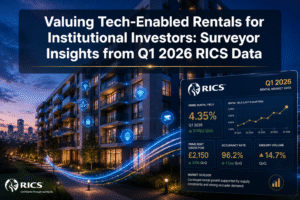

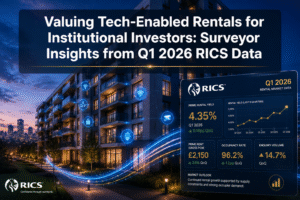

RICS data from February 2026 recorded buyer enquiries at -26% — the weakest reading in over a year — while near-term price expectations fell to -18%. For building surveyors, these numbers are not just market commentary. They are a direct instruction to revisit methodology, sharpen comparable evidence, and communicate uncertainty with greater precision than ever before.

Navigating market caution in Spring 2026: how building surveyors adjust valuations amid geopolitical uncertainty and weakening buyer enquiries is now one of the most pressing professional challenges in the UK property sector. With global trade tensions, persistent inflation concerns, and subdued transaction volumes all converging at once, the valuation profession faces a moment that demands both technical rigour and clear client communication.

This article examines the forces reshaping the Spring 2026 market, the practical steps surveyors are taking to recalibrate their approaches, and what property owners, buyers, and investors need to understand right now.

Key Takeaways 📋

- Buyer enquiries dropped to -26% in February 2026 (RICS), signalling the weakest demand sentiment in over a year.

- Geopolitical uncertainty and interest rate concerns are compressing valuations across both residential and commercial sectors.

- Surveyors must adjust comparable evidence carefully, weighting recent transactions more heavily than older data in a softening market.

- Clear, caveated client communication is essential — clients need to understand that valuations reflect a specific moment in a volatile market.

- Bifurcation is intensifying: premium, well-located properties continue to outperform lower-quality stock, making location and condition more critical than ever.

The Spring 2026 Market Landscape: What the Data Is Telling Surveyors

The property market entering Spring 2026 is best described as cautiously subdued. The RICS February 2026 survey painted a sobering picture: buyer enquiries at -26% and near-term price expectations at -18% represent a market where hesitation has become the dominant mood. Yet beneath these headline figures, the picture is more complex.

Market professionals broadly anticipate that property prices will remain "pretty static" on average in 2026, with transaction levels broadly similar to 2025 [2]. Some analysts, such as James Du Pavey of Charnock Bates, project transaction volumes could increase around 10% in 2026, particularly following key economic events that restore confidence [2]. Others are more conservative, pointing to structural headwinds that will keep activity muted.

💬 "The market is calmer, more realistic and driven by genuine movers rather than speculation." — Industry commentary, Spring 2026 [2]

This "calmer" environment has a direct implication for surveyors: the comparable evidence pool is thinner, and the transactions that do occur are increasingly price-sensitive. Buyers willing to move are doing so where pricing is realistic, not aspirational [2]. For valuers, this means relying on stale comparables from a more active 2024–2025 period carries real risk of overstatement.

Geopolitical Headwinds: The Invisible Pressure on Valuations

Geopolitical uncertainty is not a new variable in property markets, but its intensity in Spring 2026 is particularly acute. Trade policy shifts, energy market volatility, and broader macroeconomic instability have elevated risk perception among investors and lenders alike.

Interest rates, inflation, and capital availability now rank as the top concerns for real estate investors in 2026, with overall optimism measurably lower than in 2025 [1]. These concerns translate directly into:

- Higher mortgage costs suppressing buyer purchasing power

- Lender caution leading to more conservative loan-to-value ratios

- Investor hesitancy reducing demand for commercial and investment-grade property

Land markets are also feeling the pressure. Rural and broader land values are softening alongside policy uncertainty [5], a trend that is rippling into residential development pipelines and affecting new-build valuations.

For surveyors working across London and the South East — from chartered surveyors in Surrey to chartered surveyors in Berkshire — the combination of weakened buyer sentiment and geopolitical noise requires a more forensic approach to every instruction received.

How Building Surveyors Are Recalibrating Valuation Methodologies

Navigating market caution in Spring 2026 means that standard valuation approaches need deliberate adjustment. The core challenge is this: comparable evidence from 12–18 months ago may no longer reflect current market reality, yet recent transaction data is sparse. Surveyors must bridge this gap with professional judgement, transparency, and methodological discipline.

1. Weighting Recent Comparables More Heavily ⚖️

In a stable market, surveyors can comfortably use comparables spanning 12–24 months. In a softening market, the weighting must shift decisively toward the most recent evidence — even if that evidence is limited.

