The UK property market is experiencing a pivotal shift in 2026. After years of challenging conditions, first-time buyers are returning to the market in meaningful numbers, driven by stabilising mortgage rates and improved affordability in key regional markets. However, this resurgence brings a critical challenge: securing accurate property valuations that satisfy increasingly cautious lenders while reflecting true market value in competitive local markets outside the traditional South East hotspots.

Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements has become essential knowledge for both property professionals and aspiring homeowners. With mortgage rates projected to stabilise between 3.75% and 4.75%[1], and increased access to 95% and 100% mortgage products[1], the accuracy of property valuations has never been more crucial to converting buyer interest into completed purchases.

Key Takeaways

- 🏠 House prices expected to grow modestly at 0-2% nationally in 2026, with stronger performance in northern regional cities creating new valuation challenges[1]

- 📊 Mortgage rates stabilising between 3.75% and 4.75% is improving affordability and bringing first-time buyers back to the market[1]

- 🔍 RICS Home Survey Level 2 (£400-£1,000) remains the optimal choice for most first-time buyer properties, balancing cost and comprehensive assessment[4]

- 📈 Regional markets like Preston, Lancaster, and Blackpool are attracting stronger first-time buyer interest due to lower price points and stable employment[1]

- ✅ Accurate valuations are critical for mortgage approval, particularly with 95% and 100% LTV products where lenders scrutinise property condition intensively

