UK residential transactions fell to their lowest level in over a decade during the 2023–2024 correction, leaving many comparable databases thin, dated, and geographically patchy. As activity begins to recover unevenly across regions in 2026, valuation surveyors face a methodological challenge that goes beyond simply finding the right comparable sale — they must also explain uncertainty convincingly to lenders, clients, and courts. Understanding what valuation surveyors should know about the 2026 UK property market recovery: adjustments, caveats, and sparse comparables is no longer optional professional development; it is a core competency.

This article examines how to evidence value in a market defined by uneven sentiment, low transaction volumes in certain sectors, and sharp regional divergence. It covers practical methodology, the correct use of caveats, and how to communicate uncertainty without undermining professional credibility.

Key Takeaways 📌

- Sparse comparables require structured adjustment methodology, not guesswork — document every step transparently.

- Regional variation in 2026 is pronounced: commuter belts and regional cities are recovering faster than prime central London and rural markets.

- Caveats must be proportionate and specific — generic disclaimers can expose surveyors to negligence claims rather than protect them.

- Lender communication is critical: mortgage valuations must clearly signal market condition uncertainty without triggering unnecessary down-valuations.

- RICS Red Book compliance remains non-negotiable, even when the market makes compliance harder to evidence.

The 2026 Recovery Landscape: Uneven, Patchy, and Regionally Divided

The UK property market entering 2026 is not recovering uniformly. Interest rates have eased from their 2023 peaks, but buyer confidence remains fragile in certain segments. Understanding the macro context is essential before a surveyor sets foot on any property.

Where the Market Is Moving

Several broad trends are shaping the 2026 valuation environment:

| Region / Sector | Recovery Trajectory | Transaction Volume | Comparable Availability |

|---|---|---|---|

| Commuter Belt (Surrey, Berkshire, Oxfordshire) | Moderate–Strong | Improving | Reasonable |

| Prime Central London | Slow / Flat | Low | Sparse |

| Regional Cities (Manchester, Leeds, Birmingham) | Strong | High | Good |

| Rural / Coastal Markets | Mixed | Low | Very Sparse |

| New-Build / Help-to-Buy Legacy Stock | Complex | Low | Problematic |

💬 Pull Quote: "A recovering market is not a uniform market. The surveyor who treats 2026 like 2021 — or like 2023 — will produce valuations that are neither accurate nor defensible."

For surveyors operating across the South East, understanding local nuance matters enormously. The recovery dynamics in Surrey differ meaningfully from those in Oxfordshire or Berkshire, even though these markets are geographically close.

Why Sparse Comparables Are the Defining Challenge of 2026

Low transaction volumes during 2023–2024 mean that many comparable databases contain stale evidence. Properties that sold 18–24 months ago may reflect a different market entirely. The challenge is compounded by:

- Withdrawn listings that never transacted, skewing perceived demand

- Off-market sales that leave no public comparable trail

- New-build incentive packages that distort headline sale prices

- Mortgage-constrained buyers who accepted lower prices than the open market might otherwise support

When comparables are sparse, the temptation is to either over-rely on a single sale or to widen the search area to the point where the evidence is no longer genuinely comparable. Neither approach is professionally sound.

Methodology for Adjustments When Comparables Are Thin

What valuation surveyors should know about the 2026 UK property market recovery — particularly regarding adjustments — is that structured, documented methodology is the only defensible approach. Adjustments must be rational, proportionate, and explicitly reasoned.

