Last updated: May 21, 2026

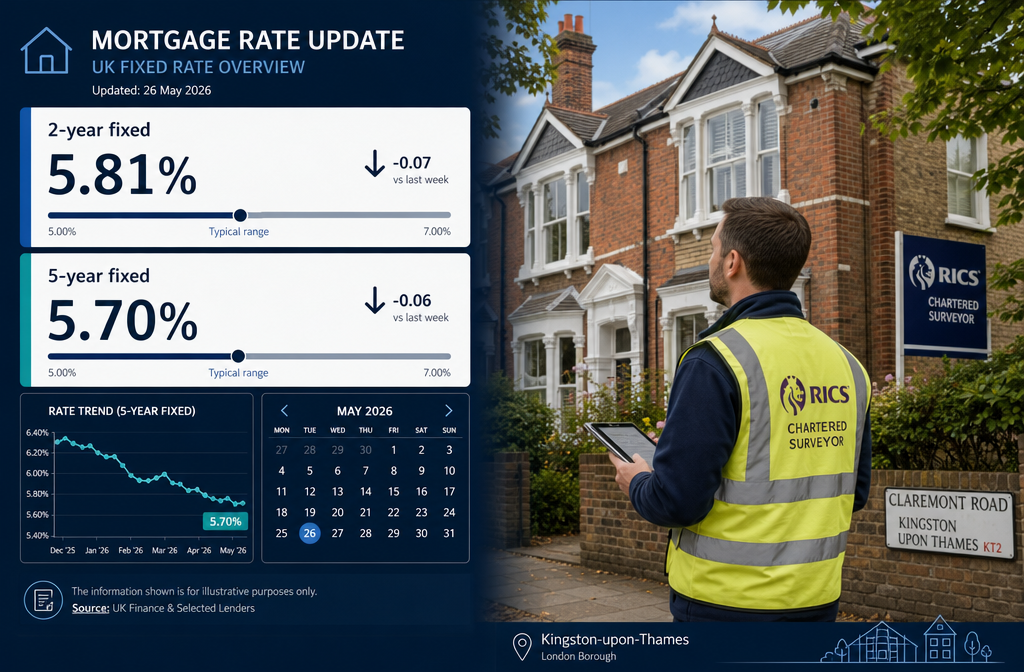

Quick Answer: Mortgage rates edged lower in May 2026 — the average two-year fixed rate fell to around 5.81% and the average five-year fix to around 5.70% — giving Kingston-upon-Thames buyers a modest affordability window. With homes for sale at an 11-year seasonal high and agreed sales only about 4% below last year's pace, this is one of the more buyer-friendly markets in recent memory. That makes it an especially good moment to commission a proper RICS survey: defects uncovered before exchange can support a price renegotiation that more than covers the survey cost.

⚠️ Rates change frequently. All rate figures in this article are approximate market averages as of May 2026. Always check current rates directly with lenders or a regulated mortgage broker before making any financial decisions.

Table of Contents

- What Are Current Mortgage Rates in Kingston for May 2026?

- How Do Kingston Mortgage Rates Compare to National Averages?

- What Factors Affect Mortgage Rates in May 2026?

- Are Mortgage Rates Expected to Drop Further in 2026?

- What Credit Score Do You Need for the Best Mortgage Rates in 2026?

- When Is the Best Time to Get a Home Survey in Kingston?

- What Type of Home Survey Do You Need in Kingston?

- How Much Does a Home Survey Cost in Kingston?

- Who Should Get a Home Survey Before Buying?

- Common Mistakes First-Time Buyers Make With Surveys and Mortgages

- FAQ

What Are Current Mortgage Rates in Kingston for May 2026? {#rates}

In May 2026, average UK fixed mortgage rates have edged down slightly from the levels seen at the start of the year. The average two-year fixed rate fell from approximately 5.90% to around 5.81%, and the average five-year fixed rate moved from around 5.78% to approximately 5.70% (source: Moneyfacts, May 2026). These are national averages; the rate any individual buyer secures will depend on their loan-to-value ratio, credit profile, and the specific lender.