The 2026 First-Time Buyer Market Landscape

Current Market Conditions and Price Trends

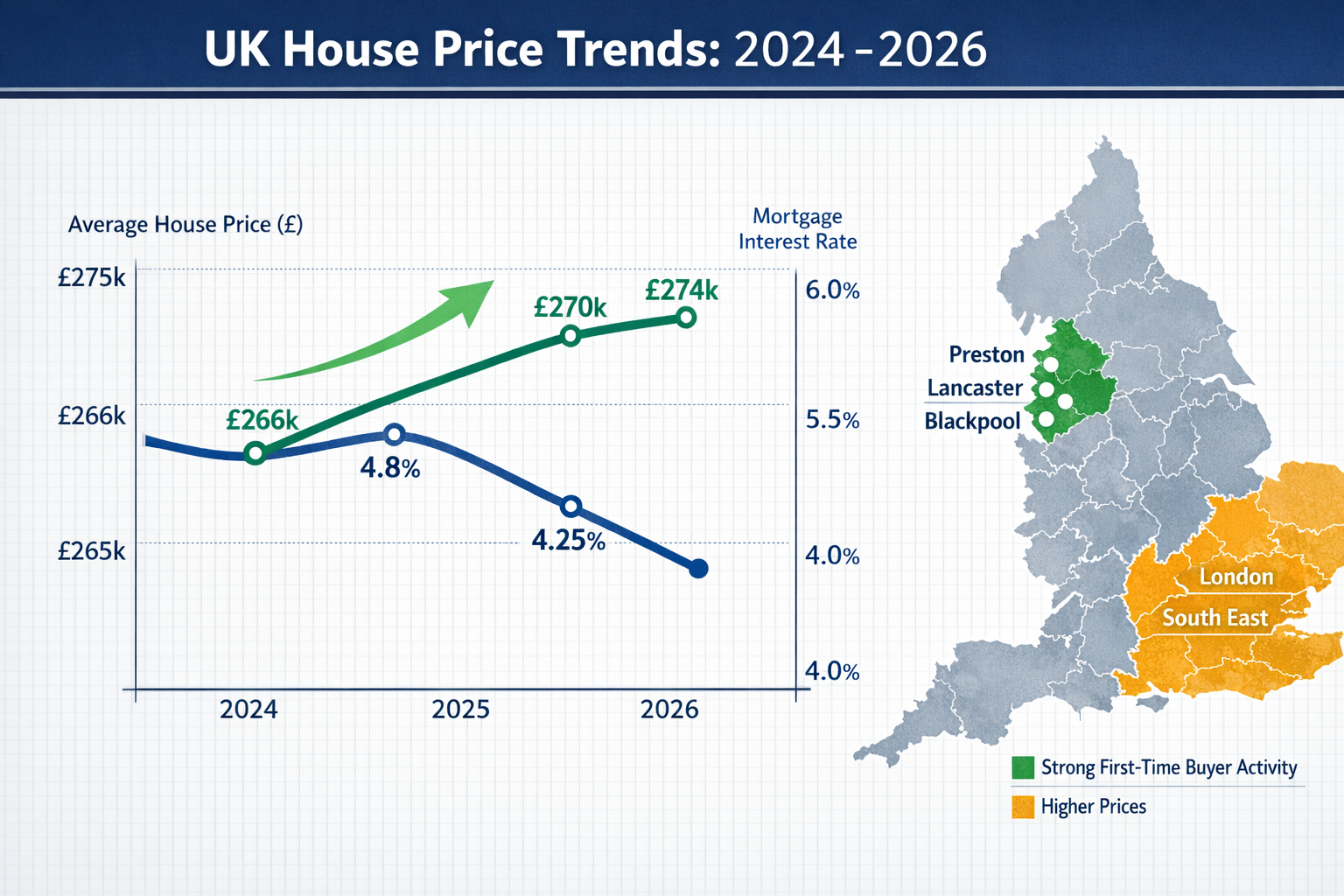

The UK property market enters 2026 with cautious optimism. The current average UK house price stands at £271,068, representing a slight decrease from £272,998 in November 2025[2]. However, this December dip should be viewed in context—the previous December saw unusually strong 4.7% growth, making year-on-year comparisons less straightforward[2].

Looking forward, major forecasters predict modest growth of 0-2% nationally throughout 2026[1]. Nationwide projects slightly higher growth at 2-4%, while Halifax forecasts 1-3%[2]. These conservative predictions reflect ongoing economic uncertainties but represent a significant improvement over the volatility of recent years.

For first-time buyers, the most significant development is regional divergence. While London and the South East face continued affordability constraints, northern cities and regional markets are experiencing renewed activity. Cities like Preston, Lancaster, and Blackpool are attracting stronger first-time buyer interest due to lower absolute price points that reduce sensitivity to interest rate changes[1].

Mortgage Affordability Improvements

The mortgage landscape has transformed dramatically since the turbulent period of 2022-2023. Mainstream mortgage products are now stabilising between 3.75% and 4.75%[1], creating a more predictable borrowing environment that allows first-time buyers to plan with confidence.

Perhaps more significantly, lenders have expanded access to high loan-to-value mortgages. The availability of 95% and even 100% mortgage products has increased substantially, particularly for lower-value regional markets[1]. This expansion addresses one of the primary barriers facing first-time buyers: deposit accumulation.

Working with chartered surveyors across London and surrounding regions, professionals report that lenders are processing applications more efficiently in 2026, though valuation scrutiny remains intense—particularly for high LTV mortgages where the lender's risk exposure is greatest.

Buyer Sentiment and Market Activity

Market confidence indicators show encouraging trends. The RICS survey reveals that buyer enquiry sentiment is improving, with the net balance for new buyer enquiries at -15% in January 2026, up from -21% in October 2025[3]. While still negative, this improvement indicates a potential turning point in market confidence.

More tellingly, long-term sales activity expectations have reached their strongest level since December 2024, with +35% net balance of RICS survey respondents anticipating increased sales activity throughout 2026[3]. This forward-looking optimism suggests that property professionals expect the first-time buyer resurgence to strengthen as the year progresses.

Understanding Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements

Why Accurate Valuations Matter More Than Ever

In the current market environment, property valuations serve multiple critical functions that extend beyond simple price determination. For first-time buyers operating with minimal deposits and maximum leverage, valuation accuracy directly impacts mortgage approval.