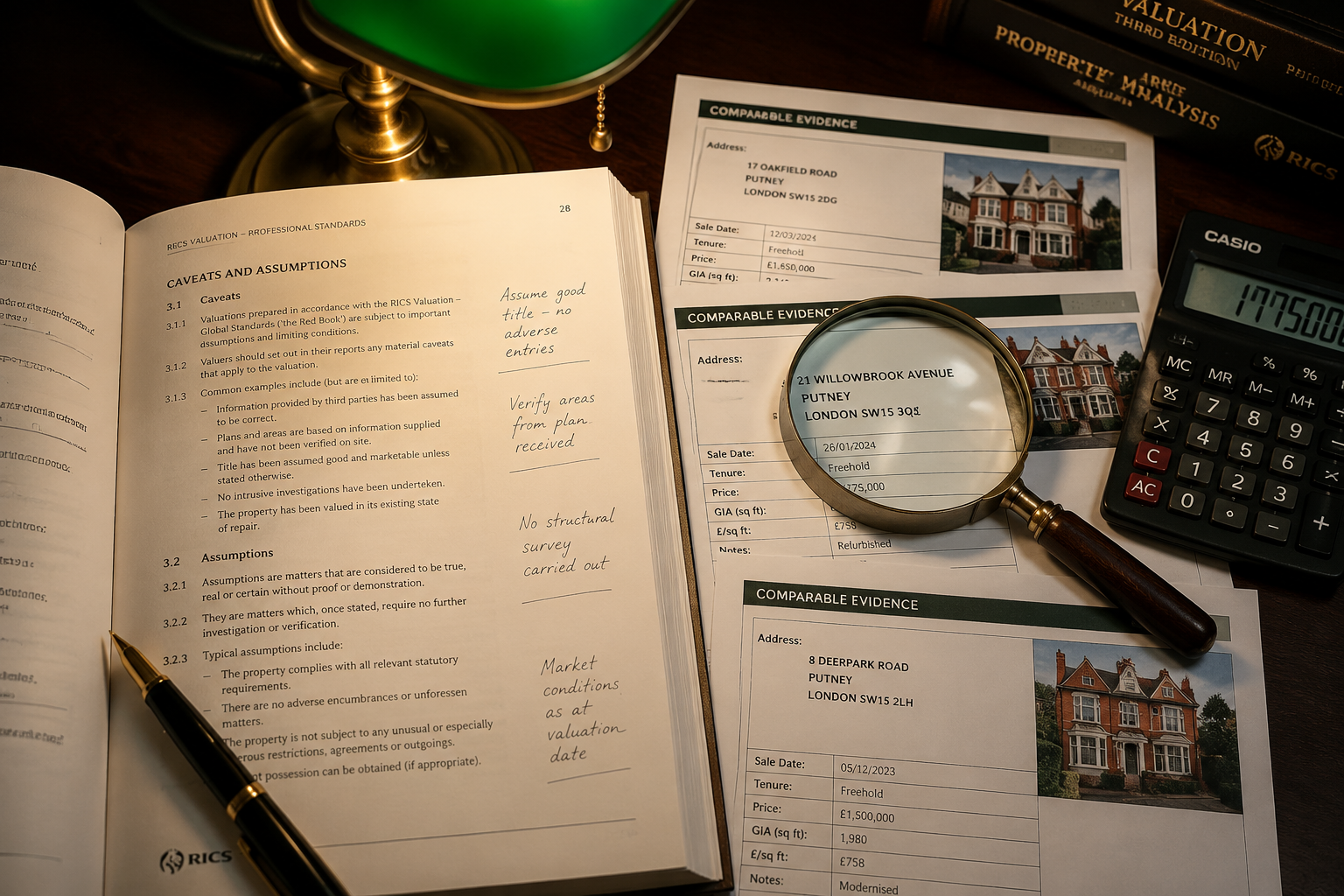

The Hierarchy of Comparable Evidence

When primary comparables (recent sales of similar properties in the same street or immediate locality) are unavailable, surveyors should work through a clear hierarchy:

- Primary: Same street, same property type, sold within 6 months

- Secondary: Same locality, similar property type, sold within 12 months

- Tertiary: Adjacent locality with demonstrably similar market characteristics, sold within 18 months

- Supporting: Asking prices of current listings (as a ceiling indicator only), auction results, and estate agent opinion

Each step down the hierarchy requires a more explicit written justification and a correspondingly wider range of uncertainty in the reported value.

Adjustment Factors to Document

When applying adjustments between a comparable and the subject property, every factor must be itemised:

- Time adjustment: Has the market moved since the comparable sold? By how much, and on what evidence?

