High | -2% to -4% |

| Outer London / Home Counties | Moderate | -1% to -3% |

| Regional cities | Low-Moderate | -0.5% to -2% |

Note: These are indicative ranges only. Each valuation must be supported by specific local evidence.

4. Reinstatement Cost Recalibration

Construction material inflation — driven partly by supply chain disruption from the conflict — means that reinstatement cost valuations require urgent review. Insurance reinstatement figures based on pre-2026 BCIS data may now understate true rebuild costs. Surveyors should:

- Source the most current BCIS location factors

- Apply an uplift for material cost inflation where local contractor quotes confirm elevated pricing

- Flag reinstatement cost uncertainty as a specific risk in the valuation narrative

5. Enhanced Market Commentary in Reports

RICS Red Book standards require valuers to disclose material uncertainty where it exists. In the current environment, material uncertainty clauses are not optional — they are professionally necessary. Every valuation report should include:

- A summary of current market conditions referencing geopolitical drivers

- Explicit acknowledgment that transaction volumes are suppressed

- A statement that the valuation reflects conditions at the specific date of inspection and may be subject to rapid revision

For clients requiring a comprehensive London property valuation, this transparency is also a client service differentiator — it demonstrates professional rigour rather than false precision.

Regional Strategies and Specialist Valuation Considerations

The practical application of navigating Middle East Conflict Impacts on 2026 UK Housing: Valuation Strategies for Building Surveyors Amid Rising Borrowing Costs varies significantly by property type, transaction purpose, and geography.

Commercial Property Valuations

Commercial property faces compounded pressures. Rising borrowing costs reduce investor yields, while supply chain disruption affects tenant businesses, increasing void risk. Surveyors conducting commercial property valuations in London should:

- Apply higher yield adjustments to reflect increased financing costs

- Review rent review assumptions downward where tenant covenant strength has weakened

- Scrutinise commercial dilapidation surveys carefully — tenants under financial pressure are more likely to defer maintenance obligations

For rent review valuations in London, the combination of weak occupier demand and higher financing costs creates a genuine risk of downward rent pressure in secondary locations.

Residential Survey Selection

Buyers who are proceeding despite market uncertainty are, understandably, more risk-averse. This is driving increased demand for comprehensive surveys over basic mortgage valuations. Surveyors should proactively guide clients toward appropriate survey levels — the comparison between a homebuyer report and a full building survey is a critical conversation in the current climate, where buyers cannot afford post-purchase surprises.

Properties with structural issues, roof defects, or subsidence risk carry amplified downside in a falling market. A structural survey or subsidence survey that identifies latent defects now protects buyers from acquiring liabilities that will be harder to exit in a depressed market.

Divorce and Shared Ownership Valuations

Market volatility creates particular complexity for legally-mandated valuations. For divorce property valuations in London and shared ownership valuations, the date of valuation is legally significant — and in a rapidly moving market, a valuation that is even 60 days old may be challenged. Surveyors should:

- Advise solicitors and clients of the heightened temporal sensitivity

- Build explicit market condition commentary into legally-instructed reports

- Consider recommending a shorter validity period than standard

Key Checklist for Surveyors in 2026 🗒️

- ✅ Apply temporal adjustments to all comparables older than 8 weeks

- ✅ Assess the realistic buyer pool (cash vs. mortgage-dependent)

- ✅ Include a material uncertainty clause in every residential and commercial valuation

- ✅ Recalibrate reinstatement costs using current BCIS data

- ✅ Apply regional demand discounts where RICS survey data confirms negative enquiry balances

- ✅ Review commercial yield assumptions upward to reflect higher financing costs

- ✅ Document all adjustments transparently with supporting rationale

- ✅ Advise clients on appropriate survey levels given amplified defect risk in a falling market

Conclusion: Actionable Next Steps for Building Surveyors

The confluence of Middle East conflict, a mortgage rate shock, and structural UK fiscal pressures has created the most challenging valuation environment since the 2008 financial crisis. House prices have already fallen below the £300,000 average threshold [3], mortgage rates have surged to 5.84% [3], and the Bank of England has signalled that cuts are not imminent [2]. These are not temporary disruptions — Knight Frank's analysis identifies four distinct stages of market impact, with structural effects persisting well beyond any geopolitical resolution [1].

For building surveyors, the immediate action priorities are:

- Audit your comparable database — identify all valuations where comparables are older than 8–10 weeks and flag for review

- Update your standard report templates to include current market condition disclosures and material uncertainty clauses

- Recalibrate reinstatement cost assumptions using the most current BCIS data available

- Engage clients proactively about survey level selection — in a falling market, the cost of a comprehensive survey is trivially small against the cost of an undisclosed defect

- Apply regional demand adjustments systematically, particularly for London and South East instructions

- Model for higher-for-longer rates in all valuation scenarios — do not assume rate cuts in 2026

The surveyors who will maintain professional credibility and client trust through this period are those who adapt their methodology to reflect market reality, communicate uncertainty transparently, and guide clients with evidence-based precision. Complacency — continuing to apply pre-2026 assumptions to a fundamentally changed market — carries both professional and reputational risk.

For expert surveying support across London and the South East, explore the full range of building surveyor services available to navigate these challenging market conditions.

References

[1] Middle East Conflict Will Impact UK Housing Market In Four Stages – https://www.knightfrank.co.uk/research/article/2026/4/middle-east-conflict-will-impact-uk-housing-market-in-four-stages

[2] How Is The Middle East Conflict Impacting The UK Housing Market – https://www.silverspringlettings.co.uk/blog/how-is-the-middle-east-conflict-impacting-the-uk-housing-market

[3] News Middle East Conflict And The UK Housing Market – https://www.thomasoliveruk.co.uk/news-middle-east-conflict-and-the-uk-housing-market-1115

[4] How Is The Middle East Conflict Impacting The UK Housing Market – https://rexgooding.com/blog/how-is-the-middle-east-conflict-impacting-the-uk-housing-market/61140

[5] How Global Conflicts In The Middle East Could Influence The UK Property Market In 2026 – https://www.99home.co.uk/blog/blog-details/How-Global-Conflicts-in-the-Middle-East-Could-Influence-the-UK-Property-Market-in-2026/

[7] Middle East Conflict To Have Limited Impact On Full Year Results Says Barratt Redrow – https://www.housingtoday.co.uk/news/middle-east-conflict-to-have-limited-impact-on-full-year-results-says-barratt-redrow/5141777.article