Lenders offering 95% or 100% LTV mortgages face substantial risk exposure. A property valued at £200,000 with a 95% mortgage leaves the lender with just £10,000 equity buffer. If the valuation proves optimistic and the property is actually worth £190,000, the lender faces immediate negative equity. Consequently, lenders scrutinise valuations intensively, often commissioning additional surveys or applying conservative adjustments when uncertainty exists.

For buyers, an under-valuation can derail a purchase entirely. If a buyer agrees to pay £250,000 but the mortgage valuation comes in at £240,000, they must either negotiate a price reduction, find an additional £10,000 deposit, or abandon the purchase. In competitive regional markets where multiple first-time buyers compete for limited stock, this can mean losing a desired property.

Conversely, over-valuations expose buyers to financial risk. Paying above true market value means starting homeownership with negative equity—a precarious position if circumstances require selling within the first few years.

Key Valuation Challenges in Regional First-Time Buyer Markets

Regional markets present distinct valuation challenges compared to established London submarkets. In areas like West London or Central London, extensive transaction data and mature market dynamics facilitate comparables-based valuations. Regional markets often lack this data density.

Limited comparable transactions represent the primary challenge. In a northern city neighbourhood experiencing renewed first-time buyer interest, recent sales may be sparse. Properties that have sold might differ significantly in condition, size, or specification from the subject property. Surveyors must exercise professional judgement to adjust comparable evidence appropriately.

Property condition variability also complicates regional valuations. First-time buyer properties frequently include Victorian terraces, 1930s semi-detached houses, and post-war builds—each with distinct maintenance profiles and potential defects. A surveyor must assess not just current condition but also deferred maintenance liabilities that affect value.

Rapid market shifts in emerging first-time buyer hotspots create temporal challenges. When buyer demand increases quickly in a previously quiet market, recent comparable sales may not reflect current market dynamics. Surveyors must balance historical evidence with current market sentiment—a nuanced judgement requiring local market expertise.

