The Environment Agency's latest projections reveal a sobering reality: by 2050, one in three UK properties will face serious flood risk, up from the current one in six[5]. This escalating threat demands a fundamental shift in how surveyors approach property assessments in vulnerable regions. Level 3 Surveys for Flood Risk Properties: Integrating EA Data and Valuation Discounts in Vulnerable UK Regions represents not just a technical evolution, but a professional imperative for chartered surveyors operating in 2026's increasingly climate-conscious property market.

As flood events intensify and insurance premiums soar in high-risk zones, property valuations face unprecedented downward pressure. Surveyors must now seamlessly integrate Environment Agency flood mapping, resilience assessments, and market-adjusted valuations into comprehensive Level 3 reports. This guide equips professionals with the methodologies, data integration techniques, and valuation frameworks essential for delivering authoritative flood risk assessments.

Key Takeaways

- Level 3 surveys now mandate flood resilience assessments as part of environmental evaluation protocols, particularly in EA-designated flood zones

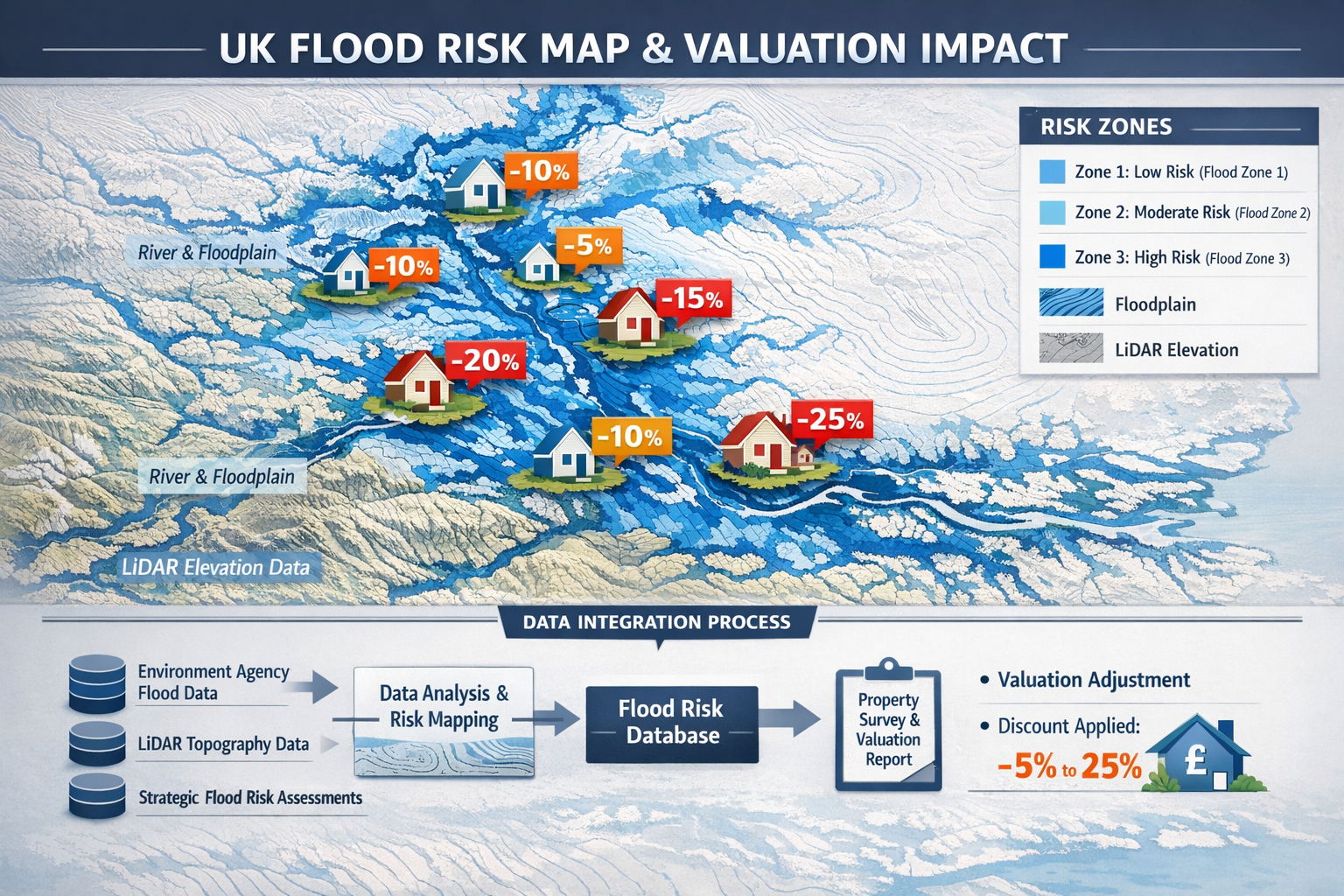

- Valuation discounts for flood-affected properties typically range from 5-25% depending on risk classification and resilience measures installed

