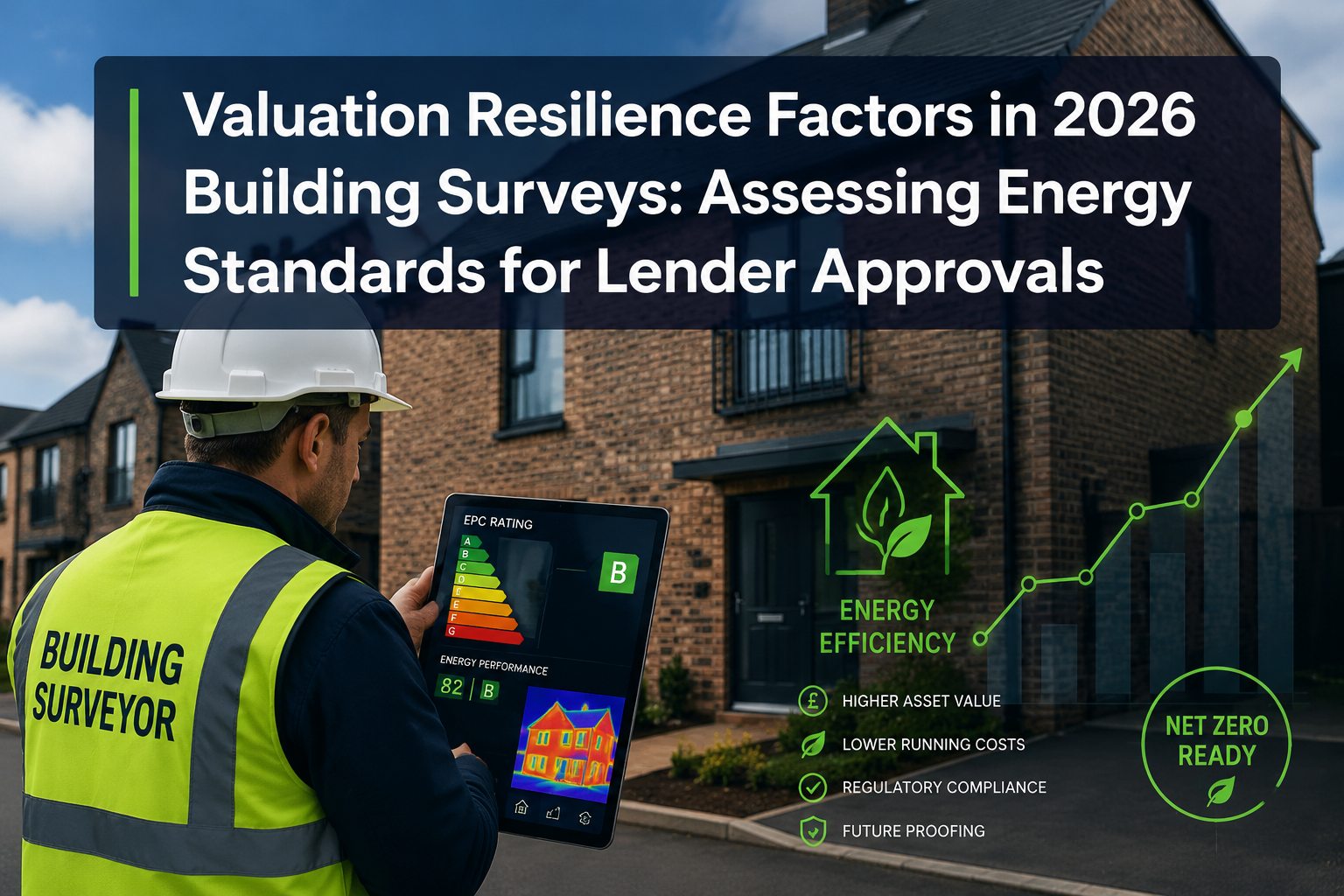

Lenders rejected nearly 23% more financing applications for properties with poor energy performance ratings in 2026 compared to just two years prior — a sharp escalation that has fundamentally changed how building surveys are commissioned, conducted, and interpreted [1]. This is not a marginal adjustment. It represents a structural shift in how mortgage lenders, commercial banks, and institutional financiers assess risk, and it places the building survey at the centre of every lending decision. Understanding the valuation resilience factors in 2026 building surveys: assessing energy standards for lender approvals is now essential knowledge for property owners, buyers, developers, and the surveyors who serve them.

