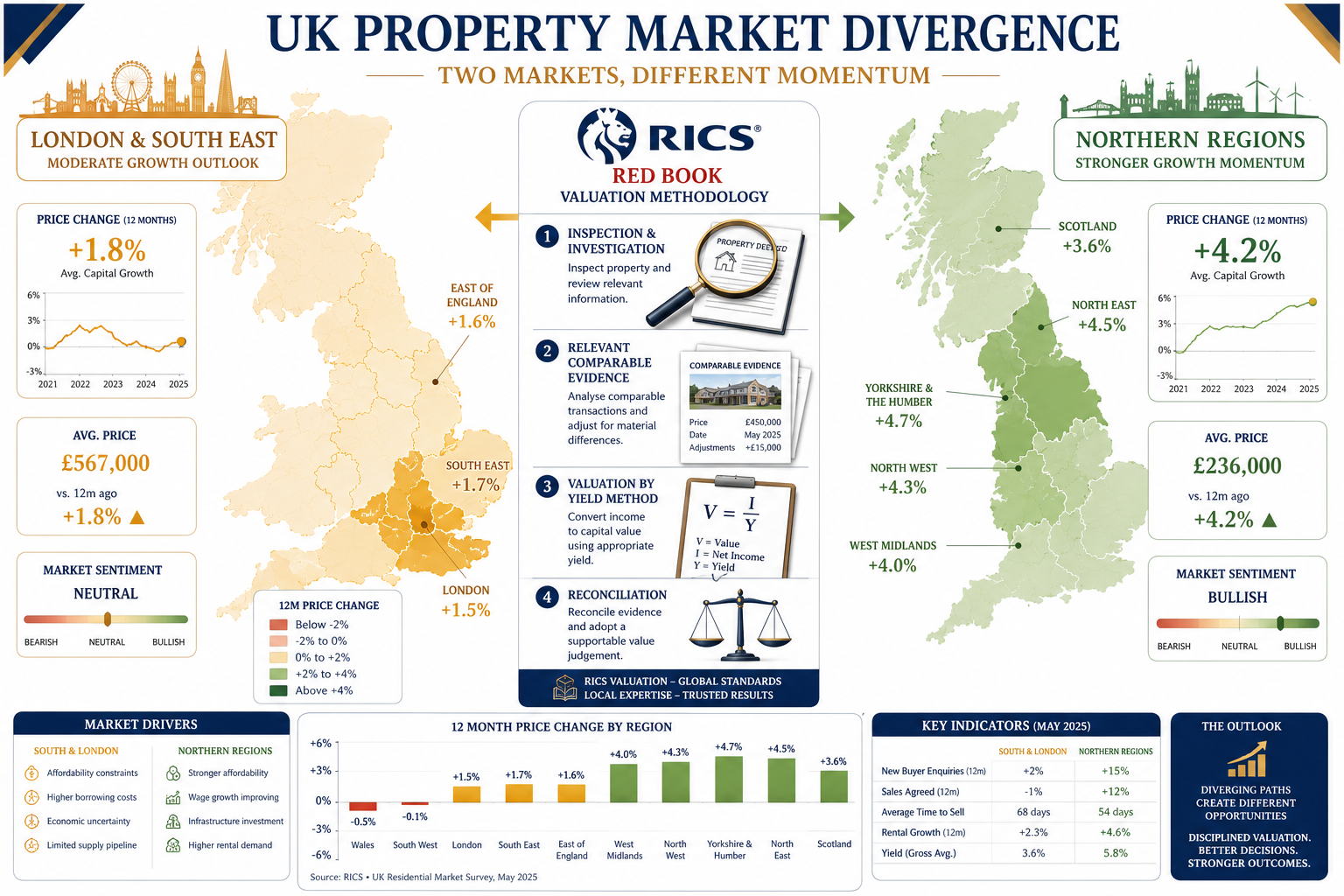

A net balance of -10% among RICS surveyors reporting falling rather than rising house prices in January 2026 marks a striking improvement from the double-digit negative readings of mid-2023. That single figure tells a nuanced story: the UK residential market has not recovered in the traditional sense, but it has stopped deteriorating at pace. For valuers, this stabilisation is both an opportunity and a methodological challenge. Applying the right RICS techniques when prices are neither clearly rising nor clearly falling requires precision, evidence discipline, and a careful reading of regional signals.