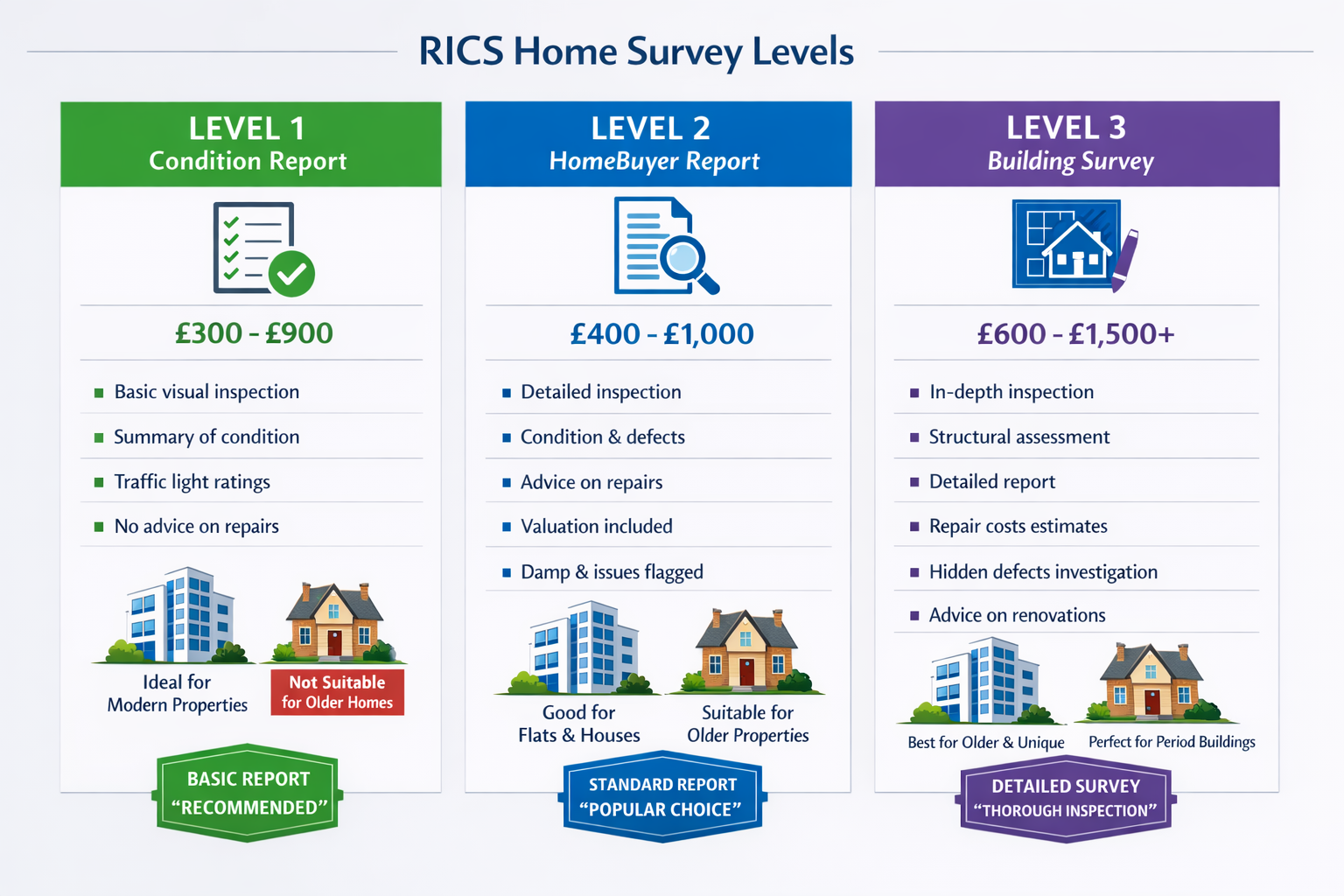

RICS Survey Levels: Choosing the Right Assessment

The Royal Institution of Chartered Surveyors (RICS) defines three survey levels, each suited to different property types and buyer needs. Understanding these options is fundamental to Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements.

RICS Home Survey Level 1 (Condition Report) provides a basic property assessment, typically costing £300-£900[4]. This survey identifies urgent defects and potential legal issues but offers limited detail. It's most appropriate for newer properties in good condition where the buyer primarily needs mortgage valuation confirmation. For most first-time buyer properties—often older stock with potential maintenance issues—Level 1 surveys provide insufficient information.

RICS Home Survey Level 2 (HomeBuyer Report) represents the optimal choice for most first-time buyers, generally costing £400-£1,000[4]. This survey includes:

- Traffic light condition ratings (1-3 scale) for major property elements

- Identification of defects requiring urgent attention

- Advice on necessary repairs and ongoing maintenance

- Market valuation and reinstatement cost assessment

- Guidance on legal issues affecting value

Level 2 surveys suit conventional properties in reasonable condition—the typical first-time buyer purchase. They provide sufficient detail to inform the purchase decision and satisfy mortgage lender requirements without the expense of comprehensive structural analysis.

RICS Home Survey Level 3 (Building Survey) offers the most detailed assessment, typically costing £600-£1,500+[4]. This comprehensive survey includes detailed analysis of construction, materials, and condition, with extensive advice on repairs and maintenance. Level 3 surveys are most appropriate for older properties, those in poor condition, properties requiring significant alteration, or unusual construction types.

For first-time buyers in regional markets purchasing standard property types, Level 2 represents the optimal balance of cost and information quality. Buyers can supplement this with specialist surveys (such as a roof survey if specific concerns exist) rather than commissioning a full Level 3 survey.