Key Takeaways

- Lenders in 2026 are actively deprioritising properties with weak EPC ratings, with rejection rates rising significantly for sub-standard energy performers.

- The RICS fourth edition ESG valuation standards, effective April 2026, now mandate that energy performance be systematically incorporated into all formal valuations.

- Green-certified buildings command rental premiums of 6-11% and sale price premiums of up to 25% compared to non-certified equivalents.

- Climate risk factors — including flood exposure and overheating potential — are now quantified within Level 3 building surveys and directly influence lender pricing models.

- Advanced digital tools such as thermal imaging and 3D modelling have become standard components of surveys used to support lender approvals.

Why Energy Standards Have Become Central to Lender Decisions

For most of the past decade, energy performance certificates were treated as a compliance formality — a document filed and largely forgotten. That era is over. The convergence of regulatory pressure, ESG investment mandates, and rising retrofit costs has pushed energy standards to the top of every lender's due diligence checklist.

The Royal Institution of Chartered Surveyors introduced the fourth edition of its ESG valuation standards, effective 30 April 2026. These standards require valuers to systematically incorporate environmental, social, and governance factors — including energy performance — into every formal property valuation [2]. This is not optional guidance. It is a mandatory framework that applies to RICS-regulated valuers across residential and commercial sectors.

At the same time, the Global Real Estate Sustainability Benchmark (GRESB) launched its Real Estate Lender Assessment, giving lenders a structured tool to evaluate ESG factors — including energy performance — during the underwriting process [6]. The result is a feedback loop: surveyors must now produce reports that satisfy both RICS standards and lender ESG frameworks simultaneously.

What does this mean in practice? A Level 3 building survey submitted to support a mortgage application in 2026 must now do far more than identify structural defects. It must assess:

- Current EPC rating and the gap to minimum lender thresholds

- Estimated retrofit costs to achieve compliance

- Climate-related risks including flood exposure and overheating potential

- Maintenance history and its effect on long-term energy performance

- Compatibility with future regulatory requirements

For complex properties — period buildings, mixed-use assets, or those in flood-risk zones — this expanded scope demands a higher level of expertise and a more sophisticated reporting framework. Working with chartered surveyors in London who understand both RICS ESG standards and lender-specific requirements is no longer optional; it is a prerequisite for a successful transaction.

How Valuation Resilience Factors in 2026 Building Surveys Shape Lender Approvals

The term "valuation resilience" refers to a property's ability to maintain or grow its assessed value under changing regulatory, environmental, and market conditions. In 2026, energy performance has become the single most influential resilience factor in lender assessments.

The EPC Rating Threshold Problem

Most major UK lenders now apply informal or formal minimum EPC thresholds as part of their lending criteria. Properties rated F or G face the highest hurdles, but even D-rated properties are attracting increased scrutiny as lenders model future regulatory risk. The anticipated government requirement for rental properties to achieve a minimum EPC C rating — and the broader trajectory toward stricter standards — means lenders are pricing in retrofit costs even before any formal regulation takes effect [8].

Properties failing to meet updated energy standards face measurable valuation discounts due to anticipated retrofit costs and potential regulatory penalties [8]. A surveyor's role is to quantify these costs accurately so that lenders can adjust their loan-to-value calculations accordingly.

The Green Premium Effect

The inverse of the energy penalty is the green premium. Research confirms that buildings with green certifications command rental premiums of 6-11% and sale price premiums of up to 25% compared to non-certified counterparts [3]. This premium is not simply a market sentiment effect — it reflects genuine reductions in operational costs, lower risk of regulatory non-compliance, and stronger tenant demand.

For lenders, a green premium translates directly into reduced default risk. A property that commands higher rents or resale values provides better collateral security. This is why lenders are not merely avoiding poor performers — they are actively incentivising energy-efficient properties through preferential loan terms, lower interest rates, and higher LTV ratios.

| EPC Rating | Typical Lender Stance (2026) | Valuation Impact |

|---|---|---|

| A-B | Preferred; green mortgage products available | Premium of up to 25% |

| C | Standard acceptance threshold | Neutral to slight premium |

| D | Increased scrutiny; retrofit cost modelling required | Neutral to slight discount |

| E | Conditional acceptance; retrofit plan required | Discount of 5-12% |

| F-G | High rejection risk; specialist lending only | Discount of 15%+ |

Climate Risk as a Valuation Factor

Energy performance does not exist in isolation. Lenders in 2026 are also factoring in climate risks — flood exposure, subsidence risk, and overheating potential — as components of overall valuation resilience [5]. Properties with documented flood resilience measures can see valuation discounts reduced from 16% to as low as 4% compared to unprotected properties [5].