For Kingston-upon-Thames buyers, these rates apply in the same way as anywhere else in England — lenders don't apply a local surcharge. However, because Kingston property prices sit well above the national average, the absolute monthly cost of a mortgage here is higher, so even a small rate movement has a meaningful cash impact.

Key figures at a glance (May 2026 national averages):

| Product | Rate (approx.) | Change vs. early 2026 |

|---|---|---|

| 2-year fixed | ~5.81% | ↓ ~0.09 pp |

| 5-year fixed | ~5.70% | ↓ ~0.08 pp |

pp = percentage points. Source: Moneyfacts, May 2026. Rates are indicative averages only.

How Do Kingston Mortgage Rates Compare to National Averages? {#comparison}

Kingston buyers access the same national mortgage market as buyers anywhere in England, so headline fixed rates are identical. The local difference shows up in loan size and affordability ratios, not in the rate itself.

Because Kingston-upon-Thames sits in one of London's most sought-after riverside boroughs, average asking prices are significantly above the UK median. A buyer borrowing a larger sum at 5.81% will pay proportionally more each month than a buyer in a lower-value area at the same rate. This is why even a 0.09 percentage point reduction in the two-year fix matters more in Kingston than it might elsewhere — on a £500,000 mortgage, that difference represents a meaningful annual saving.

For buyers also considering nearby areas, chartered surveyors covering South West London can help assess property condition across the wider region, from Putney to Esher.

What Factors Affect Mortgage Rates in May 2026? {#factors}

Fixed mortgage rates in May 2026 are primarily driven by swap rates (which reflect financial markets' expectations for the Bank of England base rate), lender competition, and broader economic conditions.

The main factors at play right now:

- Bank of England base rate: Markets have been pricing in gradual cuts, but the pace has been slower than many anticipated at the start of 2026. Lenders price fixed deals off swap rates, not the base rate directly.

- Inflation data: Persistent services inflation has made the Bank of England cautious. Any upside surprise in CPI data could slow or reverse the modest rate reductions seen so far.

- Lender competition: The 11-year seasonal high in homes for sale has increased transaction volumes, prompting some lenders to sharpen their pricing to win business.

- Loan-to-value (LTV): Buyers with a larger deposit (lower LTV) consistently access better rates. A 60% LTV deal will typically be priced lower than a 90% LTV deal, regardless of market conditions.

- Credit history: Lenders' internal credit scoring remains a significant variable (see the credit score section below).

Are Mortgage Rates Expected to Drop Further in 2026? {#outlook}

Experts are cautious. While the direction of travel in May 2026 has been modestly downward, most analysts warn that further cuts are not guaranteed and could slow or reverse if inflation proves sticky or if global economic conditions shift.

What this means for Kingston buyers: Don't hold off on a purchase purely in anticipation of significantly lower rates. The current market — with high stock levels and agreed sales running only about 4% below last year — gives buyers negotiating power that may not persist if rates do fall sharply and demand surges.

"Waiting for rates to fall further is a gamble. The buyer-friendly conditions in the Kingston market in May 2026 — high stock, moderate competition — may be more valuable than a marginal rate improvement six months from now."

Always check current rates with a regulated mortgage broker or lender directly before making any decisions. This article presents market context, not financial advice.

What Credit Score Do You Need for the Best Mortgage Rates in 2026? {#credit}

There is no single universal credit score threshold, because each lender uses its own internal scoring model and may use different credit reference agencies (Experian, Equifax, or TransUnion in the UK).

That said, the general principle is consistent: the cleaner your credit history and the higher your score on whichever scale a lender uses, the more likely you are to access the most competitive rate tiers. For the best fixed rates in 2026:

- Avoid missed payments on any credit products in the 12–24 months before applying.

- Keep credit utilisation low — ideally below 30% of available revolving credit.

- Register on the electoral roll at your current address.

- Limit hard credit searches in the months before a mortgage application.

A mortgage broker can run a soft search to indicate likely eligibility before a formal application, protecting your credit file.

When Is the Best Time to Get a Home Survey in Kingston? {#timing}

The best time to commission a home survey in Kingston is after your offer has been accepted but before you exchange contracts — and the earlier in that window, the better. This is the period when survey findings can still influence the price or the decision to proceed.

