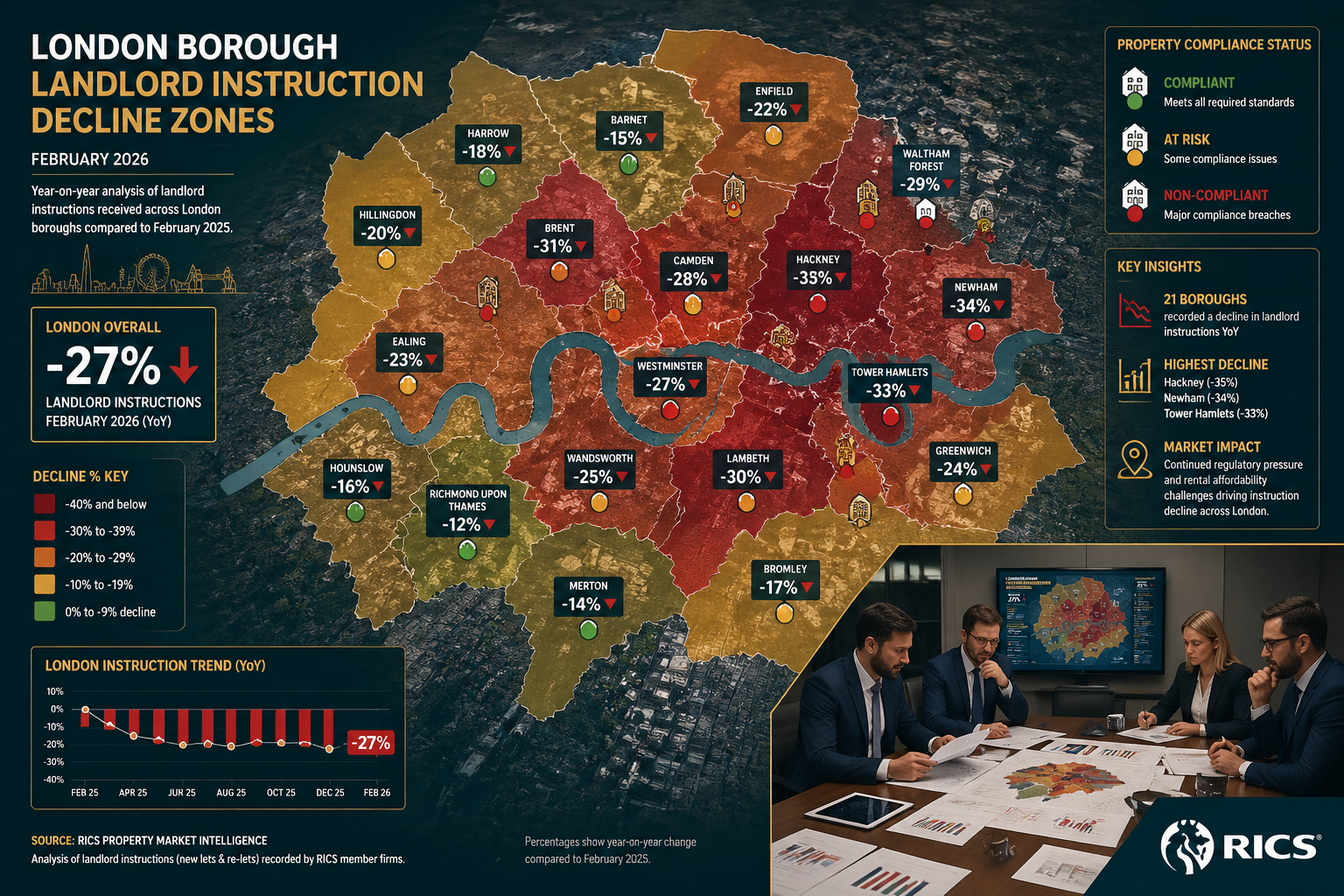

Landlord instructions in the UK private rented sector dropped -27% in February 2026 alone — a market signal that cannot be dismissed as seasonal noise [4]. With Phase 1 of the Renters' Rights Act now live and the Decent Homes Standard poised to reach private rentals for the first time in history, the valuation landscape has shifted permanently. The Valuation Impacts of Decent Homes Standard Extension to PRS: RICS Strategies Post-Renters' Rights Act May 2026 represent the most consequential recalibration of residential investment property assessments in a generation, demanding that surveyors, lenders, and landlords all update their frameworks — fast.