- Environment Agency flood maps and LiDAR data integration provides essential baseline information for comprehensive property risk profiling

- EPC ratings increasingly reflect flood vulnerability, with resilience improvements contributing to enhanced energy efficiency scores

- Professional indemnity considerations require surveyors to explicitly document flood risk findings and valuation adjustments in all high-risk properties

Understanding Level 3 Building Surveys in Flood-Prone Contexts

What Defines a Level 3 Survey?

Level 3 building surveys represent the most comprehensive property inspection available to UK buyers and owners. Unlike basic valuations or Level 2 HomeBuyer reports, these detailed assessments examine every accessible aspect of a property's construction, condition, and environmental context. The scope explicitly includes "energy efficiency and environmental issues (such as flooding or contamination)"[1], making them the appropriate choice for properties in flood-vulnerable regions.

Key characteristics of Level 3 surveys include:

- 🏠 Comprehensive structural analysis of all building elements

- 📊 Detailed defect identification with severity ratings

- 🔍 Investigation of hidden or hard-to-access areas

- 💰 Cost estimates for identified repairs and improvements

- 🌍 Environmental risk assessment including flood vulnerability

- 📋 Extensive photographic documentation

These surveys typically cost between £630-£1,500[3], with pricing influenced by property size, complexity, and location. For flood-risk properties, the investment proves invaluable given the potential for significant valuation adjustments and remediation costs.

When Level 3 Surveys Become Essential for Flood Risk Properties

Level 3 surveys are specifically recommended for "complex, larger, older properties, listed buildings, and those where structural integrity may be in doubt"[6]. Flood-affected properties frequently meet multiple criteria, as water ingress compromises structural elements, accelerates deterioration, and creates hidden defects.

Properties requiring mandatory Level 3 assessment include:

- Homes in EA Flood Zone 2 or 3 with historical flooding events

- Properties near watercourses within 250 meters of rivers or coastlines

- Older buildings (pre-1950) lacking modern flood resilience features

- Properties with visible flood damage including damp, subsidence, or foundation issues

- Buildings where insurance searches reveal elevated premiums or coverage restrictions

When environmental searches identify flood risk, specialist flood risk surveys become necessary as a distinct service[4]. However, integrating these findings into the broader Level 3 assessment creates a cohesive understanding of property condition, value impact, and remediation priorities. For guidance on selecting the appropriate survey level, consult our resource on what survey you need.

Integrating Environment Agency Data into Level 3 Survey Protocols

Accessing and Interpreting EA Flood Maps

The Environment Agency maintains the UK's most authoritative flood risk database, freely accessible through their online mapping service. Surveyors conducting Level 3 assessments must systematically integrate this data into their inspection protocols and final reports.

Essential EA data sources include:

-

Flood Zone Classifications

- Zone 1: Low probability (<0.1% annual chance)

- Zone 2: Medium probability (0.1-1% annual chance)

- Zone 3: High probability (>1% annual chance)

-

Flood Risk from Rivers and Sea – Historical event data and predictive modeling

-

Surface Water Flood Risk – Increasingly critical as drainage systems face capacity challenges

-

LiDAR Topographic Data – Precise elevation mapping revealing natural water flow patterns[4]

-

Strategic Flood Risk Assessments (SFRAs) – Local authority planning documents detailing regional vulnerability[4]

Surveyors should document the specific flood zone classification, annual probability percentages, and historical flood events within 500 meters of the subject property. This baseline establishes the environmental context for all subsequent observations.

Conducting On-Site Flood Resilience Assessments

Beyond desktop data review, Level 3 surveys for flood-risk properties demand systematic on-site evaluation of existing resilience measures and vulnerability factors. This assessment directly informs valuation adjustments and remediation recommendations.