In the context of mortgage rates May 2026 home survey timing Kingston, the current market conditions make this timing even more important. With homes for sale at an 11-year seasonal high, sellers in Kingston are operating in a more competitive environment than they were in 2022 or 2023. That means buyers have more leverage to use survey findings as a basis for renegotiation.

The typical sequence:

- Offer accepted

- Instruct solicitor / conveyancer

- Commission RICS survey ← do this promptly

- Lender valuation (separate from your survey)

- Review survey report; raise any issues with seller

- Exchange contracts

- Completion

Don't wait until you're close to exchange to book a survey — RICS surveyors in Kingston and SW London can have availability windows of one to three weeks during busy spring periods. Booking early avoids delays. Chartered surveyors in Kingston can advise on current availability.

What Type of Home Survey Do You Need in Kingston? {#survey-types}

For most Kingston buyers, the choice is between a RICS Level 2 HomeBuyer Report and a RICS Level 3 Building Survey. The right choice depends primarily on the age, type, and condition of the property.

For a detailed breakdown, see the HomeBuyer Report vs Building Survey comparison guide.

RICS Level 2 HomeBuyer Report

- Suitable for: conventional, modern properties (broadly post-1930s) in reasonable condition

- Covers: visible defects, damp, timber issues, drainage, services (visual inspection only)

- Uses a traffic-light condition rating system (1 = satisfactory, 3 = urgent action needed)

- Does not include opening up of floors, lifting carpets, or detailed structural investigation

RICS Level 3 Building Survey

- Suitable for: older properties (pre-1930s), listed buildings, unusual construction, properties showing signs of significant defects, or any property where the buyer wants maximum detail

- Covers: full structural inspection, detailed description of defects, advice on remediation and indicative costs

- Kingston has a significant stock of Victorian and Edwardian terraced and semi-detached houses — many of these warrant a Level 3 survey

Decision rule:

- Choose Level 2 if the property is a post-war flat or house in apparently good condition.

- Choose Level 3 if the property is pre-1930s, has had significant alterations, shows any visible cracking or damp, or if you simply want the most comprehensive picture before committing.

For properties with specific structural concerns, a structural survey in London provides the deepest level of investigation.

How Much Does a Home Survey Cost in Kingston? {#costs}

Survey costs in Kingston and SW London vary based on survey level, property size, and the surveying firm. The following ranges are indicative for the Kingston area in 2026 — always request a specific quote.

| Survey Type | Indicative Cost Range (Kingston, 2026) |

|---|---|

| RICS Level 2 HomeBuyer Report | £400 – £700 |

| RICS Level 3 Building Survey | £600 – £1,200+ |

| Standalone RICS Valuation | £250 – £500 |

Costs vary with property size and complexity. Larger or more complex properties sit at the upper end. Always obtain a written quote before instructing.

Important context: A Level 3 Building Survey costing £800 that identifies £15,000 of remedial works gives the buyer a strong basis to renegotiate the purchase price or request that works are completed before completion. In a market where sellers are competing with an 11-year high in available stock, that negotiating position is real. The survey pays for itself many times over in these scenarios.

Buyers purchasing properties with shared walls should also consider whether party wall matters are relevant to their purchase.

Who Should Get a Home Survey Before Buying? {#who-needs}

Every buyer purchasing a property in Kingston should commission an independent RICS survey. The lender's mortgage valuation is not a survey — it is a brief assessment carried out for the lender's benefit to confirm the property is adequate security for the loan. It will not identify defects in detail, and the buyer has no recourse against the valuer.

Especially important for:

- Buyers of pre-1930s properties (very common in Kingston, Surbiton, and New Malden)

- First-time buyers who may not recognise signs of structural movement, damp, or poor-quality repairs

- Buyers purchasing at the top of their budget, where unexpected repair costs would cause financial strain

- Anyone buying a property that has been extended, converted, or significantly altered

- Buyers of leasehold flats, where a schedule of condition report may also be relevant

For buyers looking at properties across the wider SW London area, chartered surveyors in Putney, Twickenham, and Barnes cover the neighbouring neighbourhoods.

Common Mistakes First-Time Buyers Make With Surveys and Mortgages {#mistakes}

Understanding mortgage rates May 2026 home survey timing Kingston also means knowing what not to do. These are the most frequent errors that cost buyers money or cause transactions to fall through.