Surveyor Tactics for Accurate First-Time Buyer Property Valuations

Comparables Analysis in Competitive Regional Markets

Effective comparables analysis requires systematic methodology, particularly in regional markets with limited transaction data. Professional surveyors employ several tactics to ensure accuracy:

Geographic radius adjustment involves expanding the search area strategically. While ideal comparables come from the immediate neighbourhood, surveyors may need to consider properties within a 1-2 mile radius in areas with sparse transactions. However, this requires careful adjustment for location-specific factors like school catchments, transport links, and neighbourhood desirability.

Temporal weighting recognises that older comparables may not reflect current market conditions. In a rising market, surveyors adjust older sale prices upward; in declining markets, downward adjustments apply. The RICS guidance suggests that comparables beyond six months old require careful consideration and adjustment[3].

Specification normalisation is critical when comparable properties differ from the subject property. A surveyor must adjust for differences in:

- Size: Price per square foot/metre provides a baseline, but non-linear relationships exist (larger properties typically command lower per-unit prices)

- Condition: Properties in superior condition command premiums; those requiring work sell at discounts

- Specification: Modern kitchens, bathrooms, double glazing, central heating, and period features all affect value

- Outdoor space: Gardens, parking, and garages add significant value in regional markets

Professional surveyors working in areas like Surrey or Berkshire develop detailed adjustment matrices based on local market evidence, ensuring consistency across valuations.

Assessing Property Condition and Maintenance Liabilities

Property condition assessment directly impacts valuation through two mechanisms: immediate repair costs and deferred maintenance liabilities. Surveyors must evaluate both to provide accurate valuations.

Immediate defects requiring urgent attention typically result in direct valuation reductions. Examples include:

- Structural movement requiring underpinning (£10,000-£50,000+)

- Roof failures requiring replacement (£5,000-£15,000 for typical first-time buyer properties)

- Rising or penetrating damp requiring remediation (£2,000-£10,000)

- Electrical systems requiring complete rewiring (£3,000-£8,000)

- Boiler or heating system failures (£2,000-£4,000)

Surveyors typically deduct estimated repair costs plus a contingency (often 10-20%) from the value that would apply if the property were in good condition. This reflects both the actual repair cost and the inconvenience/risk to the buyer.

Deferred maintenance presents a more nuanced challenge. Properties with serviceable but aging systems (15-year-old boiler, 20-year-old windows, aging roof covering) don't require immediate repair but face predictable replacement costs within 5-10 years. Surveyors consider this when assessing value, though the impact is less direct than immediate defects.

For first-time buyers in regional markets, condition assessment is particularly critical because many are purchasing older stock. A Victorian terrace in Richmond or a 1930s semi in Bromley may offer excellent value but require careful assessment of period-specific issues like solid wall construction, original single-glazed windows, and aging services.

Market Sentiment and Forward-Looking Analysis

Professional valuations in 2026 must incorporate forward-looking market analysis alongside historical comparables. This is particularly important in regional markets experiencing rapid changes in first-time buyer demand.

Surveyors consider several forward-looking factors:

Local economic indicators including employment trends, major employer announcements, and infrastructure investments. A regional city securing a major employer or transport investment may experience strengthening demand that isn't yet fully reflected in historical transaction data.

Supply-demand dynamics are assessed through market activity metrics. Rising viewing numbers, decreasing time-on-market, and increasing offer-to-asking-price ratios all indicate strengthening demand. The RICS survey data showing +35% net balance expecting increased sales activity[3] suggests strengthening conditions that may support values above purely historical comparables.

Mortgage availability in the specific local market affects achievable prices. Areas where lenders offer competitive high-LTV products typically see stronger first-time buyer demand and correspondingly firmer values.

Comparable properties currently marketed provide insight into seller expectations and buyer alternatives. A surveyor must consider whether the subject property offers competitive value relative to current market alternatives, not just historical sales.

Professional RICS registered valuers synthesise these factors to provide valuations that reflect both current market evidence and reasonable forward-looking expectations—critical for first-time buyers making long-term financial commitments.