Critical inspection elements include:

Exterior Assessment:

- Ground levels and drainage gradients

- Flood defense installations (barriers, gates, airbrick covers)

- Foundation type and damp-proof course condition

- External wall materials and permeability

- Drainage system capacity and condition

- Distance to watercourses and natural flood paths

Interior Assessment:

- Evidence of historical water ingress (staining, tide marks)

- Electrical installation height (sockets, consumer units)

- Heating system vulnerability (boiler location, pipework)

- Floor construction and sub-floor ventilation

- Internal drainage and sump pump installations

- Water-resistant materials in high-risk areas

Structural Implications:

- Foundation movement or subsidence related to water damage

- Wall tie corrosion in cavity walls

- Timber decay in floor joists and structural members

- Masonry deterioration from salt crystallization

Detailed photographic documentation of these elements strengthens the evidential basis for valuation adjustments and provides clients with clear visual references for remediation priorities. For complex structural concerns, engaging residential structural engineers may be necessary.

Incorporating Climate Projections and Future Risk

The 2026 surveying landscape requires forward-looking risk assessment that extends beyond current flood zone classifications. Climate change projections indicate substantial increases in flood frequency and severity across vulnerable UK regions[5].

Professional Level 3 reports should address:

- 30-year risk horizon – Relevant for mortgage lending and long-term ownership

- Climate change allowances – EA guidance on increased rainfall intensity and sea level rise

- Changing flood zone classifications – Properties currently in Zone 2 may transition to Zone 3

- Infrastructure resilience – Adequacy of local flood defenses and drainage systems

- Insurance availability trends – Market withdrawal from highest-risk areas

This forward-looking analysis enables clients to make informed decisions about property suitability, anticipated holding costs, and long-term value trajectories.

Calculating Valuation Discounts for Flood Risk Properties in Vulnerable UK Regions

Market Evidence and Discount Methodologies

Flood risk demonstrably impacts property values, though quantifying the precise discount requires nuanced analysis of multiple factors. Market evidence from recent transactions in comparable flood-affected areas provides the most reliable baseline.

Typical valuation discount ranges:

| Flood Risk Category | Discount Range | Key Factors |

|---|---|---|

| Zone 2 (Medium Risk) | 5-12% | Insurance availability, historical events, resilience measures |

| Zone 3 (High Risk) | 10-25% | Frequency of events, insurance costs, market sentiment |

| Zone 3 + Recent Flooding | 20-35% | Stigma effect, limited buyer pool, lender reluctance |

| Uninsurable Properties | 30-50%+ | Severely restricted market, cash buyers only |

These ranges reflect 2026 market conditions where flood awareness has reached unprecedented levels among buyers, lenders, and insurers. Surveyors must justify specific discount percentages through:

- Comparable sales analysis – Recent transactions of similar properties in equivalent flood zones

- Insurance cost differentials – Annual premium increases compared to low-risk equivalents

- Remediation cost deductions – Capital required for flood resilience improvements

- Market absorption rates – Extended marketing periods in high-risk areas

- Lender appetite – Reduced loan-to-value ratios or outright lending restrictions

For comprehensive valuation services incorporating flood risk adjustments, professional RICS valuation expertise ensures defensible market assessments.

Adjusting for Resilience Measures and Mitigation

Properties with professionally installed flood resilience measures command premium valuations within their risk category. Level 3 surveys must identify and evaluate these improvements when calculating net valuation impact.

Value-enhancing resilience measures:

Passive Defenses (5-8% value recovery):

- Raised electrical installations above predicted flood levels

- Flood-resistant doors and airbrick covers

- Non-return valves on drainage systems

- Water-resistant floor and wall finishes

- Elevated heating systems and white goods

Active Defenses (8-12% value recovery):

- Automatic flood barriers and gates

- Sump pump systems with battery backup

- Property-level flood warning systems

- Landscaping modifications directing water away

- Enhanced drainage capacity installations

Structural Modifications (10-15% value recovery):

- Raised floor levels throughout ground floor

- Waterproof tanking to walls and floors

- Amphibious foundation systems

- Complete re-engineering of ground floor layout

The cumulative effect of comprehensive resilience measures can reduce the net valuation discount by 50-70%, transforming a property from "high risk" to "adequately protected" in market perception.

Integration with EPC Ratings and Energy Efficiency

The intersection of flood resilience and energy performance creates unique valuation considerations in 2026's environmentally conscious market. Flood-resistant materials and construction methods often enhance thermal performance, while necessary ventilation for flood resilience may compromise insulation effectiveness.