Key Takeaways 📌

- Phase 1 of the Renters' Rights Act (May 2026) abolishes Section 21 evictions and converts all ASTs to rolling periodic tenancies, fundamentally altering income stability assumptions in valuations.

- The Decent Homes Standard will extend to the PRS — with implementation proposed for 2035 or 2037 — but lenders and valuers must begin pricing remediation costs now.

- RICS guidance confirms the vacant possession assumption remains defensible but must be assessed on a case-by-case basis under new Section 8 grounds.

- Landlord registration, a PRS database, and a mandatory Ombudsman scheme (Phase 2, late 2026) introduce new compliance costs and reputational risks that directly affect borrower creditworthiness.

- Surveyors play a central role in compliance audits, capex reserve modelling, and defending valuations in disputes under the new regulatory environment.

The Regulatory Architecture: What Changed in May 2026

The Renters' Rights Act 2026 did not arrive quietly. Its Phase 1 implementation on 1 May 2026 triggered the simultaneous abolition of Section 21 'no-fault' evictions and the conversion of all existing and new Assured Shorthold Tenancies (ASTs) into Assured Periodic Tenancies (APTs) — rolling monthly arrangements with no fixed minimum term [2].

This single structural change reshapes every income-based valuation model. Previously, a landlord could recover possession on a predictable timeline by simply serving a Section 21 notice. That mechanism is gone. Valuers relying on discounted cash flow (DCF) models must now account for the slower, more uncertain possession recovery process under Section 8 grounds, which requires demonstrating specific fault — rent arrears, anti-social behaviour, or a landlord's intention to sell or occupy [1].

Rent Increase Restrictions and Their Valuation Consequences

The Act also introduces strict rent review controls with direct valuation consequences:

| Restriction | Detail | Valuation Impact |

|---|---|---|

| No increases in first 12 months | Rent frozen for new tenancies | Suppresses early-year income projections |

| Maximum one increase per year | Annual cap on rent reviews | Limits upside rental growth assumptions |

| Two months' notice required | Up from one month | Delays income adjustment timing |

| Section 13 notice mandatory | Contractual review clauses ineffective | Removes landlord flexibility in lease structures |

💬 "Contractual rent review clauses — long a standard feature of tenancy agreements — are now effectively redundant. Valuers must treat Section 13 as the only lawful mechanism." [2]

For professional property valuations in London, these restrictions mean rental income projections must be stress-tested against the new statutory framework rather than relying on historic contractual assumptions.