This article examines how surveyors and valuers can approach valuing stabilised national prices in early 2026: RICS techniques from January survey insights, covering the data backdrop, core valuation methodology adjustments, and the regional divergences that make a one-size-fits-all approach unreliable.

Key Takeaways

- The RICS January 2026 survey records a national net balance of -10%, indicating price stabilisation rather than continued decline or recovery.

- Surveyors must apply tighter comparable evidence windows and explicit time adjustments when markets are neither trending up nor down.

- Regional divergence is significant: London and the South East lag behind parts of the Midlands and North, requiring location-specific calibration.

- Improving buyer sentiment and easing mortgage rates are positive leading indicators but have not yet translated into uniform price growth.

- RICS Red Book standards remain the non-negotiable framework; surveyors must document assumptions transparently in a stabilised market.

Understanding the January 2026 RICS Survey Data

The RICS Residential Market Survey is one of the most closely watched leading indicators in UK property. Its net balance methodology asks surveyors whether prices in their area have risen, fallen, or stayed the same over the previous month. A reading of -10% in January 2026 means that 10% more respondents reported falling prices than rising prices — but critically, this is the narrowest negative reading in over two years.

What a -10% Net Balance Actually Means for Valuers

It is tempting to read stabilisation as neutrality, but the -10% figure still signals a mild downward bias at the national level. Valuers must resist the urge to treat this as a green light for upward adjustments. Instead, the appropriate response is:

- Maintain conservative comparable selection, favouring transactions from the most recent three-to-six months.

- Apply modest negative time adjustments where comparable evidence predates the stabilisation period (mid-2025 onward).

- Flag market conditions explicitly in valuation reports, noting that the net balance figure remains negative even as sentiment improves.

The distinction between stabilisation and recovery matters enormously in formal valuations, particularly for mortgage lending purposes. RICS registered valuers in London and across the UK are required to base opinions of value on current market evidence, not anticipated future movements.

Sentiment vs. Transaction Evidence

The January survey also captured improving buyer enquiries and a modest uptick in agreed sales. However, sentiment indicators lead transaction evidence by several months. A surveyor who prices optimistically on the basis of improved enquiries, without supporting comparable sales, risks a valuation that does not withstand scrutiny.

The professional standard here is clear: opinion of market value must reflect what a willing buyer would pay a willing seller on the date of valuation, based on available evidence. Sentiment is context; comparable sales are evidence.

Core RICS Valuation Techniques for a Stabilised Market

Valuing stabilised national prices in early 2026 using RICS techniques from January survey insights demands a more granular approach than either a rising or falling market. When the trend is ambiguous, every methodological decision carries greater weight.

The Comparable Method: Tightening the Evidence Window

The comparable method remains the primary approach for residential valuation. In a stabilised market, the evidence window should be compressed. Best practice in early 2026 suggests:

| Evidence Age | Adjustment Required | Reliability Rating |

|---|---|---|

| 0-3 months | Minimal or none | High |

| 3-6 months | Small negative adjustment | Moderate |

| 6-12 months | Moderate negative adjustment | Lower |

| Over 12 months | Significant adjustment or exclude | Low |

Where fewer than three directly comparable transactions exist within a tight timeframe, surveyors should document the shortage and explain the basis for any adjustments applied to older evidence. Transparency in the report is not optional — it is a Red Book requirement.

For those seeking to understand the cost framework of formal valuations, the RICS valuation cost guide provides useful context on what comprehensive, evidence-based work involves.

Time Adjustments in a Flat Market

Time adjustments are among the most technically demanding elements of valuation in a stabilised environment. When prices were falling sharply in 2023 and early 2024, a negative monthly adjustment of 0.3-0.5% was defensible for many markets. By January 2026, the appropriate adjustment has compressed significantly.

A practical approach for early 2026:

- National baseline: Apply a small negative adjustment of 0.0% to -0.1% per month for comparables more than three months old, unless local evidence suggests otherwise.

- Document the basis: Reference the RICS January survey net balance, Land Registry price paid data, and any local agent intelligence as the foundation for the chosen adjustment rate.

- Sensitivity test: Where the adjustment materially affects the concluded value, run a sensitivity analysis and note the range in the report.