EPC implications of flood resilience:

- Improved ratings – Solid concrete floors and water-resistant insulation materials

- Reduced ratings – Increased ventilation requirements and moisture management systems

- Neutral modifications – Raised electrical installations and mechanical equipment

Surveyors should explicitly address EPC implications within Level 3 reports, as energy efficiency increasingly influences buyer decisions and property values. Properties achieving improved EPC ratings despite flood risk may experience reduced valuation discounts compared to less efficient equivalents.

The relationship between flood resilience and energy performance represents an emerging area of professional expertise, requiring surveyors to understand building physics, sustainable construction methods, and regulatory requirements under Part C (Site Preparation and Resistance to Contaminants and Moisture) and Part L (Conservation of Fuel and Power) of Building Regulations.

Regional Variations: Vulnerable UK Areas Requiring Enhanced Assessment

High-Risk Regions and Local Market Dynamics

Flood risk distribution across the UK exhibits significant regional variation, with certain areas experiencing acute vulnerability that demands specialized surveying approaches and valuation methodologies.

Priority regions for enhanced Level 3 flood assessment:

South East England:

- Thames Valley and tributaries

- Coastal Sussex and Kent

- Surrey river corridors

- Market impact: 15-20% baseline discount in Zone 3 areas

For properties in these regions, our chartered surveyors in Surrey provide specialized flood risk assessment expertise.

South West England:

- Somerset Levels

- Devon and Cornwall coastal areas

- Severn Estuary regions

- Market impact: 12-18% baseline discount with insurance challenges

Yorkshire and Humber:

- River Ouse, Aire, and Calder catchments

- Hull and East Riding coastal zones

- Market impact: 10-15% baseline discount, improving with defenses

North West England:

- Cumbria lake districts

- Lancashire river systems

- Greater Manchester urban flooding

- Market impact: 8-14% baseline discount, variable by micro-location

East Anglia:

- Norfolk Broads

- Cambridgeshire Fens

- Essex coastal erosion zones

- Market impact: 12-20% baseline discount with increasing climate risk

Regional market dynamics significantly influence valuation impacts beyond pure flood probability. Areas with established flood defense infrastructure, community resilience programs, and strong local markets demonstrate reduced discounts compared to regions experiencing repeated events without adequate protection.

Local Authority Planning Policies and Development Restrictions

Strategic Flood Risk Assessments conducted by local planning authorities establish development policies that directly impact property values and future use potential. Level 3 surveys should reference relevant planning constraints affecting the subject property.

Critical planning considerations:

- Sequential Test compliance – Restrictions on extensions or substantial alterations

- Exception Test requirements – Mandatory flood risk assessments for planning applications

- Permitted development limitations – Reduced rights in high-risk flood zones

- Future development potential – Impact on property value for homes with extension possibilities

Properties in areas with restrictive flood-related planning policies face additional valuation pressure beyond immediate flood risk, as future flexibility becomes constrained. Surveyors should explicitly document these restrictions within Level 3 reports to ensure clients understand long-term implications.

Professional Standards and Liability Considerations

RICS Guidelines for Flood Risk Reporting

The Royal Institution of Chartered Surveyors provides specific guidance on environmental risk assessment within property surveys. Compliance with these standards protects surveyors from professional liability while ensuring clients receive comprehensive information.

Key RICS requirements include:

- Explicit flood zone identification in executive summaries

- Clear valuation impact statements quantifying flood-related discounts

- Recommendation for specialist assessments when risk exceeds surveyor expertise

- Photographic evidence of flood vulnerability factors

- Future risk commentary addressing climate change projections

Surveyors should maintain detailed working papers documenting EA data sources, comparable sales evidence, and reasoning behind specific valuation adjustments. This documentation proves essential if valuations are challenged by clients, lenders, or in legal proceedings.

For comprehensive valuation services meeting RICS standards, engaging RICS registered valuers ensures professional compliance and defensible assessments.

Insurance and Lender Requirements

The mortgage lending landscape for flood-risk properties has evolved substantially, with lenders imposing stringent requirements for properties in high-risk zones. Level 3 surveys must address these requirements to facilitate successful transactions.

