Over 8 million property transactions across England and Wales now carry measurable flood-related value penalties — and that figure is growing [2]. The spring 2026 flood events, which inundated significant stretches of the Thames Valley, the Severn corridor, and parts of Yorkshire, have forced a sharp recalibration of how chartered surveyors approach Level 3 building surveys and formal property valuations. For buyers, sellers, and lenders alike, understanding the valuation impacts of spring 2026 flood events: integrating EA flood maps into Level 3 building surveys is no longer optional — it is a professional and financial necessity.

This article sets out the practical strategies surveyors are using in 2026 to embed Environment Agency (EA) flood data into their assessment frameworks, adjust valuations accordingly, and help clients make genuinely informed decisions.

Key Takeaways 📌

- Properties in high flood-risk zones are experiencing persistent, compounding value discounts that widen with each successive flood event [2].

- EA flood maps must now be cross-referenced at every stage of a Level 3 building survey, not just noted as a caveat.

- Approximately 25% of buyers already factor flood risk data into purchase decisions — a figure projected to reach 50% within a decade [1].

- Flood-resilient features (flood doors, raised electrics, tanking) can partially offset valuation penalties and improve insurability.

- RICS-registered valuers must apply transparent, evidence-based adjustments when flood zone classification affects market value.

Understanding the Post-Spring 2026 Flood Landscape

The spring 2026 events were notable not just for their geographic spread but for their timing. Coming after two consecutive mild winters, many homeowners in Flood Zone 2 and 3 properties had grown complacent. When floodwaters arrived in March and April 2026, the damage — and the market reaction — was swift.

What the EA Flood Maps Now Show

The Environment Agency updates its Risk of Flooding from Rivers and Sea (RoFRS) dataset regularly. Following the spring 2026 events, several postcode areas were reclassified upward, moving from Flood Zone 2 (medium probability: 0.1%–1% annual chance) into Flood Zone 3a (high probability: greater than 1% annual chance). A smaller number of previously unclassified properties were added to Zone 2 for the first time.

Key EA flood map layers surveyors must now consult include:

| EA Data Layer | What It Shows | Relevance to Level 3 Survey |

|---|---|---|

| Risk of Flooding from Rivers & Sea | Flood zone classification | Primary valuation input |

| Surface Water Flood Map | Pluvial flood risk | Often missed in standard checks |

| Historic Flood Map | Past flood extents | Evidence of prior events |

| Flood Storage Areas | Upstream retention zones | Downstream risk indicator |

| Long Term Flood Risk | 20–50 year projections | Climate-adjusted valuations |

"Flood zone reclassification following the spring 2026 events has created a two-tier market in several riverside postcodes — with properties that flooded trading at discounts of 10–18% compared to equivalent unaffected homes on the same street."

Surveyors working across affected areas — including those providing chartered surveying services in Richmond and Twickenham, both historically vulnerable to Thames flooding — report that buyers are arriving at inspections with EA map printouts already in hand.

Valuation Impacts of Spring 2026 Flood Events: Integrating EA Flood Maps into Level 3 Building Surveys — The Surveyor's Methodology