Technology-Enhanced Valuation Techniques

Modern surveying increasingly incorporates technology to enhance accuracy and efficiency. Several innovations are particularly relevant to Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements:

Digital measurement tools including laser distance measurers and digital floor plan applications ensure accurate property dimensions. Precise measurements are essential for comparables analysis based on price per square foot/metre.

Thermal imaging cameras identify hidden defects like insulation gaps, moisture ingress, and heating system inefficiencies that affect both property condition and running costs—increasingly important considerations for first-time buyers managing tight budgets.

Drone surveys enable detailed roof inspections without expensive scaffolding access. Drone roof surveys are particularly valuable for properties where roof condition significantly impacts value but access is challenging.

Database analytics platforms aggregate transaction data, market trends, and property characteristics to support comparables analysis. While professional judgement remains essential, these tools help surveyors identify relevant comparables and appropriate adjustments more efficiently.

Digital reporting systems enable surveyors to provide comprehensive reports with annotated photographs, condition ratings, and valuation analysis in accessible formats. This transparency helps first-time buyers understand valuation conclusions and make informed decisions.

Regional Variations: Tactics for Specific Markets

Northern Cities and Emerging First-Time Buyer Hotspots

Regional cities like Preston, Lancaster, and Blackpool are experiencing renewed first-time buyer interest driven by lower absolute price points and stable employment prospects[1]. Valuing properties in these markets requires specific tactical considerations.

Lower price sensitivity to rates characterises these markets. When average property prices range from £150,000-£200,000 rather than £300,000-£400,000, the absolute impact of interest rate changes on monthly payments is proportionally smaller. This creates more stable demand dynamics compared to high-price markets.

University influence in cities like Lancaster creates distinct submarkets. Properties suitable for student accommodation or young professional renters may command premiums in specific neighbourhoods. Surveyors must understand these local dynamics when selecting comparables and assessing value.

Regeneration and infrastructure investment significantly impacts values in regional cities. Areas benefiting from town centre regeneration, transport improvements, or major employer investments may experience rapid value appreciation. Surveyors must balance current comparable evidence with reasonable expectations of future market strengthening.

Property stock characteristics differ from London markets. Regional first-time buyer properties frequently include traditional terraces, semi-detached houses, and ex-local authority properties. Surveyors must understand the specific maintenance profiles and value drivers for these property types.

London and South East Markets

While affordability improvements are less pronounced in London and the South East, these markets remain significant for first-time buyers, particularly in outer boroughs and commuter towns. Surveyors working in areas like South East London, Ealing, or Enfield employ specific tactics:

Leasehold considerations are critical in London markets where many first-time buyer properties are flats. Lease extension valuations become essential when remaining lease terms fall below 80 years. Surveyors must assess both current value and potential lease extension costs that buyers will face.

Service charge and ground rent analysis affects value significantly. Properties with high service charges or onerous ground rent terms command discounts. Surveyors must review lease terms carefully and adjust valuations accordingly.

Transport connectivity drives value differentials in London markets. Properties within walking distance of Underground or Overground stations command substantial premiums. Surveyors must carefully select comparables with similar transport access.

Planning constraints and permitted development affect value in London's constrained market. Properties with potential for loft conversions, extensions, or other improvements command premiums. Surveyors should identify and reflect these value-enhancement opportunities.

Commuter Belt and Satellite Towns

Areas like Watford, Guildford, and Epsom occupy a middle ground—more affordable than inner London but more expensive than northern regional cities. These markets present unique valuation considerations:

Commuting costs versus property costs create trade-offs that affect value. First-time buyers balance lower property prices against higher commuting costs. Surveyors must understand how transport links and commuting patterns affect local demand and values.

School catchments drive significant value premiums in commuter belt markets where families prioritise education. Properties within catchments for high-performing schools may command 10-20% premiums over otherwise identical properties outside catchment areas.

Hybrid working impact has altered commuter belt dynamics since 2020. Reduced commuting frequency has expanded the viable commuting radius, potentially supporting values in previously marginal locations. Surveyors must consider whether this trend is sustainable when assessing values.