Lender considerations affecting valuations:

- Reduced loan-to-value ratios – Typically 75-85% maximum in Zone 3 areas

- Mandatory flood insurance – Properties must demonstrate insurability

- Retention of funds – Lenders may withhold amounts pending resilience improvements

- Specialist lender referrals – Mainstream lenders withdrawing from highest-risk areas

- Valuation monitoring – Enhanced scrutiny of surveyor assessments in flood zones

Surveyors should explicitly state whether properties meet typical lending criteria or require specialist mortgage products. This transparency enables clients to understand financing implications before committing to purchases.

The Flood Re scheme provides insurance backstop for properties built before 2009, but properties constructed after this date face open market insurance pricing that can prove prohibitive. Level 3 reports should clarify Flood Re eligibility as this substantially affects ongoing ownership costs and property marketability.

Practical Implementation: Delivering Comprehensive Level 3 Flood Risk Reports

Report Structure and Essential Content

Effective Level 3 surveys for flood-risk properties require structured reporting that clearly communicates risk, valuation impact, and remediation priorities to diverse stakeholders including buyers, lenders, insurers, and legal advisors.

Recommended report structure:

Executive Summary:

- Flood zone classification and annual probability

- Overall property condition rating

- Valuation impact statement (percentage discount)

- Critical recommendations requiring immediate action

Environmental Risk Section:

- Detailed EA data integration and mapping

- Historical flood events affecting the property

- On-site resilience assessment findings

- Climate change projections and future risk

- Insurance availability and cost implications

Structural Assessment Section:

- Flood-related defects and deterioration

- Foundation condition and movement analysis

- Damp and moisture ingress evaluation

- Timber condition in flood-vulnerable areas

Valuation Section:

- Comparable sales analysis in similar flood zones

- Specific discount calculation methodology

- Resilience measure valuation adjustments

- Market absorption and liquidity considerations

Recommendations Section:

- Priority resilience improvements with cost estimates

- Maintenance requirements for flood defenses

- Specialist referrals (structural engineers, flood consultants)

- Planning considerations for future modifications

This comprehensive structure ensures all stakeholders receive the information necessary for informed decision-making while protecting surveyors through thorough documentation.

Cost-Benefit Analysis of Remediation Measures

Clients require clear guidance on whether flood resilience investments prove financially justified given property values and ongoing ownership intentions. Level 3 reports should provide this analysis.

Remediation cost-benefit framework:

| Measure | Typical Cost | Value Recovery | Payback Period |

|---|---|---|---|

| Raised electrics | £2,000-£4,000 | £5,000-£8,000 | Immediate |

| Flood barriers | £3,000-£8,000 | £8,000-£15,000 | Immediate |

| Sump pump system | £2,500-£5,000 | £6,000-£10,000 | Immediate |

| Floor tanking | £8,000-£15,000 | £15,000-£30,000 | 2-3 years |

| Complete resilience package | £25,000-£50,000 | £50,000-£100,000 | 3-5 years |

These figures reflect 2026 construction costs and market valuations in typical flood-affected UK regions. Surveyors should adjust recommendations based on property value, client circumstances, and long-term ownership intentions.

For properties where remediation costs exceed 15-20% of current market value, surveyors should explicitly question purchase viability unless clients demonstrate specific motivations justifying the investment.

Coordinating with Specialist Consultants

Complex flood risk properties often require multi-disciplinary assessment beyond typical surveyor expertise. Level 3 reports should identify when specialist input becomes necessary and facilitate coordinated assessment.

Specialist referrals to consider:

- Flood risk consultants – Detailed hydraulic modeling and defense design

- Structural engineers – Foundation assessment and remediation design

- Geotechnical specialists – Ground conditions and subsidence risk

- Building services engineers – Mechanical and electrical resilience design

- Insurance brokers – Coverage options and premium negotiations

- Planning consultants – Development potential and restriction analysis

Coordinating these specialists before finalizing Level 3 reports ensures comprehensive assessment and cohesive recommendations. The additional cost proves justified for high-value properties or complex risk scenarios.

Our network includes structural survey specialists who regularly collaborate on flood-affected properties requiring detailed engineering assessment.

Future-Proofing Flood Risk Assessment Practices

Emerging Technologies and Data Sources

The 2026 surveying landscape benefits from technological advances that enhance flood risk assessment accuracy and efficiency. Progressive surveyors integrate these tools into standard Level 3 protocols.

Innovative assessment technologies:

🚁 Drone surveys – Rapid roof and drainage assessment with thermal imaging capabilities. Our drone roof survey services provide detailed aerial documentation.