The Investment Method and Yield Calibration

For residential investment properties — houses in multiple occupation, buy-to-let flats, and mixed-use assets — the investment method applies. Stabilising prices affect both the yield and the reversionary capital value assumptions.

In early 2026, gross yields in many UK cities have edged upward from their 2021-2022 lows, partly because capital values have softened and partly because rental demand remains strong. Surveyors using the investment method should:

- Source current yield evidence from RICS market surveys, property data providers, and recent auction results.

- Avoid anchoring to peak-market yields from 2021, which would produce inflated capital values.

- Consider the impact of the Renters' Rights Bill and energy efficiency requirements on future rental income assumptions.

Red Book Compliance in an Uncertain Market

The RICS Valuation — Global Standards (Red Book) require that valuers disclose any material uncertainty that may affect the reliability of the opinion of value. In a stabilised but not clearly recovering market, a material uncertainty clause may be appropriate where:

- Transaction volumes remain thin in the subject property's micro-market.

- The property type has shown divergent price behaviour from the broader area.

- Significant policy or economic events are pending that could shift values materially.

The Red Book valuation service in London provides a framework for ensuring full compliance with these standards, which is especially important when valuations are being used for mortgage lending, litigation, or financial reporting.

Regional Divergences: Why National Averages Are Insufficient

The national -10% net balance in the January 2026 RICS survey conceals significant regional variation. Applying national averages to local valuations is one of the most common and consequential errors a surveyor can make in a divergent market.

London and the South East: Continued Pressure

London and the South East continue to underperform the national average. Affordability constraints, elevated mortgage costs relative to local incomes, and a higher proportion of leasehold properties subject to ongoing legislative uncertainty have all weighed on values.

Surveyors working across central London and west London should note that the net balance for these regions likely sits below the national -10% figure. Comparable evidence from 2024 will generally need a negative time adjustment even in early 2026, and the evidence window should be kept tight.

For leasehold properties specifically, the interaction between price stabilisation and lease length is critical. A flat with fewer than 80 years remaining on its lease faces a compounding discount that operates independently of market trends. Valuers must separate the market movement adjustment from the lease-specific adjustment and apply both transparently.

The Midlands and North: Relative Outperformance

Parts of the East and West Midlands, Yorkshire, and the North West have shown relative resilience. In some micro-markets, the net balance has approached zero or even turned marginally positive by January 2026. This reflects:

- Lower absolute price levels, making affordability less of a barrier as mortgage rates ease.

- Stronger employment markets in logistics, manufacturing, and public sector roles.

- Investor demand for higher-yielding residential assets outside the capital.

Surveyors in these regions should be cautious about applying the national negative time adjustment. Where local evidence supports a flat or marginally positive trend, the adjustment should reflect that local picture — and the report should cite the specific evidence base.

Scotland and Wales: Separate Regulatory Contexts

Scotland and Wales operate under distinct property law and regulatory frameworks. The Scottish property market has shown its own stabilisation pattern, influenced by the Land and Buildings Transaction Tax structure and the Scottish Government's approach to rent controls. Welsh market conditions have been shaped by second-home legislation and local demand dynamics.

Valuers operating across borders must ensure they are applying jurisdiction-specific evidence and are familiar with the relevant regulatory context, not simply extrapolating from English market data.

Practical Implications for Valuation Reports

The regional divergence argument has a direct practical implication: every valuation report in early 2026 should include an explicit market conditions section that:

- References the national RICS net balance figure as context.

- Identifies the regional and local net balance where available.

- States the time adjustment applied and its evidential basis.

- Notes any material uncertainty arising from thin comparable evidence.

This level of transparency protects the valuer professionally and gives the client, lender, or court a clear audit trail of the reasoning applied.

Applying January Survey Insights to Specific Valuation Scenarios

Valuing stabilised national prices in early 2026 using RICS techniques from January survey insights is not purely theoretical. Several common valuation scenarios require specific methodological responses.

Mortgage Lending Valuations

Lenders require valuations that reflect current market value without optimism bias. In a stabilised market, the key discipline is avoiding the temptation to shade values upward because sentiment has improved. The valuation must be supportable by comparable evidence on the date of inspection.