Practical Guidance for First-Time Buyers

Preparing for the Valuation Process

First-time buyers can take several steps to facilitate accurate valuations and smooth mortgage approval:

Property information compilation helps surveyors work efficiently. Buyers should gather:

- Energy Performance Certificates (EPCs)

- Building regulations certificates for any works

- Guarantees for recent works (roof, damp-proofing, windows)

- Service charge and ground rent documentation (for leasehold properties)

- Planning permissions for extensions or alterations

Property presentation matters more than many buyers realise. While surveyors assess underlying condition rather than décor, ensuring the property is accessible and well-lit facilitates thorough inspection. Clearing clutter from lofts, basements, and other inspection areas demonstrates transparency and enables comprehensive assessment.

Realistic expectations about value are essential. Buyers should research recent sales of comparable properties using Land Registry data and property portals. Understanding the likely valuation range helps buyers avoid over-bidding in competitive situations.

Early survey commissioning can prevent disappointment. Rather than waiting until after offer acceptance, buyers in competitive markets might commission a survey before making an offer. This identifies any significant defects that affect value and enables informed offer pricing. While this involves upfront cost, it can prevent costly surprises later.

Responding to Valuation Shortfalls

When mortgage valuations come in below the agreed purchase price, buyers face several options:

Price renegotiation is the most direct solution. Armed with the professional valuation, buyers can request a price reduction to the surveyor's assessed value. In the current market where sellers are motivated to complete sales, many will negotiate rather than risk losing the sale.

Additional deposit funding bridges the gap if renegotiation fails. If a property valued at £240,000 was purchased for £250,000, the buyer needs an additional £10,000 deposit. While challenging, family assistance or additional savings may make this feasible for some buyers.

Lender challenge is possible if the buyer believes the valuation is unreasonably conservative. Providing evidence of comparable sales at higher prices may persuade the lender to commission a second valuation. However, this delays the process and incurs additional costs.

Alternative lender approaches may yield different valuations. Different lenders use different surveyors and valuation methodologies. While time-consuming, approaching alternative lenders might result in a valuation that supports the purchase price.

Transaction withdrawal remains an option if the valuation reveals significant concerns. While disappointing, discovering major defects or over-valuation before completion protects buyers from poor financial decisions.

Working with Professional Surveyors

Selecting and working effectively with professional surveyors optimises outcomes:

RICS qualification verification ensures professional competence. All surveyors should be RICS members (MRICS or FRICS) with appropriate professional indemnity insurance. The RICS website provides member verification.

Local market experience is valuable. Surveyors with extensive experience in the specific local market understand property types, common defects, and market dynamics better than generalists. When purchasing in areas like Chiswick or Battersea, selecting surveyors with local expertise yields more accurate valuations.

Clear communication about requirements ensures appropriate service delivery. Buyers should explain their circumstances (first-time buyer, high LTV mortgage, specific concerns) so surveyors can tailor their assessment and reporting accordingly.

Question asking is encouraged. Professional surveyors expect clients to seek clarification about findings, valuations, and recommendations. Understanding the rationale behind valuation conclusions helps buyers make informed decisions.

Report review thoroughness is essential. Buyers should read survey reports completely, not just the valuation figure. Understanding identified defects, maintenance recommendations, and condition ratings provides valuable information for negotiation and future planning.

Future Outlook: Valuation Practices Beyond 2026

Evolving Market Dynamics

The first-time buyer market is likely to continue evolving throughout 2026 and beyond. Several trends will influence Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements:

Continued regional divergence seems probable. While London and the South East face ongoing affordability constraints, regional cities with strong employment and lower absolute prices will likely attract increasing first-time buyer interest. This geographic rebalancing will require surveyors to develop expertise in previously less active markets.

Mortgage product innovation may expand further. The return of 100% LTV mortgages and development of shared equity schemes create new valuation challenges. Surveyors must understand how different mortgage structures affect risk and value assessment.