Survey-related mistakes:

- Relying on the mortgage valuation as a survey. It isn't one. The lender's valuer spends 20–30 minutes at the property and is assessing value, not condition.

- Choosing the cheapest survey without checking RICS accreditation. Always verify the surveyor holds RICS membership.

- Booking the survey too late. Leaving it until two weeks before exchange removes the time needed to get specialist quotes for any defects found, weakening your negotiating position.

- Ignoring the survey report. Some buyers receive a report flagging significant issues and proceed without renegotiating or investigating further. The report exists to be acted on.

Mortgage-related mistakes:

- Not getting a mortgage in principle before making offers. Sellers and agents in Kingston take offers more seriously from buyers with a decision in principle in place.

- Making multiple credit applications in a short period. Each hard search leaves a mark on your credit file. Use a broker who can assess options with soft searches first.

- Assuming rates will keep falling. As noted above, experts caution that the modest reductions seen in May 2026 may not continue.

FAQ {#faq}

Q: Are mortgage rates in Kingston different from the rest of the UK in May 2026?

A: No. Lenders apply the same fixed rate products nationally. Kingston buyers access the same rates as buyers elsewhere, but borrow larger sums due to higher local property prices, so rate changes have a bigger absolute impact on monthly payments.

Q: Can I negotiate my mortgage rate with a local Kingston bank or broker?

A: High street lenders publish fixed rates that are not typically negotiable on an individual basis. However, a whole-of-market mortgage broker can identify the most competitive products available for your specific LTV and credit profile, which effectively achieves the best rate available to you. Always use a regulated broker.

Q: How long does a typical home survey take in Kingston?

A: A RICS Level 2 HomeBuyer Report inspection usually takes two to four hours on site, with the written report delivered within three to five working days. A Level 3 Building Survey inspection may take four to eight hours for a larger property, with the report following within five to seven working days. Timelines vary by firm and property complexity.

Q: Can survey findings really help me renegotiate the price?

A: Yes, and in the current Kingston market this is particularly relevant. With stock at an 11-year seasonal high, sellers have less leverage than in recent years. A survey identifying, say, £10,000 of roof repairs gives a buyer a documented, professional basis to request a price reduction or ask the seller to carry out the works before completion.

Q: Do I need a survey if I'm buying a new-build property in Kingston?

A: New-builds typically come with an NHBC Buildmark or similar warranty, but a snagging report carried out before legal completion can identify defects that the developer is then obligated to fix. This is different from a standard RICS survey but equally valuable.

Q: What is the difference between a survey and a valuation?

A: A valuation establishes the market value of a property — relevant for mortgage purposes, tax, or sale. A survey assesses the physical condition of the property and identifies defects. They serve different purposes, and a buyer needs both: the lender arranges a valuation, but the buyer should independently commission a survey.

Conclusion: Actionable Next Steps for Kingston Buyers in May 2026

The combination of slightly easing mortgage rates and high property stock levels makes May 2026 a more favourable environment for Kingston buyers than much of the past three years. Rates are not dramatically lower, but the direction is positive and the market is less competitive than it was at the peak.

Here's what to do now:

- Check current mortgage rates with a regulated whole-of-market broker — don't rely on published averages alone.

- Get a mortgage in principle before making offers, so sellers treat your bid seriously.

- Commission a RICS survey promptly after offer acceptance — don't wait until close to exchange.

- Choose the right survey level: Level 2 for modern properties in good condition; Level 3 for older, extended, or visibly defective properties.

- Use survey findings actively — in a market with 11-year-high stock levels, sellers are more open to renegotiation than they have been in years.

- Don't assume rates will keep falling — the current window of buyer-friendly conditions may be more valuable than waiting for a rate cut that may not materialise.

For expert guidance on surveys across Kingston and the wider SW London area, the team at Kingston Surveyors can advise on the right survey type for your specific property.

References

- Moneyfacts, UK Mortgage Trends Treasury Report, May 2026

- Bank of England, Money and Credit Statistics, April 2026

- Rightmove, House Price Index, May 2026

- RICS, HomeBuyer Report and Building Survey guidance, 2023, https://www.rics.org