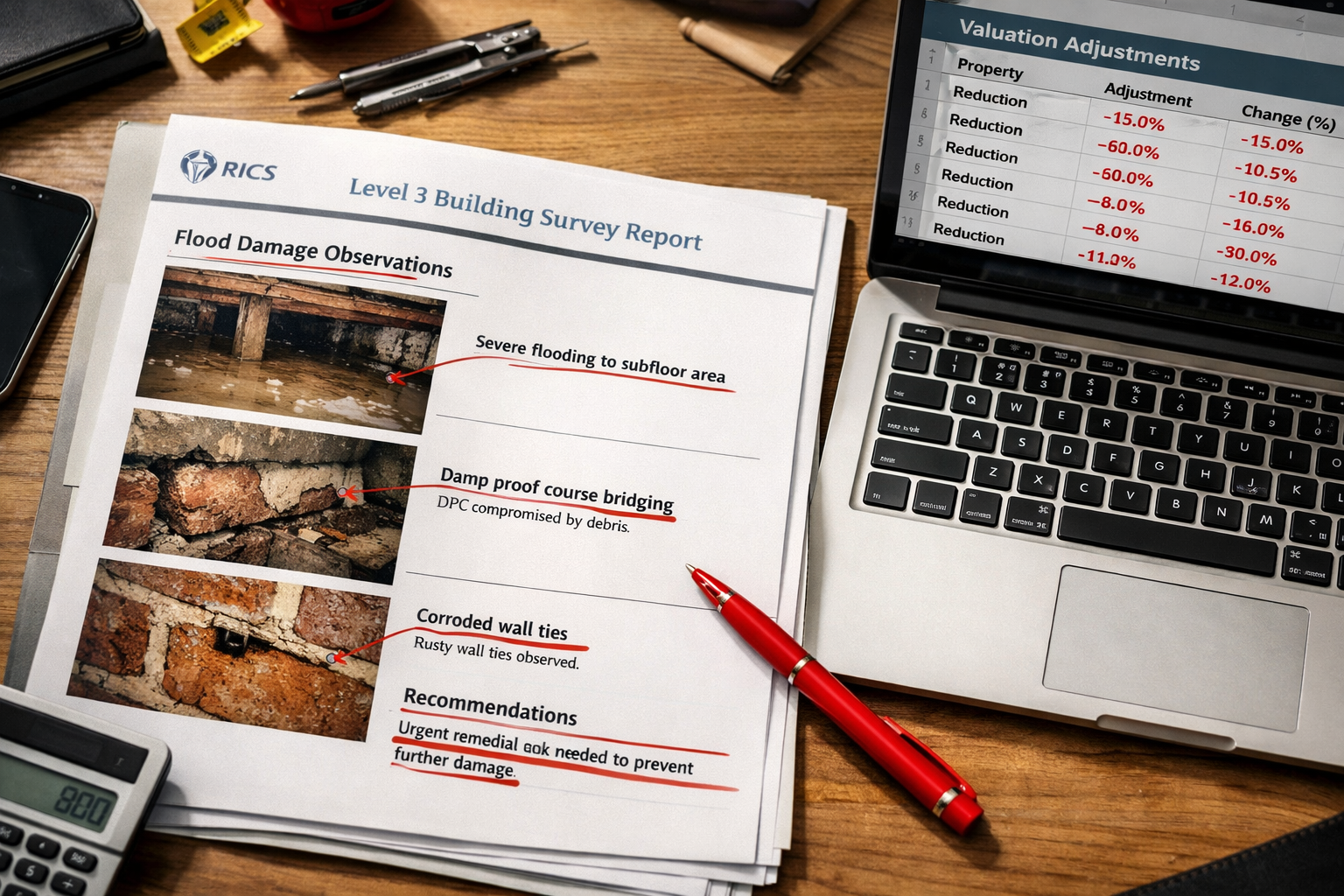

A Level 3 building survey (formerly the RICS Building Survey) is the most thorough inspection available for residential properties. Its scope makes it the natural vehicle for integrating flood risk analysis — but only if the surveyor follows a structured, evidence-based approach.

Step 1: Pre-Inspection EA Data Pull

Before visiting the property, the surveyor should:

- Download the current EA flood zone classification for the specific property address.

- Check the Historic Flood Map to identify whether the site has been inundated previously.

- Review the Surface Water flood layer — many spring 2026 losses occurred in properties not in a river flood zone but vulnerable to overwhelmed drainage.

- Note any recent zone reclassifications that may not yet be reflected in the seller's property information forms.

This pre-inspection research shapes the entire on-site inspection strategy. It is not sufficient to simply note "the property is in Flood Zone 2" in the survey report — the surveyor must investigate the physical implications of that classification.

Step 2: On-Site Physical Assessment

During the Level 3 inspection, flood-specific checks include:

- Subfloor voids and air bricks: Are vents at or below likely flood levels? Have they been fitted with automatic flood vents?

- Damp proof course (DPC) height: Is the DPC above the modelled flood level for a 1-in-100-year event?