📱 Mobile GIS applications – Real-time EA data overlay during site inspections

🌡️ Moisture detection technology – Thermal imaging and moisture meters identifying hidden water ingress

📊 Predictive modeling software – Climate change scenario analysis and future risk projection

🗺️ High-resolution LiDAR – Precise topographic analysis revealing micro-drainage patterns

These technologies enable more accurate risk assessment while improving report quality through enhanced visual documentation and data integration.

Regulatory Developments and Market Trends

The UK regulatory environment continues evolving in response to escalating flood risk, with implications for surveying practice and property valuation.

Anticipated 2026-2030 developments:

- Enhanced EPC flood risk disclosure – Integration of flood vulnerability into energy certificates

- Mandatory resilience standards – Building Regulations requiring flood protection in new construction

- Property Flood Resilience (PFR) certification – Standardized assessment and rating schemes

- Expanded Flood Re eligibility – Potential extension to post-2009 properties

- Local authority retrofit programs – Grant funding for resilience improvements in vulnerable areas

Surveyors should monitor these regulatory developments and adjust assessment protocols accordingly. Early adoption of emerging standards positions practices as market leaders while ensuring continued professional relevance.

Conclusion

Level 3 Surveys for Flood Risk Properties: Integrating EA Data and Valuation Discounts in Vulnerable UK Regions represents essential professional competence for chartered surveyors operating in 2026's climate-affected property market. The integration of Environment Agency flood mapping, comprehensive resilience assessment, and evidence-based valuation adjustments transforms standard building surveys into authoritative risk assessments that serve clients, lenders, and insurers.

The escalating flood threat facing UK properties demands systematic approaches that combine desktop data analysis, detailed on-site inspection, forward-looking climate projections, and nuanced market valuation. Surveyors who master these integrated methodologies position themselves as indispensable advisors in transactions involving flood-vulnerable properties.

Actionable Next Steps

For surveying professionals:

- Enhance technical knowledge – Complete CPD training on flood risk assessment and resilience measures

- Establish EA data protocols – Integrate flood mapping into standard pre-inspection procedures

- Build specialist networks – Develop referral relationships with flood consultants and structural engineers

- Update report templates – Incorporate comprehensive flood risk sections and valuation frameworks

- Invest in technology – Adopt moisture detection, thermal imaging, and GIS mapping tools

For property buyers and owners:

- Commission appropriate surveys – Specify Level 3 assessments for any property in EA flood zones

- Review EA flood maps – Independently verify flood risk before property viewings

- Evaluate resilience measures – Assess existing flood defenses and improvement potential

- Confirm insurance availability – Obtain quotes before exchange of contracts

- Consider long-term projections – Evaluate 30-year flood risk trajectories, not just current classifications

For mortgage lenders and insurers:

- Require Level 3 surveys – Mandate comprehensive assessments for all Zone 2 and 3 properties

- Establish valuation guidelines – Provide surveyors with clear discount frameworks

- Incentivize resilience – Offer preferential terms for properties with certified flood protection

- Monitor climate projections – Adjust lending and underwriting criteria based on evolving risk

The convergence of climate change, regulatory evolution, and market awareness creates unprecedented challenges and opportunities in flood-affected property assessment. Surveyors who embrace comprehensive, data-driven methodologies will deliver exceptional client value while building sustainable practices resilient to market changes.

By systematically integrating Environment Agency data, conducting thorough resilience assessments, and applying evidence-based valuation adjustments, Level 3 surveys become powerful tools for informed decision-making in vulnerable UK regions. The professional standards established today will define surveying practice for decades as flood risk becomes an increasingly central consideration in property transactions.

References

[1] Building Survey Level 3 – https://www.propertysolvers.co.uk/services/building-survey-level-3/

[2] Level 3 Building Surveys For First Time Buyers In 2026 Spotting Risks Amid Affordability Improvements – https://nottinghillsurveyors.com/blog/level-3-building-surveys-for-first-time-buyers-in-2026-spotting-risks-amid-affordability-improvements

[3] What Sort Of Survey Should I Have – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/what-sort-of-survey-should-i-have/

[4] Flood Risk Survey Property Purchase – https://www.unda.co.uk/flood-risk-assessments/flood-risk-survey-property-purchase/

[5] What Is Flood Risk Assessment When Is It Required – https://www.surveyorlocal.co.uk/news/post/what-is-flood-risk-assessment-when-is-it-required

[6] Rics Home Survey Level 3 – https://thehousesurveyors.co.uk/rics-home-survey-level-3/