- Location adjustment: Is the comparable in a genuinely equivalent micro-location?

- Physical adjustment: Size, condition, specification, floor level (for flats), garden, parking

- Tenure adjustment: Leasehold vs freehold, remaining lease length (see lease extension valuation guidance for leasehold-specific considerations)

- Legal adjustment: Restrictive covenants, rights of way, planning constraints

Best practice: Produce a written adjustment grid for every comparable used. This is not merely good practice — it is essential evidence if a valuation is later challenged.

Using Indices and Market Data to Support Adjustments

In a thin comparable environment, surveyors can legitimately reference published house price indices (Land Registry HPI, Halifax, Nationwide) to evidence time adjustments. However, indices must be used carefully:

- Use the most granular index available (regional, not national, where possible)

- Acknowledge the lag in index data (Land Registry data typically lags 2–3 months)

- Never use an index as a substitute for comparable evidence — only as corroboration

For Red Book valuations, the RICS Valuation — Global Standards require that market evidence takes precedence over modelled data. Indices support; they do not replace.

Caveats, Assumptions, and How to Explain Uncertainty Without Undermining Your Report

The most misunderstood aspect of what valuation surveyors should know about the 2026 UK property market recovery concerns caveats. A well-drafted caveat protects the surveyor and informs the client. A poorly drafted one — either too vague or disproportionately alarming — can damage both.

The Difference Between Assumptions and Caveats

The RICS Red Book draws a clear distinction:

- Assumptions are matters the valuer takes as fact without verification (e.g., that the title is good and marketable, that no undisclosed environmental issues exist).

- Special assumptions are counterfactual — they ask the valuer to assume something that is not currently true (e.g., that planning permission has been granted).

- Caveats are qualifications to the opinion of value that reflect genuine uncertainty in the evidence base.

In a sparse comparable environment, the appropriate response is usually a caveat, not a special assumption. The caveat should:

✅ Identify the specific source of uncertainty (e.g., "Only two comparable sales were available within a 12-month period")

✅ Explain the potential impact on value (e.g., "The opinion of value carries a wider margin of uncertainty than would normally be the case")

✅ State what additional evidence, if available, might resolve the uncertainty

❌ Do NOT use generic boilerplate caveats that could apply to any property in any market

❌ Do NOT caveat so heavily that the valuation becomes unusable for its intended purpose

Communicating Uncertainty to Lenders

Mortgage lenders are sophisticated users of valuation reports, but they operate within rigid credit policy frameworks. A surveyor who communicates uncertainty poorly risks one of two outcomes: the lender ignores the caveat entirely, or the lender rejects the valuation and instructs a second opinion.

Practical guidance for lender-facing reports in 2026:

- Use the market conditions section of the report to describe the current transaction environment factually and without alarmism

- Quantify uncertainty where possible: "In the absence of more proximate comparable evidence, the margin of uncertainty on this opinion of value is estimated at ±5%"

- Flag if the property is in a sector with known pricing pressure (e.g., high-rise new-build flats with cladding issues, properties with short leases)

- Recommend a re-inspection clause if market conditions are moving rapidly

For complex or high-value cases, surveyors should also consider whether a retrospective valuation of a prior transaction date is relevant — particularly in refinancing scenarios where the original purchase price may now be contested.

Communicating Uncertainty to Private Clients

Private clients — whether buying, selling, or involved in legal proceedings — need uncertainty explained in plain language. The surveyor's role is not to hedge so thoroughly that the client cannot act, but to ensure they understand the confidence level of the opinion.

For clients involved in matrimonial valuations or probate valuations, the stakes of an imprecise or poorly caveated report are particularly high. Courts and HMRC both scrutinise the evidence base, and a valuation that cannot be defended under cross-examination is a professional liability.

Sector-Specific Challenges in the 2026 Market

Beyond general methodology, certain property sectors present acute challenges in the current recovery environment.