- Electrical installations: Are consumer units, sockets, and wiring at or below flood risk height?

- Wall construction and finishes: Evidence of previous flood damage — tide marks, replaced plasterboard, mismatched floor finishes — is often concealed.

- Drainage and outfall: Can the drainage system cope with backflow during a flood event?

- Flood resilience measures: Flood doors, non-return valves, flood barriers, tanked basements.

For properties with complex drainage or structural issues potentially linked to flood saturation, a specific defect report may be commissioned alongside the Level 3 survey to isolate and cost individual problems.

Step 3: Valuation Adjustment — Applying the Evidence

The valuation impacts of spring 2026 flood events: integrating EA flood maps into Level 3 building surveys require surveyors to move beyond qualitative commentary and apply quantified adjustments where the evidence supports them.

Research published in 2025 confirms that flood exposure creates a negative and persistent impact on property values, with effects that compound over time rather than recovering to pre-flood levels [2]. Homes with lower flood risk have shown faster price appreciation over the past decade, with the gap widening markedly in the past three years [1].

Practical adjustment factors for 2026 valuations:

- 🔴 Flood Zone 3a, no resilience measures, post-2026 event: Discount range 12–20% against comparable unaffected properties.

- 🟠 Flood Zone 3a with documented resilience features: Discount range 5–10%.

- 🟡 Flood Zone 2, no prior flooding recorded: Discount range 2–6%, with sensitivity note.

- 🟢 Flood Zone 2, resilience measures installed, insurability confirmed: Minimal or nil adjustment, with commentary.

These ranges are indicative. The RICS Red Book (Global Standards) requires that adjustments be supported by comparable evidence drawn from the local market. Surveyors should document their comparable selection methodology carefully, particularly where post-spring 2026 sales data is limited.

For clients needing a formal RICS-compliant valuation for lending or legal purposes, a Red Book valuation provides the structured framework within which flood risk adjustments must be transparently reported.