Energy efficiency focus will intensify as regulatory requirements tighten and energy costs remain significant. Properties with poor energy performance will face increasing value discounts. Surveyors must incorporate energy efficiency assessment more systematically into valuations.

Climate risk considerations are emerging as a valuation factor. Properties in flood risk areas or vulnerable to other climate impacts may face value pressures as insurance costs rise and lender appetite diminishes. Forward-looking valuations must consider these long-term risks.

Regulatory and Professional Developments

The surveying profession continues evolving to meet changing market needs:

Enhanced valuation standards from RICS and other professional bodies will likely emphasise transparency, consistency, and risk assessment. This benefits first-time buyers through more reliable valuations but may increase survey costs.

Technology integration will accelerate. Automated valuation models (AVMs), artificial intelligence, and big data analytics will increasingly supplement professional judgement. However, human expertise remains essential for nuanced assessment of property condition and local market dynamics.

Sustainability reporting may become standard practice. Surveyors might routinely assess and report on energy efficiency, climate resilience, and environmental impact alongside traditional condition and value assessment.

Consumer protection enhancements through clearer reporting standards, standardised terminology, and improved accessibility will help first-time buyers understand survey findings and make informed decisions.

Conclusion

Valuing First-Time Buyer Properties in 2026: Surveyor Tactics Amid Affordability Improvements represents a critical intersection of improving market conditions and professional expertise. As mortgage affordability strengthens and first-time buyers return to the market—particularly in regional cities offering better value—accurate property valuations become the essential gateway to successful homeownership.

The modest house price growth forecast for 2026 (0-2% nationally)[1], combined with stabilising mortgage rates between 3.75% and 4.75%[1], creates a more predictable environment than recent years. However, this stability demands precision: first-time buyers operating with minimal deposits and maximum leverage cannot afford valuation errors that expose them to negative equity or prevent mortgage approval.

Professional surveyors employ sophisticated tactics to navigate the challenges of regional markets, limited comparable data, and varying property conditions. From systematic comparables analysis and detailed condition assessment to forward-looking market analysis and technology-enhanced inspection techniques, these methods ensure valuations reflect true market value while satisfying cautious lender requirements.

For first-time buyers, understanding the valuation process—from selecting the appropriate RICS survey level to preparing properties for inspection and responding to valuation outcomes—transforms a potentially opaque procedure into a manageable component of the purchase journey.

Actionable Next Steps

First-time buyers should:

✅ Research local market conditions using Land Registry data and property portals to understand typical values in target areas

✅ Budget for appropriate surveys (typically RICS Level 2 at £400-£1,000) as an essential investment rather than an optional expense

✅ Select RICS-qualified surveyors with demonstrated local market expertise in the specific area where they're purchasing

✅ Compile property documentation including EPCs, guarantees, and certificates to facilitate efficient surveyor assessment

✅ Maintain realistic expectations about property values based on comparable evidence rather than emotional attachment

✅ Engage early with professional surveyors to understand the valuation process and timeline before committing to purchases

The improving affordability landscape of 2026 offers genuine opportunities for first-time buyers who approach the market with preparation, realistic expectations, and professional guidance. Accurate property valuations—underpinned by expert surveyor tactics adapted to regional market dynamics—provide the foundation for confident, successful homeownership that endures beyond the initial purchase excitement into long-term financial security.

References

[1] Uk Property Market Forecast For 2026 What Buyers Should Expect – https://www.farrellheyworth.co.uk/blog/uk-property-market-forecast-for-2026-what-buyers-should-expect/

[2] House Prices Start 2026 On A Cautious Note What Buyers Should Know – https://arnoldandbaldwin.co.uk/insights/house-prices-start-2026-on-a-cautious-note-what-buyers-should-know

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] What Sort Of Survey Should I Have – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/what-sort-of-survey-should-i-have/