Leasehold Flats: The Double Uncertainty Problem

Leasehold flats — particularly in urban centres — face two compounding uncertainties in 2026:

- Market sentiment remains cautious toward leasehold following ongoing legislative reform under the Leasehold and Freehold Reform Act 2024

- Comparable evidence is sparse because many flat owners have delayed selling pending clarity on reform implementation

Surveyors valuing leasehold flats must explicitly address remaining lease length, ground rent terms, and service charge levels as distinct adjustment factors. The shared ownership valuation sector faces similar complexity, with staircasing transactions providing limited comparable utility.

New-Build and Help-to-Buy Legacy Properties

The winding down of the Help to Buy equity loan scheme has left a cohort of properties where the first resale is now occurring. These properties present a particular challenge:

- The original purchase price included government equity loan support, inflating the effective price paid

- Resale values may be below original purchase prices in some areas

- Comparable evidence from the original new-build phase is not reliable for resale valuations

Surveyors should approach Help to Buy valuations in the current market with particular care, ensuring that the comparable evidence used reflects genuine open market resale transactions rather than developer-supported initial sales.

Commercial Property: An Adjacent Challenge

While this article focuses on residential markets, it is worth noting that commercial property valuers face an even more acute sparse comparable problem in 2026, particularly in the retail and office sectors. Commercial building surveys and valuations in these sectors require explicit acknowledgement of structural market shifts — not merely cyclical ones.

Professional Standards and Risk Management in 2026

RICS Compliance in a Difficult Market

The RICS Red Book does not relax its requirements because the market is difficult. If anything, a challenging market demands stricter adherence to methodology, because the consequences of error are greater and the scrutiny of reports is higher.

Key compliance points for 2026:

- Basis of value: Ensure the correct basis (Market Value, Mortgage Lending Value, etc.) is clearly stated and appropriate for the instruction

- Valuation date: In a moving market, the valuation date is critical — a report dated even 30 days earlier may not reflect current conditions

- Independence: Surveyors must be alert to conflicts of interest in a market where repeat instructions from lenders or developers may create subtle pressure

- Competence: If a surveyor lacks genuine knowledge of a specific market sector or locality, declining the instruction is the professionally correct response

Documenting Your Reasoning

In any market, but especially in 2026's uneven recovery, the valuation file must contain sufficient documentation to reconstruct the reasoning behind the opinion of value. This means:

- Printed or saved copies of all comparables considered (not just those used)

- Notes on why certain comparables were rejected

- Evidence of market condition research (index data, agent discussions, auction results)

- A clear adjustment grid as described above

This documentation is the surveyor's primary defence in any negligence claim or RICS disciplinary proceeding.

Conclusion: Actionable Steps for Surveyors in 2026

The 2026 UK property market recovery presents genuine professional challenges, but none that cannot be addressed through rigorous methodology, honest communication, and disciplined documentation. Here are the key actions surveyors should take now:

1. Build a regional comparable database proactively.

Do not wait until an instruction arrives to discover that comparables are thin. Maintain ongoing awareness of transaction activity in your core operating areas.

2. Develop a standard adjustment grid template.

Consistency in adjustment methodology across your practice reduces error and improves defensibility. Every adjustment should be quantified and justified in writing.

3. Draft market-specific caveat language.

Generic caveats are professionally inadequate. Develop caveat language that accurately describes current conditions in the specific sectors and localities you value.

4. Invest in lender communication skills.

The ability to explain valuation uncertainty clearly and proportionately — without triggering unnecessary lending decisions — is a high-value professional skill in the current market.

5. Stay current with RICS guidance.

The RICS issues regular market updates and professional statements. In a recovering market, these are not optional reading.

6. Know when to decline.

If comparable evidence is so sparse that no defensible opinion of value can be formed, declining the instruction is the correct professional response. A report that cannot be defended is worse than no report.

For surveyors operating across London and the South East, staying connected to local market intelligence — whether in North London, Guildford, or Central London — is the foundation of credible valuation practice in 2026.

The surveyors who navigate this recovery well will be those who treat methodological rigour not as a burden, but as the very thing that distinguishes professional opinion from informed guesswork.

For professional valuation services across London and the South East, explore our London property valuation guide or contact a chartered surveyor in London to discuss your specific requirements.