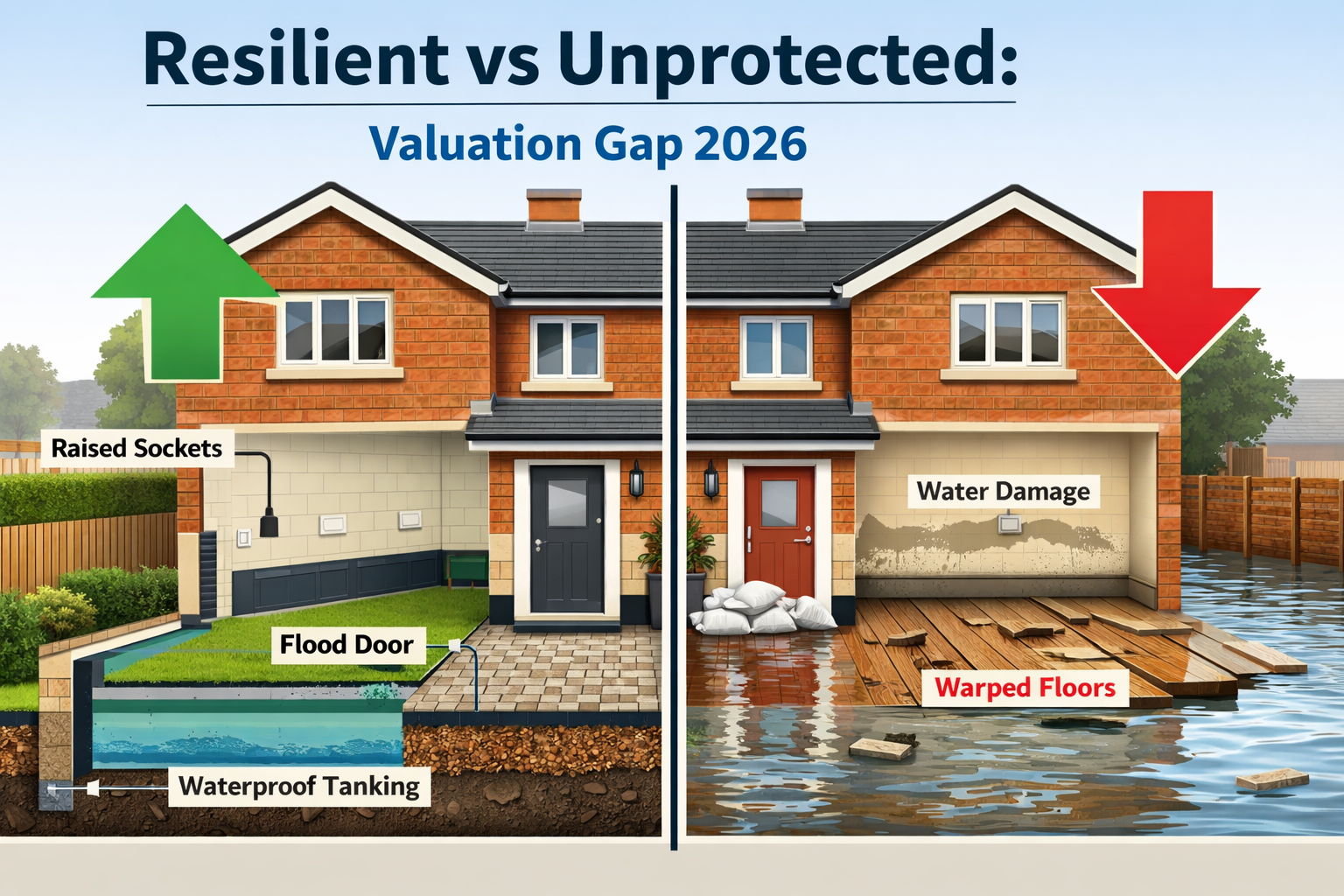

How Flood-Resilient Features Affect Property Values in 2026

The post-spring 2026 market is not uniformly negative for flood-zone properties. A growing body of evidence — and surveyor experience on the ground — shows that documented flood resilience can meaningfully offset valuation penalties and, critically, restore insurability.

Resilience Features That Add Value

| Feature | Estimated Value Impact | Notes |

|---|---|---|

| Flood doors (certified) | +2–4% vs unprotected equivalent | Must be professionally fitted and documented |

| Raised electrical installation | +1–3% | Particularly valued by mortgage lenders |

| Non-return drainage valves | +1–2% | Reduces surface water ingress risk |

| Tanked basement/lower ground | +3–6% | Significant for below-grade habitable space |

| Permeable driveway surfacing | +0.5–1% | Contributes to surface water management |

| Flood-resilient plaster and finishes | +1–2% | Reduces reinstatement cost, lowers insurance premium |

"A property in Flood Zone 3a with a full suite of certified resilience measures sold in April 2026 at just 4% below its unaffected comparables — compared to a 16% discount for an identical unprotected property on the same road."

Surveyors should request documentation for all resilience measures, including installation certificates, product specifications, and any flood risk assessment reports prepared under the National Planning Policy Framework (NPPF). Undocumented or poorly installed measures carry little weight in a formal valuation.

The Insurance Dimension 🏦

Flood zone classification directly affects buildings insurance availability and premium levels. The Flood Re scheme provides a reinsurance backstop for eligible properties, but it excludes homes built after 2009, leasehold flats in multi-storey blocks, and commercial properties. Post-spring 2026, several insurers have tightened eligibility criteria for properties newly reclassified to Flood Zone 3a.

Surveyors should note insurance status and Flood Re eligibility in their Level 3 reports. Where insurability is uncertain, buyers should be directed to obtain written insurance quotations before exchange of contracts. This is especially relevant for reinstatement cost valuations, where the rebuild figure must reflect the full cost of flood-resilient reinstatement, not merely standard construction rates.

Valuation Impacts of Spring 2026 Flood Events: Integrating EA Flood Maps into Level 3 Building Surveys — Buyer Guidance and Market Implications

The spring 2026 events have accelerated a shift in buyer behaviour that was already underway. Research shows that around one in four buyers now actively considers flood data when selecting a property [1], and projections suggest this will rise to one in two within ten years [1]. Surveyors, valuers, and estate agents who fail to engage with this shift risk providing advice that is materially incomplete.