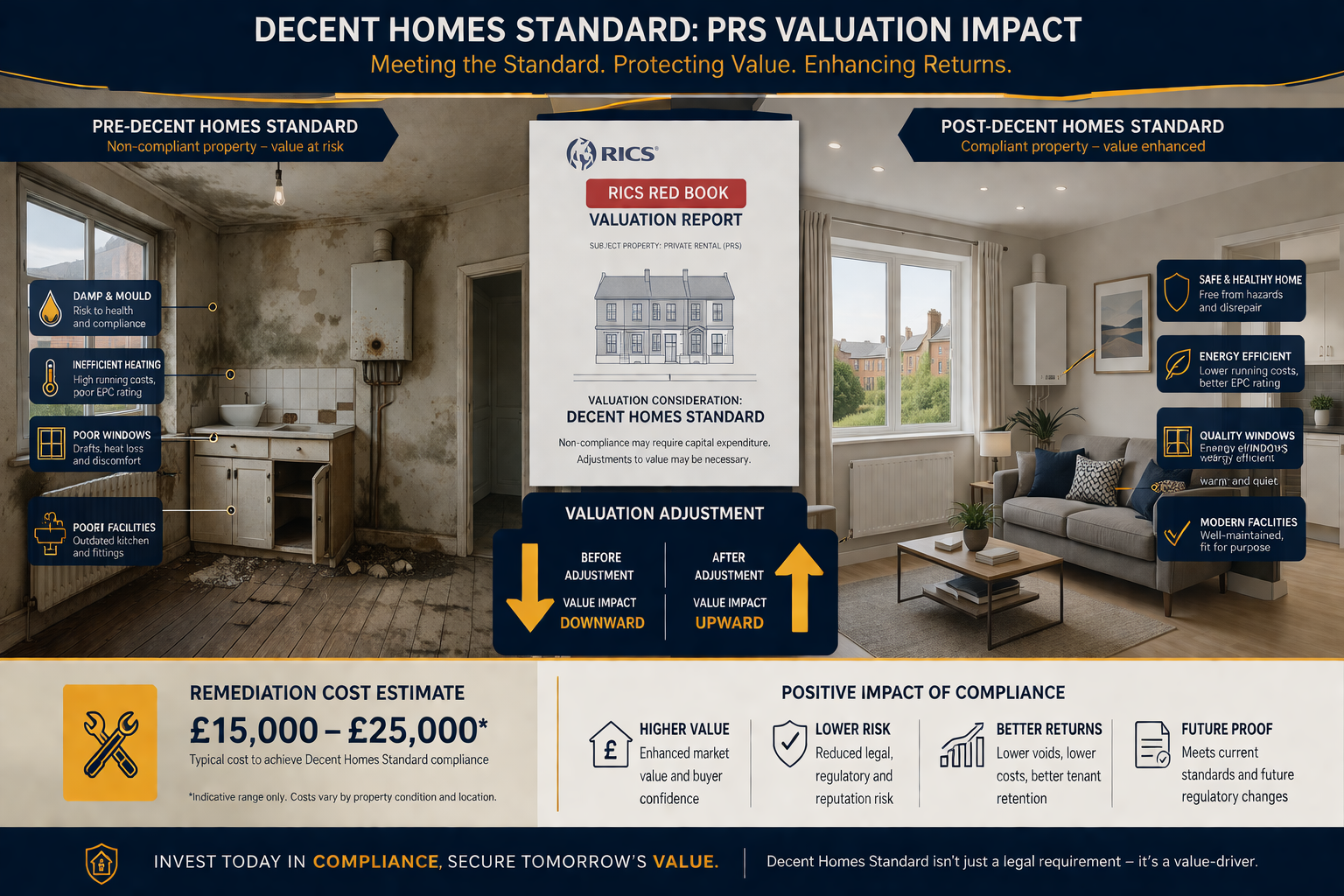

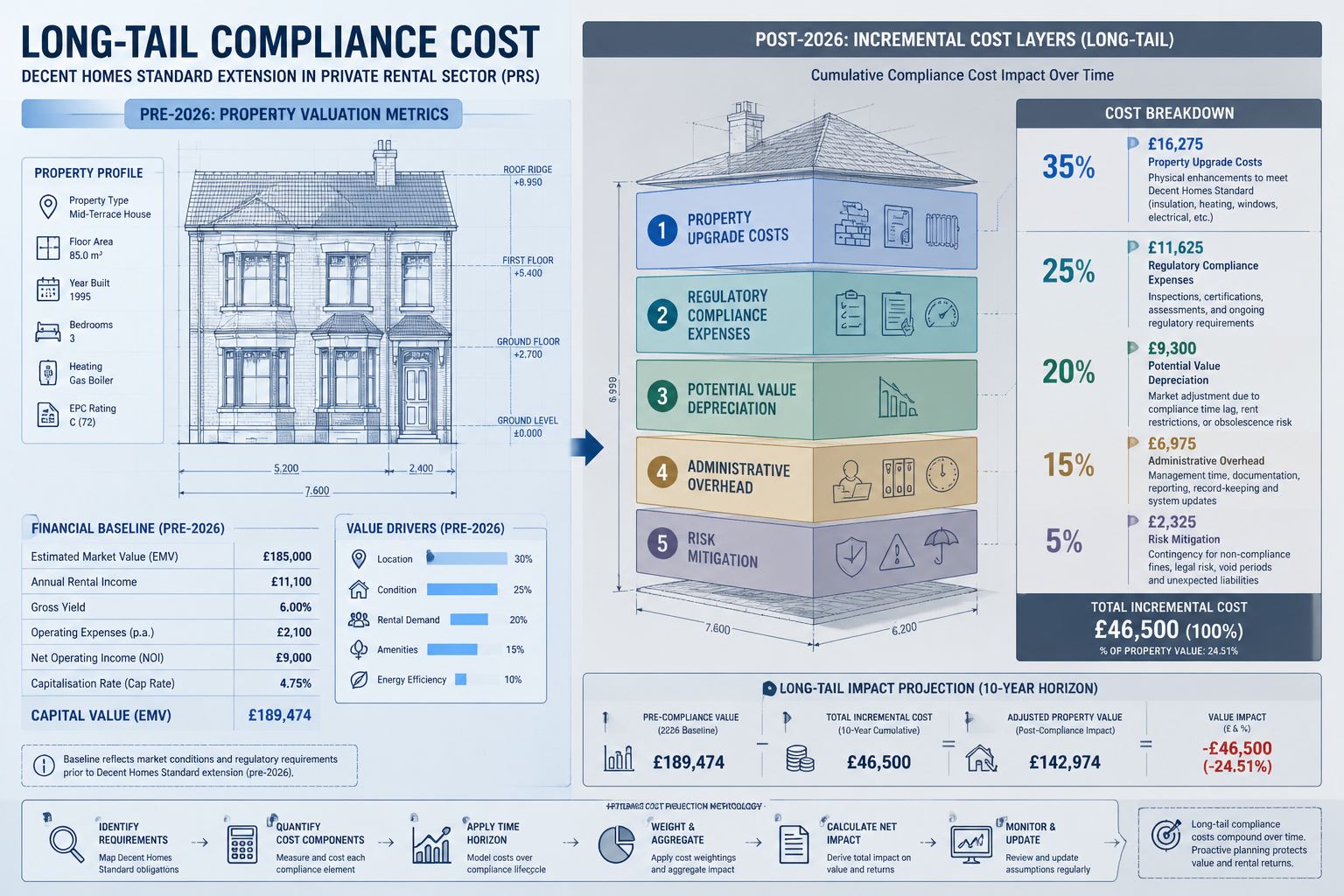

Decent Homes Standard Extension: Pricing the Long-Tail Compliance Cost

The Decent Homes Standard (DHS) has applied to social housing since 2006. Its extension to the private rented sector marks an unprecedented shift — and the Valuation Impacts of Decent Homes Standard Extension to PRS: RICS Strategies Post-Renters' Rights Act May 2026 are being felt even before the standard formally applies, because lenders and sophisticated investors are already pricing compliance risk into acquisition decisions.

Timeline Uncertainty Creates Valuation Complexity

The DHS extension timeline remains genuinely uncertain: implementation is proposed for either 2035 or 2037, depending on government consultation outcomes [2]. This ambiguity does not reduce the valuation relevance — it amplifies it. A 9–11 year runway sounds long, but for buy-to-let portfolios with 25-year mortgage terms, the remediation liability is very much within the loan period.

The Government's own impact assessment identifies four core criteria a property must meet under the DHS:

- 🏠 Decent condition — free from serious hazards under the Housing Health and Safety Rating System (HHSRS)

- 🔧 Reasonably modern facilities — kitchens, bathrooms, and utilities within defined age thresholds

- 🌡️ Effective insulation and heating — a warm, dry, and weatherproof structure

- 🛠️ Good state of repair — structural integrity and maintained building fabric [3]

Capex Reserve Modelling: The Surveyor's New Core Task

RICS guidance is explicit: lenders assessing rental income on a net basis should factor the potential cost of bringing properties to Decent Homes Standard into underwriting decisions, with specific consideration for maintenance and capital expenditure (capex) reserve accounts [2].

For surveyors, this creates a new deliverable: the compliance-adjusted valuation, which incorporates:

- A condition audit benchmarked against DHS criteria

- An estimated remediation cost schedule (typically £8,000–£25,000+ per property depending on age and condition)

- A net present value (NPV) deduction reflecting the timing of required expenditure

- A sensitivity analysis showing valuation under 2035 vs. 2037 implementation scenarios

This work sits naturally alongside existing dilapidation survey services and schedule of dilapidations assessments, which already quantify the cost of returning a property to a defined standard of repair.