Where a property is being purchased at a price that appears to reflect anticipated recovery rather than current market value, the surveyor must report the value as assessed, not the agreed purchase price, if the two differ materially.

Capital Gains Tax and Matrimonial Valuations

Retrospective and current-date valuations for tax or legal purposes must be particularly precise about the market conditions prevailing at the relevant date. A capital gains tax valuation carried out in early 2026 requires the valuer to pinpoint the market conditions at the disposal date, which may differ from current conditions if the disposal occurred during the more volatile 2023-2024 period.

Similarly, matrimonial valuations require a clear statement of the date of valuation and the market conditions applying at that date, with the January 2026 RICS survey data providing useful context for current-date instructions.

Lease Extension Valuations

Lease extension valuations under the Leasehold Reform, Housing and Urban Development Act 1993 (as amended) require a current market value opinion for the subject flat. In a stabilised market, the relativity tables used to calculate the premium must be applied to a base value that reflects actual market conditions, not an aspirational figure.

For those navigating the complexities of lease extension valuation in London, the stabilisation of prices in early 2026 means that base values should be derived from tightly evidenced comparables, with any adjustments clearly documented.

Insurance Reinstatement Valuations

It is worth noting that insurance reinstatement valuations are not affected by market price movements in the same way as market value assessments. Reinstatement cost reflects the cost of rebuilding, not the market value of the property. However, surveyors should be aware that construction cost inflation, which has been significant in recent years, continues to affect reinstatement figures independently of market price stabilisation.

Professional Standards and Documentation in Early 2026

The RICS professional standards framework does not change with market conditions, but the emphasis on certain requirements intensifies when markets are in transition. Three areas deserve particular attention in early 2026.

Conflicts of interest: In a market where some clients are under financial pressure, the temptation to produce valuations that support a desired outcome increases. RICS members must maintain independence and document any potential conflicts before accepting an instruction.

Competence in specialist property types: Stabilisation has not been uniform across property types. Purpose-built student accommodation, build-to-rent blocks, and mixed-use assets have each followed distinct price paths. Surveyors should only accept instructions for property types within their demonstrated competence.

Continuing professional development: The January 2026 survey insights, combined with the evolving legislative landscape around leasehold reform and energy efficiency, represent significant knowledge requirements. RICS members are expected to maintain current awareness as part of their CPD obligations.

For those considering what level of survey or valuation is appropriate for a specific transaction, the guide to choosing the right survey provides a practical starting point before engaging a valuer.

Conclusion

The January 2026 RICS survey data presents a market in careful equilibrium — not recovering, not declining sharply, but stabilising at a level that demands methodological precision from every valuer who works within it. The national -10% net balance is a useful headline, but it is the regional detail, the evidence window discipline, and the transparent documentation of assumptions that will define the quality of valuations produced in this period.

Actionable next steps for surveyors and property professionals in early 2026:

- Compress comparable evidence windows to three-to-six months wherever possible and document the rationale for any older evidence used.

- Apply regionally calibrated time adjustments rather than a single national figure, citing local RICS survey data and Land Registry evidence.

- Include a market conditions section in every valuation report, referencing the January 2026 RICS net balance and its local equivalent.

- Consider whether a material uncertainty clause is warranted, particularly for thin-market property types or locations showing divergent price behaviour.

- Maintain CPD currency on leasehold reform, energy efficiency requirements, and their interaction with market value.

- Engage a RICS registered valuer with demonstrable local market knowledge for any valuation where the stakes — financial, legal, or regulatory — are significant.

Stabilisation is not stagnation. It is a market condition that rewards careful, evidence-based practice and penalises assumptions borrowed from either the boom years or the downturn. The surveyors who navigate it well will be those who let the evidence lead.

References

- RICS Residential Market Survey, January 2026. Royal Institution of Chartered Surveyors.

- RICS Valuation — Global Standards (Red Book). Royal Institution of Chartered Surveyors, 2022.

- HM Land Registry UK House Price Index. Published monthly, various dates 2024-2025.

- Leasehold Reform, Housing and Urban Development Act 1993 (as amended by the Leasehold and Freehold Reform Act 2024).

- RICS Professional Standards and Guidance, UK: Valuation of Individual New-Build Homes. Royal Institution of Chartered Surveyors, 2023.