This means a building survey supporting a lender application must now integrate Environment Agency flood maps, local drainage data, and evidence of any flood-proofing measures. For properties in areas such as the Thames floodplain or low-lying coastal zones, this assessment can be the difference between approval and rejection.

The best London property valuation guide provides useful context on how these risk factors are weighed in urban valuations, particularly for properties where flood and overheating risks intersect with heritage constraints.

Advanced Survey Practices Supporting Valuation Resilience Factors in 2026

The expansion of what lenders expect from building surveys has driven a parallel evolution in survey methodology. The days of a visual inspection and a handwritten report are long gone for any property where lender approval is at stake.

Digital Tools Now Standard in Level 3 Surveys

Building surveys now routinely incorporate advanced digital tools, including thermal imaging and 3D modelling, to provide detailed assessments of a property's energy performance [7]. These technologies serve a dual purpose: they identify defects that would be invisible to the naked eye, and they generate quantified data that lenders can use directly in their risk models.

Thermal imaging reveals heat loss through walls, roofs, and floors — identifying insulation failures, cold bridges, and air leakage points that directly affect EPC ratings. A thermal survey can also detect moisture ingress before it becomes visible damp, which is particularly relevant for older UK properties.

3D modelling and BIM (Building Information Modelling) allow surveyors to map a building's energy profile in three dimensions, identifying where retrofit interventions would deliver the greatest efficiency gains. For lenders, this translates into more accurate retrofit cost estimates and a clearer picture of the investment required to bring a property to compliance.

For complex or older properties, a structural survey in London that incorporates these digital tools provides the depth of analysis that modern lender requirements demand.

Mandatory Property Condition Assessments

From August 2026, Fannie Mae requires comprehensive property condition assessments — including energy performance evaluations — for all condominium projects with more than 10 units [4]. While this is a US regulatory development, it reflects a global direction of travel that UK lenders are tracking closely. UK commercial lenders are increasingly adopting equivalent requirements for multi-unit residential and commercial assets.

For commercial properties, a commercial building survey in London now typically includes energy performance assessment as a standard component, rather than an optional add-on. This reflects both lender requirements and the growing importance of GRESB scores for institutional investors [6].

Maintenance Records and Long-Term Performance

Lenders are not only interested in a property's current energy performance — they want evidence of how that performance has been maintained over time. A building with a good EPC rating achieved through recent cosmetic improvements is treated differently from one with a consistent maintenance history that demonstrates sustained energy efficiency.

Surveyors are therefore increasingly requesting and reviewing:

- Boiler and heating system service records

- Roof and external envelope maintenance logs

- Records of any energy efficiency improvements and their dates

- Utility consumption data where available

This maintenance-focused approach aligns with the RICS ESG standards requirement to assess long-term viability, not just current condition [2]. A schedule of condition report can provide a baseline record that supports ongoing maintenance documentation and future lender assessments.

Practical Implications for Property Owners, Buyers, and Developers

Understanding the valuation resilience factors in 2026 building surveys: assessing energy standards for lender approvals is not just an academic exercise. It has direct financial consequences for anyone buying, selling, or developing property in the current market.

For Buyers

Buyers should commission a Level 3 building survey — the most comprehensive survey type — for any property where energy performance is uncertain or where the building is older, larger, or more complex. A standard homebuyer report will not provide the depth of energy assessment that lenders increasingly require. Understanding the difference between survey types is important; the homebuyer report vs building survey comparison explains when each is appropriate.

Buyers should also request a copy of the property's current EPC and compare it against the lender's minimum threshold before proceeding. If the rating falls short, commissioning an independent energy assessment alongside the survey will provide the retrofit cost data needed to negotiate on price or plan improvements.

For Sellers and Developers

Properties that cannot demonstrate energy resilience face a shrinking pool of lenders and buyers. Proactive investment in energy improvements — insulation, glazing upgrades, heat pump installation, solar panels — before marketing a property can significantly reduce the risk of valuation discounts and lender rejections.

For developers working on commercial assets, understanding how dilapidations interact with energy compliance obligations is increasingly important. A commercial dilapidation survey can identify where energy-related defects overlap with lease obligations, helping developers plan remediation works that satisfy both landlord and lender requirements.