Phase 2 Compliance Costs: Registration, Database, and Ombudsman

Beyond the DHS, Phase 2 of the Renters' Rights Act (expected late 2026) introduces three additional compliance layers with direct cost implications:

1. PRS Database and Landlord Registration

All private landlords must register on a new national database before marketing properties for letting. Rental advertisements must display valid registration numbers [2]. Non-compliance risks enforcement action and property marketing restrictions — a material risk for portfolio valuations.

2. Independent PRS Landlord Ombudsman

Mandatory membership is required by 2028, with scheme decisions enforceable as court orders [2]. This creates potential cash flow impairment risk — awards against landlords can be enforced without further litigation — and introduces reputational risk that lenders must assess when evaluating borrower creditworthiness.

3. Enhanced Due Diligence Documentation

Compliance costs are rising due to Deposit Protection Scheme verification, DHS compliance documentation, and new regulatory record-keeping requirements [1]. Surveyors instructed to produce RICS Red Book valuations must now include commentary on regulatory compliance status as part of their market evidence analysis.

RICS Strategies: Defending Valuations Post-Renters' Rights Act

The Valuation Impacts of Decent Homes Standard Extension to PRS: RICS Strategies Post-Renters' Rights Act May 2026 demand not just updated inputs but a fundamentally revised methodology. RICS has issued specific guidance on how valuers should approach PRS properties under the new framework.

The Vacant Possession Assumption: Still Defensible, But Conditional

One of the most debated questions among valuers post-May 2026 is whether the vacant possession assumption — valuing a property as if unoccupied — remains appropriate for tenanted PRS assets.

RICS has confirmed that this assumption remains justified because Section 8 possession grounds are still available to landlords [1]. However, the guidance is clear that valuers must:

- Assess the reasonableness of the assumption on a case-by-case basis

- Reflect any market impact of the changed possession landscape in their reported figures

- Document their reasoning transparently within the valuation report

This is not a blanket permission to ignore the regulatory change. Where a property has a sitting tenant with a strong tenancy history and no obvious Section 8 grounds available, the vacant possession assumption may require a market-supported discount to reflect the realistic timeline to recovery.

Data-Driven Protocols for Dispute Defence

As enforcement activity increases and landlord-lender disputes become more common in a contracting market, surveyors need robust, data-driven protocols to defend their valuations. Key elements include:

📊 Comparable Evidence Selection

- Prioritise post-May 2026 transaction evidence wherever possible

- Flag pre-Act comparables with explicit adjustment notes

- Distinguish between vacant possession sales and tenanted investment sales

📋 Regulatory Compliance Checklist

Include a standardised compliance commentary covering:

- EPC rating and trajectory to minimum standard

- HHSRS hazard assessment status

- Landlord registration status (Phase 2)

- Ombudsman membership status

- Deposit protection compliance

💰 Income Approach Adjustments

For investment valuations using an income capitalisation or DCF approach:

- Apply void period assumptions reflecting the slower possession process under Section 8

- Use net rental income (after estimated compliance costs) as the income base

- Apply a DHS remediation deduction as an NPV adjustment

- Stress-test yields against a scenario where the property fails to meet DHS criteria by the implementation date

For landlords with complex portfolios, a retrospective valuation may also be needed to establish a pre-Act baseline for tax or dispute purposes.

Lender Covenant Updates: A Parallel Obligation

RICS guidance directed at lenders is equally prescriptive. Mortgage undertakings must be updated to [2]:

- Require borrower landlords to maintain properties to the Decent Homes Standard (replacing older 'good repair' language)

- Prohibit letting policies that breach the Renters' Rights Act

- Include capex reserve account requirements as a lending condition for PRS portfolios

This has direct implications for rent review assessments and portfolio refinancing decisions, where surveyors are increasingly being asked to provide compliance-adjusted valuations as a condition of loan renewal.