What Buyers Should Ask Before Purchasing in a Flood Zone

✅ What is the current EA flood zone classification — and has it changed since the spring 2026 events?

✅ Has the property flooded before? (Check the EA Historic Flood Map and ask the seller directly via the TA6 property information form.)

✅ What flood resilience measures are installed, and are they documented?

✅ Is the property eligible for Flood Re insurance?

✅ What is the estimated reinstatement cost if flooding occurs?

✅ Has a Level 3 building survey been commissioned — not just a mortgage valuation?

A homebuyer report versus a building survey comparison is worth reviewing before commissioning any inspection: for flood-zone properties, the Level 3 survey's depth of investigation is almost always warranted.

Lender Attitudes in 2026

Mortgage lenders have become noticeably more cautious following the spring 2026 events. Several high-street lenders have introduced:

- Mandatory flood risk questionnaires for properties in Flood Zones 2 and 3.

- Retention clauses where flood resilience works are required before full mortgage advance.

- Reduced loan-to-value (LTV) ratios for properties in Flood Zone 3a without confirmed Flood Re eligibility.

Valuers instructed by lenders must ensure their reports address flood risk explicitly. A vague reference to "the property being in a flood zone" is no longer sufficient — lenders expect commentary on resilience measures, insurance status, and the surveyor's view on marketability and saleability in the current climate.

For properties where value has been affected by a past flood event, a retrospective valuation may be required to establish the pre-event market value for insurance or legal purposes.

Geographic Hotspots in 2026

Areas where the valuation impacts of spring 2026 flood events are most acutely felt include:

- Thames Valley: Properties in Richmond, Twickenham, and Barnes saw repeated inundation.

- South-West London: Putney and Battersea riverside properties experienced tidal surge effects.

- Surrey commuter belt: Esher and Leatherhead recorded significant Mole Valley flooding.

Surveyors operating in these areas should maintain up-to-date local comparable databases that capture post-spring 2026 transaction evidence, noting flood zone status as a standard variable in every comparable analysis.

Conclusion: Actionable Next Steps for Surveyors, Buyers, and Owners

The valuation impacts of spring 2026 flood events — and the imperative of integrating EA flood maps into Level 3 building surveys — represent one of the most significant shifts in residential property assessment practice in recent years. The evidence is clear: flood exposure creates lasting value penalties [2], buyer awareness is rising fast [1], and lenders are tightening their requirements in response.

For surveyors and valuers:

- Embed EA flood map consultation as a mandatory pre-inspection step, not an afterthought.

- Quantify valuation adjustments with reference to post-spring 2026 comparable evidence.

- Report on resilience measures, insurance status, and Flood Re eligibility in every Level 3 survey for flood-zone properties.

- Consider commissioning a specific defect report where flood-related structural or drainage issues require deeper investigation.

For buyers:

- Commission a Level 3 building survey for any property in Flood Zone 2 or 3 — the cost is negligible against the financial exposure.

- Obtain written insurance quotations before exchange.

- Request full documentation of any flood resilience measures claimed by the seller.

For existing owners in flood zones:

- Invest in certified resilience measures — they demonstrably reduce valuation discounts and improve insurability.

- Ensure reinstatement cost valuations reflect flood-resilient rebuild specifications.

- Keep all flood resilience documentation in order for future sale or remortgage.

Flood risk is now a permanent feature of the UK property landscape. Surveyors who integrate EA data rigorously and communicate its valuation implications clearly are providing a service that is not just professionally sound — it is genuinely essential.

References

[1] Flood Maps Changing Home Sales – https://www.realtor.com/advice/sell/flood-maps-changing-home-sales/

[2] Full – https://www.frontiersin.org/journals/environmental-economics/articles/10.3389/frevc.2025.1615802/full

[3] Nhess 26 571 2026 – https://nhess.copernicus.org/articles/26/571/2026/nhess-26-571-2026.pdf