Practical steps include:

| Action | Rationale |

|---|---|

| Prioritise sales from Q4 2025 – Q1 2026 | Reflects current buyer sentiment and pricing |

| Apply downward adjustments to older comparables | Accounts for market softening since transaction date |

| Cross-reference asking price vs. achieved price | Reveals true market depth and negotiation margins |

| Note time-on-market trends | Longer marketing periods signal reduced demand |

Where comparable evidence is genuinely thin, surveyors should document this explicitly in their reports. Transparency about data limitations is not a weakness — it is a professional obligation.

2. Applying Market Condition Adjustments

RICS Red Book valuation standards require that surveyors reflect market conditions at the date of valuation. When buyer enquiries are at -26% and price expectations are negative, a surveyor who ignores these signals risks producing a valuation that is technically compliant but commercially misleading.

Adjustments to consider include:

- Liquidity discounts where evidence suggests extended marketing periods are likely

- Condition and quality premiums/discounts reflecting the intensifying bifurcation between prime and secondary stock [1]

- Location adjustments that account for hyper-local demand variations

The bifurcation point deserves particular emphasis. Overall office sector valuations remain far below pre-pandemic peaks, yet top-tier buildings in prime locations are commanding record rents [1]. Lower-quality and less-central properties face elevated vacancies and persistent pricing pressure [1]. The same dynamic is visible in residential markets: well-presented, well-located homes are transacting; tired or peripheral stock is sitting.

For a thorough understanding of the factors that drive property value in any market condition, the valuation factors guide provides a comprehensive framework that remains highly relevant in 2026's cautious environment.

3. Structural Survey Integration 🔍

In a buyer's market, structural condition becomes a more significant valuation variable. Buyers with greater negotiating power are using survey findings to justify price reductions. Surveyors who integrate structural assessment findings into their valuation narrative — rather than treating them as separate exercises — provide clients with a more complete picture.

A structural survey in London that identifies significant defects in a Spring 2026 market carries more valuation weight than it might have done during the frenzied activity of 2021–2022. Defects that were previously overlooked by motivated buyers are now deal-breakers or leverage points.

4. Commercial Property: A Sector Under Particular Scrutiny

Commercial valuations face additional complexity in Spring 2026. CBRE forecasts commercial real estate investment activity to increase by 16% in 2026 to $562 billion globally [4], suggesting institutional appetite remains, but UK-specific conditions — including stamp duty changes and occupier uncertainty — are creating localised headwinds.

Commercial property surveyors in London are navigating a market where niche asset classes — data centres, senior housing, self-storage, and student housing — are reshaping investment demand [1], while traditional office and retail valuations remain under pressure.

For commercial instructions, surveyors should pay particular attention to:

- Lease covenant strength (tenant financial resilience in an uncertain economy)

- Void period assumptions (more conservative in a weakened occupier market)

- Capitalisation rate adjustments reflecting higher risk premiums

Communicating Market Softness to Clients: The Surveyor's Responsibility

The technical recalibration of valuation methodology is only half the challenge. Communicating the results — and the uncertainty surrounding them — to clients is equally critical. This is where many surveyors underperform, defaulting to figures without adequate context.

Navigating market caution in Spring 2026 requires surveyors to be more explicit than usual about:

- The volatile market conditions at the date of valuation

- The limitations of comparable evidence available

- The range of outcomes that could reasonably apply

- The specific risks that could cause values to move in either direction

Structuring the Valuation Report for Clarity

A valuation report issued in Spring 2026 should include a dedicated Market Conditions section that references:

- Current RICS market sentiment data (buyer enquiries, price expectations)

- Relevant macroeconomic context (interest rate environment, geopolitical factors)

- Local market observations specific to the subject property's area

This is not about hedging or avoiding professional accountability. It is about giving clients the information they need to make informed decisions. A seller who understands that buyer enquiries are at -26% is better positioned to set realistic expectations than one who receives a valuation figure without context.

Managing Vendor and Buyer Expectations 🤝

The Spring 2026 market is described by practitioners as driven by "genuine movers rather than speculation" [2]. This is actually a healthy dynamic — but it requires honest conversations about pricing.

For vendors: Surveyors should clearly explain that aspirational pricing in a market with -18% near-term price expectations is likely to result in extended marketing periods, further price reductions, and ultimately a worse outcome than realistic initial pricing.