The Market Contraction Signal: What -27% Means for Valuers

The -27% decline in landlord instructions recorded in February 2026 is not just a supply statistic — it is a valuation signal [4]. When supply contracts while tenant demand remains elevated, two competing forces act on PRS property values:

| Force | Direction | Valuation Effect |

|---|---|---|

| Reduced investment confidence | ↓ | Compresses investor yields, reduces demand for tenanted stock |

| Rental income growth | ↑ | Supports income-based valuations for compliant properties |

| Compliance cost burden | ↓ | Reduces net income, increases capex deductions |

| Scarcity premium for compliant stock | ↑ | Premium for DHS-ready properties over non-compliant stock |

The net effect is a bifurcated market: compliant, well-maintained properties command a scarcity premium, while non-compliant stock faces accelerating value discounts as the DHS deadline approaches. Surveyors must reflect this divergence explicitly in their comparable selection and yield analysis.

For landlords considering exit strategies, understanding the best approach to London property valuation in this environment is essential before making disposal decisions.

Practical Implications for Landlords, Lenders, and Surveyors

For Landlords 🏘️

- Commission a DHS compliance audit now — do not wait for the implementation deadline

- Budget for remediation costs as a capital reserve, not an operating expense

- Register on the PRS database ahead of the Phase 2 deadline to avoid marketing restrictions

- Review tenancy agreements to ensure Section 13 rent review procedures are correctly documented

For Lenders 🏦

- Update standard mortgage covenants to reference the Decent Homes Standard explicitly

- Require compliance-adjusted valuations for new PRS lending and portfolio refinancing

- Assess Ombudsman membership status as part of borrower due diligence from 2026 onwards

- Build capex reserve requirements into loan conditions for portfolios with pre-2000 stock

For Surveyors 📐

- Update valuation methodology notes to reflect RICS guidance on vacant possession assumptions

- Develop a standardised DHS compliance commentary for inclusion in all PRS valuation reports

- Build DCF models that incorporate Section 8 possession timelines and Section 13 rent review restrictions

- Maintain a post-May 2026 comparable database to support defensible market evidence

Surveyors operating across London and the South East — including those providing services in Chiswick, Central London, and East London — are already seeing instruction volumes shift as landlords seek compliance-focused survey advice ahead of regulatory deadlines.

Conclusion: Actionable Next Steps in a Transformed Market

The Valuation Impacts of Decent Homes Standard Extension to PRS: RICS Strategies Post-Renters' Rights Act May 2026 are not theoretical — they are live, material, and accelerating. The combination of abolished Section 21 evictions, rolling periodic tenancies, rent increase restrictions, mandatory registration, and the long-tail DHS compliance obligation has created a valuation environment that requires updated tools, updated methodology, and updated professional judgement.

The most important actions to take now:

- ✅ Commission a DHS compliance audit for every PRS property in a portfolio — establish the remediation cost liability before a lender or buyer does it for you.

- ✅ Update valuation reports to include explicit RICS-compliant commentary on the vacant possession assumption, Section 8 possession timelines, and DHS remediation deductions.

- ✅ Revise DCF income models to use net rental income after compliance costs, with Section 13 rent review restrictions built into growth assumptions.

- ✅ Engage a chartered surveyor experienced in post-Renters' Rights Act PRS valuations — the regulatory complexity now demands specialist knowledge, not general residential expertise.

- ✅ Monitor the DHS implementation timeline closely — a shift from 2035 to 2037 changes the NPV of remediation costs meaningfully and should trigger a valuation review.

The PRS market is not collapsing — but it is bifurcating. Compliant, well-maintained stock will command premiums. Non-compliant stock will face deepening discounts. The surveyors and landlords who act now will be positioned to defend their valuations, satisfy lender requirements, and capture the compliance premium. Those who wait will find themselves on the wrong side of an increasingly data-driven market.

References

[1] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[2] Renters Rights Act Lenders Landlords – https://ww3.rics.org/uk/en/journals/property-journal/renters-rights-act-lenders-landlords.html

[3] Dhs Final Impact Assessment – https://assets.publishing.service.gov.uk/media/69789688128d9c1d09a98bd5/DHS_Final_Impact_Assessment.pdf

[4] Rental Supply Shortage And Valuation Sensitivity Assessing Prs Property Values Amid Tenant Demand Surge In 2026 – https://nottinghillsurveyors.com/blog/rental-supply-shortage-and-valuation-sensitivity-assessing-prs-property-values-amid-tenant-demand-surge-in-2026