For Leaseholders

Leaseholders face a particular challenge because energy improvements to the building fabric often require landlord consent and may be subject to lease restrictions. A licence to alter is typically required before a leaseholder can install insulation, replace windows, or make other structural energy improvements. Understanding this process early — ideally before purchasing a leasehold property — can prevent costly delays when lender approval depends on planned energy upgrades.

Key Actions for 2026

- Commission a Level 3 building survey with explicit energy performance assessment for any property where lender approval is required.

- Request thermal imaging as part of the survey scope for older or poorly insulated properties.

- Obtain retrofit cost estimates from the survey report and factor these into purchase price negotiations.

- Review flood risk data alongside EPC ratings — both now influence lender valuations.

- Maintain comprehensive records of all energy improvements and maintenance works.

- Engage an RICS-registered valuer who is familiar with the 2026 ESG valuation standards for formal Red Book valuations.

For formal valuations that must satisfy lender requirements, working with RICS registered valuers in London ensures that the valuation methodology aligns with current RICS ESG standards and lender expectations.

Conclusion

The convergence of RICS ESG standards, lender ESG frameworks, and rising retrofit costs has made energy performance a non-negotiable component of every building survey intended to support lender approval. Valuation resilience factors in 2026 building surveys — encompassing EPC ratings, climate risk, maintenance history, and retrofit cost modelling — are now as important as structural condition in determining whether a property secures financing and at what terms.

Actionable next steps for anyone navigating this landscape:

- Engage a qualified chartered surveyor experienced in RICS ESG standards before committing to any property purchase or refinancing.

- Treat the EPC rating as a financial instrument, not a compliance document — understand what it means for your lender's risk appetite.

- Invest in thermal imaging and detailed energy assessments for older or complex properties, even if not strictly required by the lender.

- Document all energy improvements and maintenance works systematically, as lenders increasingly request this evidence.

- Factor climate risk — particularly flood and overheating exposure — into your pre-purchase due diligence alongside energy performance.

The market is rewarding energy resilience with premium valuations and preferred lending terms. Properties that cannot demonstrate this resilience face a growing financial penalty. The building survey is now the primary instrument through which this resilience is assessed, quantified, and communicated to lenders — making the quality and scope of that survey more consequential than ever.

References

[1] Valuation Resilience Factors Assessing Energy Standards And Maintenance For Lender Decisions In 2026 – https://princesurveyors.co.uk/blog/valuation-resilience-factors-assessing-energy-standards-and-maintenance-for-lender-decisions-in-2026/?utm_source=openai

[2] Rics Sustainability Report 2025 Valuation Frameworks For Energy Efficiency Epc Ratings And Long Term Property Viability In 2026 – https://wimbledonsurveyors.com/rics-sustainability-report-2025-valuation-frameworks-for-energy-efficiency-epc-ratings-and-long-term-property-viability-in-2026/?utm_source=openai

[3] Building Resilience Integrating Esg And Climate Readiness In Real Estate – https://www.lewissilkin.com/en/our-thinking/the-collective/insights/2026/03/04/building-resilience-integrating-esg-and-climate-readiness-in-real-estate?utm_source=openai

[4] Property Condition Assessments As Standard Upfront Requirements How 2026 Lending Reforms Will Transform Building Survey Practices – https://wimbledonsurveyors.com/property-condition-assessments-as-standard-upfront-requirements-how-2026-lending-reforms-will-transform-building-survey-practices/?utm_source=openai

[5] Valuation Impacts Of Spring 2026 Flood Events Integrating Ea Flood Maps Into Level 3 Building Surveys – https://kingstonsurveyors.com/valuation-impacts-of-spring-2026-flood-events-integrating-ea-flood-maps-into-level-3-building-surveys/?utm_source=openai

[6] Understanding The New Gresb Real Estate Lender Assessment – https://perspectives.se.com/sustainability/understanding-the-new-gresb-real-estate-lender-assessment?utm_source=openai

[7] Current Trends In Building Surveying Whats Changing In 2026 – https://www.asg-consulting.co.uk/learning-and-resources/current-trends-in-building-surveying-whats-changing-in-2026?utm_source=openai

[8] Valuing Properties Under Stabilising National Prices Rics Techniques For Q1 2026 House Price Net Balance Of 10 – https://manchestersurveyors.com/valuing-properties-under-stabilising-national-prices-rics-techniques-for-q1-2026-house-price-net-balance-of-10/?utm_source=openai