For buyers: Where a Red Book valuation is being used for mortgage or legal purposes, clients should understand that the valuation reflects current market conditions — which include genuine uncertainty — and that values could move in either direction over the coming months.

For investors: The cautious optimism evident in some market commentary [3] should be contextualised against the specific risks of the subject asset class and location. Lifestyle-led buying activity — families relocating from London, downsizers releasing equity — is supporting certain market segments [2], but this demand is selective and price-sensitive.

The Role of Expert Surveyor Advice

In uncertain markets, the value of qualified professional guidance increases significantly. Property owners, buyers, and investors who attempt to navigate Spring 2026 conditions without professional support risk making decisions based on outdated market assumptions or misleading asking price data.

Expert surveyor advice becomes particularly valuable when:

- A transaction is being considered in a sector experiencing rapid value change

- Lender valuations are coming in below agreed purchase prices

- Commercial lease renewals or rent reviews are due in a softening occupier market

- Probate, matrimonial, or other formal valuation purposes require RICS-compliant assessments

For those involved in estate administration, a probate valuation in London conducted in Spring 2026 must carefully reflect the subdued market conditions at the date of death — not historical peak values that no longer represent achievable prices.

Regional Variations: Not All Markets Are Moving Equally

One of the most important nuances in Spring 2026 is that market caution is not uniformly distributed. Surveyors operating across different regions and property types are experiencing meaningfully different conditions.

London and the South East

The London market continues to demonstrate its characteristic resilience in prime locations, while outer and secondary markets feel the weight of affordability constraints and reduced buyer confidence. Areas with strong lifestyle appeal — Richmond, Chiswick, Barnes, and parts of West London — are seeing continued demand from upsizers and relocators [2].

Surveyors covering West London and South East London are observing a clear price sensitivity threshold: properties priced at or below market are transacting; those priced above are not. This gap between asking and achieved prices is a critical data point for comparable analysis.

Commuter Belt and Rural Markets

Commuter belt markets — Surrey, Hampshire, Berkshire, and beyond — are experiencing the lifestyle-led demand noted above [2], but this is tempered by affordability pressures and the ongoing recalibration of hybrid working norms. Rural land markets are softening alongside broader policy uncertainty [5], affecting both agricultural and residential development land valuations.

Commercial Sector Bifurcation

The commercial market's bifurcation between prime and secondary assets [1] is perhaps the starkest illustration of Spring 2026's selective conditions. Commercial building surveys in London are increasingly revealing condition-related issues that, in a tighter market, carry direct valuation consequences. A well-maintained Grade A office in a central location commands premium rents; a secondary building with deferred maintenance in a peripheral location faces structural vacancy risk.

Conclusion: Actionable Steps for Surveyors and Property Stakeholders

The data is clear: Spring 2026 is a market that rewards caution, precision, and honest communication. For building surveyors, the professional response to weakening buyer enquiries and geopolitical uncertainty is not to retreat from difficult conversations — it is to lead them.

✅ Actionable Next Steps

For building surveyors:

- Review and update comparable evidence databases to prioritise Q4 2025 – Q1 2026 transactions

- Include a dedicated Market Conditions section in all valuation reports issued in Spring 2026

- Apply documented adjustments where older comparables are used

- Engage in proactive client communication about the limitations of valuations in volatile conditions

- Ensure commercial valuations reflect updated void period and covenant strength assumptions

For property owners considering selling:

- Commission a current market valuation from a chartered surveyor in London before setting an asking price

- Accept that realistic pricing in a -18% price expectation environment will outperform aspirational pricing over time

- Use structural survey findings proactively to address defects before marketing

For buyers and investors:

- Treat lender valuations that come in below agreed prices as market intelligence, not obstacles

- Seek independent valuation advice before committing to significant transactions

- Recognise that the bifurcation between prime and secondary assets creates both risk and opportunity

The Spring 2026 property market is not in freefall — cautious optimism remains justified in the right segments [3]. But it is a market that punishes complacency and rewards those who engage with professional, evidence-based guidance. Navigating market caution in Spring 2026 successfully means treating uncertainty not as an obstacle, but as the defining context within which every valuation decision must be made.

References

[1] Episode352 – https://www.tylercauble.com/podcast/episode352

[2] Article – https://www.maywhetter.co.uk/news/article.html?id=1769511787

[3] money.tmx – https://money.tmx.com/quote/BRE/news/7176012207216596

[4] Markets – https://theideafarm.com/category/markets/

[5] Navigating A Cautious Market – https://www.carterjonas.co.uk/rural-view/navigating-a-cautious-market